BABA - Forget Alibaba And Take A Look At Kaspi Instead

2023-05-12 10:41:54 ET

Summary

- In this article, I'm trying to prove that Kaspi stock has much more growth potential compared to Alibaba. A comparison I assume you've never seen before.

- What Alibaba failed to do - create a full ecosystem with financial solutions inside - Kaspi succeeded in doing. Kaspi's ecosystem yields better growth and margins.

- Kaspi occupies >41% of its market, and that share, if you look at the numbers, is only continuing to grow (unlike Alibaba's share in China).

- Alibaba's projected EPS growth is a CAGR of ~8.1% from 2023 to 2025. Kaspi's EPS grew 76.7% YoY in U.S. dollars. Both stocks have nearly the same P/Es.

- I don't recommend trying to catch another falling knife in BABA. Better buy what grows higher, costs about the same in terms of valuation, and has fewer geopolitical risks.

Introduction

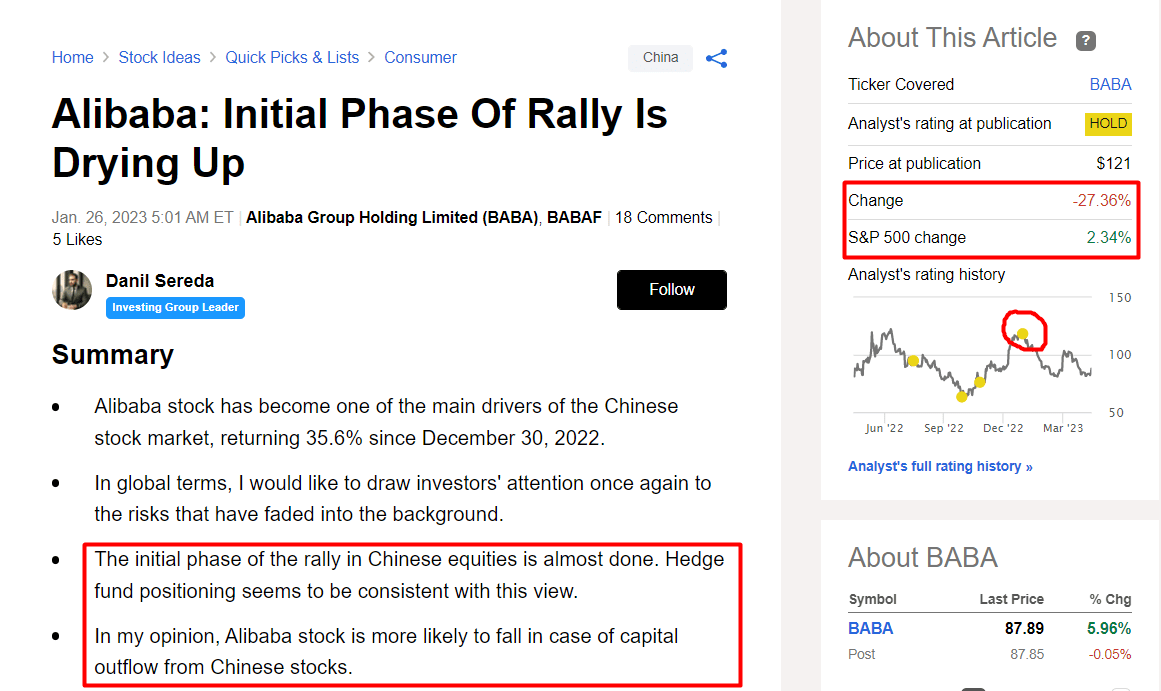

I've been writing about Alibaba Group Holding Ltd (BABA) (BABAF) stock here on Seeking Alpha since September 2021 when 1 ADR was trading for ~$150. I was bearish from the start and didn't change my rating to Neutral until December 2021 when it dropped to ~$113 per ADR. Since then, I've not changed my Neutral rating despite the continued downward momentum and attempts of BABA stock to rebound based on various catalysts and expectations. The last time I managed to warn SA readers of the impending correction in BABA stock right at the top of its another bear rally. Then I noticed that hedge funds were selling the rips in Chinese stocks on a massive scale:

Seeking Alpha, my latest article on BABA stock

{kind=link}

Today's article will be somewhat unusual in the context of my previous coverage because it'll be based on a comparison of BABA with an alternative that most readers aren't familiar with. Analysts usually compare Alibaba to Amazon ( AMZN ), eBay ( EBAY ) or JD.com ( JD ), and PDD Holdings ( PDD ), but I don't recall anyone on Seeking Alpha or elsewhere putting Alibaba Group Holding and this company side by side. Well, it's nice to be the first.

The company I'm talking about is called Kaspi.kz (KAKZF). Let's go in-depth together.

Business Models

Based on the recent announcement of a new organizational and governance structure, Alibaba Group Holding Limited should consist of 6 major business groups, each independently managed by its own CEO and board of directors:

- Cloud Intelligence Group: This group encompasses Alibaba's cloud computing, artificial intelligence [AI], DingTalk, and other related businesses. Daniel Zhang, who is also the Chairman and CEO of Alibaba Group, serves as the CEO of this group.

- Taobao Tmall Business Group: This group includes popular e-commerce platforms such as Taobao, Tmall, Taobao Deals, Taocaicai, and 1688.com, among others. Trudy Dai is the CEO of this group.

- Local Services Group: The Local Services Group comprises Amap, Ele.me, and other businesses focused on providing localized services. Yongfu Yu leads this group as the CEO.

- Global Digital Business Group: This group oversees various international digital businesses, including Lazada, AliExpress, Trendyol, Daraz, and Alibaba.com. Fan Jiang serves as the CEO of this group.

- Cainiao Smart Logistics: This group is responsible for Alibaba's logistics operations, ensuring efficient and smart delivery services. Lin Wan holds the position of CEO in this group.

- Digital Media and Entertainment Group: This group is engaged in digital media and entertainment ventures, including Youku and Alibaba Pictures. Luyuan Fan serves as the CEO of this group.

If you read my article " Alibaba's Asset Structure Is Another Reason To Stay Aside " you probably remember that the company's business structure used to look a little different. In its consolidated form, BABA consisted of operating 7 segments, with the units not related to e-commerce and logistics accounting for only about 15% of total revenue [Cloud + Digital Media + Innovation Initiatives]. In other words, by and large, the company was and still is [until the spin-off is done] an e-commerce company that operates various marketplaces and is responsible for the logistics of goods sold.

Okay, what about Kaspi?

Important note: Unfortunately, the OTC quote you see here isn't liquid - AIX (Kazakhstan Stock Exchange) and London Stock Exchange (ticker "80TE") have the most liquidity.

Kaspi.kz is a $16 billion market cap payments, marketplace, and fintech ecosystem that provides different services in the Republic of Kazakhstan primarily through an online mobile app. To date, it's not just a commercial bank as it was initially supposed to be - it's a full-fledged mobile super-app that combines many different features, which you'll learn about below. The company divides its activities into 3 segments:

| Segment |

| Description from the Kaspi's IR |

| Payments |

| The Payments Platform enables customers to pay for regular household needs, make purchases online and in-store, and make seamless online P2P Payments within and outside Kaspi Ecosystem, both in Kazakhstan and globally to any Mastercard or Visa card. |

| Marketplace |

| Our Marketplace Platform is positioned as the starting point and destination for customer shopping journeys via our Mobile App, website, and in-store. Customers come to our Marketplace to buy a broad selection of products from various merchants. |

| Fintech |

| Through the Fintech Platform, we enable our customers to access consumer financial products primarily online through Kaspi.kz Mobile App. Our technologically-advanced infrastructure allows us to make a high-quality credit decision in real-time, usually within seconds, which ensures a seamless customer experience |

Source: Taken from my previous article on Kaspi stock

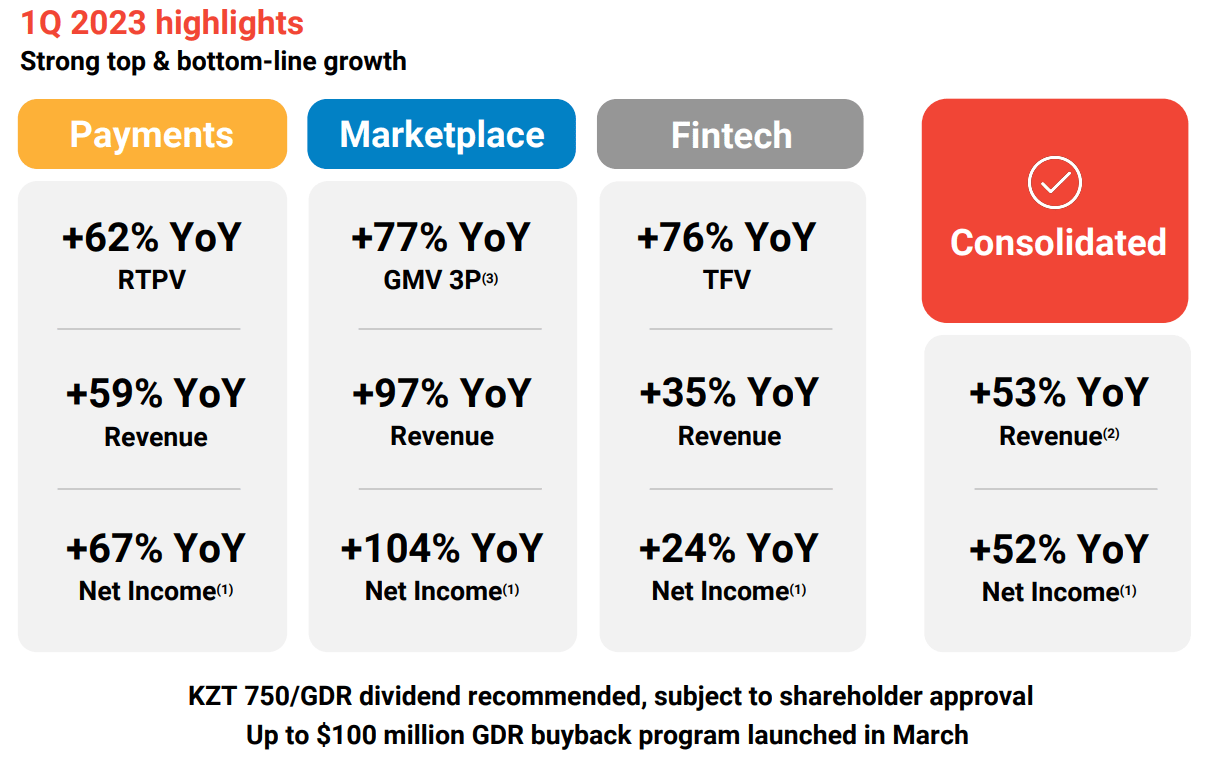

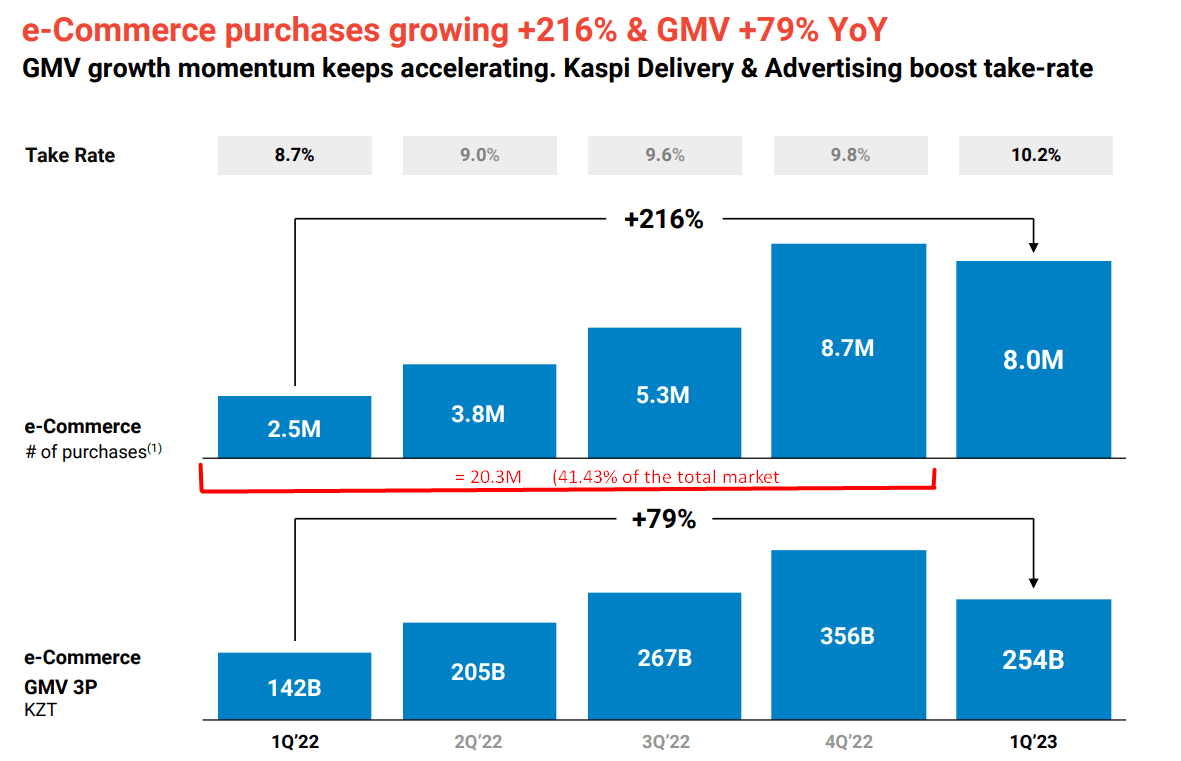

As the user base in the Marketplace segment continues to expand (6.1 million compared to 5.4 million in October 2022), there is also significant growth in the Fintech segment (5.7 million compared to 5.2 million). This growth is driven by the unique advantage that Kaspi offers its users as an officially registered commercial bank. Unlike Alibaba's customers, Kaspi's users have the ability to quickly and easily order goods on credit or in installments, thereby boosting both Fintech and Marketplace sales. We see this in the operational growth of the whole ecosystem in Q1 FY2023 :

{kind=link}

As we know, Alibaba also wanted to integrate financial services solutions [Alipay] into its ecosystem. Alipay was originally developed as a payment platform for Alibaba's e-commerce platforms, primarily to facilitate transactions on its online marketplace Taobao. Over time, Alipay evolved into a separate company - Ant Group. BABA doesn't directly own Ant, but it uses Alipay as the primary payment method on its platforms, and Ant Group benefits from Alibaba's e-commerce ecosystem by acting as a key financial services provider. The problem is that Alibaba's shareholders feel no impact from Alipay's operations, while Kaspi's shareholders gain an edge from the symbiotic relationship between its Fintech and Marketplace business units .

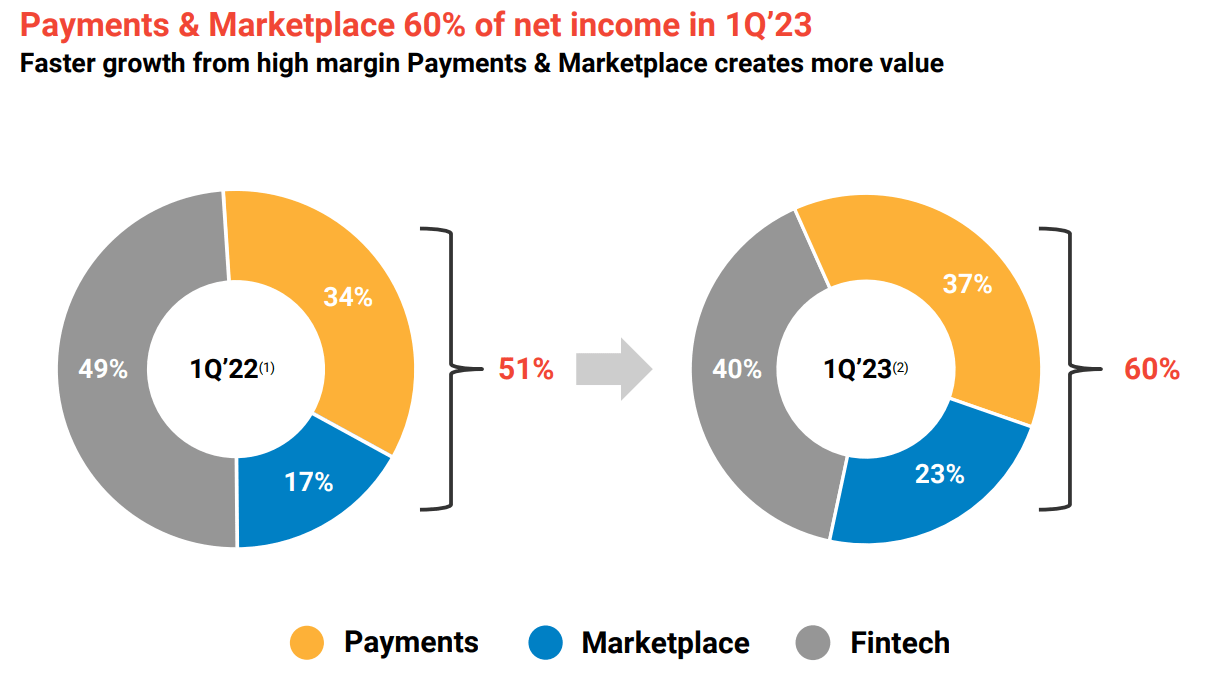

What Alibaba failed to do - create a full ecosystem with financial solutions inside - Kaspi succeeded in doing. Moreover, Kaspi initially started as an ordinary commercial bank, which made the transition to a marketplace, the share of which continues to grow year by year:

Kaspi's Q1 FY2023 IR materials

{kind=link}

In terms of operational efficiency, I think Kaspi has a much more sustainable business model - at least the company won't have to spin off anytime soon.

Addressable Markets

I think this is one of the most important issues for investors - the state of addressable markets. Alibaba is a true giant in its geographic market with a market cap of $227 billion and a GMV of ~8.32 trillion yuan (~$1.20 trillion) according to Statista . Total e-commerce sales in China recorded a CAGR of 17.7% from 2017 to 2021. By 2025, e-commerce platform users are expected to account for 83.9%, with an estimated user base of 1,230.4 million. The market for cross-border B2B e-commerce in China is expected to grow by 160% between 2021 and 2025. Mobile devices play a crucial role in this, with 75% of China's 1.6 billion mobile users conducting e-commerce transactions.

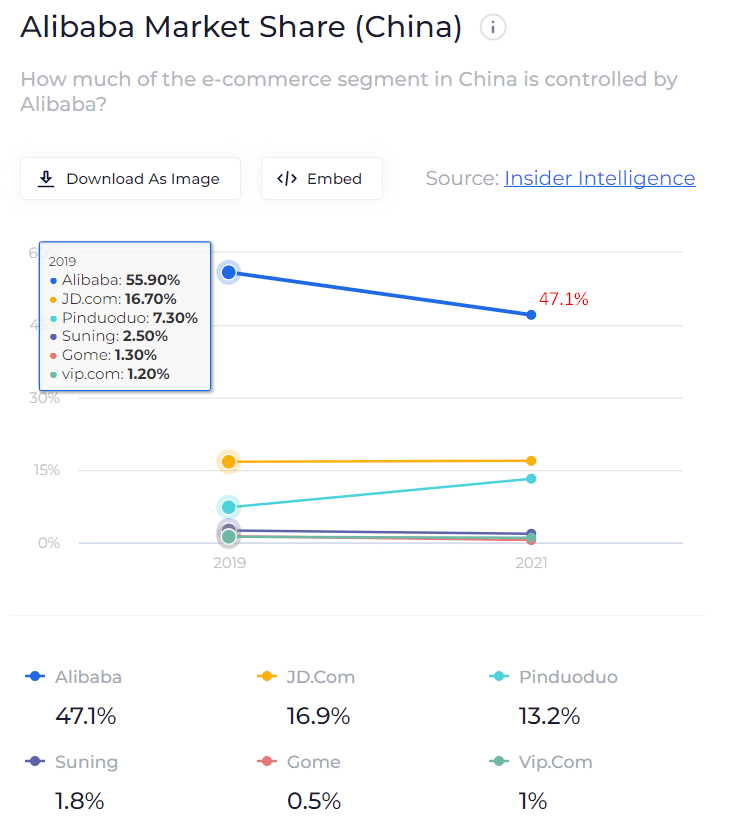

So China is indeed a very important and one of the fastest-growing e-commerce markets in the world. Alibaba Group has witnessed remarkable revenue growth, surpassing 850 billion yuan in FY2022, representing a more than 40-fold increase compared to a decade ago. The company has expanded its business both domestically and internationally, attracting millions of overseas consumers to its online shopping platforms and diversifying into cloud computing, logistics services, O2O customer services, and entertainment. However, Alibaba faces intensified competition from other players like Pinduoduo, Douyin, and Kuaishou, who have gained popularity through social commerce and short-video commerce. This is why Alibaba's market share is rapidly declining :

Wallstreetzen's data, author's notes

{kind=link}

Additionally, Alibaba has faced challenges related to unfavorable views of Chinese companies globally and regulatory scrutiny in China, including the suspension of Ant Group's IPO and investigations into Alibaba for potential antitrust violations.

What about Kaspi?

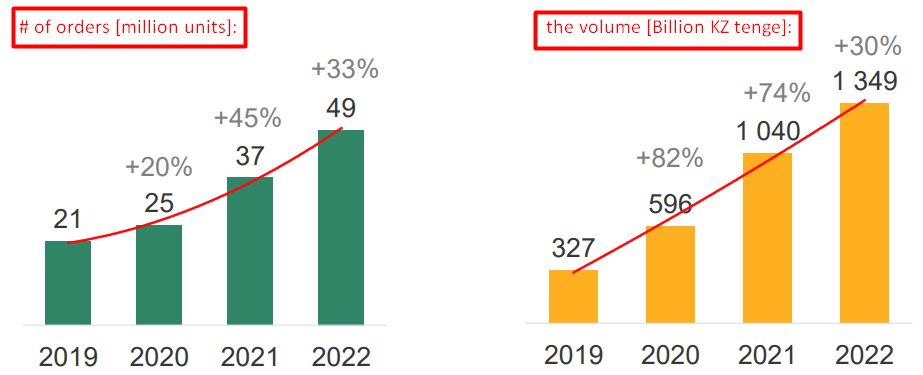

The Kazakh market is obviously many times smaller than the Chinese market - Kaspi's capitalization is also ~93% smaller than Alibaba's. However, the market growth dynamics are impressive:

PWC, Cross Insights, author's notes [proprietary source]

{kind=link}

Although the average check amount in the online sector decreased by 3% in FY2022 [YoY], there was a significant increase of 33% in the number of transactions - it helped the whole market to grow by 30% YoY in volumes and 33% in the number of orders. But what's left going forward?

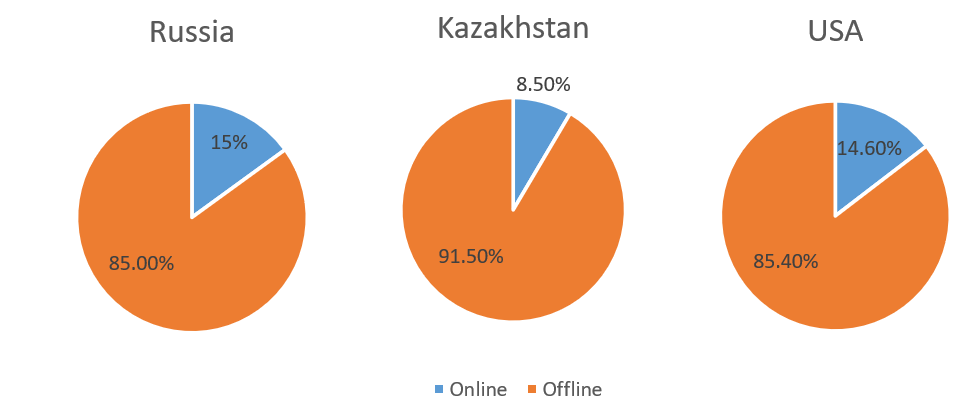

According to the study by Data Insights [proprietary source], the online channel's share in retail trade in Kazakhstan was around 1.5 times lower than in Russia and 1.7 times lower than in the USA [FY2022 data].

Author's work, based on Data Insight's data

{kind=link}

Thus, the size of the e-commerce market in Kazakhstan should almost double to match the market's conditions of its nearest northern neighbor [Russia] - these are huge volumes that Kaspi can get organically, as I calculate that the company occupies more than 41% of the total market, and that share, if you look at the numbers, is only continuing to grow (unlike Alibaba's share in China).

{kind=link}

I'll give a little insight. Recently, I attended a closed conference held by representatives from Bloomberg who came to the region where I now live and shared their vision of where the whole region and its individual countries are headed. Kazakhstan was on the list, and as one of the leading macroeconomists said at the conference, this country has one of the strongest economic growth forecasts for the coming years. The consequences of the Russian war against Ukraine have affected the Kazakh economy in two ways. First, the national currency [tenge] has weakened sharply due to geopolitical instability [ now fully recovered to the pre-war levels]. Second, a huge flow of political refugees poured into Kazakhstan - young, able-bodied men and their families who settled in very quickly, easily obtained the documents needed for employment, and are currently continuing to work and develop their host country's economy in large numbers. In a previous article on Kaspi, I wrote more extensively about this - how mobilization in Russia has become a strong tailwind for the company and its peer Freedom Holding ( FRHC ). However, this new labor force is not the only thing that has migrated to the country. As the Bloomberg macroeconomist said, Russian capital began to seek massive refuge in nearby countries, and Kazakhstan's established financial infrastructure became a good option for that.

From all of the above, I'd like to draw an interim conclusion: Yes, Alibaba's market is many times larger than Kaspi's, but the latter is gaining market share and seems to be able to hold on to it, while the former isn't. There are some objective reasons why it'll be easier for Kazakhstan's e-commerce market to grow at double-digit rates in the foreseeable future [5-10 years], outpacing the growth rates of the Chinese market. Therefore, Kaspi's growth potential looks much more optimistic than Alibaba's, given the strong competition in China and the excessive stringency of Xi Jinping's regulators.

Fundamentals And Valuation

Alibaba reported notable highlights in its FY2022 results. In the quarter ending December 31, 2022, the company achieved a 2% year-over-year revenue increase of RMB247,756 million (US$35,921 million). Income from operations saw a significant surge, rising 396% year-over-year to RMB35,031 million (US$5,079 million), driven by an RMB22,427 million decrease in impairment of goodwill within the Digital media and entertainment segment. Adjusted EBITA, a non-GAAP measure, rose by 16% year-over-year to RMB52,048 million (US$7,546 million). The company is set to report for the first 3 months of FY2023 on May 18, according to Seeking Alpha , but solely based on the recently released BABA's report of an 88% increase in buyers seeking sustainable products over the past year, we can assume, that Q1 results will likely show a great YoY dynamic. Recent results from JD.com indirectly support this conclusion:

{kind=link}

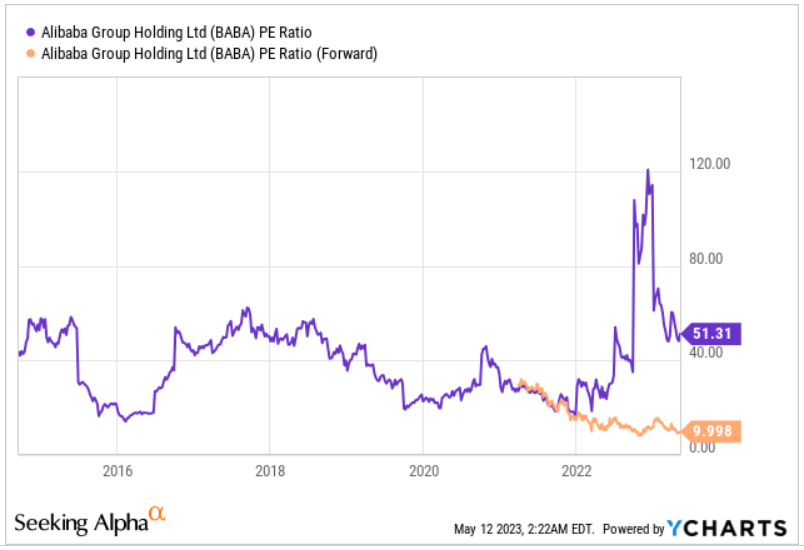

BABA stock is trading with a large divergence between the TTM and FWD multiples, reflecting the high hopes for an imminent operational turnaround that the market is waiting for. The forwarding multiple of ~10x is at the lowest level in its historical perspective - BABA is as cheap as it's ever been:

{kind=link}

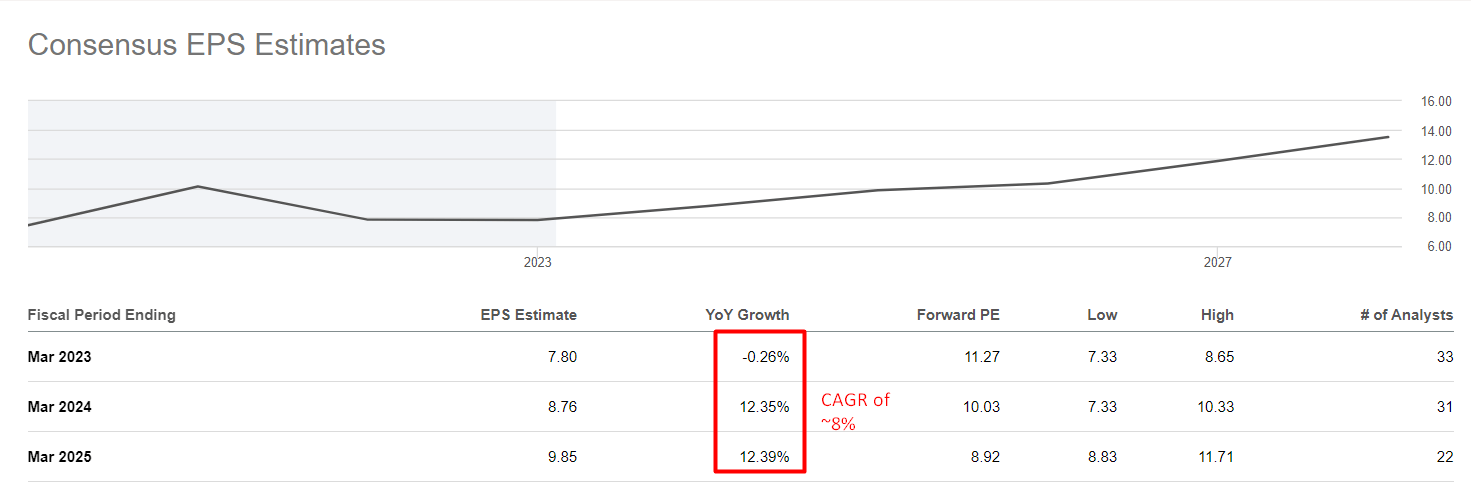

However, the projected EPS growth is a CAGR of ~8.1% from 2023 to 2025 - relatively low in my opinion:

Seeking Alpha, BABA, author's notes

{kind=link}

In my opinion, this consensus [if true] could lead to the P/E ratio of BABA remaining in the low teens for quite a while. If this is the case, the prospects for shareholders' returns are likely to be limited.

And what about Kaspi?

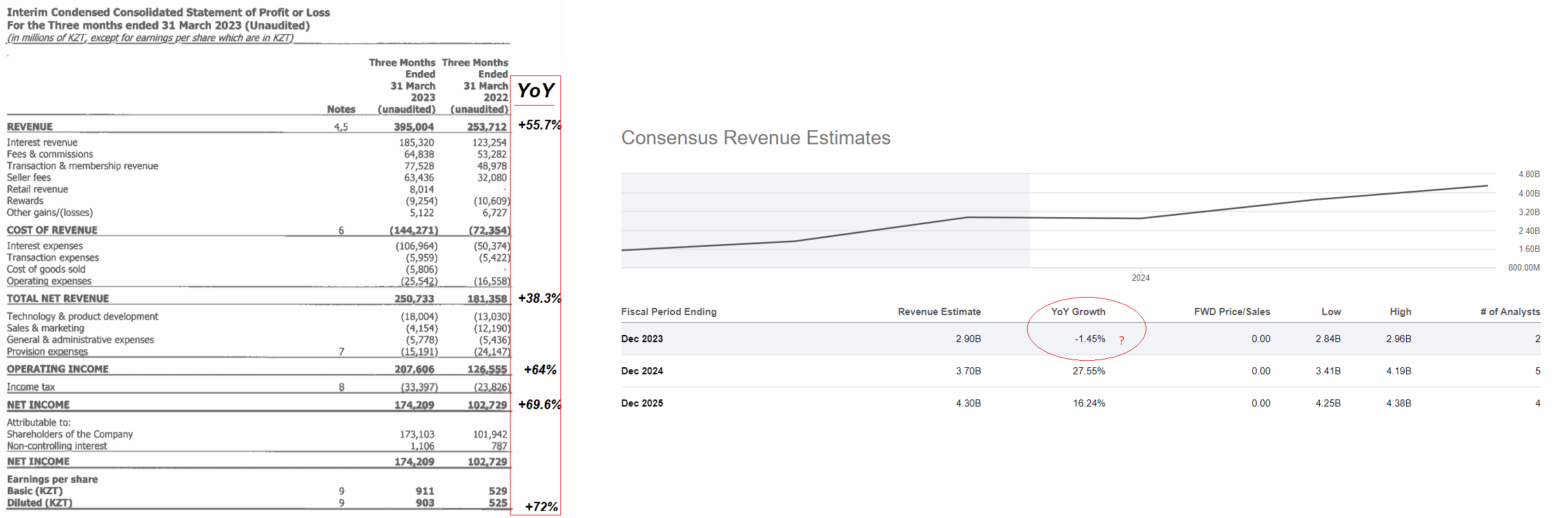

To be honest, I've never seen such a large discrepancy between analysts' forecasts and the company's actual results:

Author's work, based on Kaspi's and SA's data

{kind=link}

Net of interest expenses [again, Kaspi is a functioning commercial bank], the company posted total net revenue of 250.7 billion tenges [~$552.2 million; USDKZT = 454 as of March 31, 2023], while this metric was only 181.4 billion tenges or ~$386 million [USDKZT = 470 as of March 31, 2022] a year earlier. Annual growth in US dollar terms is +43%, even higher than in tenge terms. Kaspi's earnings per share in U.S. dollars grew 76.7% year over year. Where does the forecast of a -1.45% y/y decline in EPS at the end of FY2023 come from? Even the exchange rate difference suggests otherwise.

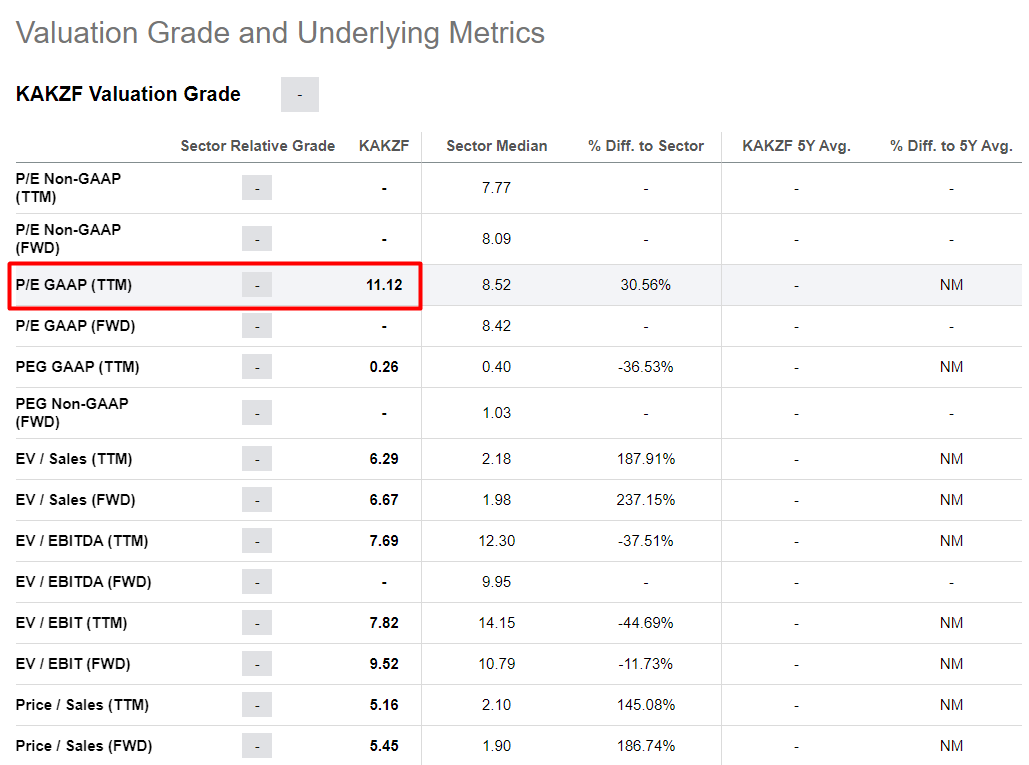

The company is underfollowed and unseen by most retail and institutional investors. So when they open their terminal with EPS forecasts and see a YoY decline in EPS, they're likely to pass by and not try to look deeper. You know - who wants to figure out what's going on with a fintech company from Kazakhstan, especially with declining profits? This leads to a severe undervaluation, a kind of market inefficiency that cannot be logically explained. Why do I say undervaluation? Because despite an obviously more dynamic addressable market with a huge potential for online penetration and a near doubling of earnings per share in Q1 FY2023, Kaspi stock trades at only 11 times TTM earnings:

{kind=link}

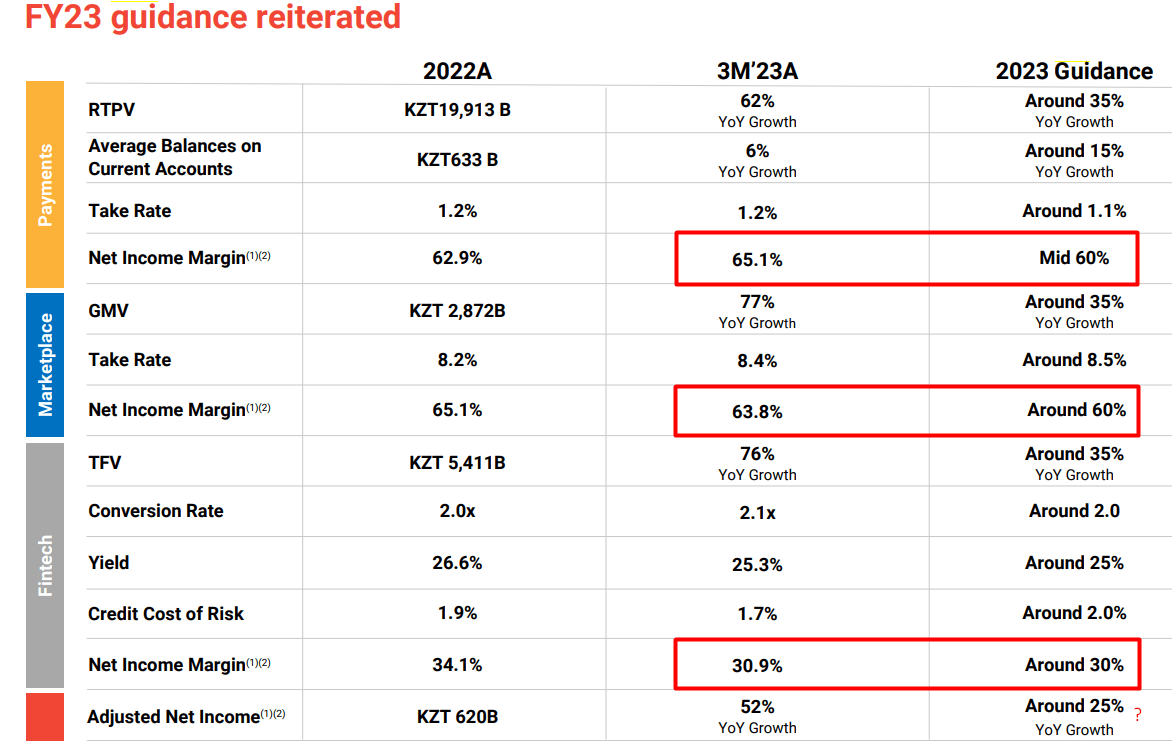

According to management's guidance, the company is expected to maintain current bottom line margins through the end of FY2023 in all of its 3 segments. Then why the net income growth rate should drop from the current +52% to just +25% YoY?

Kaspi's Q1 FY2023 IR materials

{kind=link}

I don't see any major one-time events in the first quarter that should disappear from the financial statements in future periods. It seems to me that management is trying to stay conservative with its forecasts. Most likely, Kaspi will achieve net income growth of over 25% this year - even at 30% growth, the FWD P/E multiple arrives at 8.5x, according to my calculations. This is a severe undervaluation - at the current growth rate, Kaspi should trade at 15-20x, giving the stock a huge upside potential.

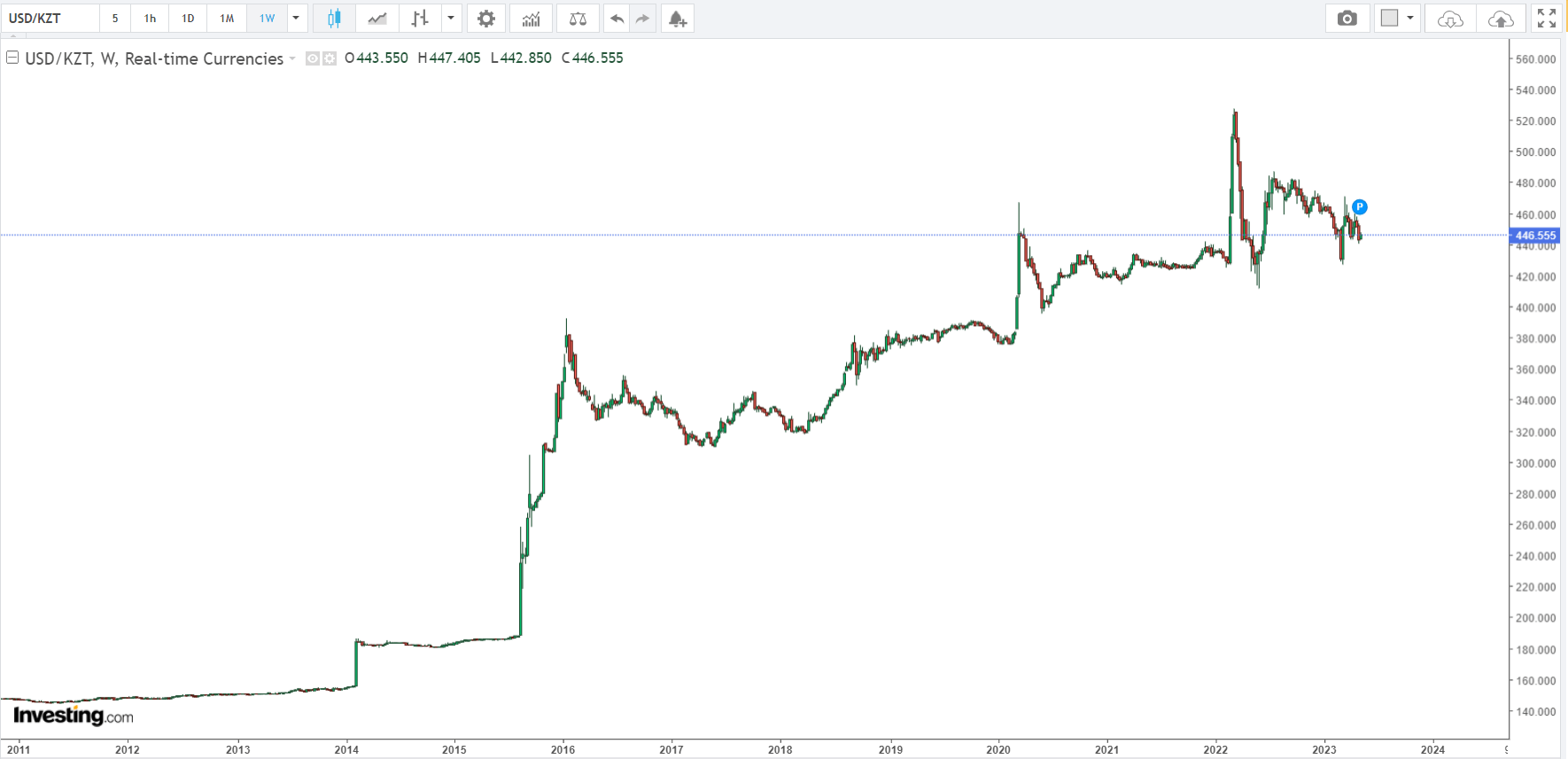

Risks To My Thesis

I dismiss the fear of an attack from Russia [on Kazakhstan], taking into account China's assurance of protection for its western neighbor. But I'm more concerned about currency risk - take a look at how the USD/KZT exchange rate has outperformed in recent years.

Investing.com , USD/KZT

{kind=link}

As Kaspi generates all its revenues in Kazakh tenge, the company needs to grow faster than the appreciation of the USD/KZT exchange rate for investing in the company to be worthwhile.

Also important to note that Kazakhstan's economy is tied to commodities, particularly oil & gas, and with the possibility of a commodity super-cycle, the state should have a stable exchange rate in the coming months, providing potential income for foreign investors as Kaspi's operations grow in tenge [Kaspi's Q1's financials prove it when translated into US dollars]. But here lies the risk: if energy prices continue to fall, as they have in recent weeks, this may harm the exchange rate and thus the dollar equivalent of Kaspi's revenues.

In addition, Kaspi shares are traded on the LSE - there is enough volume there. This makes it difficult for US investors - Kaspi's depositary receipts are almost inactive in the US gray market. This is something to keep in mind.

Also, I might be short-sighted about Alibaba's growth prospects. Many major banks have a bullish view of China's digital economy and consider the BABA stock as one of the obvious candidates to ride China's recovery from the corona-crisis:

Morgan Stanley, proprietary source [27 April 2023]

{kind=link}

So, I may be wrong when I say that Kaspi stock looks better than the BABA stock - things can change at any time. I encourage everyone to do their own due diligence before putting their hard-earned savings into both stocks.

The Takeaway

Although I'm relatively more positive about BABA now than before, I don't recommend trying to catch another falling knife in this stock. Don't let stuck hedge funds dump their stakes in the company [how it was throughout 2022 as far as I could see]. Better buy what grows higher, costs about the same in terms of valuation, and has fewer geopolitical risks.

So Kaspi looks like an obvious, higher-quality replacement for Alibaba in the portfolio of a Western investor seeking an allocation to the emerging Asian market [Kazakhstan is a Central Asian country].

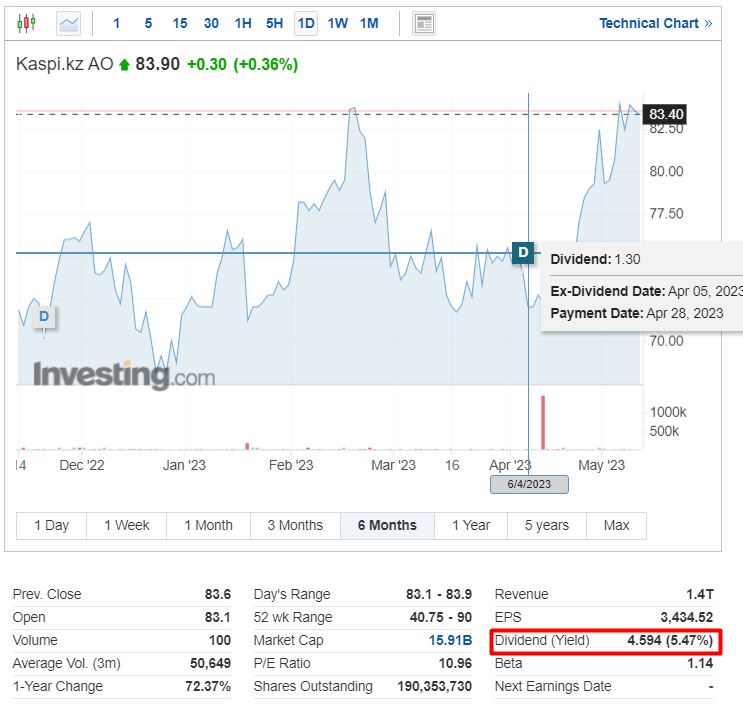

In addition, Kaspi pays quite generous dividends in US dollars [>5%] and is very active in buying back its shares - so why pass by an ideal combination of growth and value in one place?

{kind=link}

Thank you for reading! Please, let me know what you think in the comment section below!

For further details see:

Forget Alibaba And Take A Look At Kaspi Instead