TSLA - GDV: Valuation Remains Attractive With Steady Monthly Paying Distribution

2023-11-20 13:40:05 ET

Summary

- The Gabelli Dividend & Income Trust provides a more value-oriented portfolio, and its discount presents a buying opportunity for the long-term investor.

- The GDV closed-end fund has paid a consistent monthly distribution for most of its life, with cuts only occurring during the GFC.

- The fund is modestly leveraged, but with most of that leverage being from preferred with fixed-rate dividends, they aren't having to deal with ballooning interest expenses.

Written by Nick Ackerman, co-produced by Stanford Chemist.

The Gabelli Dividend & Income Trust ( GDV ) has been having a mediocre year. The fund's tilt towards a value-oriented portfolio has meant it hasn't participated in most of the upside that the Magnificent Seven largely drove so far in 2023. That being said, with broader equity markets slumping and combining that with the fund's discount, it presents an interesting time to consider the fund.

The fund will rely on capital gains to pay its distribution, like any other equity closed-end fund ("CEF"), but despite the weak markets, the distribution doesn't seem to be in jeopardy for the foreseeable future. The fund is also leveraged, but unlike most other traditional equity CEFs, they have utilized fixed-rate preferreds for most of their borrowings. Therefore, they have not seen the negative impact of rising interest rates, and that's reflected in the fund's net investment income not taking a hit but rising as its underlying portfolio starts to pay out higher dividends.

The Basics

- 1-Year Z-score: -1.55

- Discount: -17.01%

- Distribution Yield: 6.77%

- Expense Ratio: 1.17%

- Leverage: 13.9%

- Managed Assets: $2.5 billion

- Structure: Perpetual.

GDV is described as "a diversified, closed-end management investment company whose objective is to provide a high level of total return." Their investment policy is:

"under normal market conditions, the Fund invests at least 80% of its assets in dividend-paying or other income-producing securities. In addition, under normal market conditions, at least 50% of the Fund's assets will consist of dividend-paying equity securities."

The fund employs leverage, and even while it is a modest amount, any leverage has the potential to increase the potential downside moves as well as the upside moves. I've been mostly avoiding adding too much more leverage to my portfolio this year; GDV would get a pass. This is because they aren't being impacted nearly as badly as some leveraged funds, thanks to their fixed-rate preferred.

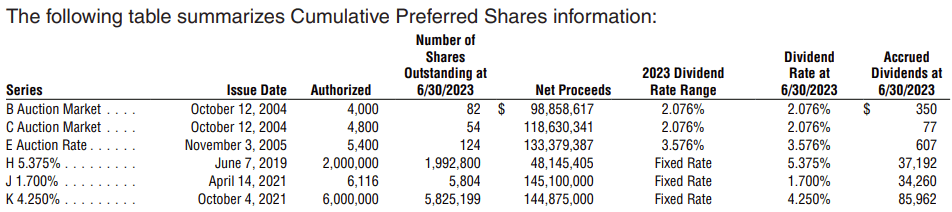

GDV Capital Structure (Gabelli)

The 5.375% Series H ( GDV.PR.H ) and 4.25 Series K ( GDV.PR.K ) are publicly traded and do not have maturity dates. At the time these were issued, they were expensive forms of leverage. Now, Gabelli is the one laughing while leverage costs for most credit facilities in other CEFs ballooned to 6%+.

The Series J does have a mandatory redemption date of March 26, 2028, but at a 1.7% fixed coupon, the fund got a steal of a deal. That's a large portion of their leverage, too. They have several years before it matures, with it being callable any time after March 26, 2024. Given that rate, though, it is unlikely ever to be called early.

The Series B, C and E are auction rates, but they are only a small portion of the fund's leverage. Also, as of their last semi-annual report , these preferred were paying hardly anything at all either at rates of between 2 and 3.5%. Paying lower costs than the U.S. Government is a pretty great place to be.

{kind=link}

Performance - Lagging SPY But Comparable To Most Equities

One example of the portfolio not being aligned with the Magnificent Seven can probably be best highlighted by looking at the performance since our last update . That article was posted earlier this year in April.

GDV Performance Since Last Update (Seeking Alpha)

The fund has underperformed on a total return basis the S&P 500 Index (SP500), widely seen as a measurement of the broader market. During this time, the fund's discount has also widened further, which put even more added pressure on the fund.

If we look at the YTD performance of GDV compared to SPDR® S&P 500 ETF Trust ( SPY ), we can start to see exactly where the divergence started to occur. In fact, if we also include the Invesco S&P 500 Equal Weight ETF ( RSP ), we also see something else quite interesting. GDV and RSP have performed almost identically, and that is to say, they both really haven't done anything in 2023. However, the divergence between SPY to GDV and RSP started to take place right around March/April.

YCharts

For the first couple months of the year, all equities were participating in a solid rebound. That rebound then faltered in March during the banking crisis. From that point on, most equities didn't really participate in a significant rebound, and SPY is only where it is today, largely by the Mag 7.

In my opinion, GDV has been performing about as well as we would expect. Perhaps even better than expected as it's a leveraged fund, and that leverage comes with costs, even if they are fixed. With a portfolio moving sideways, that leverage isn't doing much to 'enhance' any returns. So they are having to contend with that as well.

GDV generally carries a deep discount. However, at this time, the discount is deeper than usual, which generally can mean a buying opportunity.

YCharts

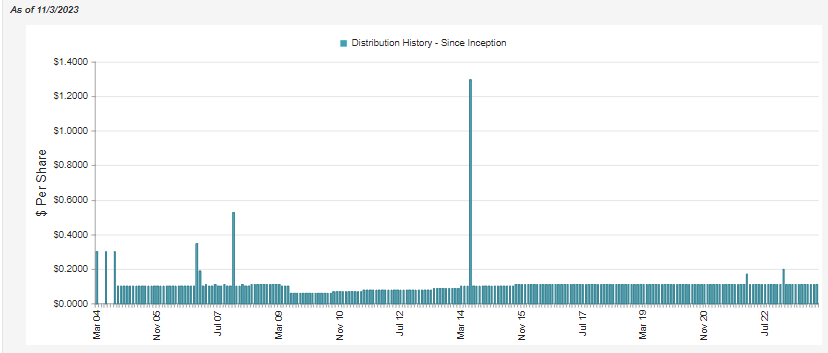

Distribution - Holding Steady

Shortly after the launch of the fund, it switched to a monthly distribution policy. Since then, it has never missed a distribution and has only cut during the Global Financial Crisis.

{kind=link}

Despite the weaker market performance of equities and being an equity fund that will rely on capital gains to fund its payout, I don't foresee a distribution cut at this time. The fund's NAV distribution rate comes in at a modest 5.61%.

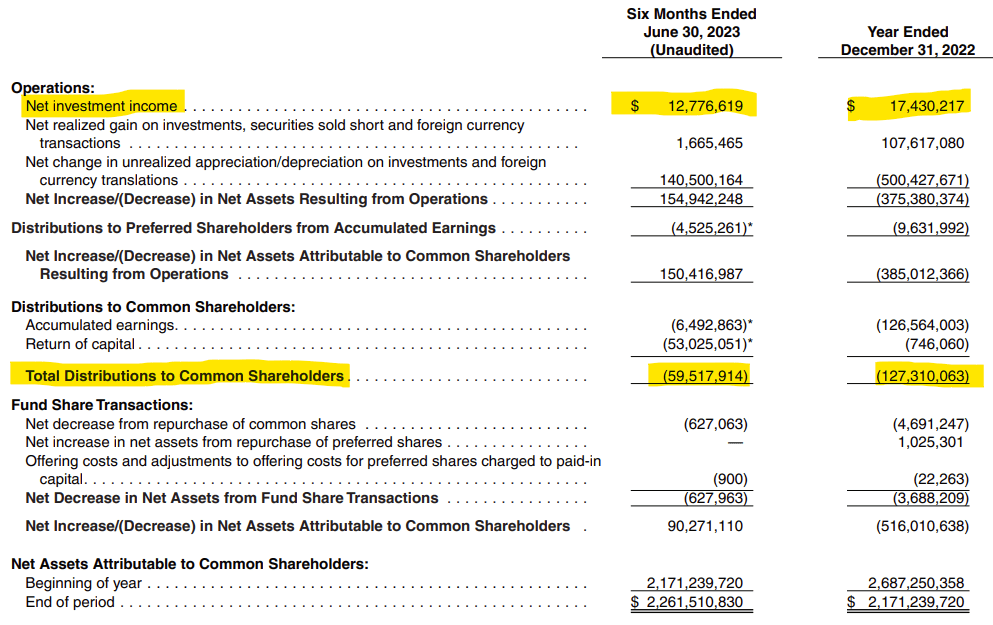

If we look at the semi-annual report for the period ended June 30, 2023, we also see that the fund's net investment income should be increasing year-over-year if the trajectory holds up.

{kind=link}

One thing leveraged funds generally have to deal with is rising borrowings on their leverage. Fortunately, some are hedged in a variety of ways, giving them some time for rates to either go lower once again or adjust to the new environment. In the case of GDV, the majority of their leverage is fixed rate preferred, as we discussed above. That's why we can see NII increase year-over-year for a leveraged fund when we've been seeing mostly the opposite elsewhere.

On the other hand, most CEF investors gripe about the fund's 'low' 6.77% distribution rate, in general. This probably explains some of the widening discounts when interest rates are increasing and risk-free rates become more attractive.

That said, GDV can offer some potential upside as one of only several CEFs with an inception pre-GFC that also has a higher NAV per share now than it did at launch. So not only did it drop in the GFC, but it recovered all of that drop and is even higher now than at inception when considering the latest market slump. Additionally, the fund paid out roughly $22.46 in total distributions during the time.

Given that most of the fund's distribution is covered by capital gains, this is unsurprisingly reflected in the fund's tax classifications for its distribution. Here's what we had to say in our previous update when discussing the latest tax information for 2022.

For tax purposes, we have another benefit of GDV. With most of the distribution for common shareholders regularly long-term capital gains, they are generally more tax-favorable for investors. Additionally, in 2022 , they noted that 100% of the ordinary income was classified as qualified dividends.

This would mean the distributions would have been taxed at 0 to 20% for investors.

{kind=link}

GDV's Portfolio

One of the other more boring parts of GDV, besides its consistently boring monthly distribution, is the portfolio. With a turnover rate that only touched 5% in their last report, there simply aren't a lot of changes. This is consistent with how this fund is often run as well. The high watermark for the turnover rate came in 2020 and 2019, where it peaked at 16% in each of those years.

The fund has generally been overweight to the financial, healthcare and food & beverage areas of the market. This was consistent with what we saw earlier this year in that update for data as of December 31, 2022. This breakdown is from their fact sheet for Q3 ended September 30, 2023.

GDV Sector Allocation (Gabelli)

That being said, while I find one of the more appealing aspects of GDV to be a diversifier in my portfolio away from some tech, they do still carry all of the Mag 7 names; they just aren't as heavily held in the fund. With around 550 holdings, you own a bit of everything. Those mega-cap tech names that make an appearance in the top ten include Alphabet ( GOOG ) and Microsoft ( MSFT ).

GDV Top Ten Holdings (Gabelli)

The MSFT and GOOG forward P/E are on the lower end when compared to some of the other Mag 7 names, which could be why they get a higher allocation. GOOG is coming in at a forward multiple of 22.7x and MSFT at 31.53x. That can be compared to Tesla ( TSLA ) at 68.37x or Nvidia ( NVDA ) at 41.29x.

Then again, they are carrying Eli Lilly and Company ( LLY ) in their portfolio, which trades at 84.92x. That being said, they are carrying a cost basis of around $128.42 per share. So, the only reason that LLY is where it is today is because it has provided them a 342% return since they've owned the position on price appreciation only. They are similarly carrying an envious cost basis for MSFT of around $87.48.

Conclusion

In the end, a bet on GDV is a bet on equities in general, with a portfolio that isn't overly concentrated in the tech arena. More specifically, a fund that isn't overly concentrated in the Mag 7 like the S&P 500 Index has become. This is one of the reasons that I find GDV appealing for the added diversification to a more value-oriented approach. The fund has also delivered a steady and reasonable distribution to investors consistently every month. At this time, I don't view the fund's distribution as being at risk for a cut - despite a weaker market. Given the deeper-than-usual discount, I would continue to view GDV as a buy for the long-term investor.

For further details see:

GDV: Valuation Remains Attractive With Steady Monthly Paying Distribution