FYBR - Frontier Communications Parent: Disappointing Revenues And No Catalyst In Sight

2023-06-07 14:32:03 ET

Summary

- Frontier Communications Parent faces significant risks due to share dilution, negative cash flows, and a high net debt/EBITDA ratio.

- The company's valuation is considered too high, with an 80x forward price-to-earnings ratio and uncertain revenue growth.

- Better investment alternatives in the market, such as Charter Communications Inc, offer lower valuations and shareholder value through dividends or buybacks.

Investment Thesis

Despite the significant position and presence, Frontier Communications Parent Inc (FYBR) hasn't been able to translate into growing revenues that much. Looking at the historical chart of revenues they look flat out horrible.

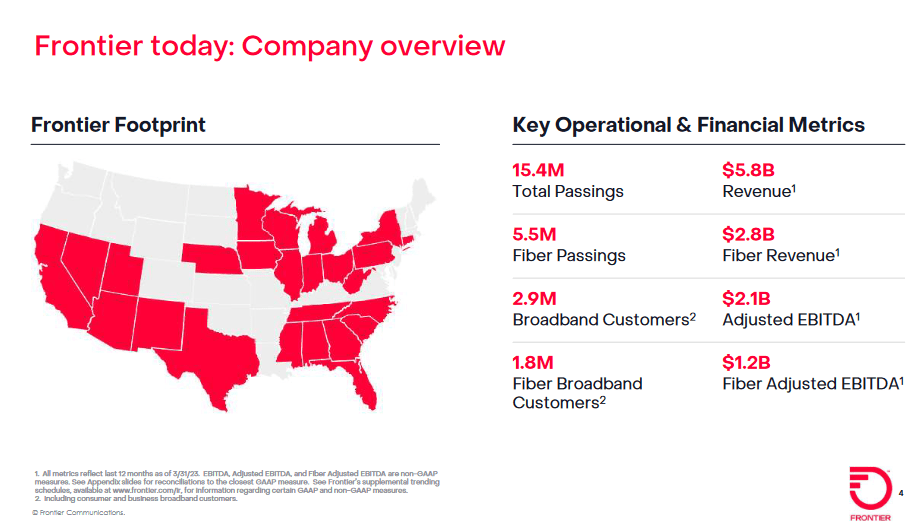

Company Market (Investor Presentation)

{kind=link}

From close to $9 billion in 2018 to under $6 billion in 2022. Pair that with significant share dilution over the years and this seems to be a bad place to put capital right now. I don't see a catalyst for the company and the actions the company has taken over the years seem to indicate they don't operate in the best interest of shareholders. Frontier is a sell from me.

The Company

Frontier Communications serves a wide range of markets throughout the United States, including both urban and rural areas. Their primary focus is on delivering reliable and high-speed broadband internet services, ensuring customers have fast and dependable connectivity. Furthermore, Frontier Communications also provides digital TV services, offering a diverse selection of entertainment options and channels to meet the diverse preferences of its customer base.

Present in the broadband market, FYBR is growing its customer base at a solid rate, 19% YoY as of the last report. The broadband market is expected to grow quickly, much because of a push for further access in the US. FYBR is trying to capture this growth too. The company currently is making a majority of their revenues from data and internet services, but voice services and video services also make up about 30% together as well.

The company is investing heavily into fiber as part of a purpose the company calls Building Gigabit America, meant to connect everyone to the internet and in the long run drive revenues for FYBR as they act as a service provider. In the first quarter of 2023, the company managed to build in fiber to 339,000 locations. Establishing them as a significant presence in the industry.

Financials

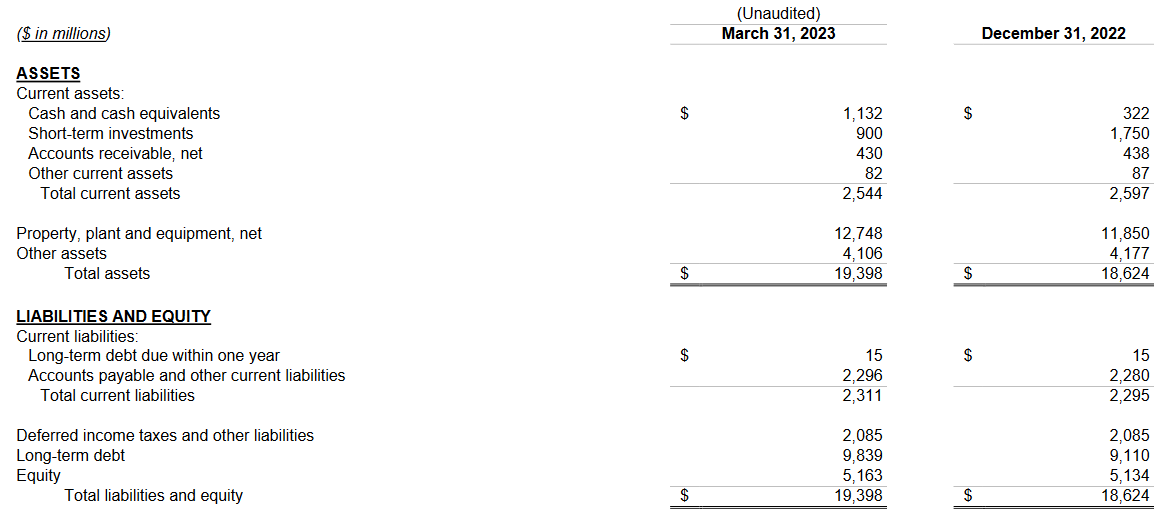

Looking at the financial state of the company the perhaps single piece of improvement or positive thing I notice is the cash position increase on a quarter-over-quarter basis. Going from $322 million to $1.1 billion is a step in the right direction. But this is quickly dismissed when you look at the long-term debts the company has.

Balance Sheet (Earnings Report)

{kind=link}

With close to $10 billion in long-term debt, I am worried that share dilution will continue to happen to help raise capital to meet payments on the debt. History tells us this seems to have happened over the last few years already, and with negative levered cash flows I don't see a convincing reason for the company to stop such a practice. That makes investing in FYBR right now very risky as dilution hurts an investment immensely over the years.

What more worries me is the net debt/EBITDA ratio sitting a little too high for my liking, right now at 3.26, which is above my preferred threshold of 3. Looking ahead, the company is projecting an adjusted EBITDA of around $2.11 - $2.16 billion for the full year of 2023. That would mean the ratio mentioned previously would increase further even if the company doesn't take on more debt. But as FYBR already filled up with over $700 million in long-term debt just QoQ I think the debt position will increase further during 2023 and the negative levered cash flows will do nothing to help with it.

Company Leverage (Earnings Report)

{kind=link}

To conclude the financial part of the program, I think the company is in a tough spot right now with negative cash flows not able to help pay off debt and the dilution of shares seems necessary to not default on any payments. This means uncertainty for investors and you should have to pay an 80x earnings multiple for it like you currently need to.

Company Headwinds

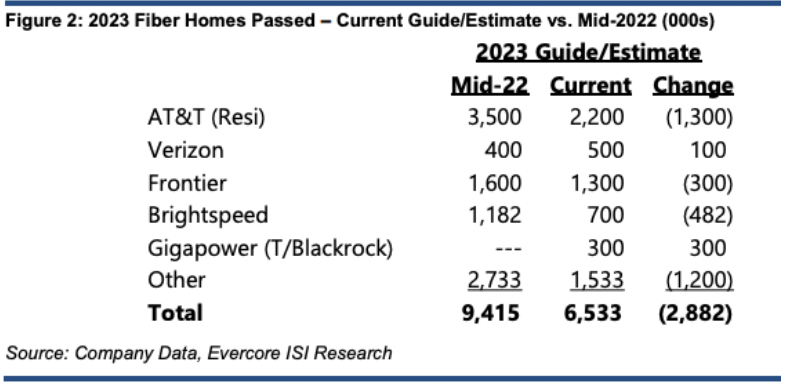

As mentioned before in this article I think the dilution of shares is one of the major risks that faces investors. It hurts an investment greatly and even more so as the share price has plummeted perhaps as a result of it. Down 30% during the last 12 months is rough. Looking ahead, some might say that fiber will be a major tailwind for the company, but it seems companies working on building it out are slowing down . The uncertainty does help the investment scenario around the company.

Company Guidance (Investor Presentation)

{kind=link}

With that said, having to pay 80x forward earnings for revenues that are incredibly hard to predict is far too high. With negative cash flows, such a high valuation should make most investors turn right around instead. Moving into the coming quarters, I think the revenues will be key to watch as they will tell the story about the investments the company is making and whether the fiber buildout is resulting in an increasing top line or not.

Valuation

Looking at the valuation of FYBR right now the forward p/e sits at 77, and when looking ahead to 2024 it only gets worse from here. EPS estimates are expected to be $0.07 per share in 2025, which would make the current valuation even more overvalued and risky. Where most investors might see the potential in a company like FYBR is the fiber build-out they continue to do. But until we actually see this translating into better margins I think it's just wishful thinking for now.

{kind=link}

With a high p/e, you often expect to see very strong growth in either revenues or significant margin expansion for a company. With FYBR you aren't getting any of those it seems. The qualities of the company aren't there to justify the current price. With a debt/cash ratio of 8.69, there is in my way too high to pay. There is also a solid argument to be made that the company will struggle with current liabilities as a result of the negative levered FCF. These uncertainties would usually result in a company getting a very low premium. But with FYBR the hope seems to be that they can grow quickly as demand for broadband increases. The 19% customer growth the company had for broadband seems to have been a catalyst for the share price. But I think it's a matter of time before the price compresses as a result of the lack of margin improvements the company will have over the coming quarters. With FYBR having a poor track record of improving margins I think further dilution will continue. In 2027 estimates suggest FYBR will generate around $6 billion in revenues, with decreasing margins I think that a 5% net margin seems fair to predict for that year. If there isn't any further dilution, which seems unlikely, the EPS would land around $1.22. Using a 14x multiple, the same as the sector, the share price would land at about $17, predicting there isn't any further dilution. That's just an 11% upside potential in 5 years. That's without collecting any dividends too. This highlights the lack of value I see with FYBR right now.

If you still want to gain exposure to this market then I think there are better-valued companies out there than FYBR right now. A company like Charter Communications Inc ( CHTR ) has a much lower valuation and a strong history of buying back shares too. These are important things to look out for in this industry in my view as it greatly helps make a long-term position more convincing of there are already things set in place to help it.

Final Words

To conclude the article, I think that FYBR is not a buy right now, nor is it a hold. The company has a very rich valuation that presents a lot of risks to investors and with negative levered cash flows the outlook remains quite unsure. I am rating it a sell. I don't see any value for investors at these prices and the nearly $10 billion debt position will be a struggle for the company to handle over the coming years if they can't efficiently increase margins. The industry is expected to grow, but there are far better-valued companies with exposure to it compared to FYBR right now, that also offer value to shareholders through either dividends or buybacks.

For further details see:

Frontier Communications Parent: Disappointing Revenues And No Catalyst In Sight