FYBR - Frontier Communications: Mixed Q2 Results But Network Adds And ARPU Expected To Grow

2023-11-22 21:22:46 ET

Summary

- Frontier Communications' 3Q23 results show mixed performance, with slight growth in consumer revenue but decline in business and wholesale segments.

- Consumer fiber broadband net adds are expected to increase, driving growth in ARPU.

- The company faces competition and operational difficulties in the broadband sector, impacting profitability and future prospects.

Overview

Note that I previously gave a hold rating for Frontier Communications ( FYBR ) due to the modest share price upside potential. I am iterating my hold rating as its 3Q23 results show mixed performance. Its average revenue per user growth is mainly driven by gift card incentives which if it was excluded, average revenue per user is flat. In addition, legacy products’ expected decline will continue to put pressure on its weak business and wholesale segment. It has a weak growth outlook and a modest share price gain.

Recent results & updates

On a consolidated level, 3Q23 total revenue was $1.44 billion, and adjusted EBITDA was $526 million. In 3Q23, consumer year-over-year revenue growth started to trend upward. $787 million in consumer revenue increased 0.3% year-over-year. Following its bankruptcy filing, this was the first quarter that FYBR's consumer revenue had grown on a year-over-year basis. I anticipate consumer year-over-year revenue growth to remain positive and accelerate in 4Q23 and in 2024 based on its outlook for ramping consumer fiber broadband net adds and accelerated growth in consumer fiber broadband average revenue per user [ARPU]. Revenue from business and wholesale, which was $634 million, fell 1.1% year-over-year. Management anticipates that total business and wholesale revenue in 4Q23 will decline slightly sequentially due to the decline in legacy products and the flat revenue from fiber.

One of the legacy products is FYBR’s exposure to copper, and it has been dragging them down. Pricing increases have appeared to mitigate the financial impact of consumer copper sub-declines and seem to have normalized. The enterprise and wholesale sectors continue to face difficulties as the growth in fiber services is more than offset by the decrease in copper. Due to lumpiness and a higher mix of copper services than customers, management indicated that enterprise and wholesale are expected to decline sequentially and year-over-year in 4Q23.

I anticipate higher levels of fiber broadband network adds in 2024. For the eighth consecutive quarter, it recorded positive total broadband net adds in 3Q23, with total fiber net adds of 79k and total broadband net adds, including copper disconnects, of 16k. Due to an accelerated rate of fiber expansion, I anticipate FYBR to continue to post positive and improving fiber broadband net adds in the future. In fact, management stated during the call that it anticipates 4Q23 fiber net additions to be higher than 3Q23's 79k and higher than 4Q22's 76k. In addition, management anticipates a higher total volume of net adds in 2024 compared to 2023.

The consumer fiber broadband ARPU of $64.49 grew 2.4% year-over-year. If gift card incentive impacts were excluded, the ARPU of consumer fiber broadband would have remained constant year-over-year. Given that management has stated that it has lowered the number of gift card promotions, implemented pricing adjustments, unbundled value-added services, and developed a pricing structure to encourage customers to move up the gigabit speed ladder, I anticipate year-over-year growth in ARPU in 4Q23 and accelerated consumer fiber broadband ARPU in 2024.

Valuation and risk

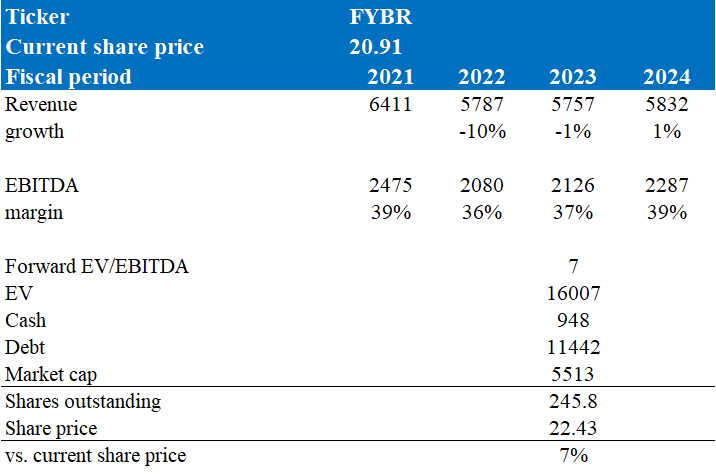

According to my model, FYBR's target price is $42 in FY24, representing a 7% increase, which does not provide enough safety buffers. My growth assumptions for FY23 and FY24 are in line with market estimates, and they were driven by the weak growth in consumer revenue and the anticipated decline in business and wholesale segments, which will offset the growth in consumer revenue. The decrease in business and wholesale segments is due to weaknesses in legacy products and fiber. On a brighter note, broadband net adds have been growing strongly and is expected to provide some form of support for FYBR. Although I note that broadband ARPU grew, it was driven by gift card incentives. If I exclude that out, it is flat.

{kind=link}

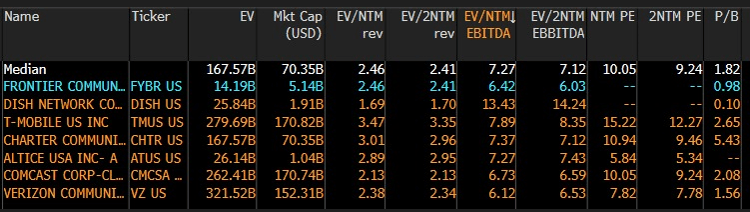

As of now, FYBR's forward EV/EBITDA stands at 6.42x, below its peers' median EV/EBITDA of 7.27x. In my opinion, I believe a 11.7% discount to peers is too much, and I will explain using peers' comparisons. FYBR’s current EBITDA margin of 30.65% is almost in line with peers’ median of 33.56%. Secondly, FYBR’s net margin of 9.75% is also close behind peers’ 10.26%. In terms of growth outlook, I take note that FYBR is expected to decline 1%, but peers are not that well off either, as they are only expected to grow 1%. By using a forward EV/EBITDA of 7x, the current share price vs. my target price does not seem to be attractive enough. Hence, I am maintaining my hold rating.

{kind=link}

Increasing competition and operational difficulties are two of the issues I would point out for the broadband sector. First, overbuilders, cable companies, and fixed-wireless access providers are all fighting for the same consumer base, making the market more competitive. Price wars, margin pressure, and even market share loss might result from this increased competition. Secondly, there are major challenges in laying fiber, which is essential for high-speed internet because of problems with the labor shortage and supply chain. These factors can increase expenses, restrict the ability to swiftly meet client demand, and delay implementation. The profitability and future development prospects of businesses operating in the broadband industry may be greatly impacted by both of these threats.

Summary

FYBR’s 3Q23 results show a mixed performance. For the first time since filing for bankruptcy in, it saw a slight increase in consumer revenue in 3Q23 when compared to the same period in the previous year. It is anticipated that this upward trend will continue, driven by an increase in consumer fiber broadband net adds and growth in ARPU. On the other hand, the business and wholesale categories experienced some decline and is putting pressure on FYBR. Although there was an increase in consumer fiber broadband ARPU, it was driven by gift card incentives. ARPU stays flat when these incentives are taken out of the mix. With my target price close to its current price, it does not provide enough safety buffers. With these, I am maintaining my hold rating for FYBR.

For further details see:

Frontier Communications: Mixed Q2 Results, But Network Adds And ARPU Expected To Grow