COST - General Mills: This Steady Dividend Payer Is An Attractive Buy Right Now

2023-12-11 13:00:00 ET

Summary

- General Mills stock is down double-digits over the past 6 months, presenting a buying opportunity for dividend investors.

- The tough macro environment has affected many businesses, including General Mills, but now is a good time to accumulate shares for long-term dividend investors.

- Although the company beat earnings by a penny, net sales have continued to face downward pressure on net sales.

- With recent acquisitions I expect General Mills to navigate the macro environment and post single-digit growth going forward.

- If the FED decides to hold or raise rates at the upcoming FOMC meeting, the stock price will likely suffer as consumer spending remains tight, affecting net sales going forward.

Introduction

The current macro environment has had and continues to have an effect on a lot of established, well-known businesses. One of those is the consumer staple giant, General Mills ( GIS ). Over the past 6 months, the stock is down double-digits, presenting a buying opportunity for dividend investors.

One of the most exciting things about retiring from the military is now I can stay home and focus on the market. This allows me to search and look for attractive buying opportunities when they present themselves. I don't have to worry about work-ups or going out in the middle of the ocean for sea-trials for months at a time in preparation for deployments anymore.

Sometimes buying opportunities can be short-lived. And with inflation moderating and the economy likely getting our first rate cut sometime next year, now is a great time to be accumulating shares in a high-quality consumer staple like General Mills. In this article, I get into why the stock is a buy for long-term dividend investors.

A Tough 2023

What companies haven't had a rough year? Of course, there are some who've navigated the macro environment better but for a lot of businesses it hasn't been easy. This year I've thought a lot about the saying, tough times don't last, tough people do. In this case, tough businesses. It's easy for a company to post great numbers when the economy is doing well. But what about when things get interesting like now? High interest rates were pretty much non-existent for a long time. But now companies and consumers are feeling the effects of the rise that started early last year.

I mean that was the point right? To get the economy to slow down because of the stimulus it received from the pandemic. Consumers had extra cash to spend so, their bank account balances increased, allowing many businesses to reap the rewards from the rise in consumer spending. We know our economy runs on consumer spending and when it slows, it shows! Well, it's showing. But that's the time to hunker down and keep buying. My portfolio is starting to look a lot better from a rough year now that the panic selling and moving into safer, fixed-rate investments seems to be leveling off. I've mentioned this in previous articles that sentiment was going to shift soon, and now we may be starting to see this, notably in the REIT sector.

Here we can see General Mills being down over 40% over the year, dropping from over $90 a share to a current price of roughly $65. When a high-quality business like GIS drops that much there's usually a reason for it. Yes, the macro environment is putting downward pressure on businesses but for an iconic brand like General Mills, there's usually another reason.

General Mills reported Q1 FY24 earnings back in September and although they beat on earnings by a penny, revenue and volumes were flat. Revenue of $4.9 billion was in-line with analysts' estimates. To be honest, the market has been unfair and unforgiving this year. GIS did disappoint investors with a decrease in earnings and net sales quarter-over-quarter. Looking at the chart below, you can see earnings also declined year-over-year but net sales increased slightly by 3.8% over the same period thanks to price increases on their products.

{kind=link}

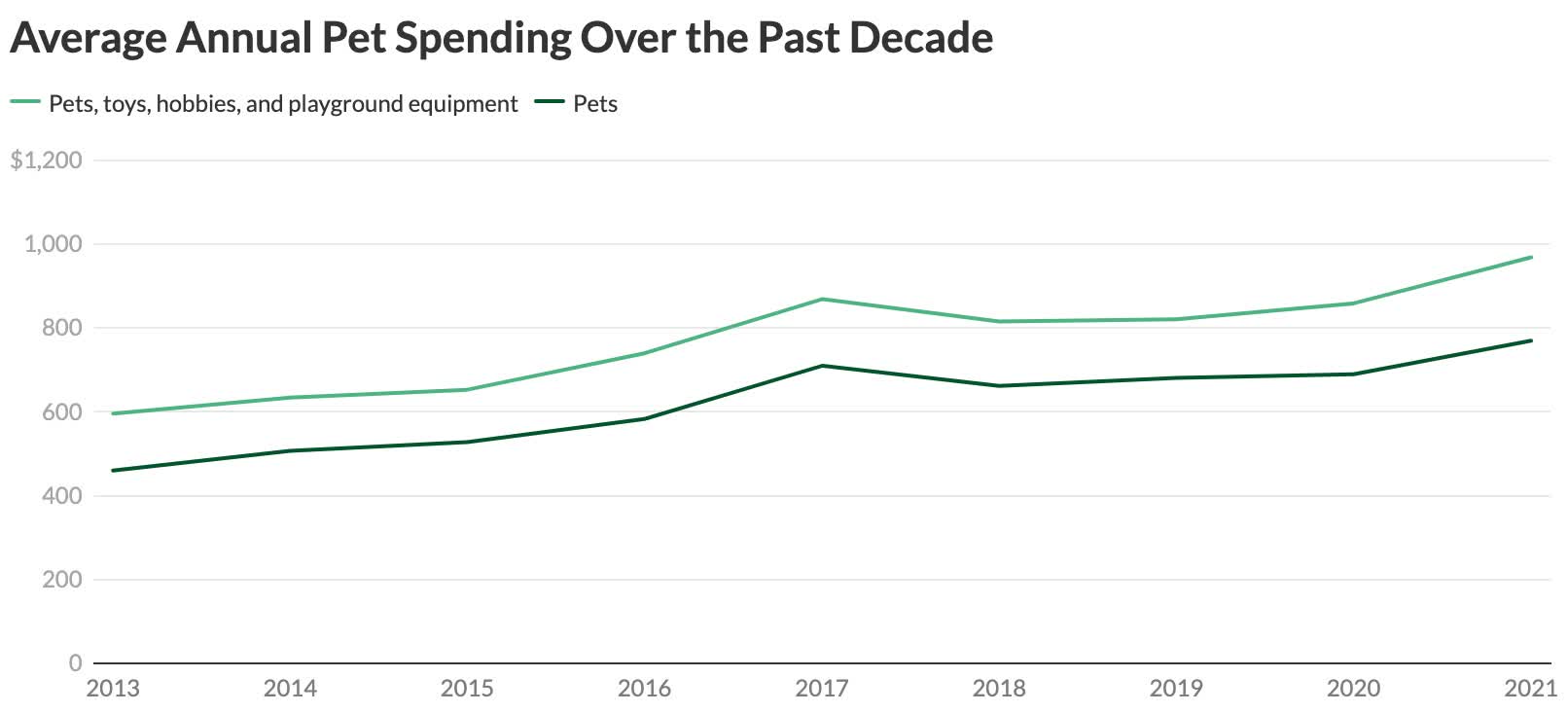

Pet sales were also disappointing and management doesn't expect a huge rebound in the this segment for the rest of the fiscal year. However, they do expect 1% to 1.5% growth in the pet population which will likely benefit GIS in the future. Furthermore, they expect to post 3% to 4% sales growth going forward. As seen in the chart below, pet spending has been increasing steadily since 2013 and I think GIS will see some impressive growth in this segment as consumers get back to spending more on their pets when interest rates and inflation continue to decline in the near future.

{kind=link}

On a positive note, the Foodservice business is growing along with the international businesses as well. The European business was up double-digits in the quarter growing 70% on their BARS business in France and India.

I think 2024 will continue to challenge the business until rates start to subside, which I expect sometime around the 2nd half. Additionally, management stated they are interested in acquiring a major snacking company and are expecting to add 50 basis points of growth through acquisitions and divestitures. One thing I like about companies like General Mills is you can almost count on steady, low single-digit growth. Those are the ones I generally gear my portfolio towards, especially when they're on sale like now. Although September & October are historically the worst months for the market, where many stocks tend to decline due to tax-loss harvesting, there are still plenty of stocks that are considered overvalued. So, finding a quality dividend-paying stock like GIS that offers low, single-digit growth isn't too shabby considering the macro environment.

The Dividend Is Safe

Even with the company facing several challenges this year, the dividend is still safe. Cash flow did decline from FY22 to FY23, causing the FCF payout ratio to become slightly elevated above 60%. Unless you're a REIT or BDC, I typically like to see below this number, preferably in the 40% to 60% range to help me sleep well at night. GIS also managed to increase the dividend by 9% last summer to $0.59.

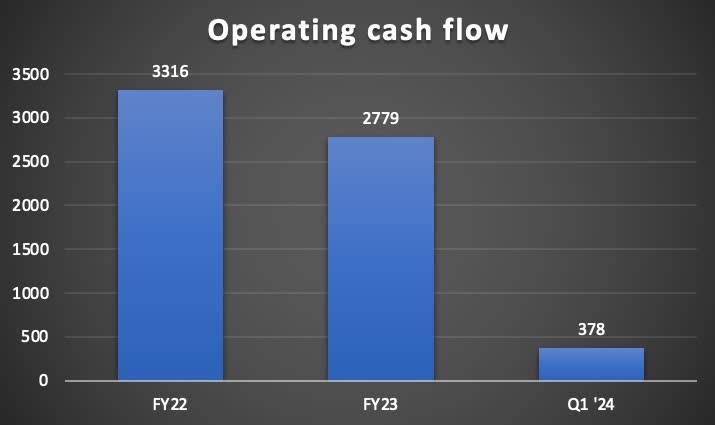

As you can see from the chart below, operating cash flow declined more than 16% year-over-year. CAPEX was $690 million for FY23 bringing the free cash flow amount to roughly $2.1 billion. GIS paid $1.3 billion in dividends for FY23 which brought the payout ratio to roughly 62%, still a safe range by most standards.

But I do understand why this has caused some concern for investors. Me, personally, I would have liked to see a smaller dividend increase while the company focuses on navigating the macro environment. Although they have a long uninterrupted dividend streak, holding the dividend wouldn't have affected the company in my opinion with only 3 years of dividend increases.

{kind=link}

In Q1, operating cash flow was $378 million, declining from $389 million a year ago. Additionally, the company repurchased $496 million worth of shares and CAPEX was $142 million. Going forward management expects a 2% reduction in shares outstanding and CAPEX to be 4% of net sales for the year. So, while the FCF payout ratio is elevated for the quarter, I expect this to decrease over the near term as the company repurchases more shares. This will likely lead to increased earnings and shareholder returns in the process. With an impressive record of 125 years of uninterrupted dividends, I wouldn't put too much stress on whether the company can or will continue to pay shareholders.

Is It A Buy, Hold, Or Sell?

With a forward P/E ratio of 15.5x at the time of writing, below their 5-year average, I think the stock is a buy for income-focused investors. Especially those who like safe and growing dividends from well-established companies that have been around for more than a century. Their P/E also trades below the sector median of more than 17x which makes them even more attractive. Currently, the stock offers some upside to its price target of nearly $71. Investors with a long-term outlook like myself, now may be a good time to start dollar-cost averaging into the stock as it trades closer to their 52-week low of roughly $60. The stock was also one of the seven consumer staples considered attractive because of their valuation.

{kind=link}

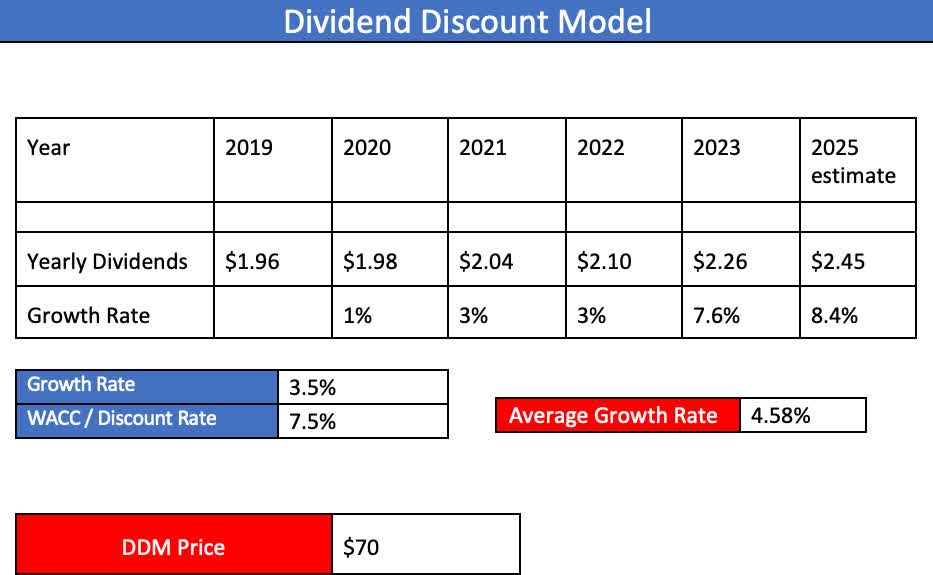

Using the Dividend Discount Model, I have a price target of $70, similar to SA. With General Mills being a low-growth stock I decided to use a WACC of 7.5% and an expected growth rate of 3.5%, the median of management's expected growth rate this year, below the 4.5% average over the last 5 years.

{kind=link}

Risk Factors

Two risks General Mills faces are high interest rates and the recent emergence of weight loss drugs. This continues to raise concerns amongst investors as these drugs gain popularity. Several companies like Costco ( COST ), Walmart ( WMT ), and most recently, Kroger ( KR ) have reported seeing a rise in prescriptions at their retail pharmacies. Although the effects on businesses remain unknown, it does raise questions as they could lead to lower food consumption , affecting the financials for consumer staples like General Mills.

The risk of a recession and tighter consumer spending also continues to pressure businesses like GIS as many look for cheaper alternatives to the more known, increasingly expensive brands. If this continues and net sales continue to decline, it's likely General Mills' stock price will suffer in the near to medium-term. The upcoming FOMC meeting could also affect the stock's price for the short-term if the FED chair pushes back on rate cuts, which many investors believe are near.

Bottom Line

While I expect GIS to continue facing headwinds in the coming months, I foresee the stock delivering on management's expectations of 3% to 4% growth this year. The stock has an impeccable track record of steady dividend payments, and with management expected to continue repurchasing shares, I see earnings increasing as well, rewarding shareholders in the process. Furthermore, they continue to seek out attractive acquisitions which will fuel steady growth along with the recent move into the pet supplement category. Pets remain an important part of people's everyday lives as spending increased 67% as seen in the chart shown previously in the article. With the recent announcement of Fera Pets, I see General Mills capturing growth from increased pet spending for the foreseeable future.

For further details see:

General Mills: This Steady Dividend Payer Is An Attractive Buy Right Now