FISV - Fiserv: Still Attractively Priced

2023-03-14 09:21:46 ET

Summary

- Fiserv is now trading near its 52-week high.

- Clover has significant potential and should continue to be the main growth driver in the future.

- Latest earnings demonstrated solid growth across the board and the guidance was also excellent.

- The current valuation remains discounted on a historical basis.

- I rate the company as a buy.

Investment Thesis

Fiserv ( FISV ) has been an outlier in the past year. Unlike most companies that struggled significantly, it performed very well and is now trading near its 52-week high. The company sees huge opportunities in Clover which should continue to be a strong growth driver moving forward. Despite facing macro headwinds, its latest earnings were impressive with solid growth on both the top and the bottom line. Shares are up nearly 20% in the past few months but the current valuation still look discounted, as multiples are below peers and its own historical average. I believe there are still decent upside potentials and I rate the company as a buy.

Clover Is A Growth Driver

Fiserv is a leading financial technology service company based in the US. The company through its subsidiaries provides solutions for POS (point-of-sale), mobile payment, omnichannel commerce, business management, payment processing, etc. Its customer includes some of the largest multinational companies such as Google ( GOOG ) and Microsoft ( MSFT ).

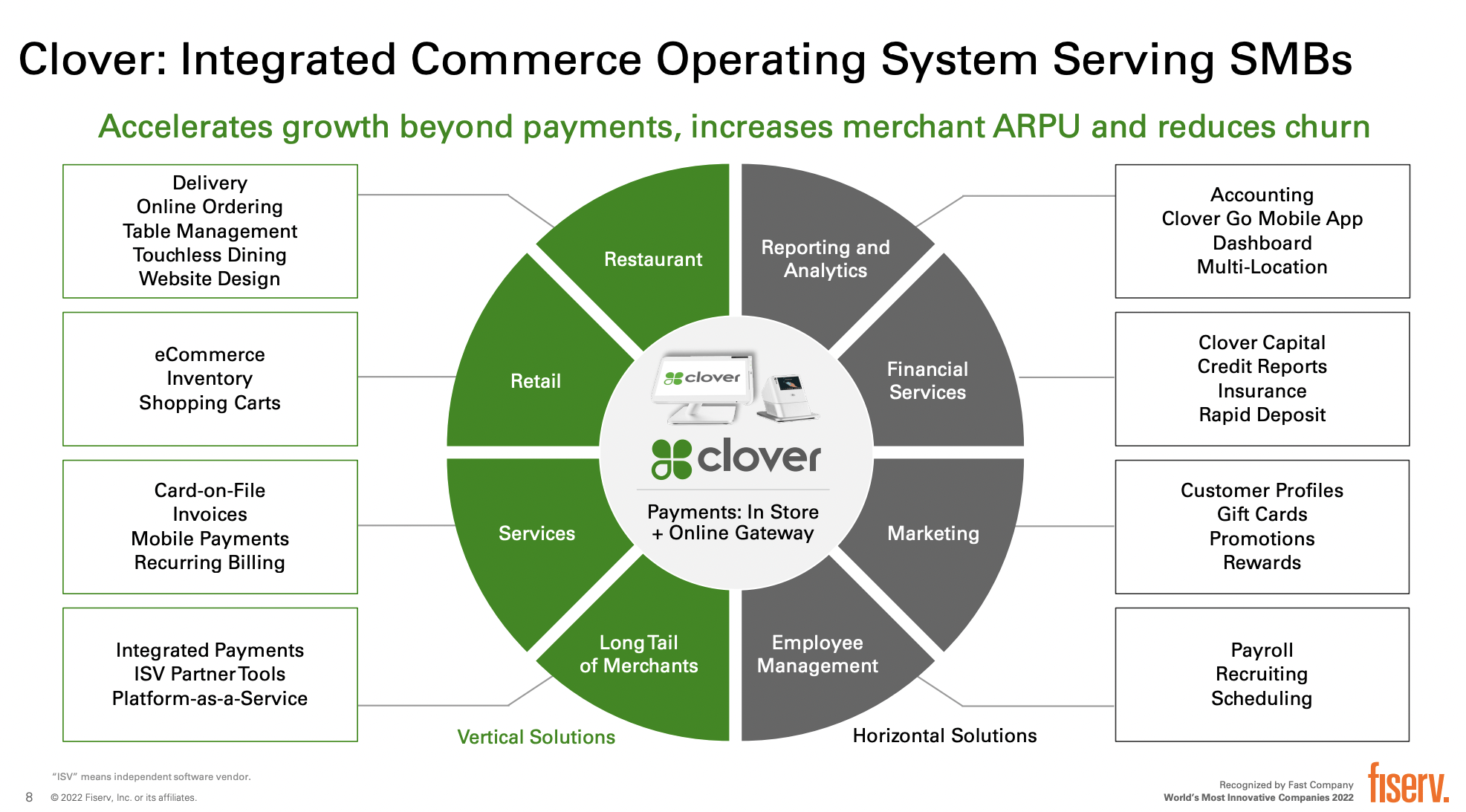

A lot of people have heard of Fiserv but may not know about Clover. It was acquired alongside the First Data acquisition that happened in mid-2019. I believe it is a valuable subsidiary with massive potential that should continue to drive growth for the company moving forward. Clover is an all?in?one commerce operating system that provides payment processing and business management solutions to SMBs (small-medium businesses).

{kind=link}

Clover allows businesses to accept payments easily through different channels such as card readers, POS, and e-commerce. It also offers other features such as reporting, inventory management, employee management, rewards programs, and more. Clover has been winning over customers as it is much more scalable and convenient compared to legacy operating systems, which vastly improves operating efficiency.

The opportunity for POS is huge and growing rapidly, as the adoption of digital payments continues to increase. More and more companies are also embracing an omni-channel strategy after the pandemic. According to Fortune Business Insights , the TAM (total addressable market) of POS is forecasted to grow from $25.2 billion in 2022 to $70.8 billion in 2029, representing a strong CAGR (compounded annual growth rate) of 15.9%. I believe Clover is well-positioned to benefit from the market expansion and should continue to see solid growth.

Q4 Earnings

Fiserv announced its fourth-quarter earnings last month and the results are outstanding, despite facing macro headwinds.

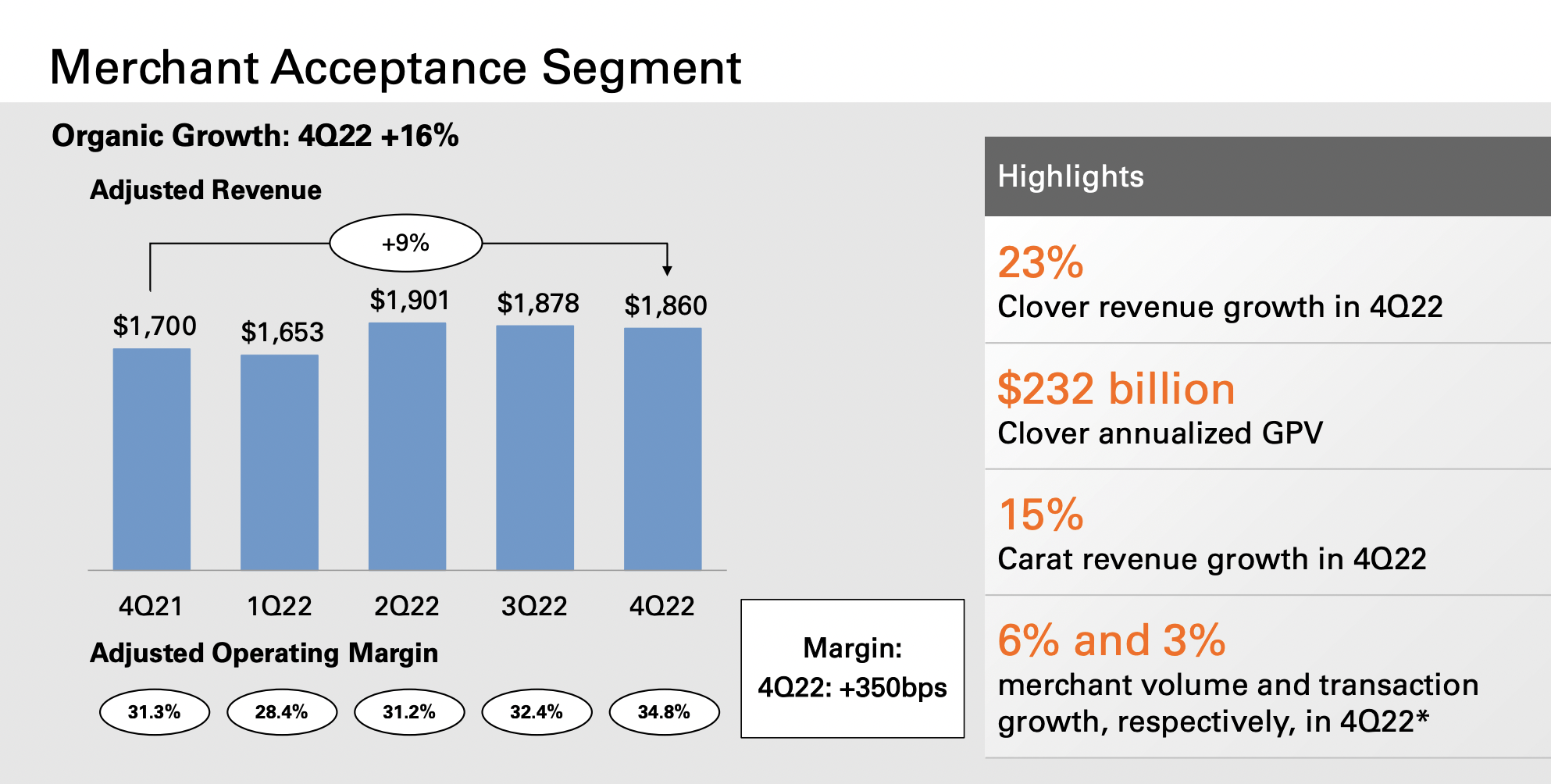

The company reported revenue of $4.63 billion, up 9% YoY (year over year) compared to $4.26 billion. The Merchant Acceptance segment grew 9% from $1.7 billion to $1.86 billion. The Payments and Network segment grew 8% from $1.54 billion to $1.67 billion. The Financial Technology segment increased by 7% from $771 million to $823 million. Clover continues to be the highlight of the quarter, with revenue growing 23% YoY. The growth is driven by both higher payment volume and active merchant count, which increased by 16% and 9% respectively. The average revenue per merchant grew by 12%.

{kind=link}

The bottom line was also impressive thanks to strong operating leverage. Despite revenue being up 9%, costs of revenue declined 10% YoY from $2.2 billion to $1.98 billion. This resulted in gross profit increasing 28.6% YoY from $2.1 billion to $2.7 billion. SG&A (selling, general and administrative) expenses also dipped slightly from $1.52 billion to $1.5 billion. The adjusted net income was $1.22 billion compared to $1.04 billion, up 17.3% YoY. The adjusted net income margin increased 190 basis points from 24.4% to 26.3%. The adjusted EPS was $1.91 compared to $1.57, up 22% YoY.

Even though the economy seems to be weakening, the company still initiated upbeat guidance for FY23. It expects revenue growth to be between 7% to 9% and adjusted EPS growth to be between 12% to 14%.

Investor Takeaway

Fiserv's latest earnings were excellent as Clover led revenue higher while improved operating leverage boosted the bottom line. The guidance was also surprisingly strong with very little slowdown in both the top and the bottom line. The opportunity for Clover remains huge and should continue to fuel growth. The company's valuation is still compelling despite trading near 52-week highs. It is currently trading at an EV/EBITDA ratio of just 13.3x which is pretty cheap on a historical basis(I am using the EV/EBITDA ratio as it takes the debt into account). This represents a significant discount of 32.8% compared to its own 5-year historical average of 19.8x. The company continues to execute and expects double digits EPS growth for the year, which should warrant it with a higher multiple. Considering its growth and valuation, I believe there is still meaningful upside and I rate Fiserv stock as a buy.

For further details see:

Fiserv: Still Attractively Priced