FRD - Friedman Industries: Mixed Q3 Results But A Strong Start To Q4 (Rating Downgrade)

Summary

- Friedman Industries booked a comprehensive income of $2.05 million in Q3 FY23, and I was disappointed by the results of the tubular division and the low gains from derivatives.

- However, the Sinton facility seems to be ramping up fast and Q4 FY23 results should get a strong boost from rising U.S. HRC prices.

- I wouldn’t be surprised if the comprehensive income for FY23 surpasses $30 million.

- However, I’m cutting my rating to buy as FRD stock is becoming expensive from a price/book standpoint.

Introduction

U.S. steel service center operator Friedman Industries (FRD) is currently my third largest position and I've written several articles about the company on SA. The latest of them was in December when I said that the tubular division was performing well, and that the hedging policy of Friedman Industries should keep the company in the black in Q3 FY23.

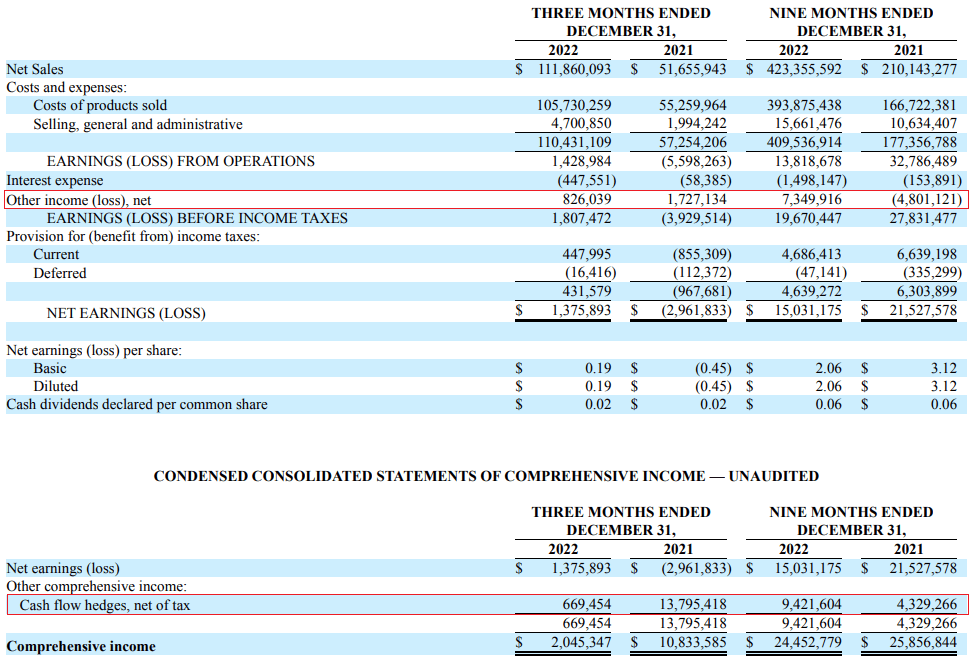

Well, production was higher than expected and Friedman Industries booked a $2.05 million comprehensive income in Q3. However, the operating profit of the tubular division was only $0.69 million and gains from cash flow hedges and HRC steel contracts derivatives were just $1.49 million. Overall, the East Chicago and Granite City facilities saved the day, which was unexpected. On another positive note, hot-rolled coil (HRC) steel prices in the USA have been rising rapidly over the past few months which should provide a strong boost for the company's Q4 FY23 results. Let's review.

Overview of the Q3 FY23 financial results

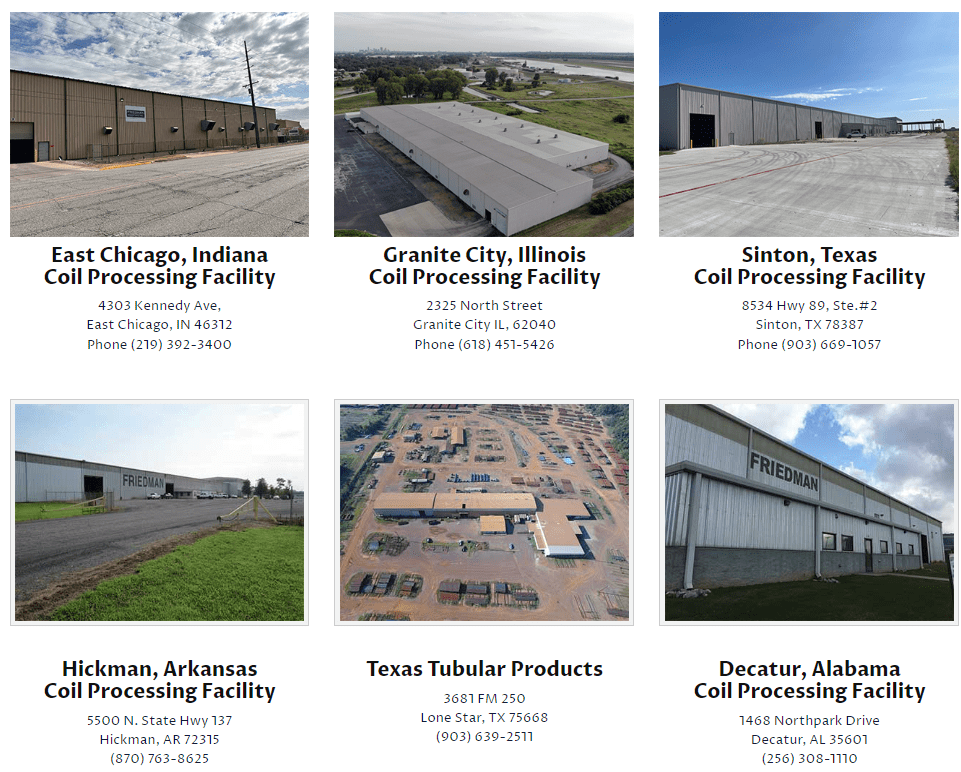

In case you haven't read any of my previous articles about Friedman Industries, here's a quick description of the business. The majority of the company's revenues come from cutting to length hot-rolled steel coils and this division has a total of five facilities across the states of Indiana, Illinois, Arizona, Alabama, and Texas. All of them have temper mill or stretcher leveler capabilities and Friedman Industries also has a tubular division involved in the manufacturing and distributing steel pipes which includes a facility in Texas. The latter operates two electric resistance welded pipe mills which are licensed to manufacture line pipe and oil country pipe.

{kind=link}

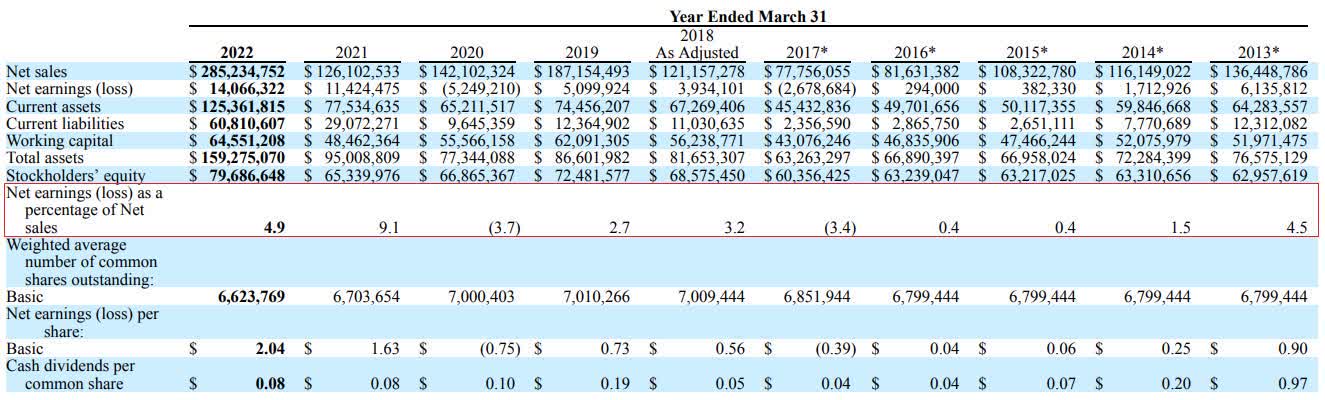

All of the facilities are located on or near water and a total of five of them have rail receiving capability which I think provides Friedman Industries with a strong competitive advantage. Looking at the financial results for the past decade, the company has rarely been in the red.

{kind=link}

However, Friedman Industries is a much different company today compared to a year ago as it has doubled the number of its facilities. In April 2022, it bought the then loss-making East Chicago and Granite City facilities for $63.8 million in cash and issued 516,041 shares. The seller was Plateplus, which is owned by Japanese group Mitsubishi Corp ( OTCPK:MSBHF ) and this deal should provide Friedman Industries with additional options for sourcing steel as the latter is now a major shareholder. In October, Friedman Industries put into operation its new coil facility in Texas, which is located on the campus of the new $1.9 billion Sinton electric arc furnace ((EAF)) flat-rolled steel mill of Steel Dynamics (STLD). The Sinton facility of Friedman Industries cost $22.3 million to build and it accounted for over 40% of the company's property, plant and equipment book value at the end of December. This new facility has 180,000 tons of annual capacity and the company expects it to produce 110,000 tons to 140,000 tons in FY24. In November 2021, Friedman Industries said that it expected the Sinton facility to generate annual EBITDA of $4.5 million to $5.5 million based on historical average margins.

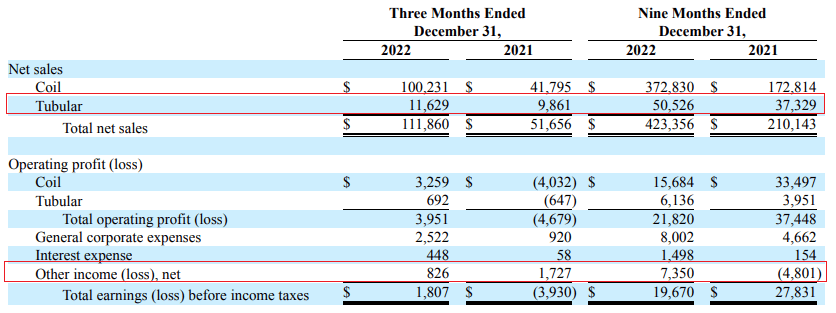

Turning our attention to the Q3 FY23 financial results, the company said in the middle of November that it was expecting a Q4 sales volume of around 105,000 tons plus a slight margin improvement and a boost from hedging activities (see page 20 here ). I was optimistic that the operating profit of the tubular division would remain above $3 million due to strong demand from the oil sector and the comprehensive income could be higher compared to the $4.05 million achieved in Q2 FY23. Gains from cash flow hedges and HRC steel contracts derivatives for the period were $5.33 million. Well, tons sold rose to 113,000 in Q3 which I think is a sign that the ramp up at Sinton is going faster than anticipated. Unfortunately, the sales of the tubular division slumped by 41.8% quarter on quarter to $11.6 million and this led to a significant decrease in profitability. Friedman Industries did not give a reason for the sales decline of this segment. In addition, gains from cash flow hedges and HRC steel contracts derivatives came in at just $1.49 million.

Friedman Industries Friedman Industries

{kind=link}

{kind=link}

Well, at least there is a good explanation why gains from derivatives were so low - major U.S. steel producers started raising prices in late November and this trend has continued into Q1 2023. I was expecting domestic HRC prices to peak at around $800 per ton this year but we're already past this level. On February 14, Argus reported that weekly domestic US HRC Midwest and southern assessments rose by $50/st to $850/st and that Cleveland-Cliffs (NYSE: CLF ) and Nucor (NYSE: NUE ) are targeting a minimum HRC price of $900/st. This should provide a boost for the result of the coil division of Friedman Industries in Q4 FY23 and it seems the company anticipated the HRC price growth as it increased coil inventory by $13.45 million quarter on quarter to $89.3 million. This move should lead to an improvement in margins. Speaking of the coil segment, I was pleasantly surprised that this unit booked a $3.26 million operating profit for Q3 FY23 and it seems that the main reason for this was the East Chicago and Granite City facilities. These two facilities generated net sales of $52 million and an operating profit of $4.6 million for the quarter. I was expecting their performance to gradually improve considering Friedman Industries CEO Mike Taylor was the President of Cargill's metals service center business from 2002 to 2014 when these facilities were part of the Cargill metals service center portfolio. However, I didn't expect them to be humming from a financial standpoint just a few months after their purchase.

Overall, I think the financial results of Friedman Industries for Q3 FY23 were a mixed bag but the prospects for Q4 looks strong due to rising HRC prices. The company expects a sales volume of 115,000 tons to 125,000 tons for the quarter and the increase is likely coming mainly from the ramp up of the Sinton facility, which I think should be moving close to breakeven.

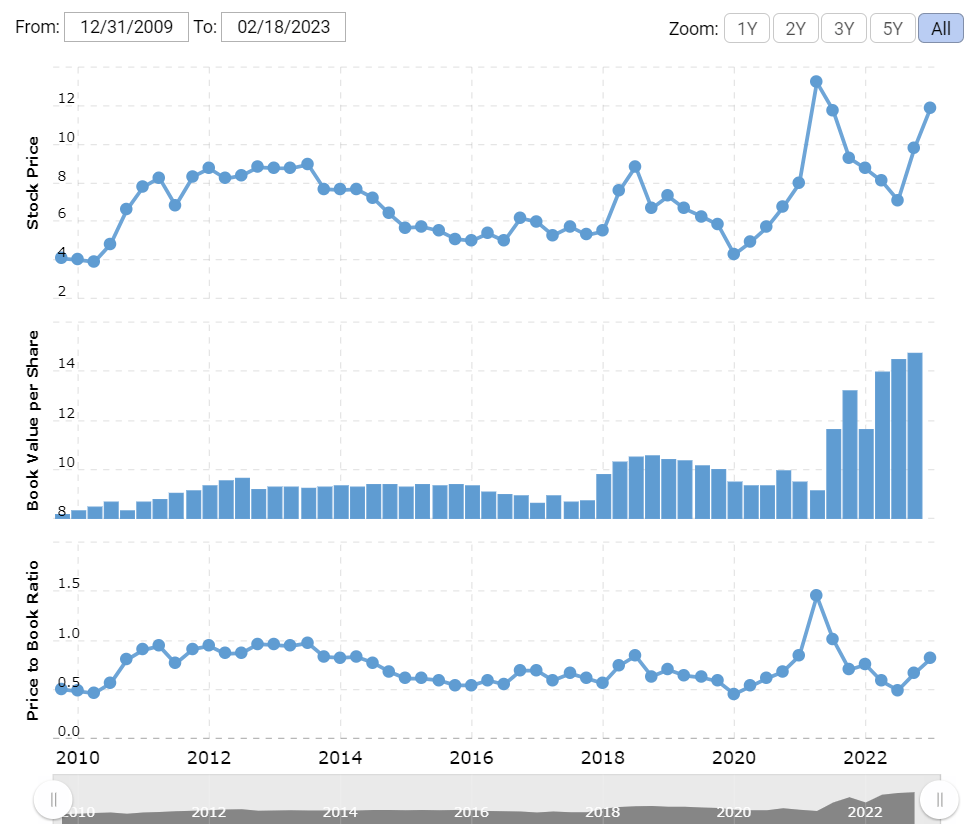

That being said, I think that Friedman Industries is becoming expensive from a price/book standpoint, and this is why I'm reducing my rating on the stock from strong buy to buy. Historically, the stock has rarely traded above 0.9x and is currently at 0.81x. The market valuation has increased by just over 30% since my previous article.

{kind=link}

Looking at the risks for the bull case, I think that there are two major ones. First, HRC steel prices have been unpredictable over the past few years due to macroeconomic policy changes and macroeconomic headwinds. It's possible that they could start to decline again in the near future which would have a negative effect on the margins of Friedman Industries. Second, it's possible that a large reason the market valuation is rising is the compelling EBITDA forecasts for the Sinton facility. Delays in the ramp up or underwhelming EBITDA results for the facility are likely to put pressure on the share price.

Investor takeaway

I think that the Q3 FY22 financial results of Friedman Industries were decent, but I was expecting more. In addition, I was surprised that the company stayed in the black thanks to East Chicago and Granite City. In my view, the Q4 FY23 financial results should be strong as HRC steel prices in the USA have increased by almost a third since November and I wouldn't be surprised if the comprehensive income for FY23 surpasses $30 million. However, I'm concerned that the price/book is approaching 1x and I plan to close my position around $14 per share.

For further details see:

Friedman Industries: Mixed Q3 Results But A Strong Start To Q4 (Rating Downgrade)