FISV - Following Up On My Best Idea: NCR Corporation

Summary

- On November 19, 2022, the SA Pro team interviewed me and published my thoughts on Value investing.

- I shared NCR Corporation as my best idea (I expressly was considering risk/reward). NCR shares opened for trading at $21.67 and are up 24.9% since publication.

- As NCR gets ready to report its Q4 FY 2022 results, I write to share my fairly comprehensive synthesizing work on the company. I hope this helps people in their research process.

On November 19, 2022, I was graciously asked by the SA Pro team to do an interview on value investing. As I really like the Pro team, and really like a lot of editors, here on SA, for that matter, I was happy to participate. Rightly so, the last question in their monthly interview series tends to be please share your best current idea. At the time of publication, Saturday November 19, 2022, I shared NCR Corporation ( NCR ), as my then best idea. On the morning of November 21, 2022, as November 19, 2022 was a Saturday, NCR opened the trading day at $21.67 per share.

As of yesterday's closing price, January 26, 2023, NCR shares closed at $27.06. So far, so good, with a respectable 24.9% total return. That said, as I only shared a shorter version of the thesis within the interview, today, I write to share the full length version. NCR Corporation is set to report its Q4 FY 2022 results on February 7, 2023, after the bell, and I figured it might be helpful for readers as well as current NCR longs to have the full and comprehensive version, as an input or supplement to their research process.

Incidentally, and before we get in the weeds on NCR, I just wanted to note that on May 15, 2021, I also did an interview series with the SA Pro team. Back then, I shared Houghton Mifflin Harcourt ( HMHC ) as my best idea. I believe HMHC shares were then trading around $10.50 to $11.50ish (I don't have the precise data as the company was bought out, so I can't find the time and sales data). As it turns out, HMHC was bought out by private equity for $21 per share, with the deal closing in April 2022. So we are talking about a good outcome and almost a 100% return in less than one year.

NCR Corporation - Full Length Version

(And please note the only sections that were updated, for today's piece, are the share price and market capitalization calculations, in order to reflect current (and this case higher) share price).

Also, for perspective, these pieces were originally published on my marketplace service in late October 2022. I blended the two pieces into one piece.

Please see below:

{kind=link}

In today's piece, I'm writing up NCR Corporation. My goal is address the following four items:

- What do they do?

- How do they make money?

- What are the drivers?

- Why is this mis-priced?

1) What Do They Do?

In case you haven't been paying attention to national events, there has been an acute labor shortage throughout many segments of the U.S. economy. With a recent national unemployment rate of only 3.5%, it is really hard to attract, retain, and manage work forces. And at the lower end of the job spectrum, in the lower skilled jobs, jobs that offer lower pay and limited advanced opportunities, it is really hard to find and keep good people. Moreover, the Great Resignation movement, with Covid acting as the big catalyst to the movement, has really exacerbated this acute shortage of workers on the front-lines and especially in relatively lower skilled jobs. In addition, as an employer, even if you somehow get to a fully staffed position, wage inflation and employee turnover has been a big thorn in your side.

Lo and behold, NCR Corp. is one of the companies at the forefront of solving this pressing business need through its comprehensive hardware and software solutions.

The company plays a big role in the automation.

The company has a strong presence in banking, retail, point of sales for restaurants, payment solutions, and telecom & technology.

{kind=link}

If you have been to Walmart ( WMT ) lately, a grocery store such as Kroger ( KR ) or Albertsons ( ACI ), a drug store such as CVS Health ( CVS ) or Walgreens ( WBA ), or any number of major retailers that have high traffic, and a check out lines that can get bottlenecked, chances are you've seen or used an NCR self check out machine.

As an aside, on the banking side, our local Bank of America ( BAC ) has frequently been closed since Covid due entirely to low staffing. When they are actually open, hours have been cut back. And when I inquired about it, the branch manager said they can't find enough people to staff the branches, so on those days, the only option is either digital banking or using the advanced ATM machines, inside the branch lobby.

{kind=link}

Given the acute labor shortage, very high wage inflation, and high employee turnover at the lower end of the economic spectrum, NCR operates in a business that has strong tailwinds, and these are multi-year secular growth trends. In other words, this isn't a flash in a pan, Covid induced one time event.

Over the past few years, the company has greatly improved the quality of its offering and has added a lot of value to its customers. In late 2018, they set their 2024 goals. After already coming very close to achieving them, management raised the bar and set new 2026 goals.

See below:

In order to provide long-term value to all our stakeholders, we set complementary business goals and financial strategies. NCR is continuing its transition to become a software platform and payments company with a shift to a higher level of recurring revenue. Our business goal is to be a leading enterprise technology provider that runs stores, restaurants and self-directed banking through our software platform and our NCR-as-a-Service solutions. By helping our customers run stores, restaurants and banks better, they have more time to create customer experiences that drive lasting success. In late 2018, we set five-year strategic goals, originally set as 2024 targets. These goals include transitioning our revenue mix so that 80 percent of our total revenue is comprised of software and services, 60 percent of our total revenue is comprised of recurring revenue, and our adjusted EBITDA margin rate increases to 20 percent. Since we were near achieving those goals, in late 2021, we established aspirational five-year goals for 2026, which include annual recurring revenue of 80 percent by 2026, annual non-GAAP diluted earnings per share ("non-GAAP EPS")(1) growth of 15 percent, and annual free cash flow(1) of $1 billion in 2026.

(Source: NCR Earnings Press Release)

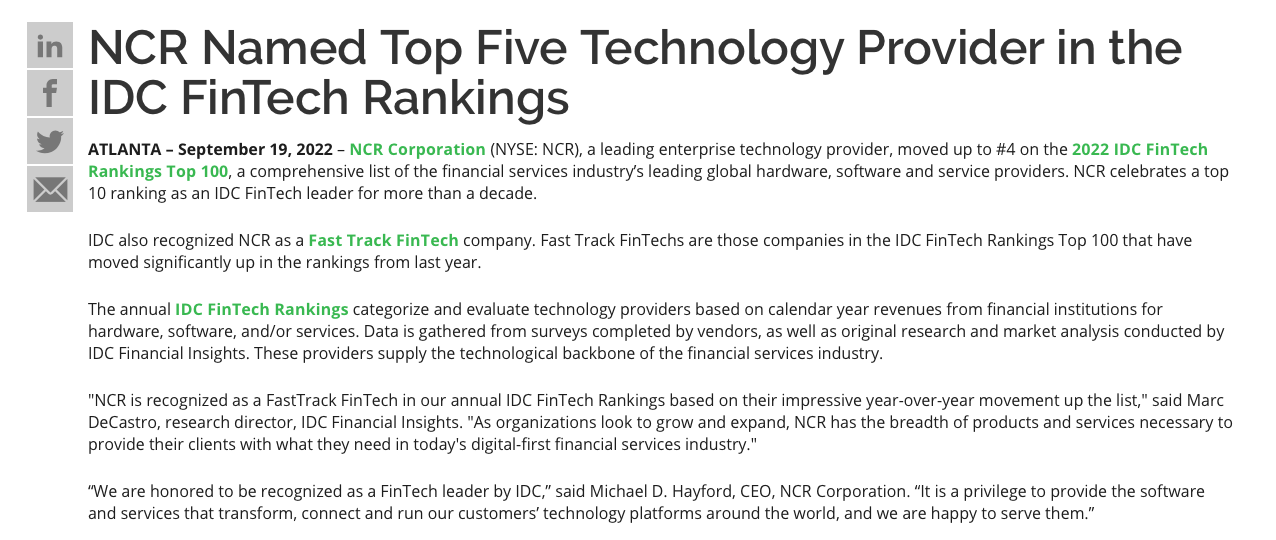

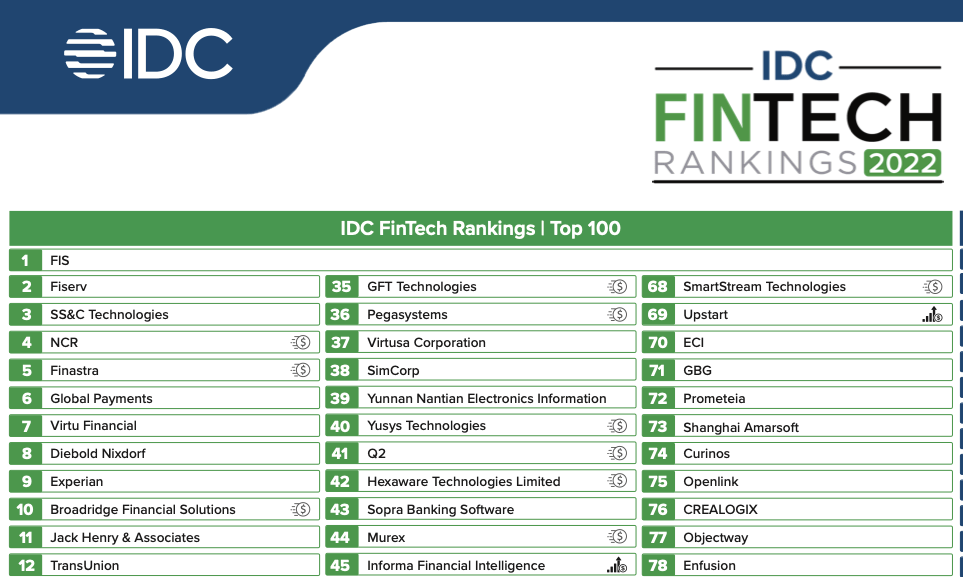

Moreover, the company's product innovations and customer satisfaction scores have improved, and recently, NCR was recognized as the #4 ranked IDC FinTech Rankings.

See here:

{kind=link}

In case you're wondering, look at who's on the list. We are talking about really well runs businesses, such as Fidelity National Information Services, Inc. ( FIS ), Fiserv, Inc. ( FISV ), SS&C Technologies ( SSNC ), and Global Payments ( GPN ). These companies all have larger to much larger market capitalization compared to NCR, and sure enough, NCR is still in the top four!

{kind=link}

Also, see here, found in FY 2021 NCR's 10-K .

Focus on our customers. We encourage our employees to treat every customer as if they are our only customer. If we provide better service and better quality products than our competitors, it is our belief that our customers will likely buy more from NCR. We are increasingly becoming active, strategic advisors to our clients, helping them retool and reinvent their business, and this is reflected in a significant increase in our Net Promoter Score from 14 in 2018 to 48 in 2021. We believe this focus has or will lead to increased access to higher level customer contacts, earlier entrance into the sales cycles, and additional opportunities for upselling and cross-selling as a software- and services- led company.

2) How Do They Make Money? (And Valuation)

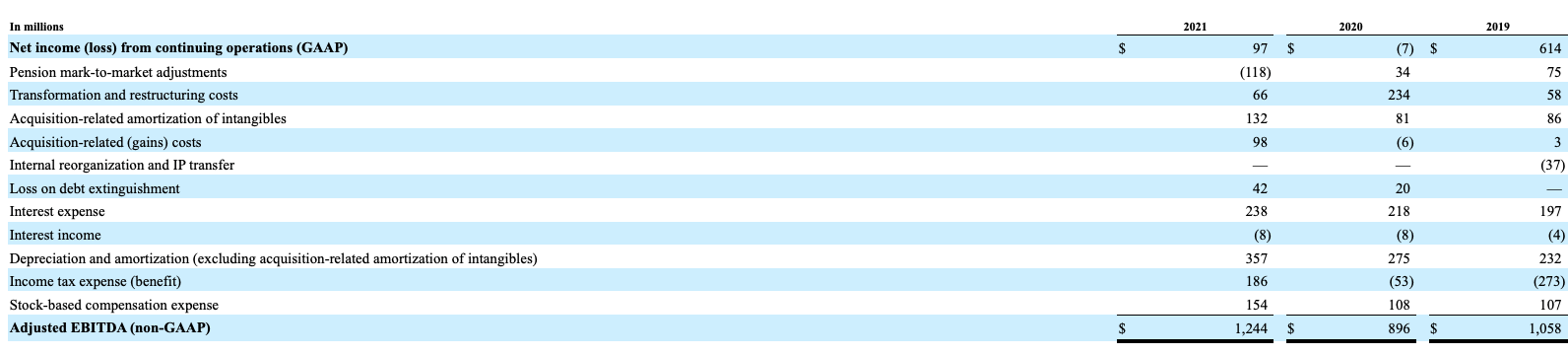

As we don't have full year FY 2022 numbers until February 7, 2023, enclosed below, so you can get for full year annual numbers, is NCR's annual Adjusted EBITDA, free cash flow, and segment data, over the past three full fiscal years.

Adj. EBITDA Details ($1.244 billion in FY 2021)

{kind=link}

Free Cash Flow ($460 million in FY 2021)

{kind=link}

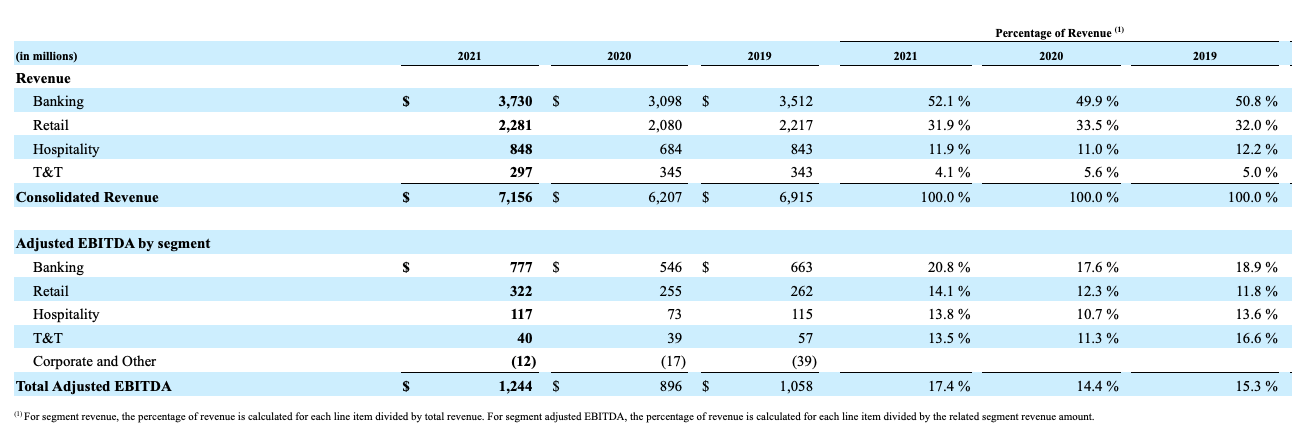

By Segment

This is a very good business, with 17.4% Adj. EBITDA margins, in FY 2021. In 2021, the lion share of revenue and Adj. EBITDA is driven by the Banking and Retail segments. Banking accounted for 62.5% of Adj. EBITDA dollars at a 20.8% Adj. EBITDA margin. Retail made up 25.9% of gross margin dollars and at a 14.1% gross margin.

{kind=link}

Valuation

NCR has 136.9 million shares outstanding x a $27.06 per share stock price (as of January 26, 2023), which translates to a $3.7 billion market capitalization. As of June 30, 2022, the company has $5.3 billion of net debt. So if you add the two figures, we are looking at an enterprise value of $9 billion.

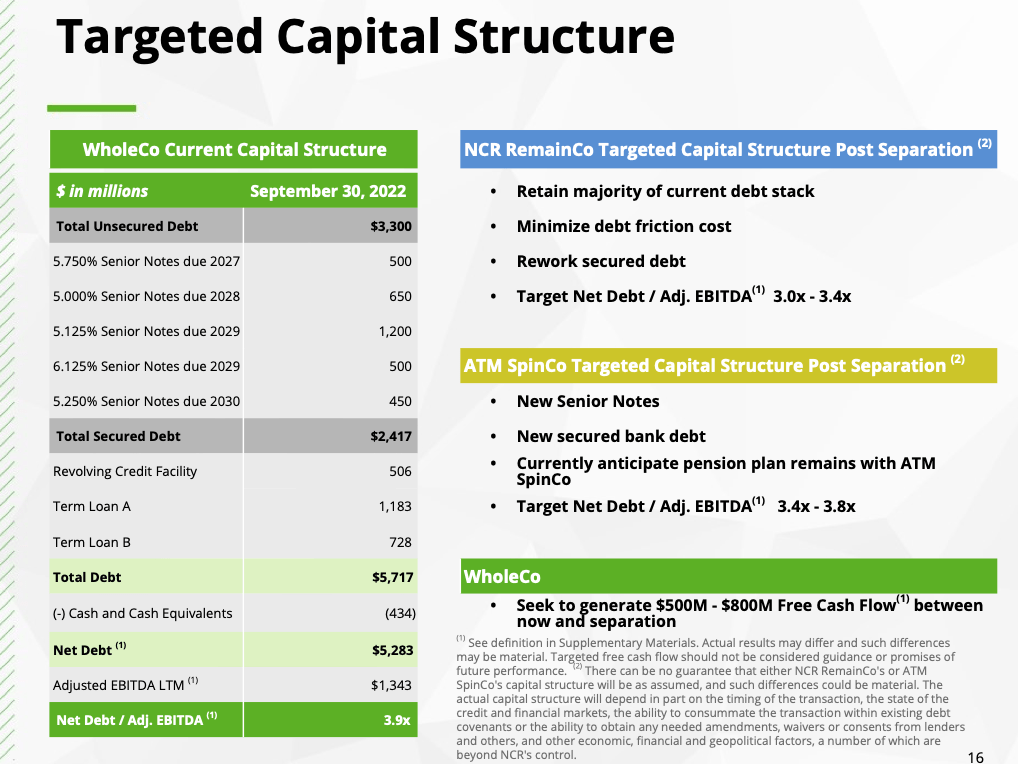

- $9 billion enterprise value / $1.244 billion (FY 2021 Adj. EBITDA) = 7.23X

- $9 billion enterprise value / $1.4 billion (FY 2022 Adj. EBITDA guidance - which excludes currency) = 6.43X

Enclosed below is an excerpt from NCR's Q3 FY 2022 conference call (October 25, 2022).

This slide also shows our net debt to adjusted EBITDA metric with a leverage ratio of 3.9, down slightly from the prior quarter due to higher profitability. We remain well within our debt covenants. And finally, before I hand it back to Mike, some thoughts on guidance for Q4.

We provided guided ranges back in April as follows, approximately $8 billion of revenue, $1.4 billion to $1.5 billion of adjusted EBITDA and $2.70 to $3.20 of EPS. Since that guidance was provided, the anticipated impact of all of the exogenous shocks, including war, component cost, freight, fuel, other inflation, interest rates and now currency has more than doubled from our April estimate of $150 million.

That said, adjusting for relief from the currency impact that could not have been anticipated at the time, we believe that our adjusted results still fall well within those ranges. More specific to Q4, we expect to deliver a fourth quarter that is very similar to Q3 from both a revenue and profit perspective accompanied by significant improvement in free cash flow.

3) What Are The Drivers?

If you closely follow my work, I spent a lot of time synthesizing conference calls. Often, and at a minimum, I will read the three most recent conferences call, sometime twice, as there are many nuances and lot of information to synthesize. In the case of NCR, I did exactly that.

If you closely read the conference calls, here are most of the big issues:

- Omicron dinged transaction volumes in Q1

- Supply chain issues (chip and component availability) pushed out orders and led to breakeven gross margins, in some spots, on the hardware side

- Higher Interest Rates (NCR had to pay interest on the cash it borrows to supply and run its ATM fleets)

- FX headwinds dinged Q2 FY 2022 revenue and EBITDA by $50 million and $15 million respectively

Note the extreme price gouging in certain areas of the semi-conductor space. Check out this excerpt from NCR's April 26, 2022 Q1 FY 2022 conference call !:

I'll just give you a couple of examples that we dealt with, chips that we were buying at $41 in the second half of the year are now in the open market that we have to go to for almost $2,900 . We had chips that were -- we were paying $0.42 for our power supplies, I should say, that we're now paying $114 for. So I will tell you that we wanted to meet customer demand, we did that. We missed on the escalation and acceleration of costs from our backlog in the third quarter to what we are building and delivering at the end of the first quarter.

To mitigate the big inflation, management has targeted $400 million in offsets ($200 million in the form of price increases and $200 million of cost improvements).

So I think -- we also talked about trying to have $200 million of cost action and $200 million of pricing actions. I'll tell you that the pricing actions are all in place because of the long lead time on some of our products. So there won't be -- we can't impact that from here. I think whether we get to $200 million now will be heavily dependent upon our ability to convert those price increases to hold those price increases in a competitive environment. We're doing okay, so far. And on the cost side, we're probably halfway to where we need to be. We've got some work to do in the second half of the year. And Owen and I are working on that. Hope that frames it for you anyway.

(Source: July 27, 2022 Q2 FY 2022 Conference Call)

Now the persistent 40 year high inflation and chronic supply chain issues have muddied the waters as they dinged Q1 FY 2022 results.

However, if you synthesize the conference call, the underlying demand for the product is solid and the company is taking smart actions to traverse this rugged terrain.

Solid Demand (excerpts from the Q2 FY 2022 conference call)

Exhibit A

NCR Q2 FY 2022 Conference Call NCR Q2 FY 2022 Conference Call

{kind=link}

Exhibit B

NCR Q2 FY 2022 Conference Call

{kind=link}

Exhibit C

Follow up, with additional information....

NCR Q2 FY 2022 Conference Call

(Other Nuances - Mitigating Actions And Price Increases Are 3 to 4 months Lagged)

See here:

Fourth, we are beginning to see the supply chain impacts easing, meaning the component costs and transportation costs have not worsened in the second quarter. But more importantly, our engineering and procurement teams have adjusted by designing alternative components and certifying more sources to begin reducing the impact.

(Source: Q2 FY 2022 Conference Call)

See here:

There are operational adjustments we can make to offset some of the higher interest rates, such as reducing the amount of cash in the ATMs, as well as passing through contractual protections triggered by higher rates. The obvious offset to cost inflation are price increases and cost productivity. We're actively working on both. While we've been implementing price increases beginning all the way back in July of '21, we have not yet seen a full realization of those increases. Hardware sold from backlog and longer-term contracts with only annual escalators caused a lag in price realization that is particularly painful in an environment of runaway inflation.

(Source: Q1 FY 2022 Conference Call)

4) Why Is This Mis-priced?

On February 8, 2022, NCR announced strong Q4 FY 2021 results and announced a strategic review process.

As you can see, the next day, the stock shot up on the news, with nearly 6 million shares changing hands.

{kind=link}

From February 8th - July 2022, there were multiple reports of interested suitors.

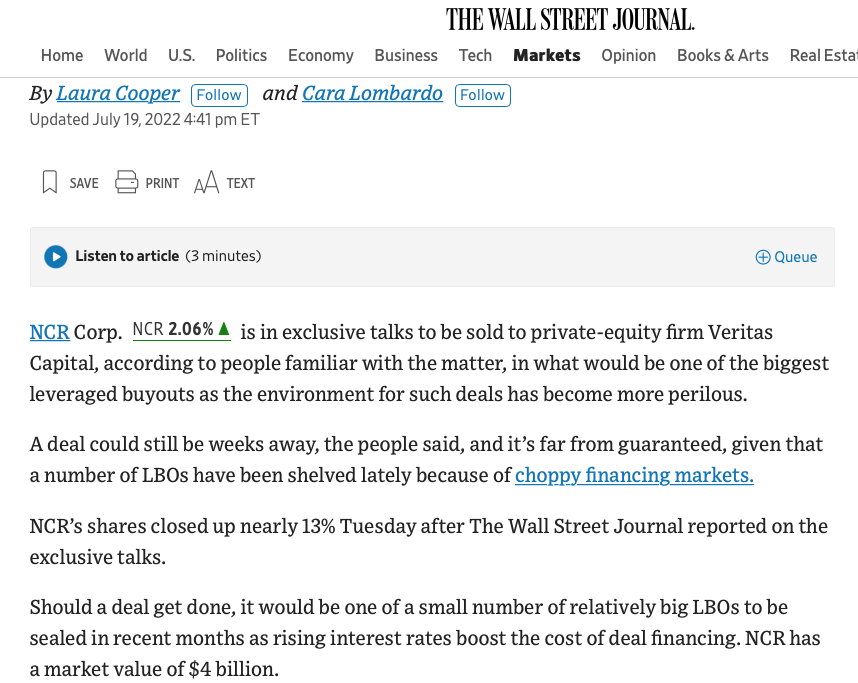

On July 19, 2022, the WSJ reported NCR was in exclusive talks with Veritas Capital to sell the business.

{kind=link}

To get across the finish line, NCR and Veritas needed to agree on price and Veritas needed to secure financing.

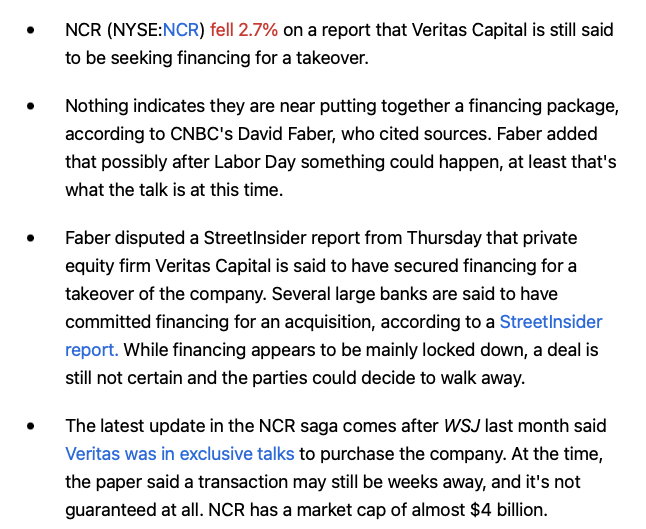

In August 2022, it was reported that Veritas had secured financing. However, soon after, CNBC's David Faber said financing wasn't secured.

{kind=link}

On September 15, 2022, after the bell, NCR announced that its Strategic Review had been tabled, and the current plan was to split the company in two, to highlight the faster growing segments.

The next day, NCR shared got dinged, dropping from $29.11 to $23.20, with north of 13 million shares changing hands. Basically, all the fast money, M&A types left in droves. Soon after, encore selling occurred and NCR's stock traded as low as $18.06, on October 13, 2022.

Other Things To Consider

1) On June 21, 2021, NCR closed its Cardtronics plc merger, for a total price of $2.47 billion. Cardtronics owns the Allpoints debit network, which accelerated NCR's SaaS strategic focus and aligns well with NCR's core banking businesses.

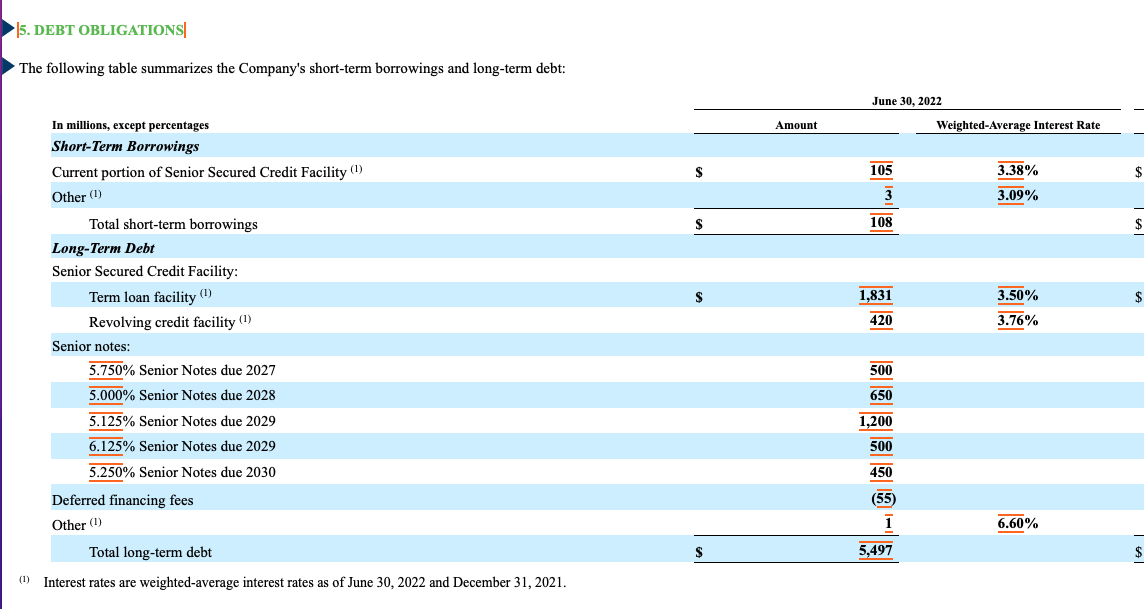

2) NCR's long-term debt is largely termed out, and at favorable fixed rates.

{kind=link}

Bonus Material

Now that I provided a fairly comprehensive piece that (hopefully) answered:

- What do they do?

- How do they make money?

- What are the drivers?

- Why is this mis-priced?

Enclosed below please find my second note, on NCR's Q3 FY 2022 results. Again, today's piece is designed to help readers enhance their research process when it comes to NCR.

Synthesizing NCR's Q3 FY 2022 Results

On October 25, 2022, I listened to NCR Corp.'s Q3 FY 2022 conference call. In today's piece, I will synthesize the quarter and conference call.

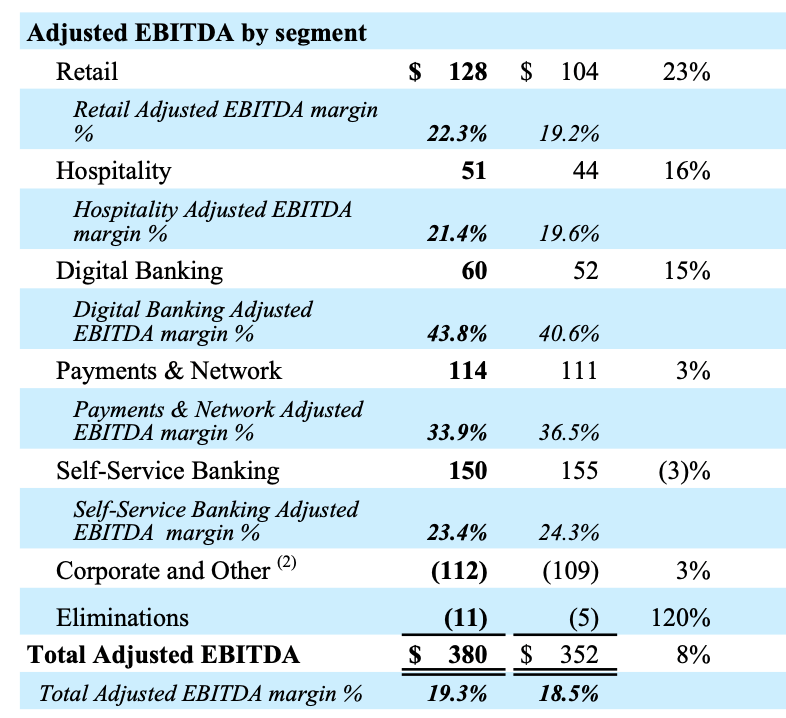

Executive Summary: NCR delivered a fantastic Q3 FY 2022 quarter! Across the board, the trajectory of its revenue growth (+8% on constant currency basis), KPIs, and EBITDA margins (19.3%) were fantastic, despite a very difficult macro backdrop. Excluding FX, Adj. EBITDA was up 15%! The only weakness was free cash flow (which I will explain in excruciating detail).

Also, if you are into nuance, the absolute level of Adj. EBITDA margins, in the Payment and Networks segment, got dinged by the higher cost of cash rentals (which flows through cost of goods sold) to run its vast fleet of managed ATM networks (see the excerpt).

Payments and Networks adjusted EBITDA increased 3% year-over-year and 7% when adjusting for FX. Beneficial revenue mix and cost leverage were offset by a significant increase in our cost to rent cash for ATM fleet, which is directly tied to interest rates. The cost of cash rental goes through EBITDA is at cost of goods. Adjusted EBITDA margin rate was 34%, down from the prior year due to those higher cash rental costs.

And see here: (higher interest rates led to $80 million in cash rental costs)

Yeah. So on the interest side, we expected back then to have about $25 million of pressure across the year. It turned out to be closer to 80. So we've had $80 million of pressure on interest rates that go through the P&L, through EBITDA at the Payments business, much higher than we anticipated. That absorbed a lot of the range, if you will, the 1.4 to 1.5.

(Source: Q3 FY 2022 Conference Call)

Note the nice Adj. EBITDA growth, really across the board.

NCR Q3 FY 2022 Earnings Report

{kind=link}

Free Cash Flow Was The Only Negative

Back in late July 2022, when NCR reported its Q2 FY 2022 results and held its conference call, management updated and refined its guidance. Guidance was updated to reflect: $8 billion in revenue, an Adj. EBITDA range of $1.4 billion to $1.5 billion, and $400 million of free cash (the original range, earlier in the year, was $400 million to $500 million).

So let's get in the weeds here.

Management is saying that Q4 FY 2022 free cash flow should only be about $200 million, and the would be and required incremental $200 million of free cash flow (from the Q2 FY 2022 guidance of $400 million in FY 2022) will get pushed to Q1 FY 2023.

Here is how they explained it on the call (please note - all excerpts are from the Q3 FY 2022 conference call).

Exhibit A:

First nine month working capital uses have been $150 million driven by higher DSO (days sales outstanding) and holding more inventory due to supply chain disruptions. Also, in Q3 FY 2022, they reduced payables by $80 million.

Days sales outstanding has increased 11 days versus the beginning of the year. Inventory days has increased another four days and the net impact of nearly seven days to the cash cycle has caused a timing impact of more than $150 million through the first three quarters of this year.

We also reduced payables in Q3 by nearly $80 million. In order to ensure improvement, I'm standing back up our cash control tower initiative that we used in 2020 to harvest most of this cash in Q4. The combination of working capital improvements, higher profitability and the lapse of the timing issue and compensation and benefits, we now anticipate $400 million of cash generation in the next two quarters with more than half of that occurring in Q4.

Exhibit B:

When they discussed the details of two company split, they noted and anticipate Q4 FY 2022 - FY 2023 free cash flow, cumulatively, to be $500 million to $800 million. In other words, they are suggesting they think the FY 2022 free cash flow shortfall could get caught up, in FY 2023. In other words, it isn't lost.

And finally, on the bottom right in green, we anticipate generating $500 million to $800 million of free cash flow between now and the separation that can be deployed to reduce overall leverage going into the split.

Exhibit C:

They are saying FX has dinged FY 2022 revenue by $262 million, Adj. EBITDA by $67 million, and impacted free cash flow by $115 million.

The - back to your question on currency. We now expect looking at FX rates today, currency to impact revenue by $262 million to impact EBITDA by $67 million and it impacts free cash flow by almost $115 million.

So when I talk about being in our side of our ranges of $1.4 billion to $1.5 billion on EBITDA or approximately $8 billion on revenue, I think you can see with relief, if you just do the math, I described Q3 to Q4, you add up where we are this year, if you add back those FX effects, we're well within those ranges trending toward the midpoint of some of them.

Exhibit D :

When pressed on a Q4 FY 2022 free cash flow figure, CFO, Tim Oliver, said $200 million. He explains the puts and takes and what caused the shift in free cash flow generation.

We've got $180 million of working capital use of cash this year. There was a year in which I thought we'd hold working capital relatively flat, $157 million used in AR and over - nearly $75 million of using inventory. Those folks who own those efforts to collect that cash tell me they can get that back. And so I expect to get at least $150 million of free cash flow out of working capital in the fourth quarter.

We'll also generate other cash in the quarter, I think we'll be north of $200 million, is my best guess. That means there's still another couple of hundred million dollars of cash that should have been generated this year that will likely harvest in Q1 of next year.

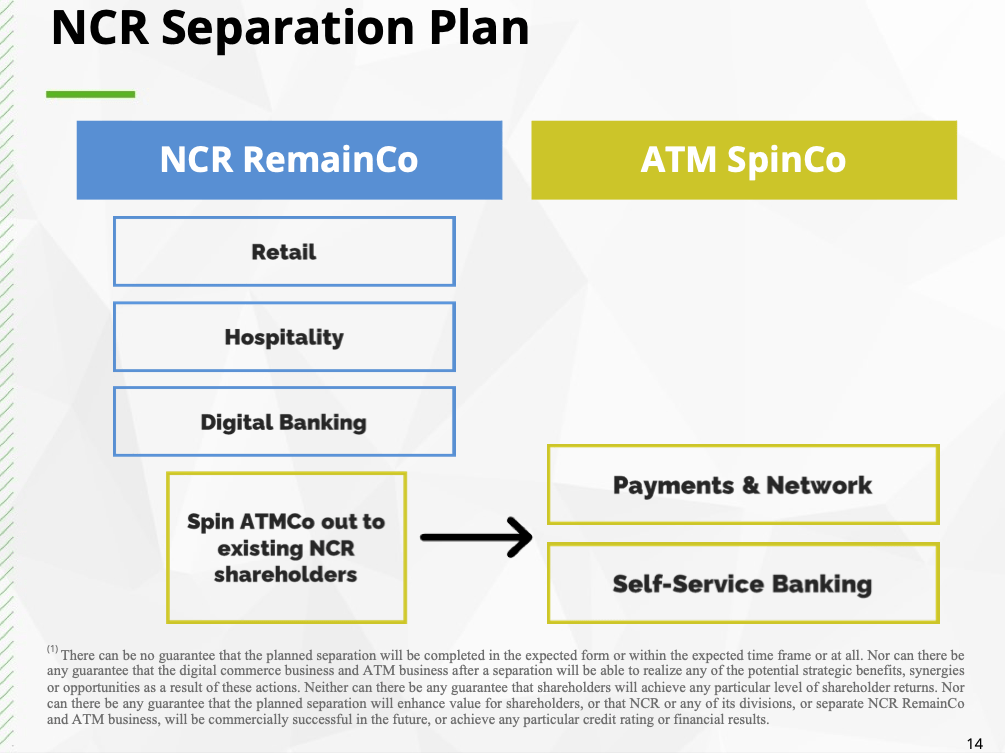

The Company Split, Via a tax-free spin-off (Targeted For The End of FY 2023)

As you might imagine, the company spent a lot of time discussing the split and tax free spin-off.

There is no sense reinventing the wheel here, so please see these three slides below.

The Two New Companies

{kind=link}

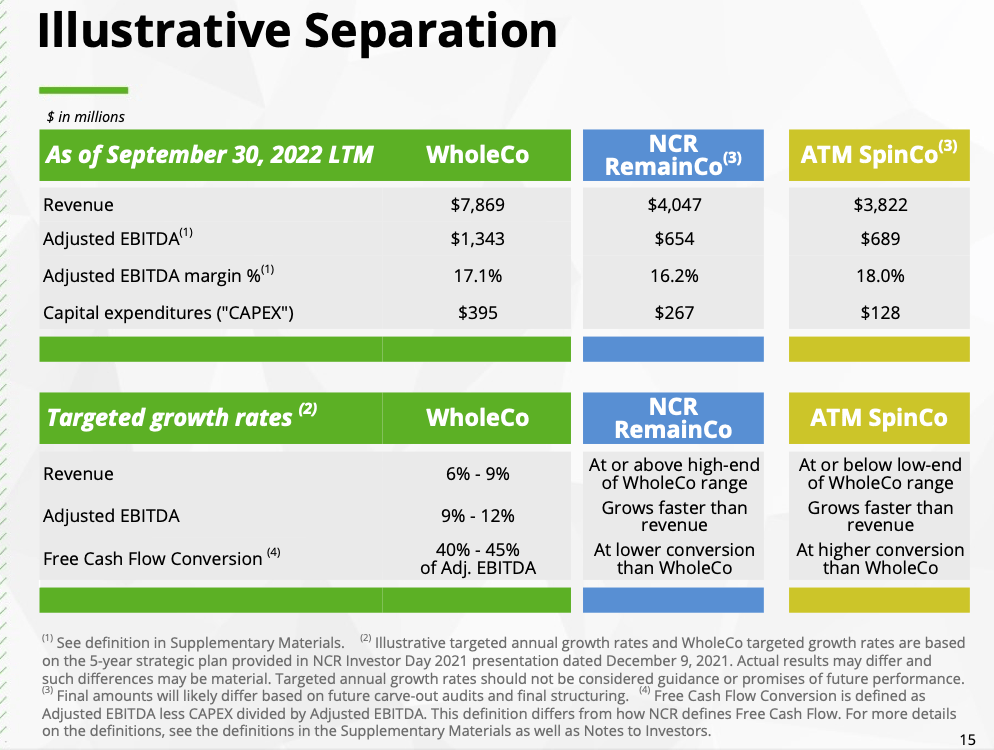

The Break Out Of The Financials and Growth Targets

{kind=link}

The Targeted Capital Structure

{kind=link}

Management Left The Door Open To Selling The Business

Please note - management left the door open to still selling the business or part of the company, if the deal terms were favorable.

See the section highlighted in bold.

In terms of leadership at each company, we have a deep bench of experienced leaders at NCR. We are working through the organizational structures. However, we intend to look internally for the management teams that will lead each company. We believe that this approach is the best path to unlock shareholder value but should alternative options become available in the future that could deliver superior value, such as a whole or partial company sale of NCR, the board remains open to considering alternative scenarios.

Buybacks

There were two references to buybacks:

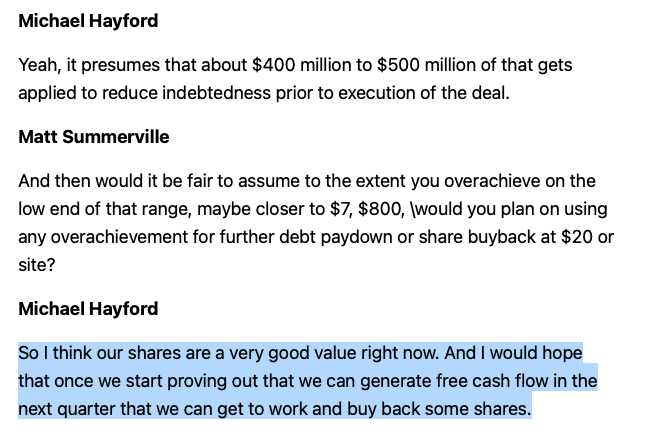

Exhibit E

Management noted their board approved repurchase authorization and balancing de-leveraging with share repurchases.

Third, we are focused on improving our cost structure. As Tim mentioned, we have identified efficiency cost actions to streamline our costs. Fourth, we expect to close out the year with a strong cash flow generation, as Tim referenced. And fifth, we expect - with the expected strong cash flow, we will continue to allocate capital to the highest return opportunities. We will balance the desire to delever with the opportunity to repurchase shares at attractive levels. As a reminder, we have a previously authorized share repurchase program that we can tap.

Exhibit F

Specifically, management tipped its hand, indicated that given the Q4 FY 2022 - FY 2023 free cash flow target of $500 million to $800 million, $400 million to $500 million would be earmarked for de-leveraging. This means that the remainder would be allocated towards stock repurchasing, holding everything else constant.

NCR Q3 FY 2022 Conference Call

{kind=link}

Putting It All Together

Although NCR shares have moved up 24.9% since the time of publication of my November 19, 2022 SA Pro interview, my six to twelve month NCR price target remains at $35.

Overall, Q3 FY 2022 was a fantastic operating quarter. The company is growing nicely and Adj. EBITDA margins and dollars are moving in the right direction despite an exceptionally tough macro backdrop and countless obstacles to maneuver.

Qualitatively, the company is delighting its customers and they had a number of nice new wins during Q4 FY 2022 (see appendix).

The only negative, and I provided excruciating details on that front, was free cash flow will only be $200 million in FY 2022 as opposed to $400 million. However, management believes much of that isn't lost, but simply pushed out into FY 2023.

On the positive front, the business is firing on all cylinders and they continue to take market share. Moreover, NCR's expansive list of customers' needs to manage and control its labor force and labor costs, in this highly constrained and inflation period. Therefore, NCR's software and products remain must have investments for its customers to effectively run their respective businesses.

Lastly, management left the door open to selling the business (in part or whole) and indicated that buybacks are a near term objective despite the lion's share of its Q4 FY 2022 - FY 2023 free cash flow (targeted at $500 million to $800 million) being earmarked to de-leveraging. If management gets comfortable with its (Q4 FY 2022 - FY 2023) free cash flow trends, meaning they think they will trend towards the upper end of the range, say $700 million to $800 million, this suggested $200 million to $300 million in buybacks.

In terms of tailwinds and headwinds, if the U.S. dollar weakens (and it has considerably since October 25, 2022), chip prices decline in price and become more readily available (they can carry less investment and have better hardware margins), and interest rates decline, all three of these things would act as big tailwinds. In terms of headwinds or uncertainty, the biggest risk is really the 2023 macro environment. We will learn more on this front, on February 7, 2023.

In closing, this is a great business and my price target remains at $35. I really hope sharing this comprehensive piece, with free site readers, helps people with their investment process. Lastly, given the nice move off the bottom, if non current NCR holders are contemplating a long position here, NCR call options are relatively cheap, given their low implied volatility (just an observation).

For further details see:

Following Up On My Best Idea: NCR Corporation