FLJP - FLJP: Slight Concern Over BoJ Pivot

2023-11-20 11:35:41 ET

Summary

- Weak Japan GDP data and a weak Yen are seeming to allay concerns around a BoJ pivot.

- But higher BoJ rates could be incoming, which could shock global markets, and especially the Japanese market.

- Despite these concerns, Japan continues to look attractive, especially if it can outlast other countries' rate hiking cycles and avoid a pivot while seeing the Yen eventually restored.

- But the weak Yen has been a price paid by the Japanese and it's hurting quite a lot of companies quite badly, as well as consumers.

The Franklin FTSE Japan ETF ( FLJP ) is a large-cap and mid-cap value-weighted Japan ETF. There are two key issues at play. Japan GDP data is weak, but also the inflation is substantially imported and they are suffering on a weak Yen. Will the policy pivot? It's not as simple as a weak economy means it won't. Higher rates may be incoming, and that would be a pretty big shock to global markets, as well as the Japanese market. Probably not a good day. Otherwise, Japan continues to look attractive, especially if it can outlast other countries' rate hiking cycles.

FLJP Breakdown

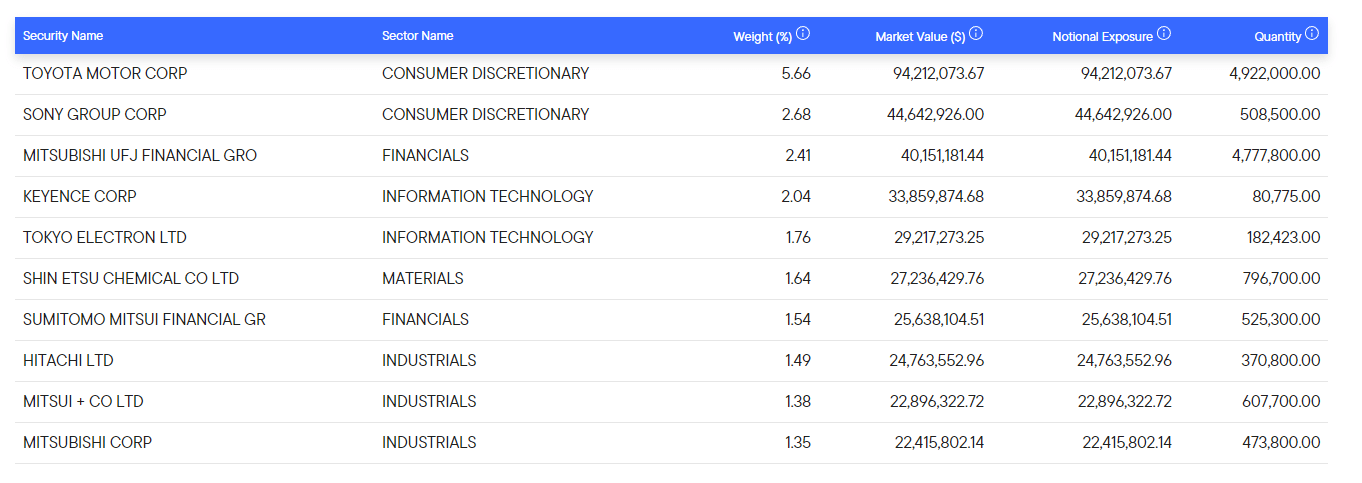

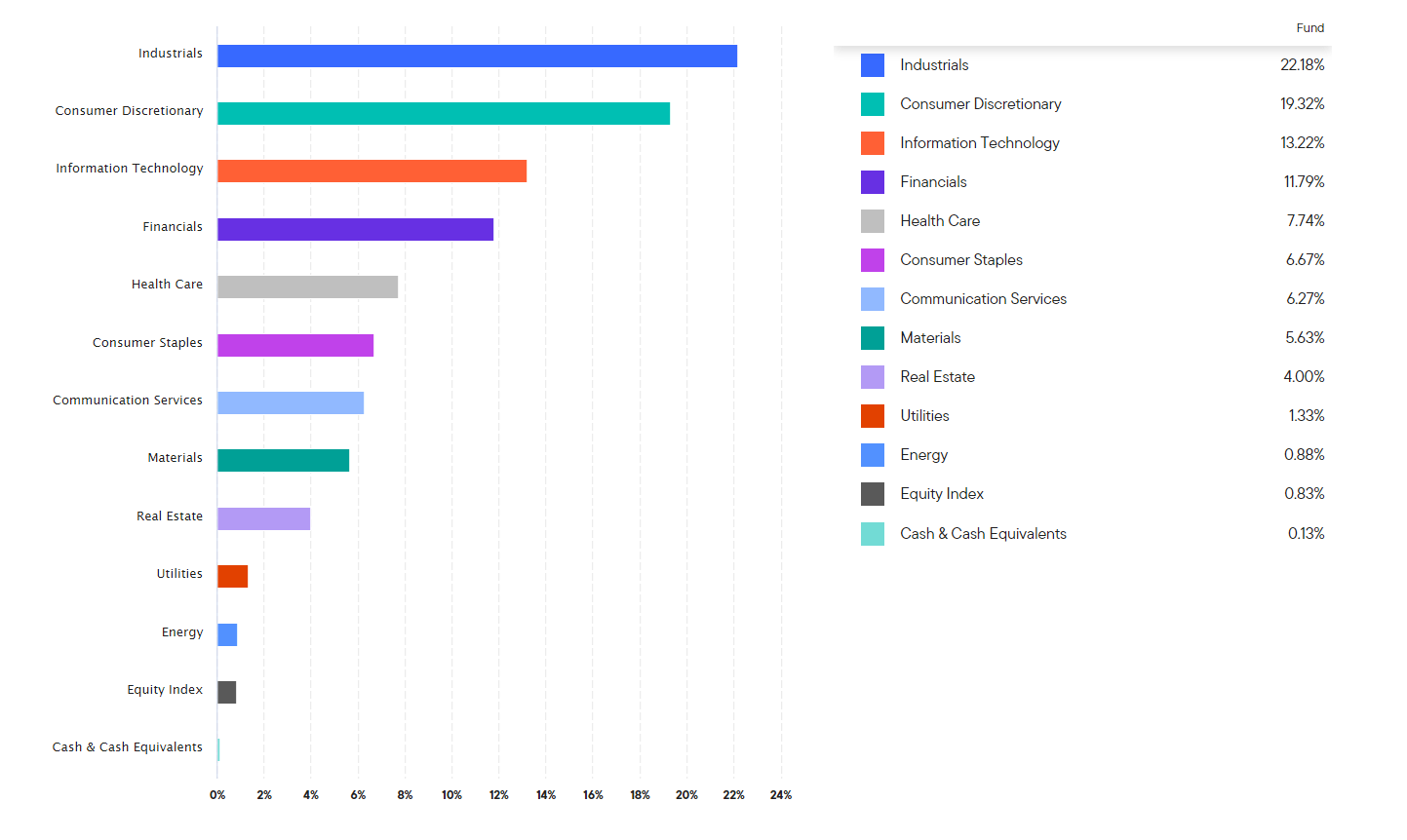

First, establishing that FLJP has a lot of large cap and mid-cap exposure with a value-weighted tendency.

{kind=link}

One key data point is that the expense ratio is 0.09% which is actually really low, considering that ETFs with foreign equities tend to be a bit more expensive.

Another thing to note are the sectoral exposures which are a reflection of the structure of the Japanese markets.

{kind=link}

A lot of industrial exposures and consumer discretionary, associated with the substantial machinery and automotive industries in Japan.

Bottom Line

GDP was under pressure in Japan reflecting the overall performance of Japan's businesses over the last couple of months. GDP actually contracted .

Consumer spending looked solid, especially domestic consumption, over the summer, while imports fell as a consequence of weaker terms of trade due to the weaker Yen: expected.

But now, there is continued flatness in consumer spending, and CAPEX has fallen quite unattractively driving declines. For consumers, despite the shunto wage increases, there hasn't really been any consequent increases in spending. This money has evidently been saved rather than spent. For producers, they are very worried about the prospects of their major trading partners, including China, and believe the outlook is actually quite gloomy in the West too. While Europe has already proven weak, the US hasn't yet there is still reticence and we've seen this universally across our Japan coverage.

The economics of Japanese companies has declined too, which is the concrete reason why CAPEX is falling. A lot of this is on the back of the Yen weakness and quite a lot of imported inflation in manufacturing. Automotive parts, but also machine parts in general, have been hard to get a hold of. Poor terms of trade on dollar denominated currencies like oil that have also inflated are another source of concern for industrial investments.

Japan has been a bit of a haven in terms of trading, IPOs and other capital markets activity. This is all thanks to the accommodative stance of the BoJ. Moreover, there has been a lot of leverage in pair trading shorts of Japanese bonds while taking proceeds to go long US Treasuries. Together, these factors lead to quite a ways to fall if the BoJ decides to pivot on policy. Global markets will be rattled by a more competitive BoJ rate. The Yen would appreciate, which is in some ways helpful for the importing industries, but automotive in Japan would not benefit, especially as they've been able to push share thanks to a weak Yen and the UAW strikes in the US. Also, any change away from ultra-loose policy would not be well-received by Japanese markets, which tend to be very sensitive and rational about cost of capital effects, especially since its markets are generally quite capitally intensive, and are sensitive in that regard.

The question is what the BoJ will do? While a weaker economy should be a sign that loose policy will have to continue until more underlying inflation can be achieved, something that Japan has uniquely lacked on the global stage, the Yen being weak also creates issues for a more virtuous inflation cycle in Japan. Terms of trade for oil are very bad, as well as other imports. While Japan is a net exporter, and a weak Yen has helped them grow in other periods this year, if foreign partners are anyway cutting back on spending, the benefits of a new tact may become more evident to Governor Ueda, who has been itching to get Japan away from ultra-loose policy.

The risks of a pivot are still low, but with so many companies in our coverage suffering on a weak Yen, we're not sure it's so clear cut. FLJP and other Japanese ETFs would not like a change in policy. It would not be good for equities.

For further details see:

FLJP: Slight Concern Over BoJ Pivot