DIS - Funko: A Lesson In Dollar Cost Averaging

2023-05-22 12:36:38 ET

Summary

- The past several months have been really tough for Funko and its investors.

- Shares plunged due to poor financial results. But we have started to see a recovery and shares look attractively priced at this time.

- The firm and my investment in it also provides an interesting look into how dollar cost averaging can pay off in a big way.

As those who follow my work know, I run a very concentrated portfolio. At any given point in time, I like to have between five and 10 holdings in my portfolio. As of this writing, I currently have nine different stocks that comprise all of my invested assets. And the largest of these happens to be Funko ( FNKO ), an enterprise that's engaged in the production of consumer entertainment toys, namely the Funko Pops!. After seeing its share price climb as high as $27 and change late last year, the stock plummeted after market forces turned against it. The 52-week low point for the company is currently $7.14. That's quite a tumble, and it has scared investors into thinking that the future for the company might not be so bright. Recently, shares of the business have started to rise back up. This is based on renewed optimism centered around the company's profitability for the current fiscal year.

Given the massive drop that shares of the company experienced, many investors likely bailed out of their position. Or if they did hold on, they made sure to buy little to no additional shares. But I would argue that this is a bad approach to take. If you believe that a company was undervalued at a higher price, and shares continue to decline, dollar cost averaging down can make a great deal of sense. This is the strategy that I took over the past several months. And although I was unable to pick up any sizable portion of the stock at the low point, I did pick up enough to drastically improve my outlook from an investment perspective. In what follows, I will cover not only the recent financial picture of the company, but also talk about why this particular firm is a great example of why dollar cost averaging is a good strategy that investors can invoke during difficult times.

Shares are still very attractive

I don't want any confusion regarding my stance on Funko. When I first started buying shares of the company in March of 2022, at a price of $16.51 apiece, I believed that the stock was worth around $28. My goal had been to sell it once it reached that point. If only I had placed that target a bit lower, I would have captured a fantastic return. This is because, by Aug. 1, shares of the company hit a high point of $27.79. By that date specifically, I owned a sizable stake in the company at a weighted average purchase price of $17.23. Had I sold out at the time, I would have had a realized gain of 61.3%. But alas, my assessment of the right price to sell at was off just a bit.

This ended up being a rather painful mistake. By the end of August, shares of the company had dropped to $22.27. And after announcing some rather painful financial results in early November, they plunged to less than $8 per share in the course of a single day. Since then, management has come out with some additional financial results. And those, combined with the market’s recognition that it had overreacted, units of the company closed at $12.86. Before I get into my dollar cost averaging experience, I would first like to cover these recent financial results.

{kind=link}

Author - SEC EDGAR Data

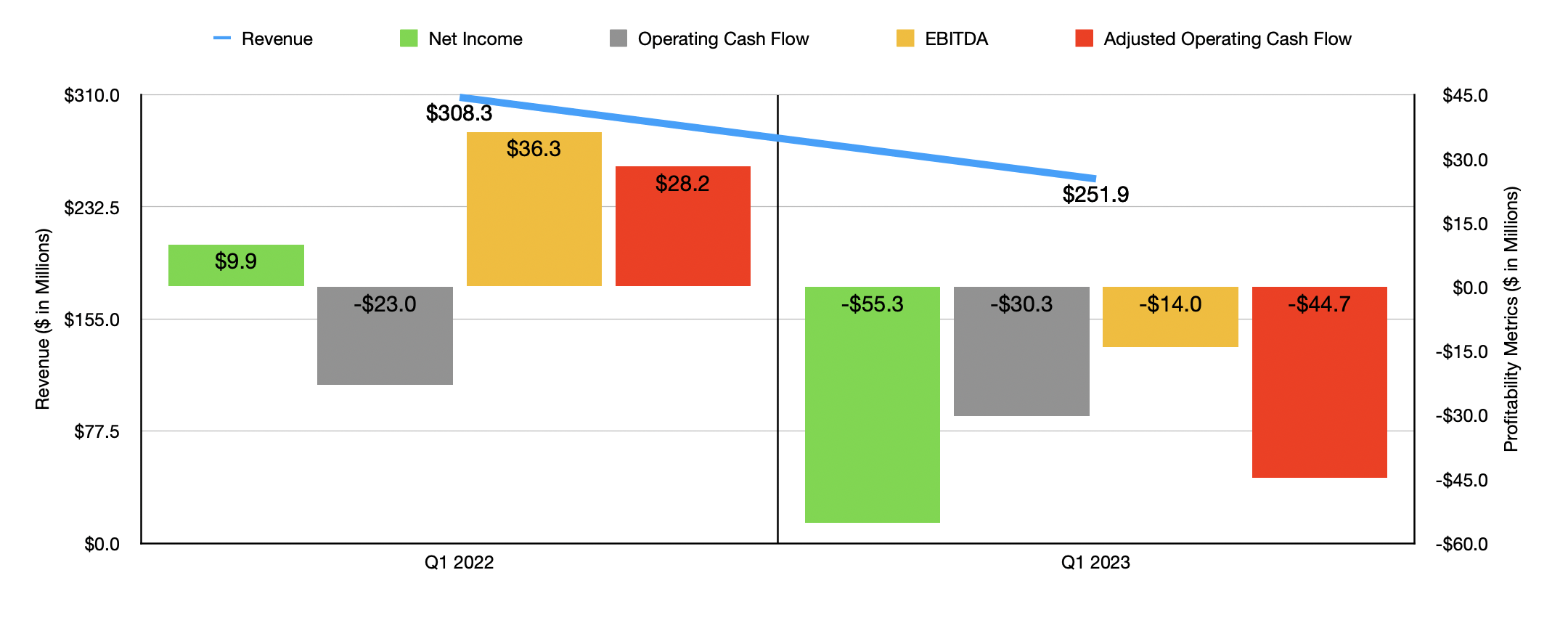

In early May, management announced financial performance figures for the first quarter of the company's 2023 fiscal year. In a vacuum, these results were horrible. Revenue for the quarter came in at $251.9 million. That's down 18.3% compared to the $308.3 million the company reported only one year earlier. This plunge in revenue was driven largely by decreased sales that the company made to specialty retailers, e-commerce sites, and distributors. In the US specifically, pain was particularly pronounced. Sales here at home plunged 23.4%. By comparison, Europe reported a 4% sales increase year over year.

While the top line results for the company were definitely bad, the results on the bottom line were even worse. The company went from generating a net profit of $9.9 million in the first quarter of 2022 to generating a net loss of $55.3 million in the first quarter of this year. Operating cash flow went from negative $23 million to negative $30.3 million. If we adjust for changes in working capital, the picture would have been even worse, with a metric turning from $28.2 million to negative $44.7 million. Meanwhile, EBITDA for the company plummeted from $36.3 million to negative $14 million.

When it came to guidance for the 2023 fiscal year as a whole, management had some bad news for investors expecting revenue growth. Instead of forecasting revenue that would be between flat and up 5% compared to 2022, which is what management had forecasted when they announced financial results for the final quarter of last year, they revised sales lower rather substantially. Now, revenue is expected to contract by between 10% and 15%. When I first saw some of these headline news items, I expected shares to take another step lower. But there were some positive developments that caused my pessimism to turn into optimism.

For starters, management is now forecasting profitability that's higher than what they thought it would be when they announced financial results in the final quarter of last year. At that time, they said that EBITDA would likely come in this year at between $50 million and $75 million. That range has now been revised higher to between $65 million and $75 million. The second really positive development is that management is working really hard on reducing inventories. And so far, the results are quite impressive. Inventories at the end of the most recent quarter totaled $191.6 million. Although that was meaningfully higher than the $161.5 million the company had at the end of the first quarter last year, it was lower than the $246.4 million that the company had at the end of the final quarter of 2022. It's unlikely that this decrease was due to seasonal fluctuations. After all, from the final quarter of 2021 to the end of the first quarter of 2022, inventories for the business fell by only $4.9 million. The other positive development relates to this reduction in inventory. During the quarter, management recorded a $30.1 million inventory write down and it plans to physically destroy that inventory no later than the end of the second quarter. That helps to explain some of the company's profitability issues in the first quarter compared to the same time last year.

{kind=link}

Author - SEC EDGAR Data

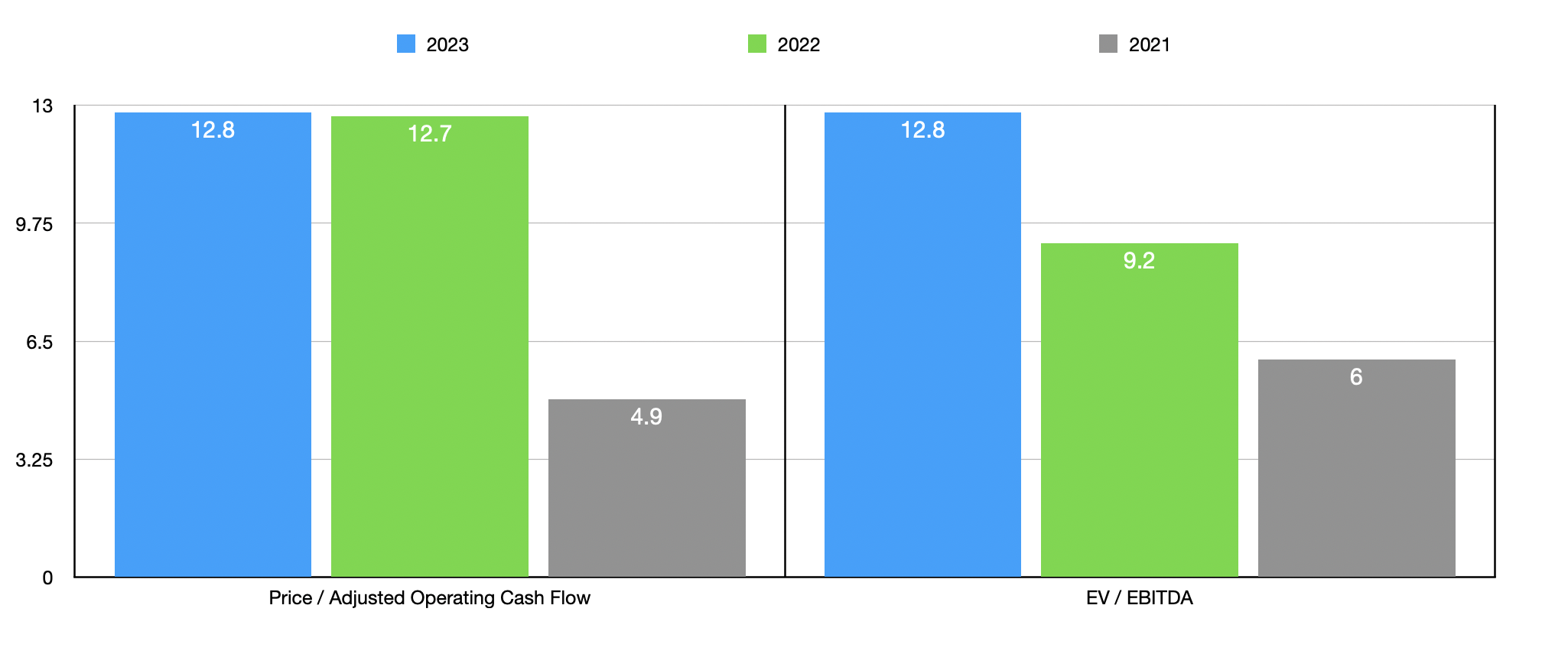

If we take midpoint guidance for EBITDA, this indicates to me that operating cash flow for 2023 will probably be around $47.3 million on an adjusted basis. Given these figures, shares of the company are quite attractively priced at this moment. As you can see in the chart above, both the forward price to adjusted operating cash flow multiple and the forward EV to EBITDA multiple come in at 12.8. Also in the table, you can see how shares are priced using results from 2121 and 2022. The picture using the 2022 data is not terribly different than the 2023 estimates. Though in the event that financial performance does improve substantially beyond this point, reaching, for instance, levels that are more similar to 2021, shares could be worth a great deal more than what they are trading for today.

My dollar cost averaging experience

{kind=link}

Author - SEC EDGAR Data

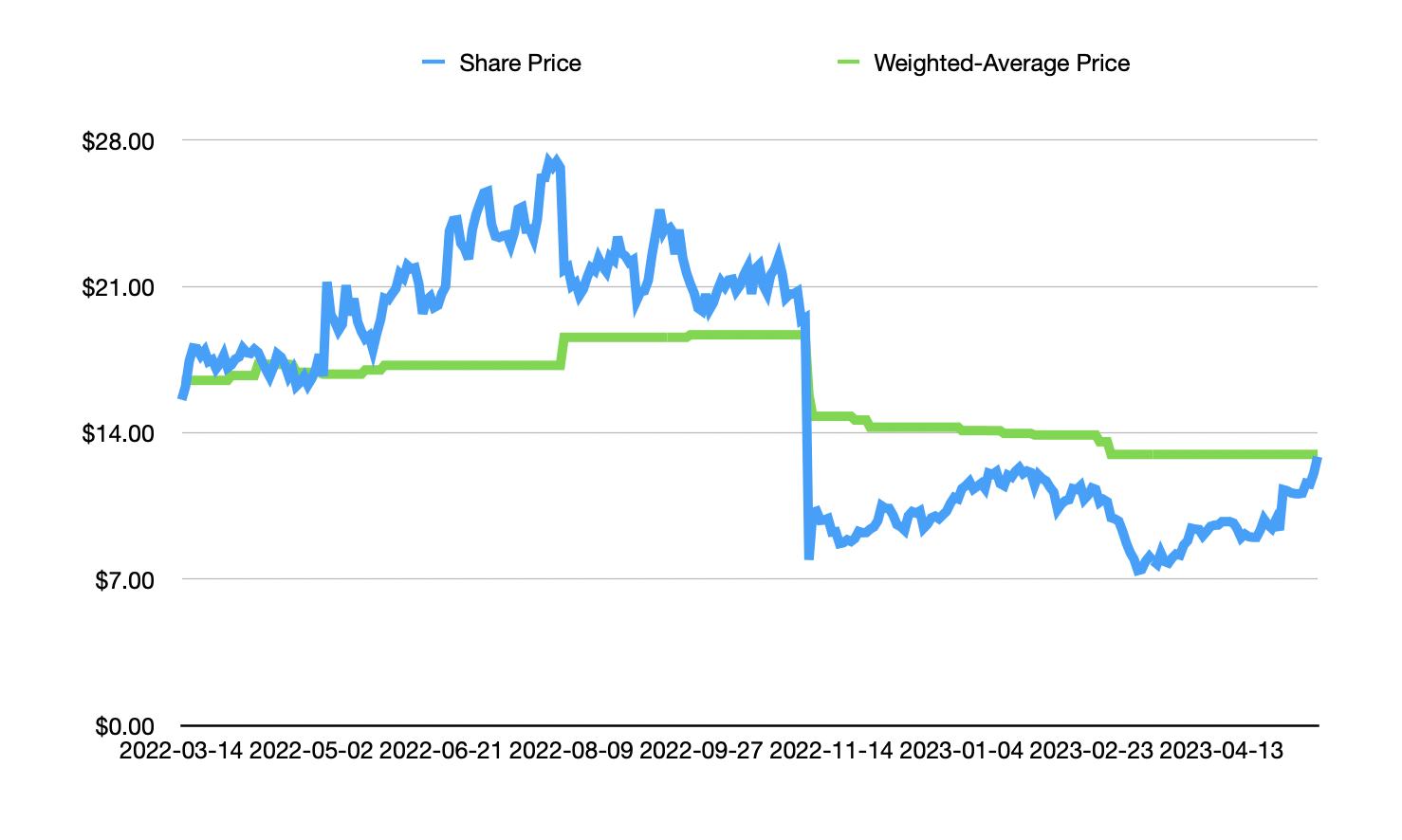

In general, I believe that dollar cost averaging is a great strategy when you firmly believe that the company you purchased shares of is still significantly undervalued after taking a tumble. In the chart above, you can see the share price that Funko has traded at from the time I bought stock in March of last year to the present day. You also can see the weighted average price that I paid for units during this time. As shares of the business plunged, I bought substantially more. And with income that I was able to continue putting toward the stock, I continued to lower my cost basis and the company by buying up more along the way.

To put this in dollar terms, at the high point, the highest weighted average cost that I had in the company came out to $18.69. This occurred on Sept. 22 of last year and continued until early November when I started picking up additional units after the stock plunged. The cheapest shares that I purchased at that time had a price of $8.91. By the end of November, my weighted average price on units had fallen to $14.27. But I continued to buy on the way down, including my most recent purchase in early March at $9.27. By this point, my price on shares had dropped to $12.97.

{kind=link}

Author - SEC EDGAR Data

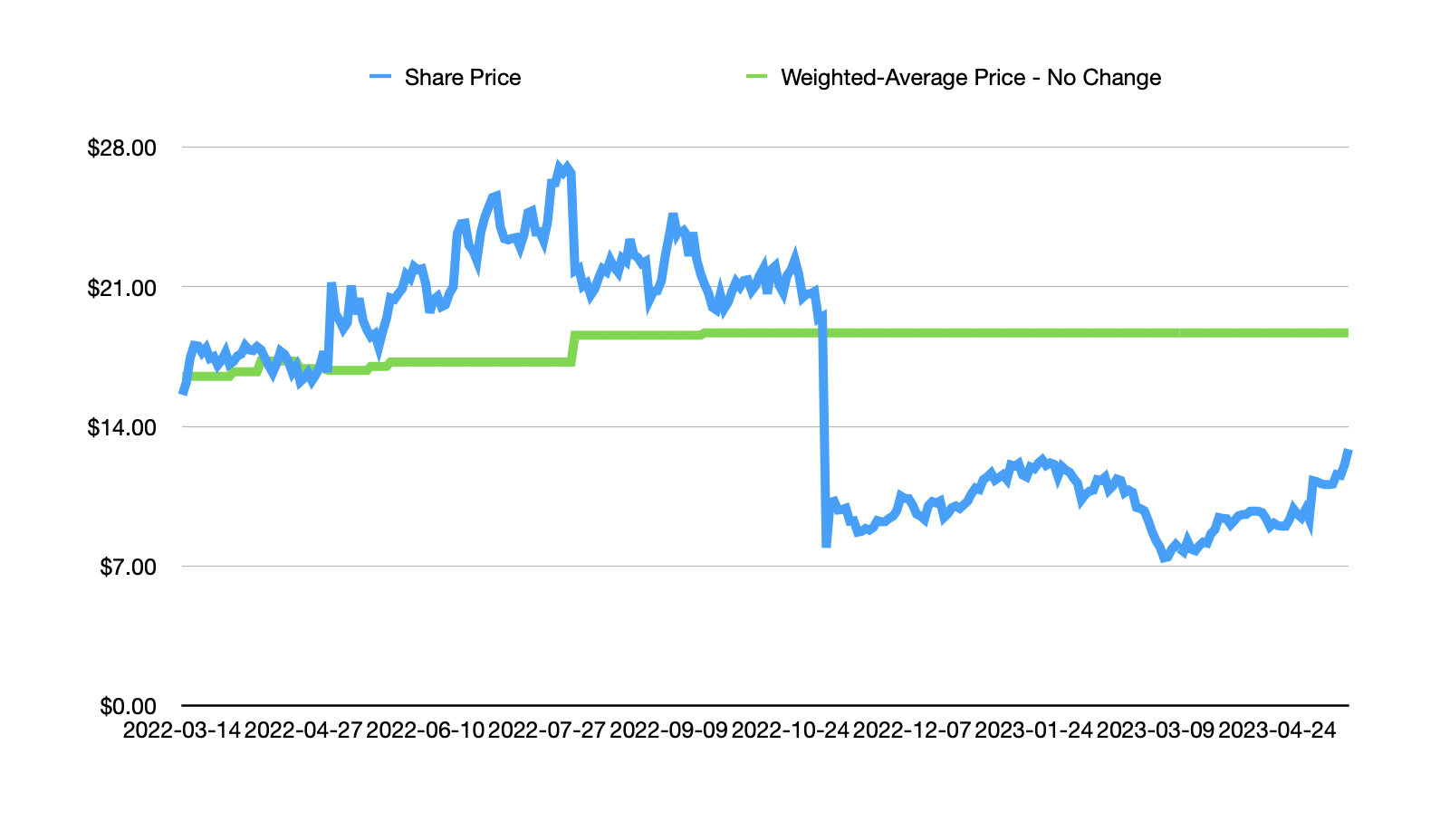

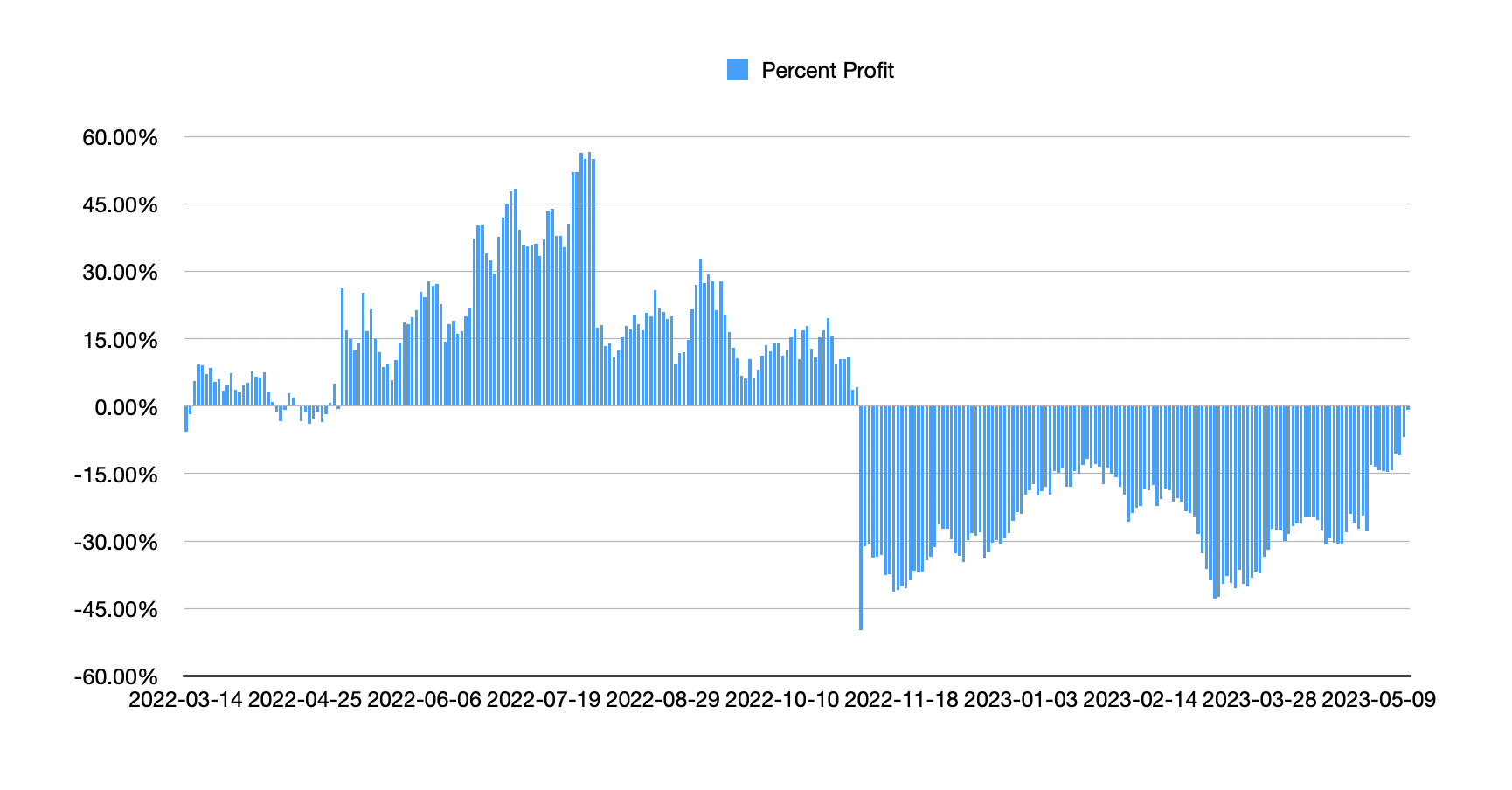

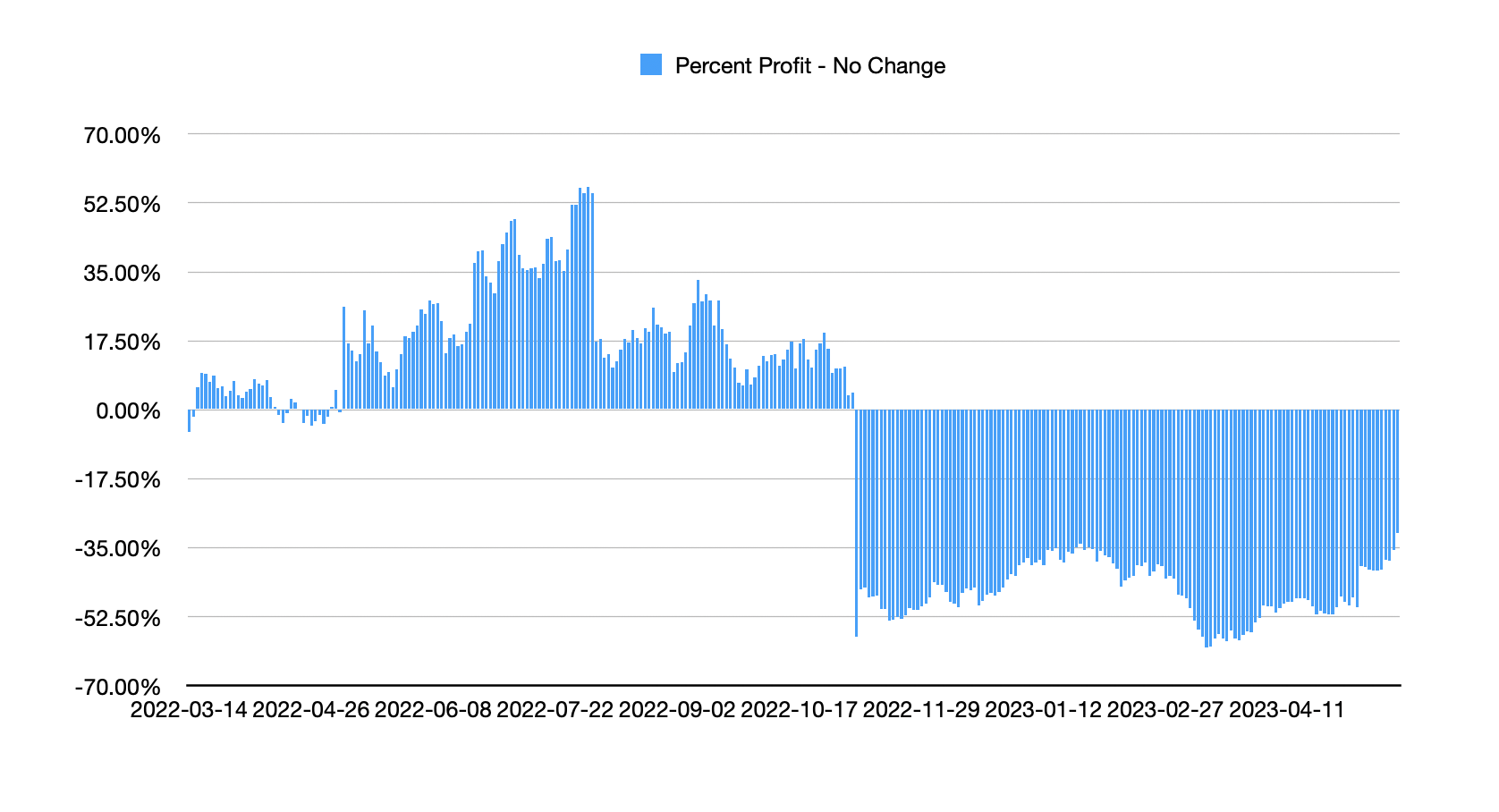

In the next chart above, you can see the same thing, but the chart assumes that, instead of dollar cost averaging lower, I would have stopped buying units of the company as shares plummeted. At this point, my weighted-average cost remains at $18.69. In the chart below, you can see my overall percent profit or loss on any given trading day in units of Funko, while in the chart below that, you can see what that picture would have looked like had I stopped buying units after they declined.

{kind=link}

Author - SEC EDGAR Data

{kind=link}

Author - SEC EDGAR Data

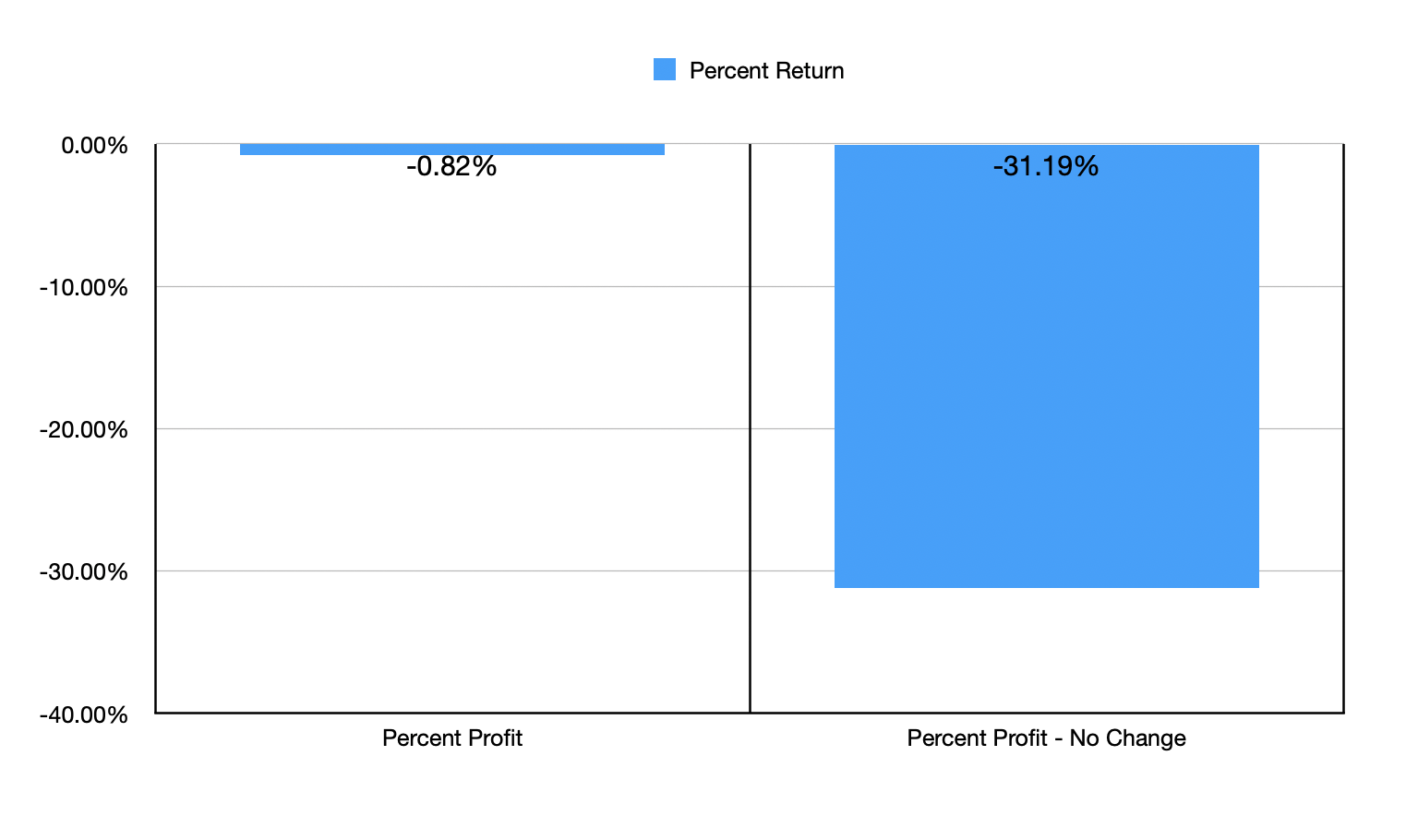

The difference here is striking. As you can see in the chart below, by buying stock as it tumbled, I was able to substantially lower how much I paid for each unit on average. And as the company started to recover, I began to reap the benefits from this strategy. As of May 18, my entire position in Funko was down only 0.82% because of the strategy. But had I only held on to my shares after the plunge, I would still be down 31.19% on my stake even though shares have posted a rather robust recovery from their 52-week low point.

{kind=link}

Author - SEC EDGAR Data

This is not the only time that I have employed this strategy. But it definitely is the most successful. Fortunately, most of my portfolio has done quite well over the past year or so. But another instance where this has played out reasonably well involves my stake in The Walt Disney Company ( DIS ). I began picking up shares of the business in March of 2022 at a price of $131.01. I picked up more shares later that month at $140.30. As the company’s share price declined, I allocated more capital to it. And as of today, I have a weighted average price of $106.05, implying downside of 11.6%. But had I only stuck with my initial stake in the business, I would be down 30.3% on it. This is a fairly small portion of my portfolio, accounting for roughly 8.5% of my holdings. But as I sell off shares of some of my other firms, I'm considering buying more if units remain as low as they are.

This is not to say that dollar cost averaging is some magic bullet that will make your returns substantially better over time. If you own shares of a company that only ever continues to drop because its fundamental condition is deteriorating and upside is no longer warranted, then all you're doing is throwing good money after bad. At the end of the day, we don't know if this is the case or not when we make an investment. And that's because we can't know the future. But in the event that you do have a company fall materially and you believe it is still worth more than its trading for after the drop, this is a great strategy to consider employing.

Takeaway

All things considered, I believe that Funko remains a very attractive prospect at this moment. Obviously, I wish I had sold off my units before they plunged. But my overall assessment of their upside potential was clearly incorrect. Fortunately, I did mitigate my pain rather substantially by buying units on the way down. Hindsight is 20/20, but I do wish I had purchased more units at lower prices. As for what the future holds, I believe that shares are meaningfully undervalued where they are today. But I definitely will not wait for them to go to $28 per share this time around. Given the change in fundamentals, I don't believe they're worth anywhere near that point. At this moment, I would likely begin selling some of my stake at around $18. And by $20 per unit, my goal would be to sell off the last remaining shares that I own. Of course, even this assessment could change. But that's how I see things at this moment.

And when it comes to dollar cost averaging, my last comment is that investors should be careful when putting more money into a company that's dropping. But when you have conviction of that company's value, and you have the financial capability to inject more capital into the firm without overexposing yourself, then you should do so. The only reason why I have not allocated more capital toward Funko recently is because, with the business accounting for over 19% of my current portfolio, I'm already exposed at a level that's perhaps a bit higher than I would normally be comfortable with. I generally like to keep individual holdings that know more than 15%. And right now, I currently have four of my nine holdings at or above that point.

For further details see:

Funko: A Lesson In Dollar Cost Averaging