CA - Frontier Lithium: Valued At Just 10.5% Its PFS-Derived NPV

2023-09-15 16:21:00 ET

Summary

- Frontier Lithium is a Canadian company with a flagship hard rock lithium project in Ontario, Canada trading at just 10.5% of its PFS-derived after-tax NPV.

- Ontario & Quebec are becoming major EV / Li-ion battery hubs, attracting global players, enticed by government pledges of support {tax breaks, infrastructure builds, etc.}.

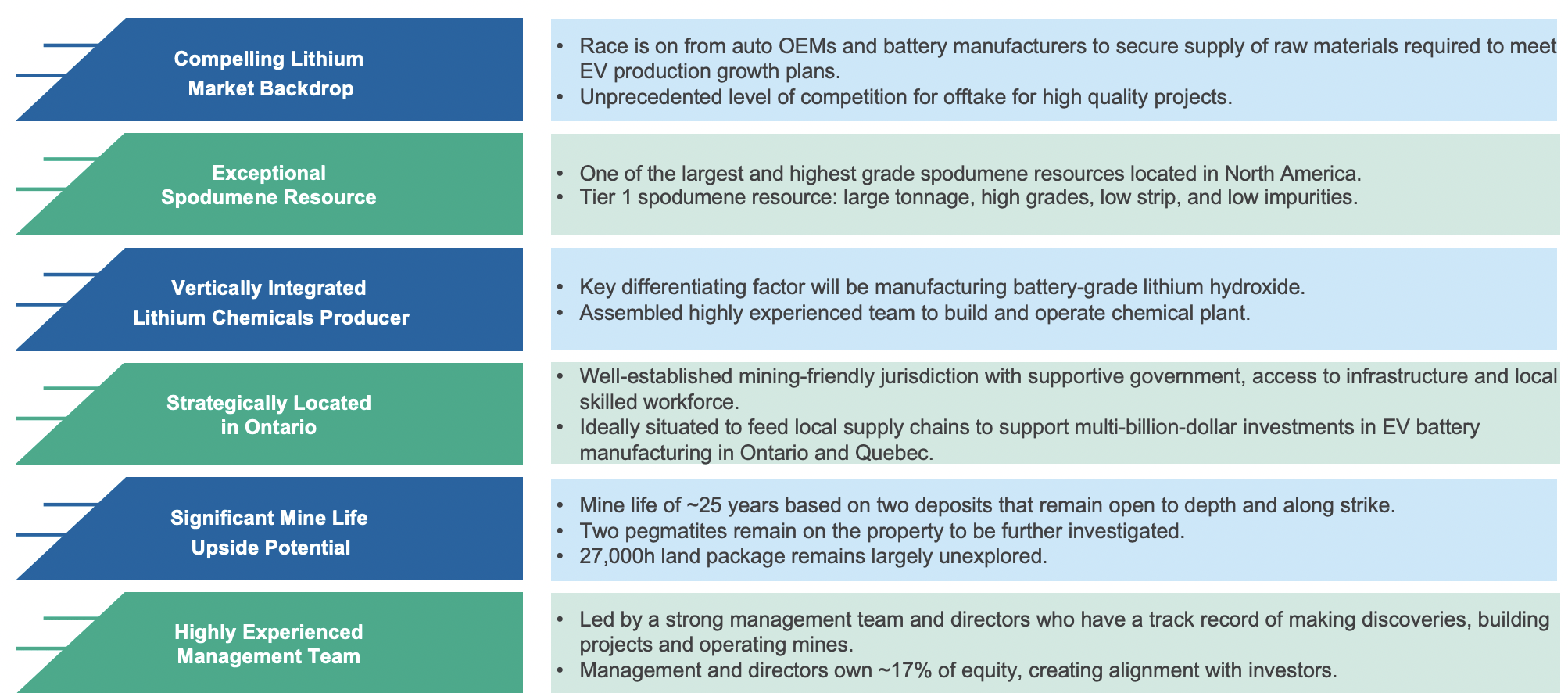

- Frontier's world-class project has a large (and growing), very high-grade, low-impurity resource -- making it a prime takeover target.

- Once a strategic investor gets involved, the project could be upsized, de-risked and possibly reach commercial production of hydroxide & carbonate sooner.

- M&A in lithium space is poised to takeoff. Sigma Lithium, Patriot Battery Metals & Liontown Resources are three of the hottest takeover speculations. All three have robust hard rock projects.

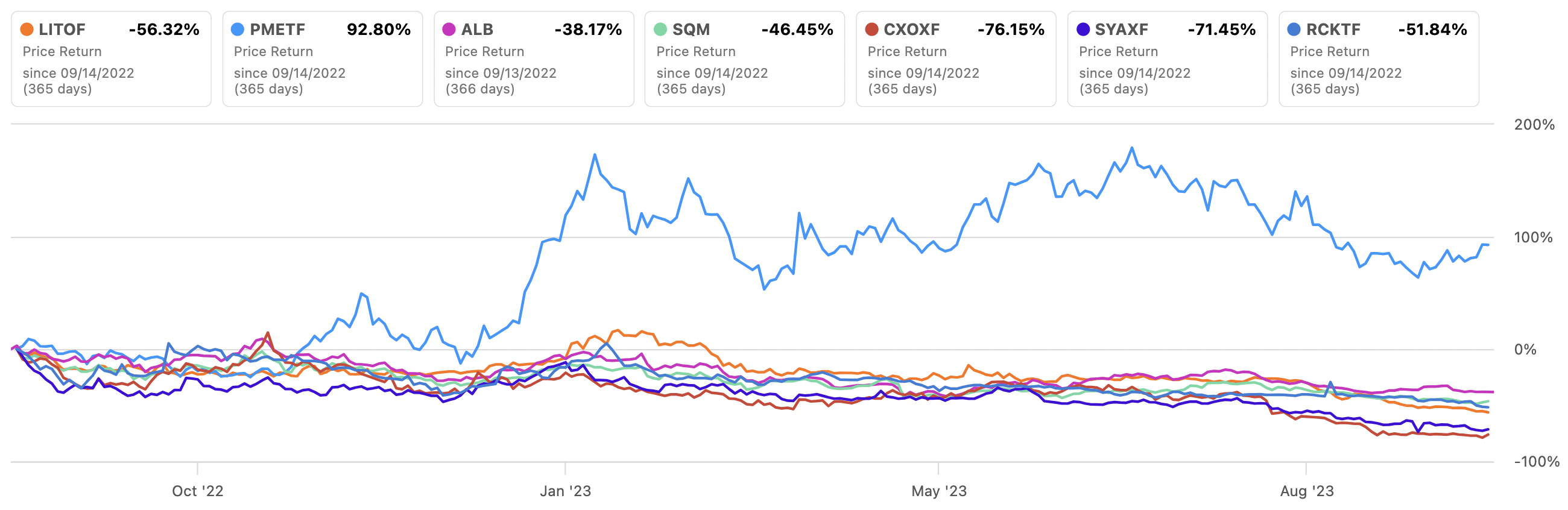

Lithium companies large & small, producers, developers, explorers, hard rock, sedimentary, brine, Direct Lithium Extraction ("DLE") plays -- almost all have been crushed. Many are down > 50% from 52-week highs. The following chart shows some of the worst performers among better-known names.

{kind=link}

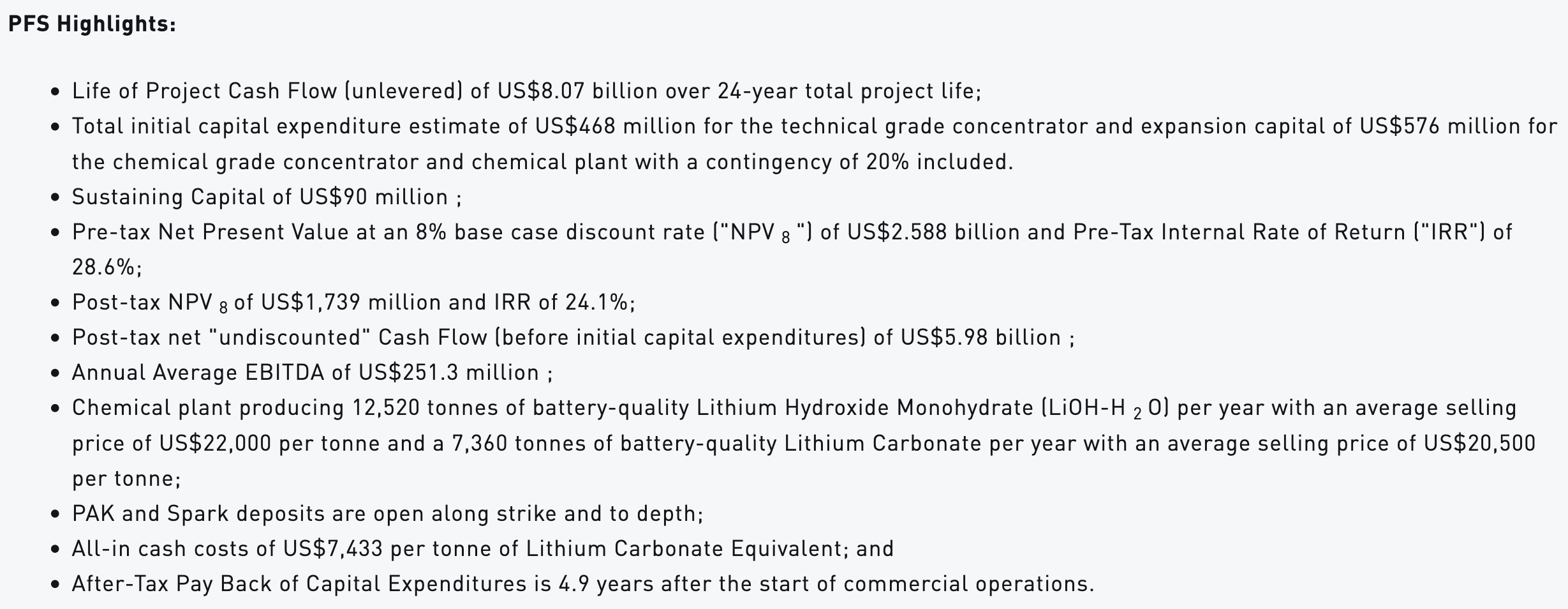

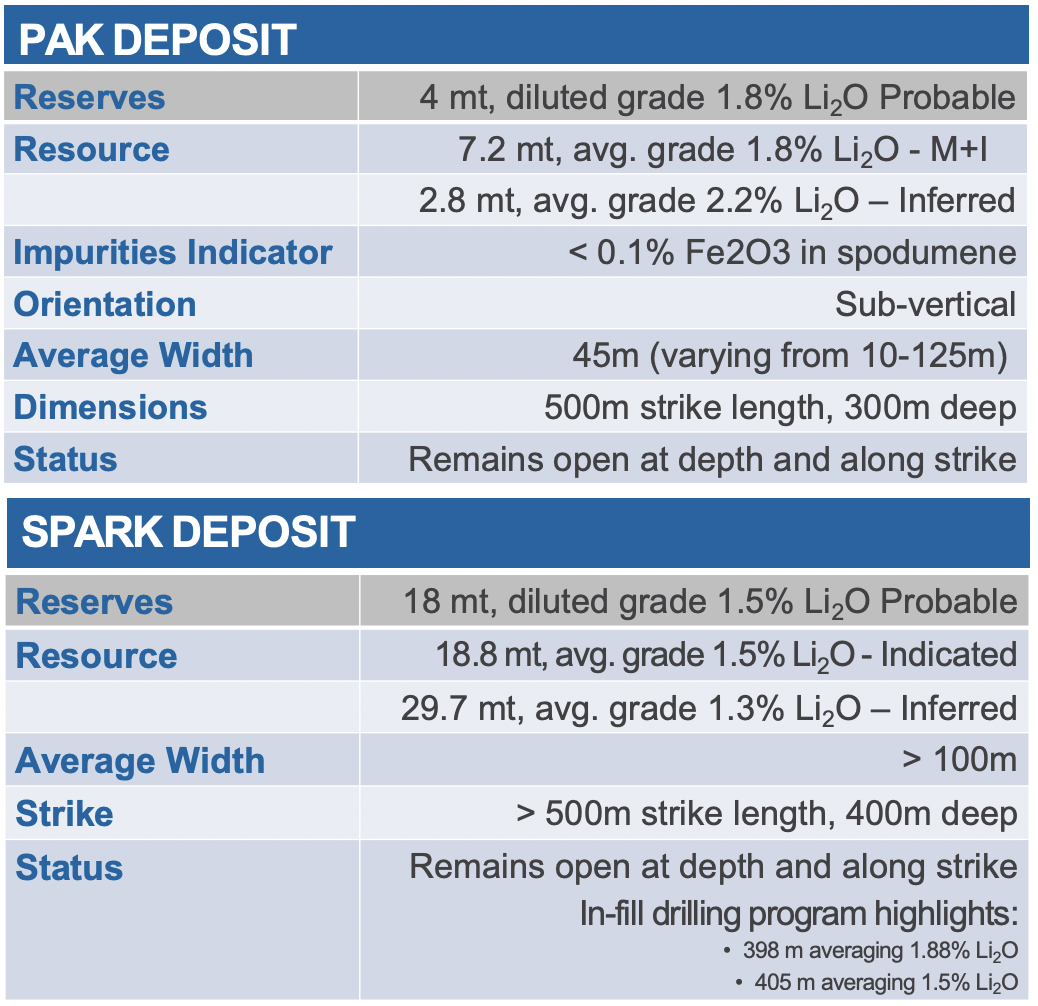

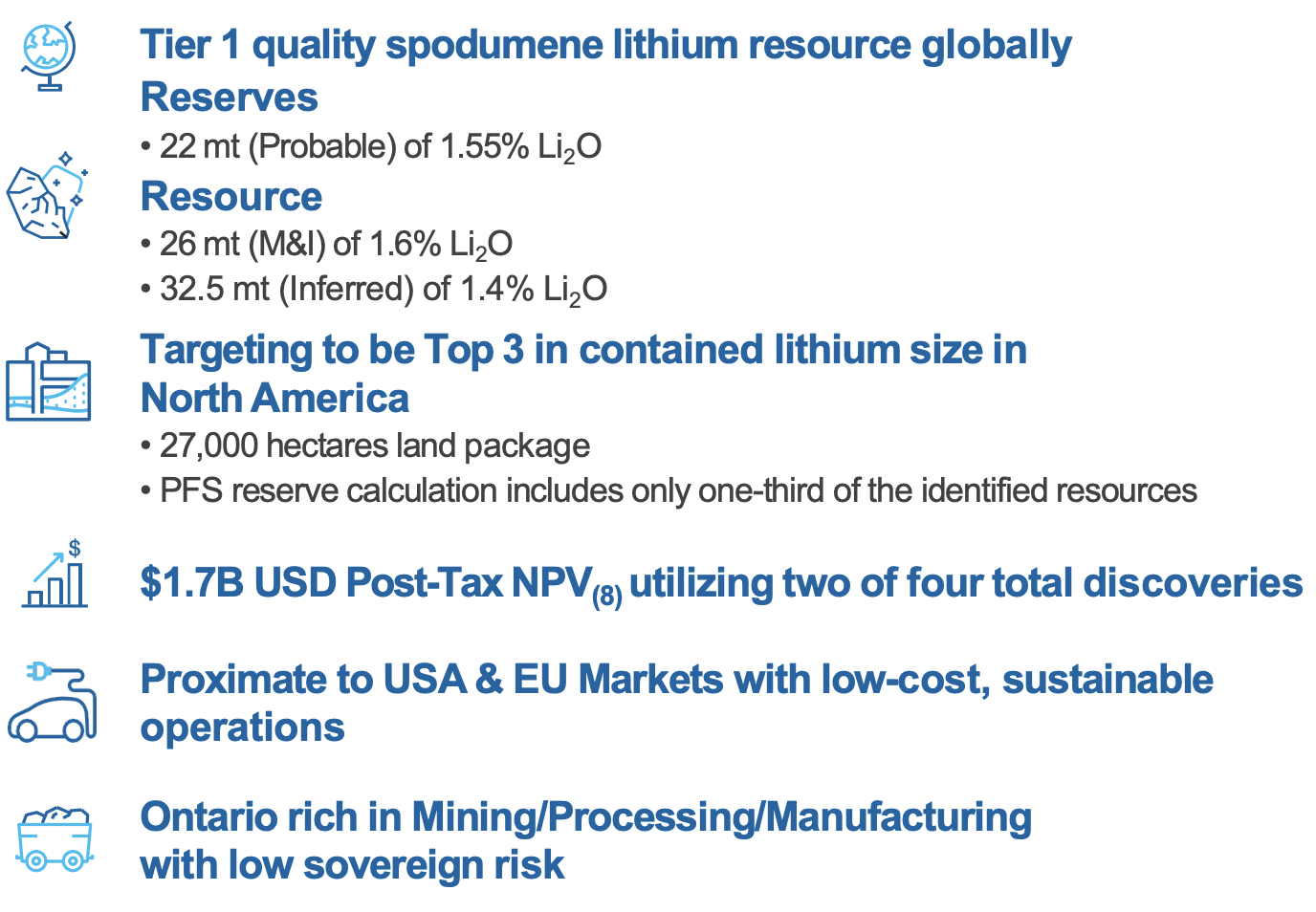

This article is about Ontario, Canada's Frontier Lithium ( OTCQX:LITOF ) / ( FL:CA ). In May, the Company transitioned into a moderately-advanced developer by delivering a strong Pre-Feasibility Study ["PFS " ]. Its flagship PAK project has a $1.74 billion after-tax NPV and a 24% IRR. Inexplicably, Frontier is trading at just 10.5% of that NPV figure. {see corp. presentation }

On September 6th CIBC published a detailed research report with a 12-18 month target price of $2.94 vs. the current share price of $0.82. The price hit $2.25 in February, months prior to the release of the robust PFS. Frontier had $16 million in cash at 6/30/23 and zero debt. Its enterprise value {market cap + debt - cash} = ~$180M, on 228 million shares outstanding.

{kind=link}

Lithium prices are down meaningfully over the past seven weeks, but many pundits believe they will rebound by year end due to upcoming seasonal strength in Electric Vehicle sales and China's recently announced $72 billion, 4-yr. electric vehicle incentive, its largest program ever. Other critically important factors to consider include the following...

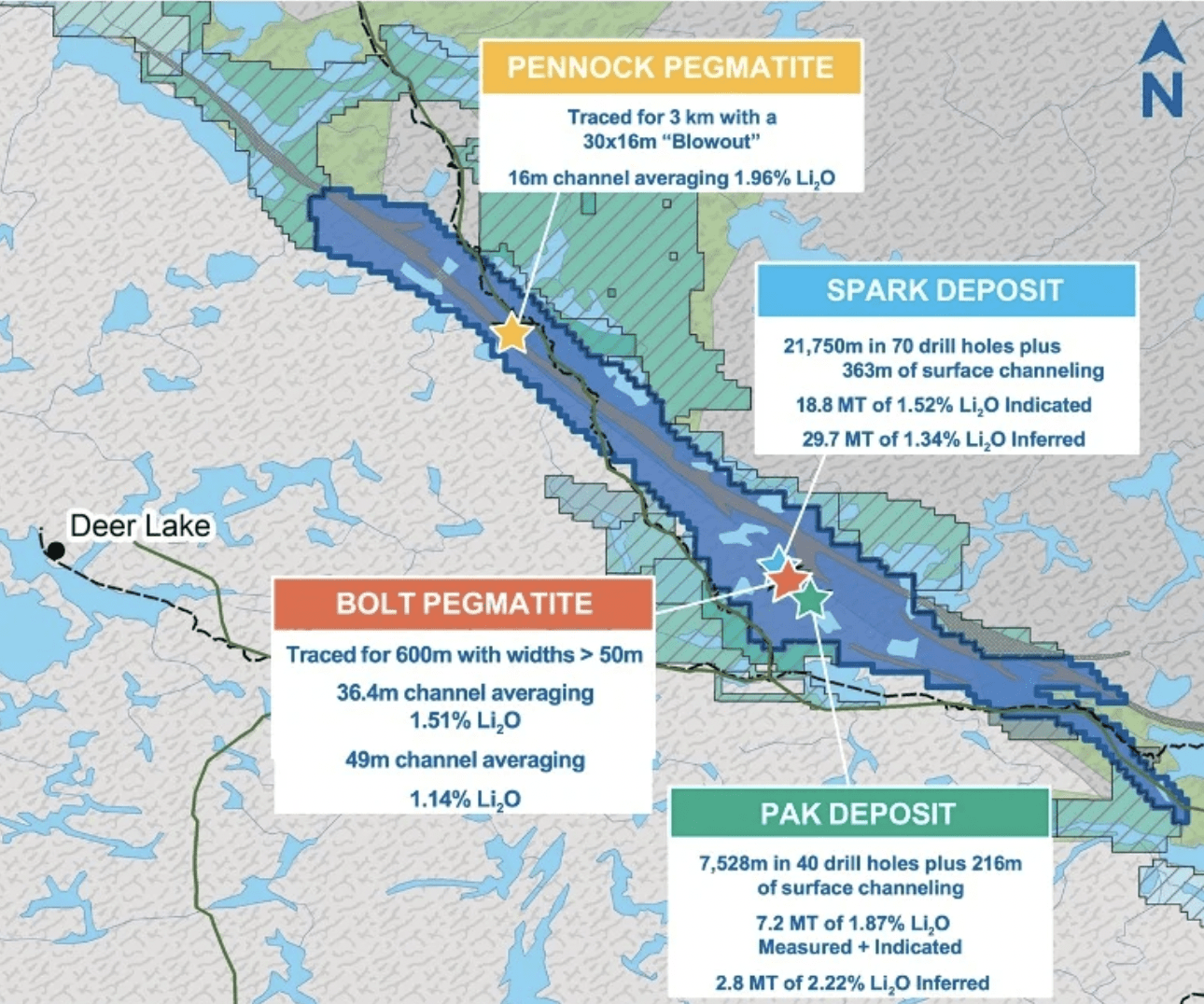

PAK Lithium project in the Tier-1 mining jurisdiction of Ontario, Canada

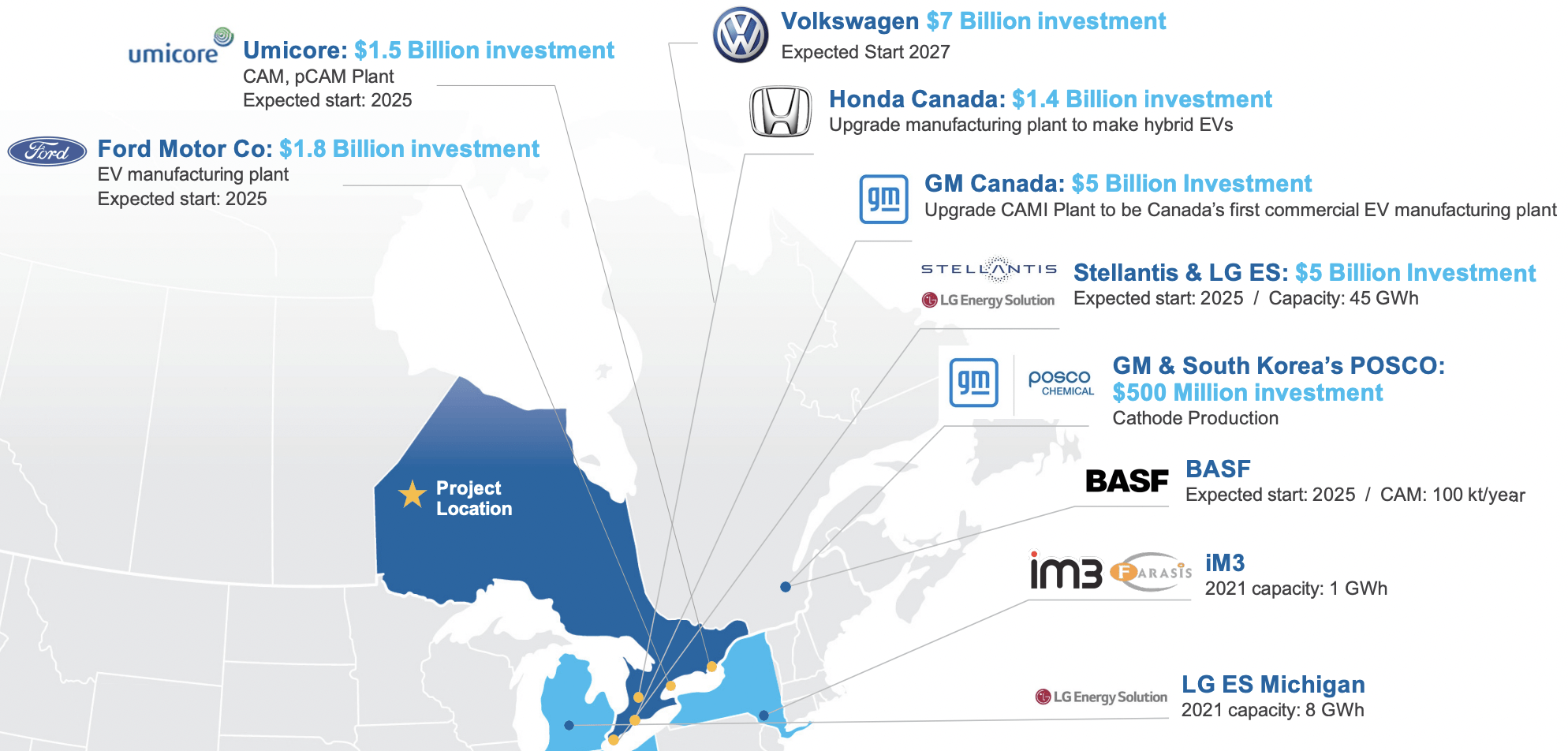

Ontario & Quebec are fast becoming world-class EV / Li-ion battery hubs. Canada has one of the greenest and lowest cost electricity grids on the planet due to nearly ubiquitous hydroelectric & nuclear power.

Ontario borders the world's third largest EV market [USA] and is closer to most European markets than Africa, Brazil, S. America & Australia. The Ontario & Canadian Federal governments are pledging long-term financial, logistical & regional infrastructure support [details pending] to global EV OEMs & Li-ion battery makers.

So far, Ford ( F ), Volkswagen ( OTCPK:VWAPY ), Stellantis ( STLA ), GM ( GM ), Honda ( HMC ), Toyota ( TM ), Umicore ( UMICY ), LG Energy Solutions, SK On, POSCO ( PKX ), Northvolt & BASF ( BASFY ) have announced big plans in Canada.

{kind=link}

Conventional hard rock mining (no DLE, sedimentary [clay] or brine risk)

Projects proposing to use DLE technologies have considerable scale-up risk. There are no existing DLE operations (at meaningful commercial scale) . DLE will require additional time (years, not months) to permit, fund, construct, commission & achieve nameplate capacity. Likewise, there are no commercial sedimentary [clay] lithium operations yet.

Lithium brine operations are well established in Chile & Argentina. However, very few new brine projects have come online in the past decade. Only a JV between [Ganfeng ( GNENF ) / Lithium Americas ( LAC )] started producing this year, while Eramet ( ERMAY ), Zijin Mining ( ZIJMF ) & POSCO have brine projects in Argentina ramping up in 2024-25. Hard rock projects in friendly places are needed to fill the gap.

Very high grade lithium resource

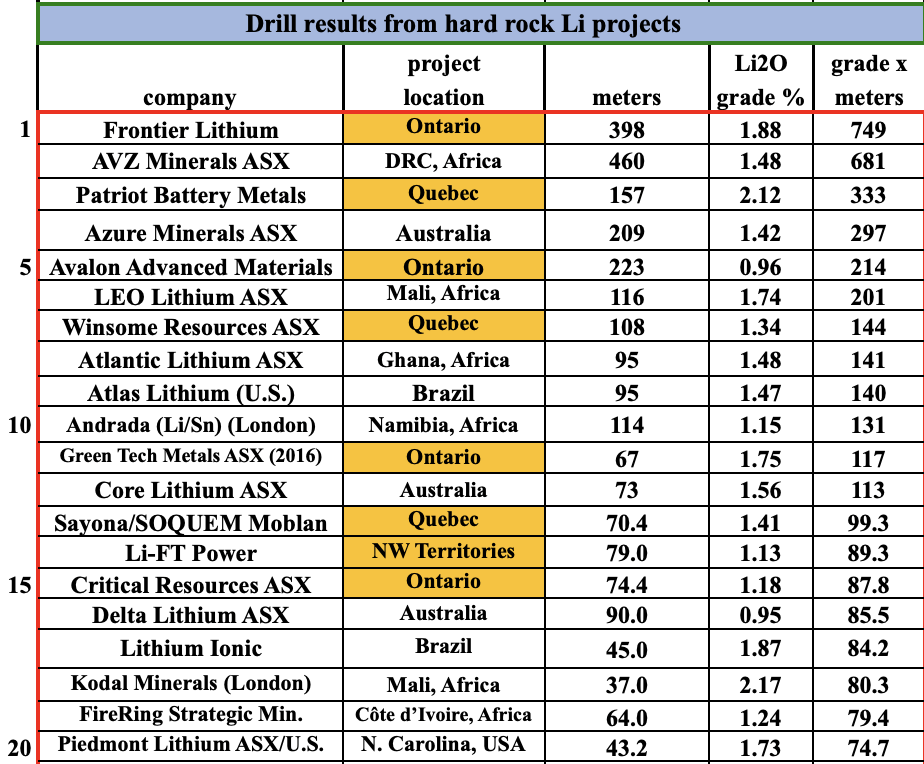

The following chart shows the best hard rock drill results as measured by [ Li2O grade x interval width ]. Frontier stands head & shoulders above the rest, 4x the average of the next five Canadian-based projects. {See February, 2023 PR }.

{kind=link}

Only Albemarle's ( ALB ) & Tianqi's ( TQLCF ) Greenbushes mine, AVZ Minerals' ( AZZVF ) Manono project and SQM's ( SQM ) & Wesfarmers' ( WFAFY ) Mt. Holland mine have a higher Measured, Indicated & Inferred resource grade than Frontier's at 1.50% Li2O.

Large-scale resource with ample room to grow

Management announced an exploration target of 100 million tonnes of mineralized material. Assuming a 20% haircut to the grade on the remaining tonnes found, that would be 3.3 million tonnes Lithium Carbonate Equiv. ("LCE"). {see short corporate video about project resources}

There's no assurance the Company will achieve 100M tonnes, but it has already booked an 58.6M tonnes = 2.2M tonnes LCE , a globally significant resource. Subsequent to delivery of that resource, substantial drilling has been done. An updated resource estimate is expected later this year.

{kind=link}

Only hard rock projects controlled by Albemarle, Pilbara Minerals ( PILBF ), soon to be merged Allkem/Livent ( AKE:CA )/( LTHM ), LEO Lithium ( LLLAF ), Patriot Battery Metals ( PMET:CA ), Tianqi, Mineral Resources ["MinRes'] (OTCPK: MALRF ), Wesfarmers, IGO Ltd. ( IPGDF ), Sigma Lithium ( SGML ), Sayona Mining ( SYAXF ) and Liontown Resources ( LINRF ) have booked more (attributable) tonnes of LCE, but the average market cap of those companies is well into the billions. By contrast, Frontier is valued at ~$180 million.

Frontier a prime takeover target

In my view, possible acquirers of Frontier include; Rio Tinto ( RIO ), POSCO, Glencore ( GLNCY ), Teck Resources ( TECK ), MinRes, Pilbara, Albemarle, SQM, Allkem/Livent, IGO Ltd. & Wesfarmers.

Smaller prospective suitors -- Sibanye-Stillwater ( SBSW ), Sigma Lithium ( SGML ), Liontown & Lithium Americas. Liontown is the subject of an active takeover attempt by Albemarle. Sigma just announced in a press release multiple indications of "interest from potential strategic partners, including global industry leaders in the energy, auto, batteries & lithium refining industries."

{kind=link}

A large, experienced partner could turbo-charge project economics

As impressive as the Company's PFS already is, if/when a multi-billion dollar partner gets involved, the economics of the PAK project could be enhanced in the upcoming Bank Feasibility Study ("BFS"). Annual production could be increased, perhaps by a lot. And, initial production of lithium hydroxide & carbonate could possibly be pulled forward a year or two. Shareholders would have to give up a meaningful interest in the project to get the financial backing, but it would be well worth it.

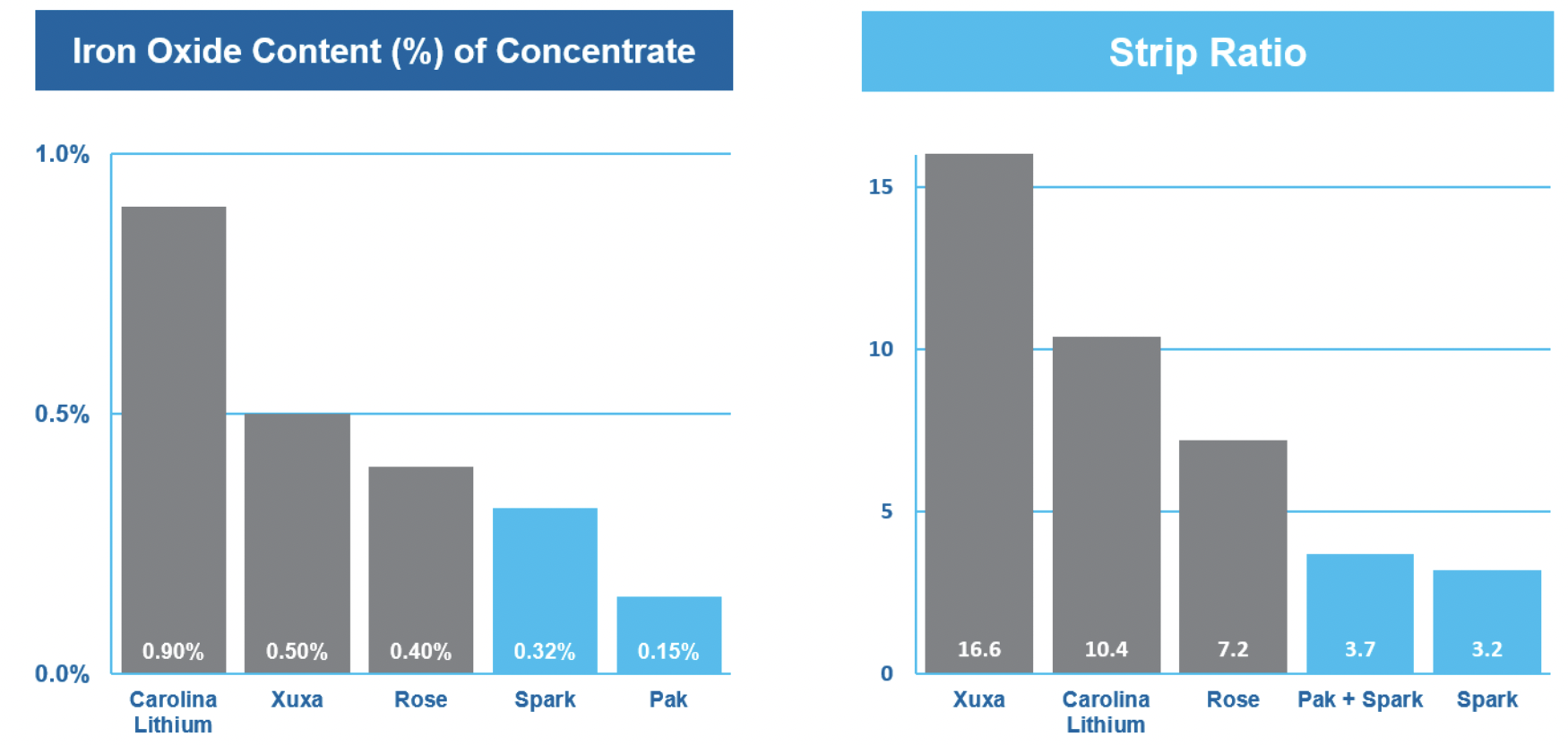

Low impurities, low strip ratio

The combination of large size (with room to nearly double the resource) , very high grade, low impurities & low strip ratio makes Frontier's PAK project quite attractive.

{kind=link}

The most pressing risk factors are; 1) lack of key regional infrastructure (a remote location), 2) raising capital in a weak market, 3) lack of a strategic partner or off-take agreements, 4) long timeline (six years) to initial hydroxide production, and 5) Li spot prices in decline.

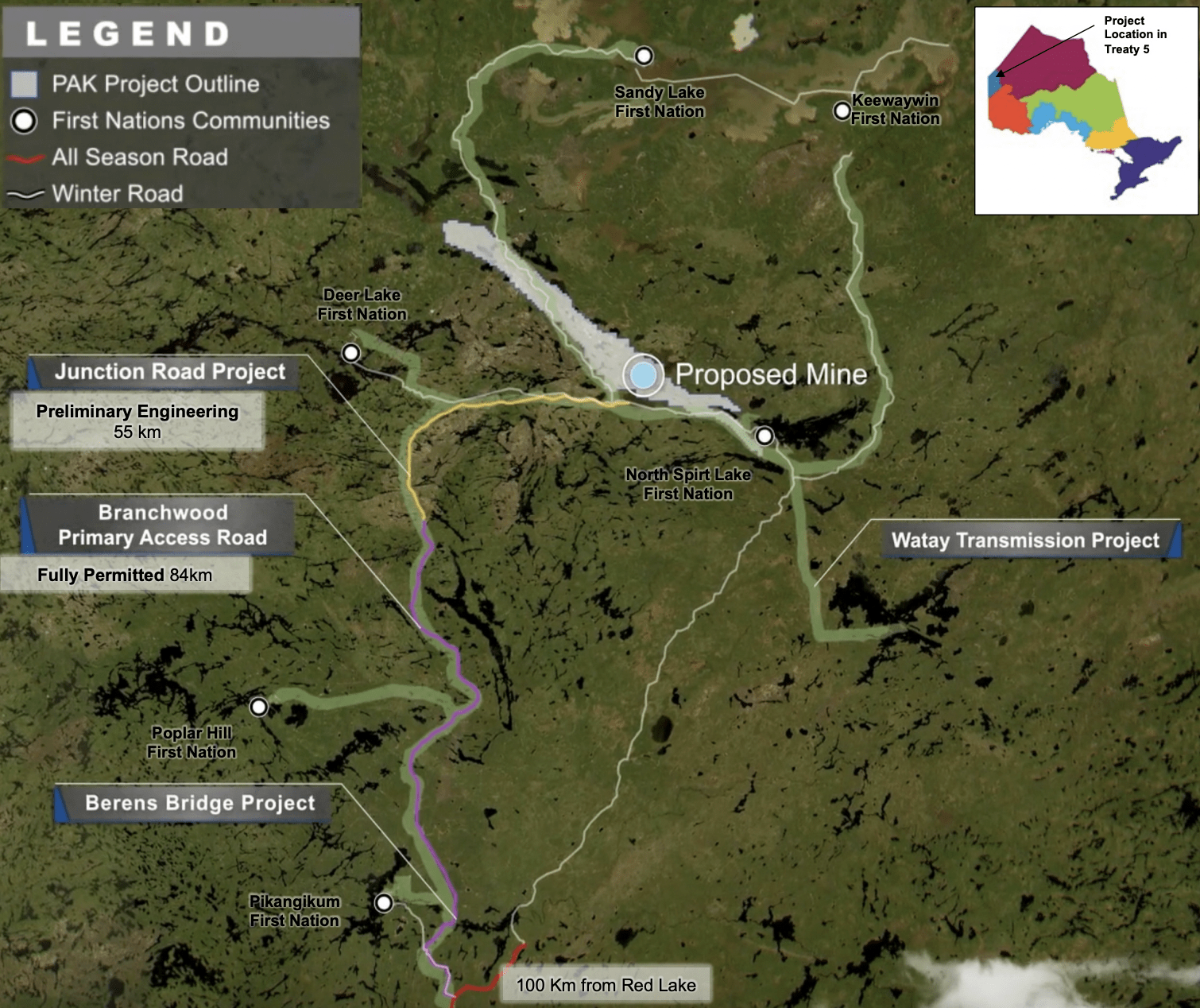

Regarding infrastructure, the main issue is a designed & partially permitted 135 km stretch of road (and a bridge) that Frontier expects will be built and paid for by government as it will be utilized by multiple companies and First Nation communities.

More specifically, an all-season road needs to be built and the existing winter road upgraded & extended. It's possible that a portion of the proposed road extension will be funded by Frontier, and they would then seek reimbursement from government.

This is NOT a deal breaker! This road/bridge does not need to be completed for several years. The total cost to Frontier, in a worst case scenario, is probably in the $10s of millions , especially as they would look to share costs with other companies. A key consideration is that First Nation communities would benefit from the road/bridge, making it more likely (in my view) to be funded by government.

{kind=link}

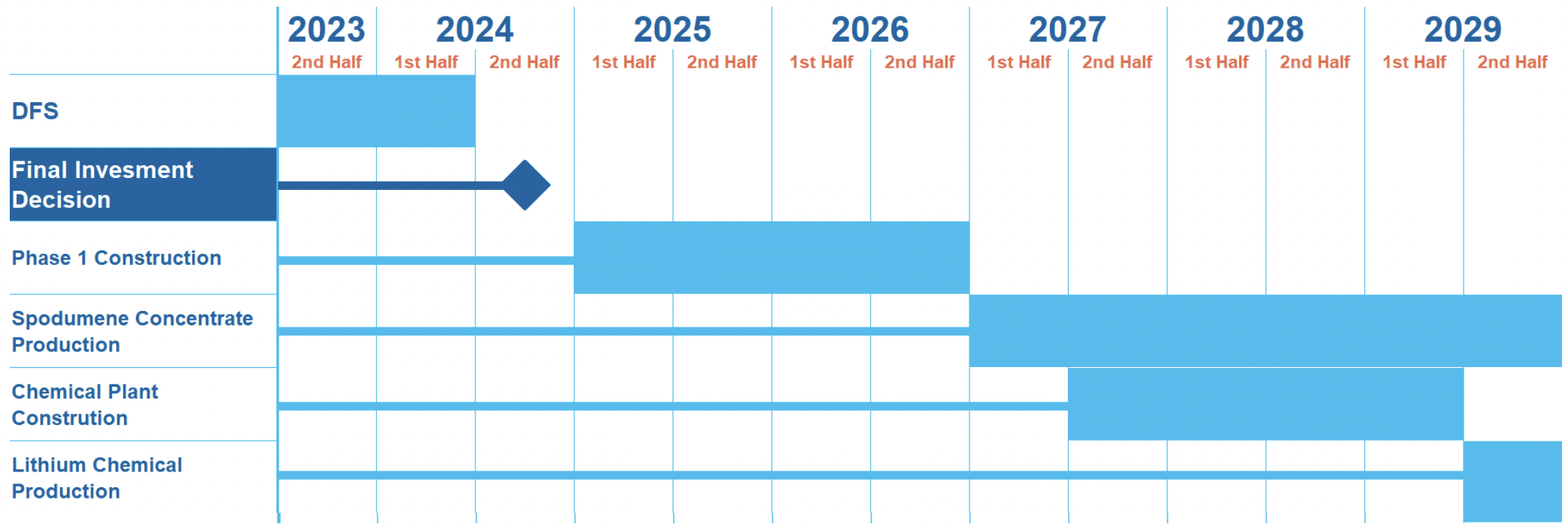

In the meantime, management can embark on Phase 1 of the operating flow sheet -- spodumene concentrate production & transport to a third-party refining facility -- with relatively modest enhancements to existing road/bridge logistics.

I believe that proposed Canadian hard rock projects, even remote ones, have far better visibility towards first production than their African counterparts. Moreover, African projects are thousands of kms (weeks of travel time) from end markets. By contrast, the PAK project is hundreds of km (1-2 days) from existing & future OEM & battery factories across southern Canada & the northern U.S.

Geopolitical issues are rising to the top of investor concerns as China & Russia scramble to lock up African supplies of battery materials in the DRC, Mali, Zimbabwe, Ghana, Angola & Namibia.

A common fear among junior mining investors is the ability to raise equity capital. Frontier had ~$16M in cash and zero debt as of June 30th. While not a lot of liquidity, it can be stretched until 2nd qtr., 2024 as the lion's share of outlays come from drilling. Frontier is done drilling for 2023.

{kind=link}

Readers should recognize that not all cash will come from equity issuance. Potential non-equity sources include; 1) the sale of a royalty or stream 2) government and/or institutional loan facilities / debt packages, 3) free money grants from government entities, 4) upfront payment for a portion of initial production via off-take agreements, 5) the sale of an interest in the project [ at the project level, no new shares issued ], and 6) mine equipment financing.

All together, Frontier might be able to fund up to 100% of cap-ex from these sources, while retaining a significant economic interest in the PAK project. This is especially true if spodumene concentrate sales can contribute meaningful cash flow from 2026-2029 as planned.

Lithium Royalty Corp. ( LITRF ) has provided funding on Canadian projects owned by Allkem, Power Metals ( PWRMF ), Green Technology Metals ( GTMLF ), Grid Metals ( MSMGF ), ACME Lithium ( ACLHF ), Winsome Resources ( WRSLF ) & Sayona Mining ( SYAXF ).

{kind=link}

Regarding the lack of a strategic partner , that's only a problem if there's no interest, which is not the case. Management is narrowing the list of prospective partners down to three. Off-take agreements are more likely to be signed after an update on the road/bridge situation and/or more explicit and detailed pledges of support by government.

As mentioned, I believe there are many lithium companies, diversified miners, commodity traders, EV OEMs & lithium-ion battery makers that would be good strategic fits. Even Oil & Gas Majors have started investing directly in lithium, mostly through wastewater brine/DLE projects.

Hard rock projects like PAK are far easier to build compared to unproven, ultra-low lithium grade wastewater brine/DLE plays.

The seemingly long timeline to lithium hydroxide / carbonate production of six years is par for the course for major lithium projects at this stage. Historical work on PAK dates back a decade. Readers should consider looking ahead 3.5 years to the intermediary step of spodumene concentrate production . If successful, the total amount of equity needed in the coming years could be smaller than feared.

{kind=link}

Regarding the falling lithium carbonate spot price in China, it's a very volatile & thinly-traded index. The quarterly contract price reported by SQM is more representative of the market -- down 42% from peak. By contrast, the spot price is down ~74% (in US$).

In April, spot bottomed around $23k/tonne and then rallied over 80% before the onset of the current contraction. Today's spot price is $26,226/t. Many pundits expect the spot price to rebound above $30k/t in the coming months.

Potential near-to-intermediate-term catalysts include; clarity around the road/bridge, drill results, updated resource estimate, securing a strategic partner, off-take agreements, permitting milestones, obtaining government grants and/or loans, delivery of a BFS, and the start of construction for phase 1 spodumene concentrate production.

Another possible catalyst could be the headline grabbing takeover of a peer. Australia's Liontown & Azure Minerals ( AZRMF ), U.S. based Sigma Lithium & Canada's Patriot Battery Metals ( PMETF ) are considered prime takeout candidates. Sigma's share price is up ~15% since September 13th on the news that several, "global industry leaders" have made indicative proposals.

{kind=link}

There are fewer than 10 world-class lithium projects that will be highly sought after near-term producers over the next five years. Frontier is one of them, but it won't be first to be acquired. As companies like Liontown & Sigma get taken out this year and next, all eyes will be on the dwindling list of major projects like Frontier's PAK.

Even if Frontier's stock were to rebound to half of CIBC's $2.94 price target, that would be a gain of +79%.

The stock traded as high as $2.25 in February, prior to the release of its excellent PFS. I think the risk/reward proposition is compelling at $0.82/shr. {see corp. presentation }

For further details see:

Frontier Lithium: Valued At Just 10.5% Its PFS-Derived NPV