FRHC - Freedom Holding: Business Keeps Growing

2023-11-21 20:32:56 ET

Summary

- Freedom Holding recently reported Q3 2023 results.

- The company's business continues to grow at a spectacular pace.

- Recent allegations against the company haven't affected its business so far.

Since this August, Freedom Holding ( FRHC ) has been under pressure from Hinderburg Research short-selling firm. Nonetheless, the latest earnings report of Freedom Holding shows that the company remains operationally sound and ready to grow even more amid a noticeable positive tailwind coming from the Russian side.

If you're comfortable with company-specific risks, Freedom Holding looks like a decent stock to buy considering its growth potential.

About Freedom Holding

Freedom is an investment holding from Kazakhstan, which operates mainly in post-Soviet countries (except Russia), but also has some market exposure in Eastern Europe and the US. Three major segments of the company are:

- Brokerage services (access to the world's largest exchanges, margin lending, providing access to IPOs in the US).

- Proprietary trading in accordance with internal policies and recommendations of the company's internal investment committees.

- An ecosystem of services in Kazakhstan, which includes a bank, insurance company, online payment service, telecom operator, and other business initiatives.

Company Overview

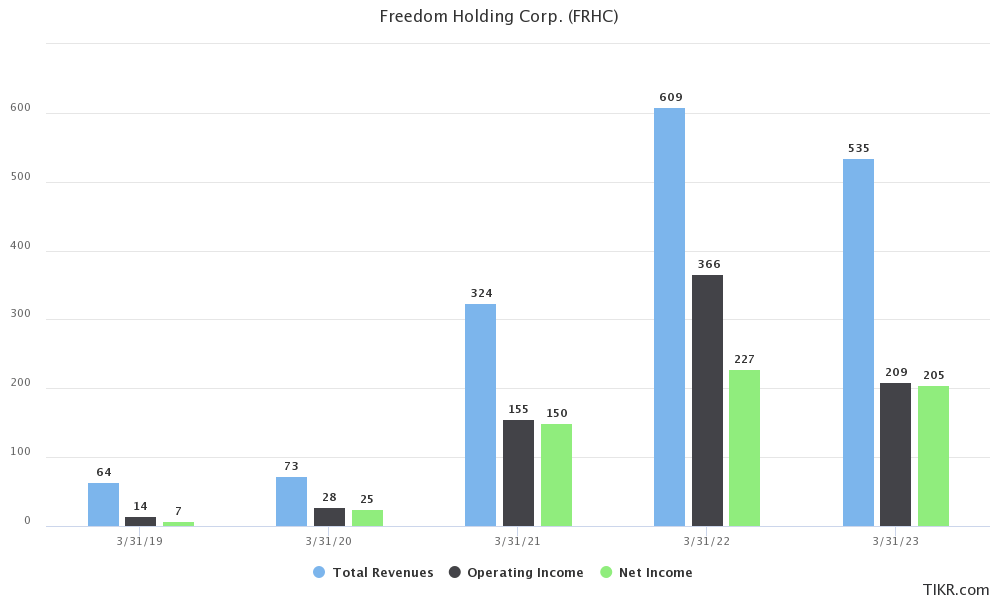

Over the last five years since Freedom's IPO, the company has demonstrated outstanding revenue growth:

{kind=link}

Last year has been tough for Freedom Holding because of the war in Ukraine and the subsequent sale of the Russian business unit. However, on an LTM basis, the company has already set a new record high of $774 million, after the previous high of $609 million in 2021.

{kind=link}

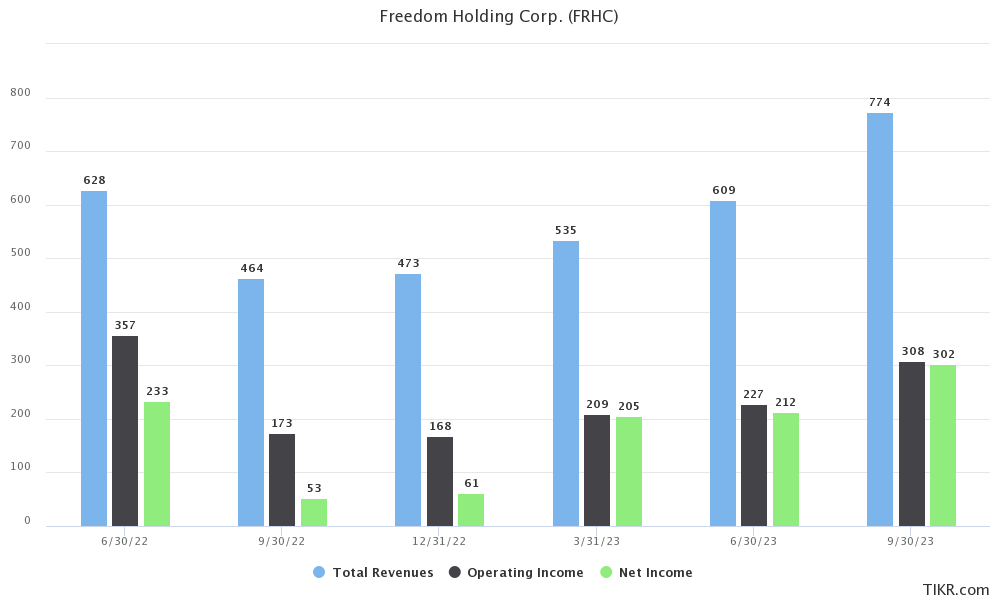

Now let's discuss the most recent Q3 results .

The company's revenue is up 141% year-over-year (y-o-y) to $435 million.

Net income grew by 134% y-o-y to $115 million. The majority of the company's income was from interest income, which is up 261% y-o-y to $213 million, driven by an expansion of the securities portfolio and increased issuance of bank loans. Income from the company's insurance business increased by 121% y-o-y to $57.9 million amid a low base effect as it actively continues its expansion in the Asian region. Net profit from securities trading in the reporting period increased 5.6 times to $50.7 million, ensured by the sale of bonds of the Ministry of Finance of the Republic of Kazakhstan.

Interest expenses increased by 241% y-o-y to $139.4 million due to an expansion in the volume of short-term financing through repurchase agreements, an increase in interest expenses on customer deposits, an increase in administrative costs by 130% y-o-y to $29.6 million and increased costs for bonuses and wages due to the active expansion of the company.

In terms of revenue geography, Central Asia and Eastern Europe continue to dominate with a share of 88% of Freedom Holding's total revenue.

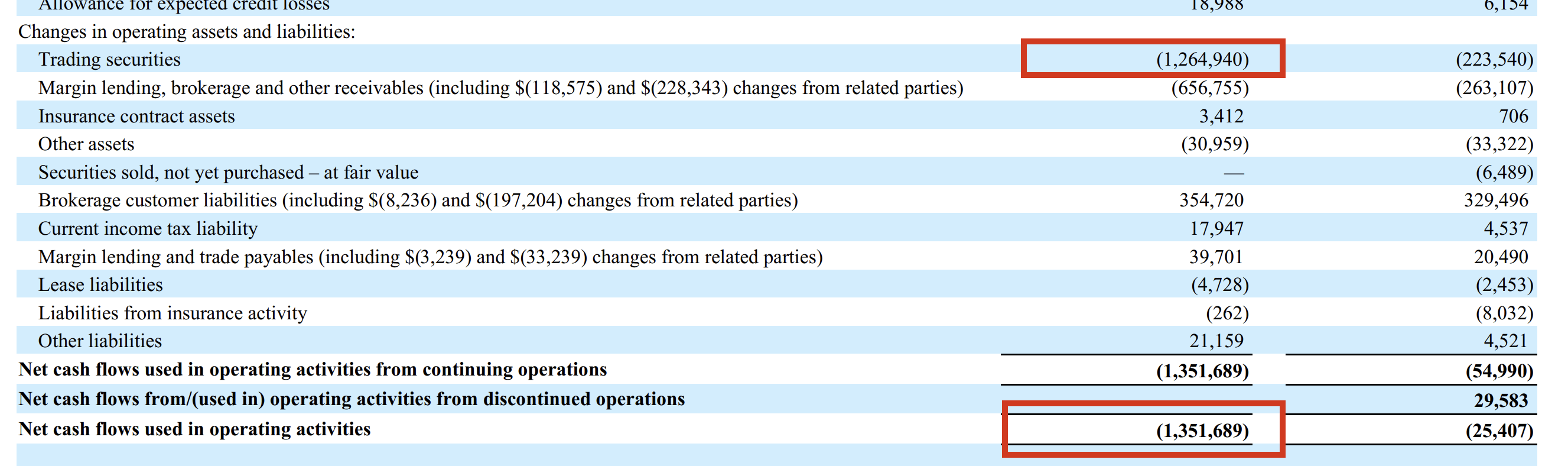

Also, investors may be concerned about the fact that the company is heavily cash flow negative:

{kind=link}

As we can see, Freedom has faced a negative cash flow in operating activities of $1.3 bn in Q3 2023. Now let's break down the reasons for a negative cash flow:

- Increases in trading securities: The company had significant cash outflows from increases in purchases of trading securities for its proprietary trading account, totaling $1.26 billion. As the company expands its proprietary trading activities, it requires more cash to acquire additional trading securities. Freedom clearly indicates that in its 10-K report : "The size of our securities positions vary substantially based upon economic and market conditions, allocations of capital, underwriting commitments and trading volume of an individual issuer's securities. Also, the aggregate value of inventories of securities which we may carry is limited by the net capital and capital adequacy rules in effect in the jurisdictions where we conduct business."

- Increases in receivables: The company had cash outflows of $657 million due to increases in margin lending and other receivables. As the company's lending and brokerage activities grow, it leads to more credit extended and higher receivables balances.

- Cash used for loan issuances: The company had $444 million in net cash outflows for originating new loans to customers, which reduces available cash.

- Offsets from customer liabilities: Cash outflows were partially offset by $355 million in inflows from increases in customer liabilities. As the company's brokerage customer base expands, it leads to more cash deposits into their accounts.

As the company notes in its Q3 report:

We maintain a majority of our tangible assets in cash and securities that are readily convertible to cash, including governmental and quasi-governmental debt and highly liquid corporate equities and debt. Our financial instruments and other inventory positions are stated at fair value and should generally be readily marketable in most market conditions.

Thus, despite a negative operational cash flow, the company has a proper liquidity cushion to remain stable financially.

Overall, in Freedom's investment case, a negative cash flow isn't much of a concern for me given the nature of its business. At the same time, triple-digit revenue and income growth make Freedom Holding a solid growth stock that keeps performing well operationally.

The Moat Continues To Strengthen

In its extensive report published in mid-August, Hinderburg Research outlined a plethora of potential issues with Freedom Holding. However, three months after the report, we barely see any consequences for Freedom:

- The company's client base remains stable and loyal;

- S&P Global Ratings has affirmed the long-term credit rating of Freedom Holding at B-, as well as the long-term and short-term credit ratings of its subsidiaries;

- The company is currently being investigated by the US Department of Justice and the Securities and Exchange Commission, according to CNBC, though nothing substantial has been found so far.

In my opinion, folks from Hinderburg Research have missed one point in the calculation of their short bet against Freedom Holding. In the post-Soviet space, you don't have much competition among brokerage companies. In this region, the majority of investors who want to trade on American and European stock exchanges are limited to two primary options: Interactive Brokers ( IBKR ) and Freedom Finance.

From my point of view as someone who regularly communicates with Russian-speaking investors, the sole fact that Freedom Finance provides services and support in the Russian language already plays a significant role in why it's preferred over Interactive Brokers and other less-known competitors. This factor will play an even greater role amid blocking sanctions against SPB Exchange based in Russia.

For context, SPB Exchange was a primary trading platform that provided access to US/EU markets to Russian retail investors. Under the newly imposed sanctions, SPB has been effectively cut off from the Western exchanges. This is a potentially huge tailwind for Freedom Holding because Russian investors now have even fewer options for investing in the US or EU.

A lack of competitors combined with a strong positioning of Freedom Holding in CIS countries, Central Asia, and Eastern Europe creates a natural moat for FH, limiting opportunities for new players to enter the regions where Freedom Holding operates.

Risks

I see the following risks for Freedom Holding:

- The company relies heavily on repurchase agreements to finance proprietary trading assets, with $2.8 billion of trading securities pledged as collateral. This introduces liquidity risk if those financing sources are reduced.

- As a result of potential future sanctions against Russia, Freedom Holding may be forced to stop providing services to those Russians who live in Russia and/or don't have citizenship or a residence permit in another, non-sanctioned country. This may have a significant impact on the company's operational growth.

- The US Department of Justice and the Securities and Exchange Commission may bring charges against the company if any serious violations are detected after the ongoing investigation finishes. However, according to Bloomberg, Freedom Holding has plans to hire a chief risk officer as well as a chief legal officer by the end of 2023. The company is also planning to publish a forensic report by year-end that will examine the accusations made by Hindenburg.

The Bottom Line

Freedom Holding has successfully withstood the short-seller's attack of Hinderburg Research and continues to flourish amid tailwinds caused by sanctions against Russian competitors.

While the stock doesn't look cheap on Price/Sales (6.3x according to Seeking Alpha) and Price to Book basis (5.45x), investors should keep in mind a 5-year CAGR revenue growth of 110.99% that keeps increasing. Not to mention ROE of 37.01% and ROA of 8.36%, which are among the best in the brokerage services industry.

Freedom Holding is definitely not a "value" stock. Just like any other growth stock, Freedom has a rich valuation that is explained by the company's sustained growth. The recent Q3 reports clearly shows that the company still has enough potential to keep going at the same excellent growth pace.

For further details see:

Freedom Holding: Business Keeps Growing