COM - Franklin Electric: Near-Term Headwinds

2023-10-10 17:29:24 ET

Summary

- Franklin Electric Co., Inc. is facing near-term headwinds from inventory destocking and declining backlog, indicating a slowdown in growth.

- The company's margin outlook is mixed, with moderating cost and labor inflation but lower sales in high-margin Fueling Systems segment.

- Despite trading at a discount, the discount is justified given slowing growth.

Investment Thesis

Franklin Electric Co., Inc. ( FELE ) has seen good growth over the past couple of years, but near-term headwinds from inventory destocking and a declining backlog indicate a slowdown in its growth rate ahead. The company is also facing challenges due to delayed customer projects in the Fueling Systems business and lower residential and agriculture demand for its Water Systems business, which should negatively impact revenue growth.

Further, the margin outlook is mixed. While cost and labor inflation are moderating, the unfavorable mix due to lower sales in the high-margin Fueling Systems segment and much more modest price increases given the slowing demand should result in flattish margin performance. Despite the stock trading at a discount compared to its historical averages, I believe this discount is justified, and I prefer to remain on the sidelines.

Revenue Analysis and Outlook

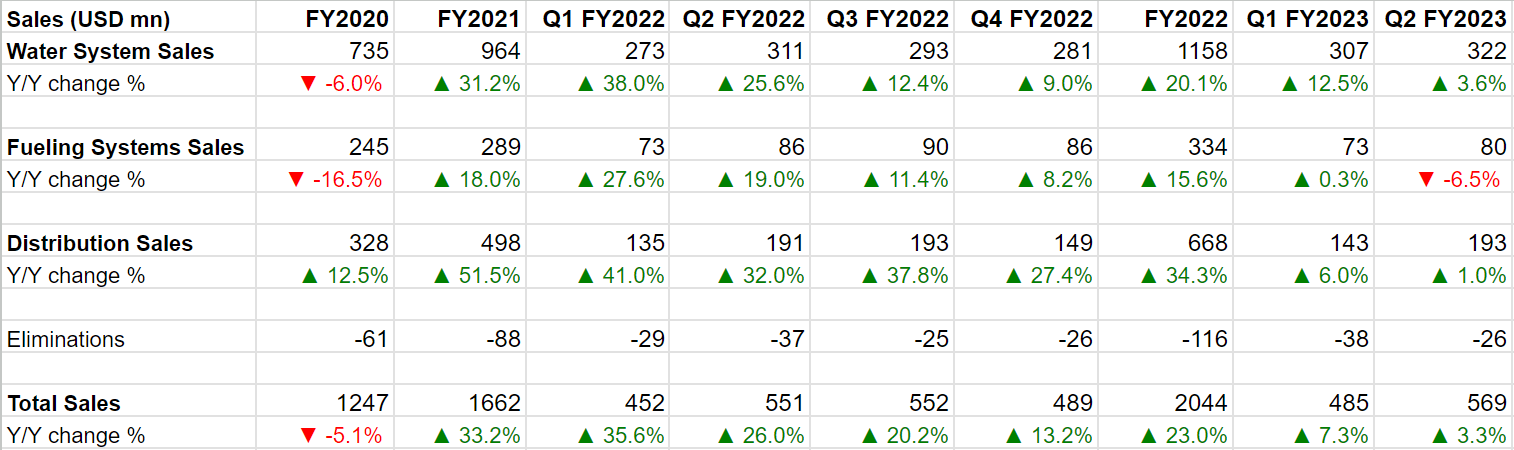

After seeing strong double digit Y/Y sales growth in FY21 and FY22, the company’s sales growth has moderated of late. In the second quarter of 2023, FELE’s net sales increased 3.3% Y/Y to $569.1 million driven by 3.6% Y/Y and 1% Y/Y sales growth in Water Systems and Distribution segments, respectively. The Fueling systems segment saw net sales decline by 6.5% Y/Y primarily driven by lower demand as customers’ planned projects are getting postponed due to macroeconomic uncertainty.

FELE’s Historical Revenue Growth (Company Data, GS Analytics Research)

{kind=link}

Looking forward, while there are good long term drivers in the water end-markets, there are some near-term headwinds for the company as well. The company’s water end market benefitted from several factors including higher ag commodity prices, strong residential market as well as trend toward rural migration during COVID. These factors are now reversing with ag commodities like Wheat ( W_1:COM ) and Corn ( C_1:COM ) prices trending downward impacting farm income and demand from agriculture end markets; high mortgage rates impacting residential demand; and the trend towards rural migration reversing with work-from-office resuming.

The company has also started seeing inventory destocking in its channel as supply chain disruptions have eased and channel inventory is returning to normal levels. Further, a continued slowdown in end-market as well as higher cost of carrying inventory due to high interest rate environment is also driving some destocking. This is expected to continue impacting the sales in the near term.

The company's water systems backlog has declined to ~$186 mn at the end of the last quarter from around $230 mn at the beginning of this year indicating near term slowdown in growth for this segment. In the fuel business, the broader macro uncertainty and higher interest rates are resulting in some of the customer’s planned projects getting delayed which is expected to adversely impact the sales in the near term. This business is also facing a long term headwind as growing adoption of Electric Vehicles (EVs) impacts the demand for the company’s fueling systems. While the company has started offering grid solutions and EV systems for the electric vehicle market, it is too early to tell if these products can offset the long term demand headwinds for fueling systems products.

Overall, I am expecting a much more modest growth for the company in FY23 and FY24, compared to ~33.2% Y/Y growth and ~23% Y/Y growth the company posted in FY21 and FY22, respectively. The current sell side estimates are modeling a sales growth of 5.82% Y/Y for FY23 with a growth of 5.43% Y/Y for Q3 2023 and 7% Y/Y for Q4 2023. I see a risk of the company missing these expectations as the sales growth in Q3 and Q4 are unlikely to accelerate from the 3.3% Y/Y growth we saw in Q2 given the headwinds discussed above.

Margin Analysis and Outlook

In Q2 2023, the company’s gross margin declined 120 bps Y/Y to 33.1% and the operating margin declined 50 bps Y/Y to 14.2%. If we look at segment wide adjusted operating margins while Water Systems’ adjusted operating margin was flat Y/Y and Fueling Systems’ margins increased 290 bps Y/Y, and Distribution segment saw 300 bps Y/Y decline in margins. Lower Distribution segment margins coupled with negative mix due to lower sales in high margin Fueling Systems segment resulted in a decline in Y/Y operating margins for the company.

FELE’s Adjusted Operating margin and Gross margin (Company Data, GS Analytics Research)

FELE’s Segment Wise Adjusted Operating margin (Company Data, GS Analytics Research)

{kind=link}

Looking forward, the company’s margin outlook is mixed. While cost and labor inflation is moderating, the company’s pricing increases are also expected to be much more modest given the slowing demand. Further, delays in customers’ planned projects in Fueling Systems should continue to result in lower segment sales negatively impacting the mix.

Valuation and Conclusion

FELE’s stock is trading at a 20.89x FY23 EPS estimate of $4.31 which is lower than its 5-year average forward P/E of 24.73x.

While the company is trading at a lower-than-historical valuation, the near term headwinds from inventory destocking, lower backlog, lower residential and Agriculture demand for water systems business should continue to adversely impact revenues resulting in a much lower growth rate compared to what we have seen over the last couple of years. So, I believe this discount is justified. Hence, I prefer remaining on the sidelines despite low valuations and have a neutral rating on the stock.

For further details see:

Franklin Electric: Near-Term Headwinds