FRD - Friedman Industries: Decent Q4 FY23 Results And A Strong Outlook (Rating Upgrade)

2023-06-30 17:53:25 ET

Summary

- Friedman Industries booked a net income of $6.3 million for Q4 FY23 thanks to high HRC steel prices, thus recording the most profitable year in its history.

- For Q1 FY24, margins are forecast to improve thanks to the higher average HRC steel price, and I expect net income to surpass $8 million.

- In my view, Friedman Industries should be valued at over 0.9x P/B, which translates to $14.09 per share.

Introduction

U.S. steel service center operator Friedman Industries ( FRD ) is among the main positions in my portfolio, and I've written four articles about the company on SA so far. The latest of them was in February when I said that the Q4 FY23 financial results should be strong as hot-rolled coil (HRC) steel prices in the USA had increased by almost a third since November.

Well, Friedman Industries announced its financial results for FY23 on June 29 and this was the best year in its history with revenues surpassing $500 million and net income coming in at $21.3 million. In Q4 FY23 alone, the company booked a net income of $6.3 million, and it said that it expects a strong performance for Q1 FY24.

In view of this, I'm upgrading my rating on the stock to a strong buy. Let's review.

Overview of the Q4 FY23 financial results

In case you're not familiar with Friedman Industries or my earlier coverage, here's a brief description of the business. The company was founded in 1965, and it currently operates five hot rolled coil processing facilities in the USA, all of which are located on mill campuses and are equipped with panel flat leveling technology. It also has a tube mill in Lone Star, Texas. All of the facilities of Friedman Industries are situated on or near water and five of them have rail-receiving capability.

Friedman Industries

The company was listed in 1972, and it has paid a cash dividend every quarter since then, with June 2023 marking the 206th consecutive quarterly cash dividend. The dividend yield stands at 0.8% as of the time of writing.

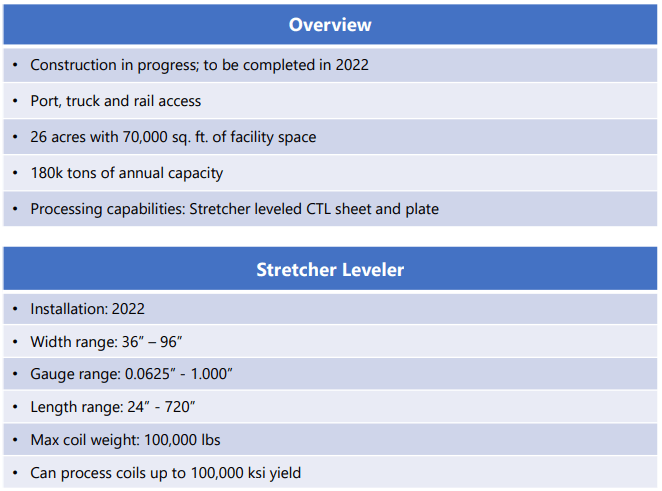

In my view, 2022 was a transformational year for Friedman Industries as it acquired the East Chicago and Granite City facilities in April in exchange for $63.8 million in cash and 516,041 shares. This was the first acquisition in its history. In addition, the company put into operation its $22.3 million coil facility in Texas, which is located on the campus of the new $1.9 billion Sinton electric arc furnace flat-rolled steel mill of Steel Dynamics ( STLD ). This facility has the largest stretcher leveler line in North America and in November 2021, Friedman Industries said that it expected it to have annual EBITDA of $4.5 million to $5.5 million based on historical average margins.

{kind=link}

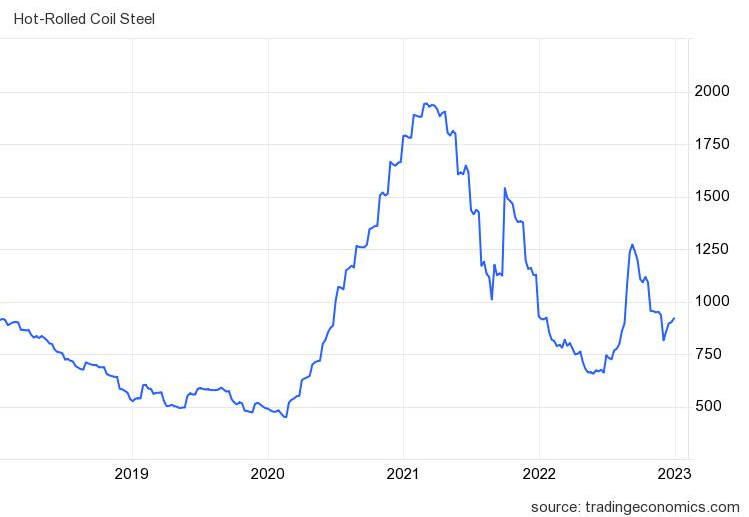

With the new Sinton facility ramping up and HRC prices in the USA peaking at $1,200/st in April thanks to strong economic activity in the country, I was expecting Friedman Industries to book strong results for Q4 FY23, with net income surpassing $10 million. HRC steel contracts for differences even briefly surpassed $1,300/t in March.

{kind=link}

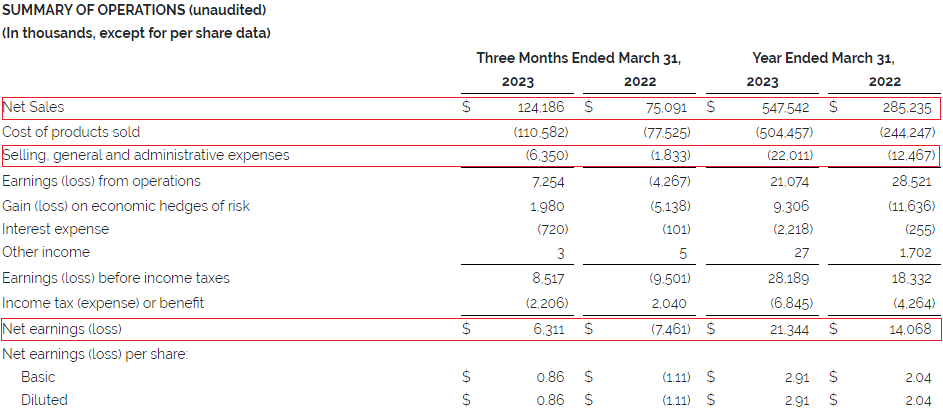

While Friedman Industries still hasn't released its FY23 annual report, the company issued on June 29 a press release about its results of operations for the quarter and fiscal year ended March 31. As we can see from the table below, high HRC steel prices and the addition of the East Chicago, Granite City, and Sinton facilities boosted net sales by 65.4% to $124.2 million in Q4 FY23. The sales of the coil segment soared by 95.8% year on year to $112.8 million as the sales volume came in at 132,000 tons, which was 152% higher than a year ago and 17% compared to Q3 FY23. The three new facilities accounted for about 84,000 tons of the sales volume in Q4 FY23. Unfortunately, net income came in at $6.3 million despite the coil segment swinging to a $7.7 million operating profit from a $1.7 million operating loss and the tubular segment swinging to a $2.5 million operating profit from a $1.5 million operating loss a year earlier. In my view, the main reason net income was lower than my expectations was a $1.65 million increase in selling, general and administrative (SG&A) expenses quarter on quarter. There should be an explanation about why these expenses increased in the annual report. Still, I think that the Q4 FY23 financial results were decent and FY23 was the most profitable year in the history of Friedman Industries with a net income of $21.3 million. As a result, the company is trading at a P/E ratio of just 3.4x as of the time of writing.

{kind=link}

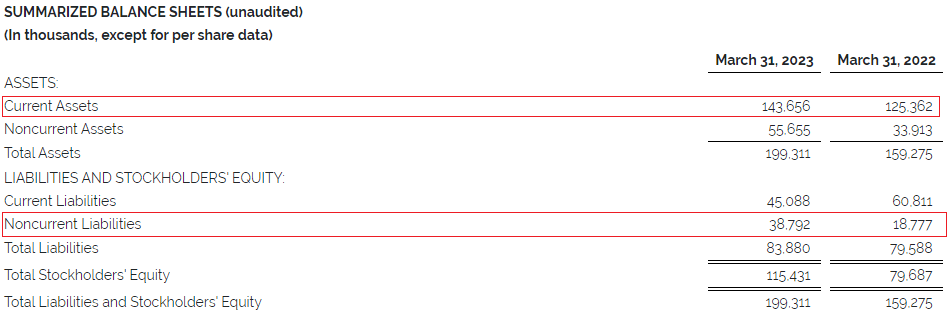

Turning our attention to the balance sheet, I was surprised that current assets decreased by $4.7 million quarter on quarter to $143.7 million. You see, they typically increase during periods with rising HRC steel prices as the value of inventories rises. In my view, the most likely scenarios are that Friedman Industries had fewer tons of steel at the end of March or that the higher value of inventories was offset by lower accounts receivable. Non-current liabilities went down by $7.9 million as the company is paying down the loan it took to buy the East Chicago, and Granite City facilities. I'm optimistic that dividend payments could increase in a year or two as the debt burden declines.

{kind=link}

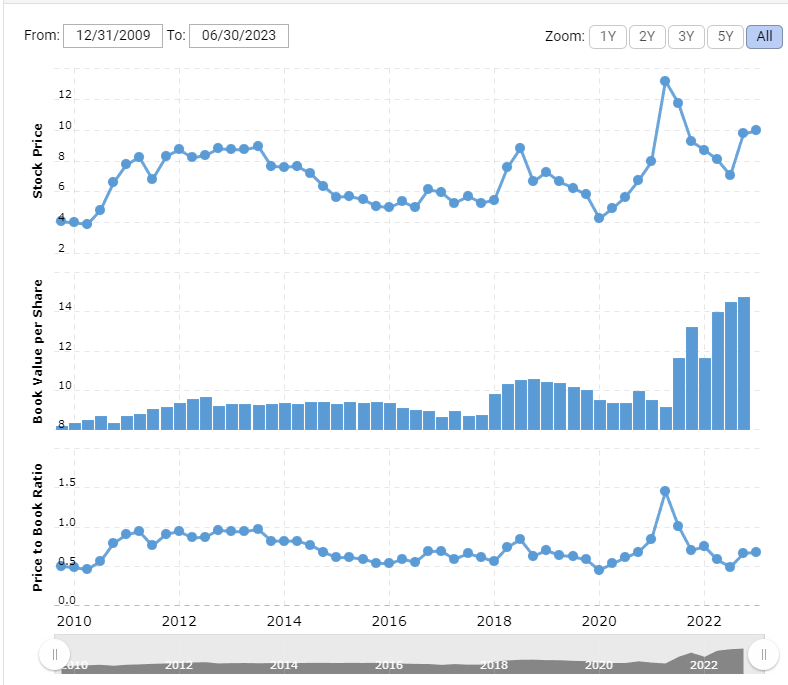

Looking at what to expect for the future, Friedman Industries said that its output for Q1 FY24 should be similar to the one for Q4 FY23 and that margins are forecast to improve thanks to the higher average HRC steel price. In view of this, I'm optimistic that net income for Q1 FY24 could surpass $8 million. Turning our attention to the valuation, I think the company looks cheap from a price/book standpoint. Over the past 10 years, Friedman Industries has often traded at above 0.8x P/B. At the moment, the company is trading at 0.64x P/B and I think it should be valued at over 0.9x P/B considering Q1 FY24 results are expected to be strong. This translates into $14.09 per share or an upside potential of 41.6%.

{kind=link}

Looking at the risks for the bull case, I think the major one is the potential lower HRC steel prices in the second half of 2023. According to data from Argus , domestic US HRC Midwest and southern assessments both went down by 60/st on June 27 on an ex-works basis as mill hikes announced in the middle of the month have failed to stick. It seems that demand could be softening, and I think it's possible we will see HRC steel prices below $750st over the next months unless the situation improves. This could put Friedman Industries in the red for Q2 or Q3 FY24.

Investor takeaway

Friedman Industries had a strong end to FY23, although the net income was below my expectations. Yet, margins and net income should improve in Q1 FY24 and I expect this to provide a boost for the share price. Friedman Industries is currently trading at just 0.64x BV and I think there is a good margin of safety here.

For further details see:

Friedman Industries: Decent Q4 FY23 Results And A Strong Outlook (Rating Upgrade)