DIS - Funko: A Small Cap Graham Number Play

Summary

- Funko has dropped 36% in one year, a chart that grabs my attention.

- The company has a licensing stronghold on all things pop-culture.

- With the company trading close to book value and the price to earnings being under 15, this is becoming a Graham Number value play.

36% Down into value territory

Funko ( FNKO ) is a brand that I have a bit of familiarity with. I have friends that are avid Funko pop doll collectors with entire stacks that approach the ceiling. All these stacks are still nicely encapsulated in their perfectly cube-shaped plastic boxes that give onlookers a nice view of the entire figurine's body and oversized head. The structure of the box is almost as important as the doll itself. You see, it is designed to look almost like a display case and the cube shape allows a collector to make a stacked wall out of the toys. Funko was brilliant in the realization that many toy collectors do not open the box at all to preserve its value. The stacking quality combined with the clear visuals almost encourages exponential buying by the patron to increase the enormity of the collection stack.

The other product of theirs that I enjoy is the Loungefly backpacks and accessories. The creativity in the design and the numerous bags you can buy, especially the Disney ( DIS ) branded ones adorn a few spots in my kid's closet. If you haven't laid eyes on the backpacks, I recommend you Google them as they are gorgeous.

The stock is a buy at these levels after the drop while it hovers in the Graham Number territory.

What they do

{kind=link}

Starting off the what they do segment with an in-your-face Halloween Mickey backpack, I couldn't resist. Although Loungefly makes up a smaller portion of its revenue mix, it is the product that I have personally purchased in the past and one that I will continue to support. The quality of the stitching and the varied designs impress me more and more every year. This particular one even glows in the dark like a Jack-O-Lantern. Below you'll see an excerpt from the most recent Funko 10-K that details the revenue growth of the Loungefly products:

Pop! branded products represented 74%, 76% and 79% of our sales in 2021, 2020, and 2019, respectively. Our Loungefly branded products are generally fashion accessories including stylized handbags, backpacks, wallets, clothing, and other accessories. Loungefly branded products represented 14%, 13% and 9% in 2021, 2020 and 2019, respectively.-Funko 2022 10K

{kind=link}

Next, we have the Funko pop dolls, the big enchilada representing 74% of the top line. If you wondered how varied their licensing portfolio was, here's Tony Soprano with a duck. You'll probably never see another toy brand take the risks Funko does which has created a cult following and collector core that doesn't seem to be going anywhere any time soon. Another amazing example of their licensing portfolio is a Zion Williamson figure set against his Panini Mosaic rookie card background. The amount of thoughtfulness and cross-licensing that has to go into an idea like this is surely not an easy thing to pull off, not discounting the creativity and awareness they have of other collectible markets. If the innovation continues, the brand will maintain an edge in my opinion. Some figures are also approaching values of over $10,000 in the collectible market. This creates a similar motivation to continue buying for investment purposes even more than enjoyment.

Recessions are a thing, and we may be in one, but at $25 a pop, this is a very manageable gift and or collector's addiction. We'll also take a look later in the article at just how cheap it is for Funko to create a new design to whet the purchasers' appetite again and again.

The Graham Number

The Graham number is my favorite methodology to use when something is trading near book value, as it incorporates both assets and earnings. These companies normally do not have a high ROA or growth rate in earnings, but can certainly be attractive at our near-the-average market earnings yield combined with the cheap price of the assets. The price target formula is simple, Square Root of 22.5 × (Earnings Per Share) × (Book Value Per Share), with 22.5 representing the threshold at which the P/E times the P/B does not exceed 22.5. The magic 22.5 number is where Benjamin Graham indicated a fair value of a stock.

Our inputs are as follows. Book value as of 2/15/23 of $8.62 and a TTM eps of $1.05. Therefore, SQRT 22.5 x ($1.05) x ($8.62)= $14.27 indicated fair value. In other words, a potential 29% upside versus today's price.

Cost efficiencies

The low cost per production of a new toy is where the company shines. It is the reason why Funko can create such a wide variation of toys and focus more so on its licensing catalog versus its manufacturing costs. Here is another excerpt from the 10K:

Our flexible and low-fixed cost production model enables us to move from product design of a figure to shipping from the factory in as few as 70 days and to the store shelf typically between 110 and 200 days, with a minimal upfront investment for most figures of $5,000 to $7,500 in tooling, molds and internal design costs.

This speed in production to the retail floor or direct-to-consumer platforms in as little as 70 days allows them to stay ahead of the game in pop culture. If something big in television, music, or sports just happened this week, expect to see a Funko pop based on it next month.

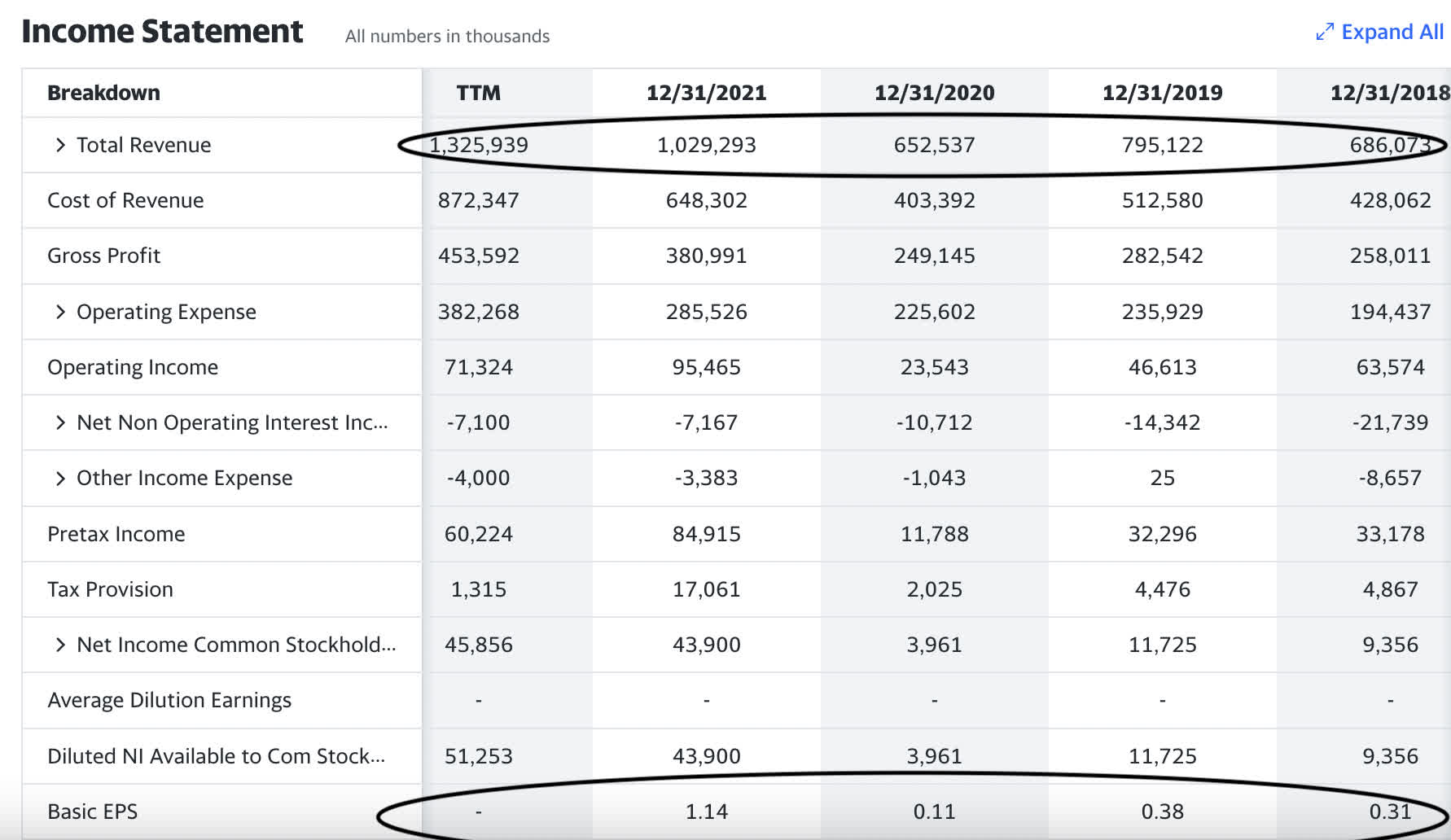

Income statement trends

{kind=link}

We can see both growth on the top and bottom lines with a CAGR in revenue of 14% per annum for the past five years and a 20% CAGR in EPS for the years 2018-2022 incorporating analysts' estimates of the full year 2022 of $0.80 EPS as the terminal number and $0.31 as the 2018 number. There is a bit of drop off in earnings expectations for 2022, but 2023 numbers look higher at an estimated $0.93 a share. Although I don't intend to price this on a PEG ratio basis, if I did use 2019 as my starting point at $0.38 EPS and 2023 estimates of $0.93 a share, we would get a growth rate of 19.6%. Using that as the multiplier (19.6) and $0.93 as the multiplicand would get us a price target of $18.22 a share, an even higher upside.

Debt and the balance sheet

{kind=link}

Nothing stands out to me as inherently risky about this balance sheet snapshot. With a debt-to-equity ratio of about 80% and no dividend, crossing the 50% debt-to-equity threshold doesn't set off any alarm bells. The current ratio exceeds 1. Current assets have risen from $260 to $519 million in the past 5 years while total liabilities have also grown from $373 to $704 million in the same period. While I would like to see liabilities fall while current assets grow, both increasing in lockstep is not worrying either as the top-line revenue continues to march upwards. Funko is consistently investing and growing the business.

Catalysts, Q3 and Q4 pops

Whether or not you believe in the future of Funko's growth, they do point out that nearly 60% of the revenue hits in Q3 and Q4:

For the years ended December 31, 2021, 2020 and 2019 approximately 59%, 64% and 55%, respectively, of our net sales were made in the third and fourth quarters, as our customers build up their inventories in anticipation of the holiday season.

Based on this and the stock trading down this much in Q1, this could also be a swing trade play that pops toward the holiday season. The product is very synergistic with Disney , and their parks are back open across the world in full swing, this should only boost sales of their products. I can see this, especially being true of Loungefly bags and accessories which are almost exclusively Disney-centric. I look forward to Loungefly representing a higher and higher proportion of the company's revenues and becoming the preeminent producer of Disney-licensed backpacks, handbags, and wallets across the world.

Risks

Funko is sensitive to inflation. Even though the top line has increased, the cost of goods as a percentage of revenue has ticked up to 65% versus hovering around 62% the four years prior. China and Vietnam are the main two suppliers of their products. The relationship to produce the type of volume they require in those manufacturing hubs would be hard to pick up and move elsewhere.

Regardless of the cost, if you've never been to China, it's hard to imagine manufacturing infrastructure that can match that of the Chinese. If you lose a supplier in Shenzhen, you can pick up shop and jump to Yiwu, lose one there and there are more in Guangzhou. When it comes to high-volume textile and plastic products, I don't think anyone will ever replace China's capacity. I think China needs to stay in close ties with U.S. producers and we need peace on earth. Important for all reasons, not just the lining of our pockets. Supplier issues remain the biggest risk in my mind.

Summary

The numbers indicate there's value in Funko based on assets, earnings and on growth. They have recently gone into a negative free cash flow position due to increased spending on PPE. The PPE spending as indicated in the Funko 10k is primarily related to tooling and molds used for the expansion of product lines rather than physical real estate. They are showing a big ramp-up with an all-time record $57 million in PPE investment for the trailing twelve months. I own Funko in a small position and would add on dips. Funko is a buy with a price target of $14.27.

For further details see:

Funko: A Small Cap Graham Number Play