NZAC - Global Economic Recovery Endures But The Road Is Getting Rocky

2023-05-13 10:00:00 ET

Summary

- The global economy’s gradual recovery from both the pandemic and Russia’s invasion of Ukraine remains on track.

- China’s reopened economy is rebounding strongly.

- Supply chain disruptions are unwinding, while dislocations to energy and food markets caused by the war are receding.

- Global inflation will fall, though more slowly than initially anticipated, from 8.7 percent last year to 7 percent this year and 4.9 percent in 2024.

- A sharp tightening of global financial conditions—a so-called ‘risk-off’ event—could have a dramatic impact on credit conditions and public finances.

Originally posted on April 11, 2023

By Pierre-Olivier Gourinchas , Economic Counsellor and the Director of Research of the IMF

Inflation is slowly falling, but economic growth remains historically low, and financial risks have risen.

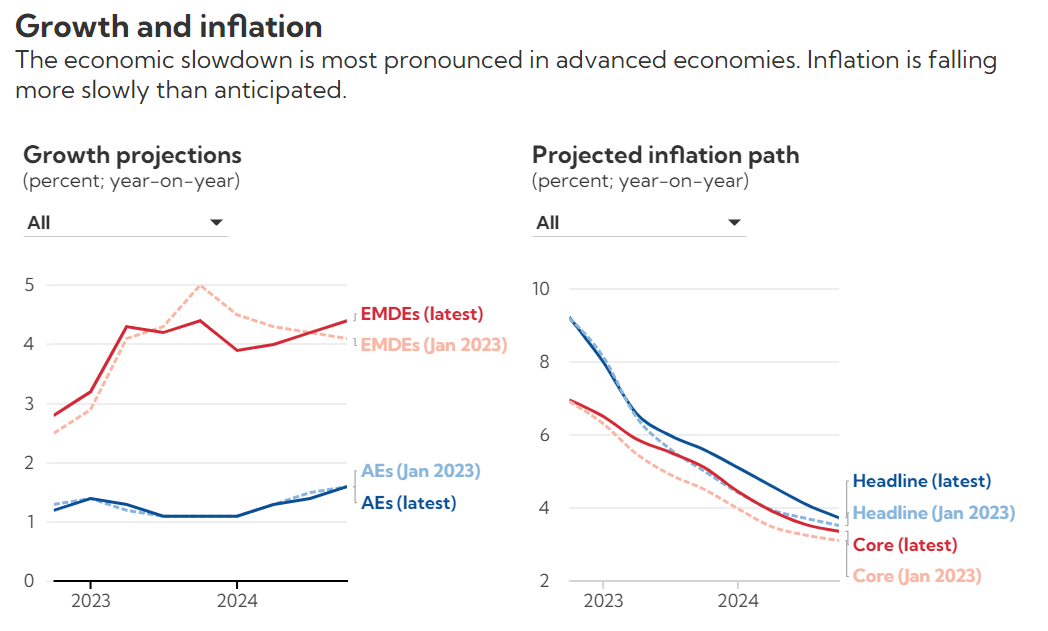

The global economy’s gradual recovery from both the pandemic and Russia’s invasion of Ukraine remains on track. China’s reopened economy is rebounding strongly. Supply chain disruptions are unwinding, while dislocations to energy and food markets caused by the war are receding. Simultaneously, the massive and synchronized tightening of monetary policy by most central banks should start to bear fruit, with inflation moving back towards targets. We forecast in our latest World Economic Outlook that growth will bottom out at 2.8 percent this year before rising modestly to 3 percent next year—0.1 percentage points below our January projections. Global inflation will fall, though more slowly than initially anticipated, from 8.7 percent last year to 7 percent this year and 4.9 percent in 2024.

Sources: IMF, April 2023 World Economic Outlook; and IMF staff calculations. Note: AEs = Advanced economies. EMDEs = Emerging market and developing economies.

{kind=link}

This year’s economic slowdown is concentrated in advanced economies, especially the euro area and the United Kingdom, where growth is expected to fall to 0.8 percent and -0.3 percent this year before rebounding to 1.4 and 1 percent respectively. By contrast, despite a 0.5 percentage point downward revision, many emerging market and developing economies are picking up, with year-end to year-end growth accelerating to 4.5 percent in 2023 from 2.8 percent in 2022.

Risks

Recent banking instability reminds us, however, that the situation remains fragile. Once again, downside risks dominate and the fog around the world's economic outlook has thickened.

First, inflation is much stickier than anticipated, even a few months ago. While global inflation has declined, that reflects mostly the sharp reversal in energy and food prices. But core inflation, which excludes energy and food, has not yet peaked in many countries. We expect year-end to year-end core inflation will slow to 5.1 percent this year, a sizeable upward revision of 0.6 percentage points from our January update, and well above target.

Moreover, activity shows signs of resilience as labor markets remain very strong in most advanced economies. At this point in the tightening cycle, we would expect to see more signs of output and employment softening. Instead, our output and inflation estimates have been revised upwards for the last two quarters, suggesting stronger-than-expected aggregate demand. This may call for monetary policy to tighten further or to stay tighter for longer than currently anticipated.

Should we worry about the risk of an uncontrolled wage-price spiral? At this point, I remain unconvinced. Nominal wage gains continue to lag price increases, implying a decline in real wages. Somewhat paradoxically, this is happening while labor demand is very strong, with firms posting many vacancies, and while labor supply remains weak— many workers have not fully rejoined the labor force after the pandemic. This suggests real wages should increase, and I expect they will. But corporate margins have surged in recent years—this is the flip side of steeply higher prices but only modestly higher wages—and should be able to absorb much of the rising labor costs, on average. Provided inflation expectations remain well-anchored, that process should not spin out of control. It may well, however, take longer than anticipated.

It was never going to be an easy ride

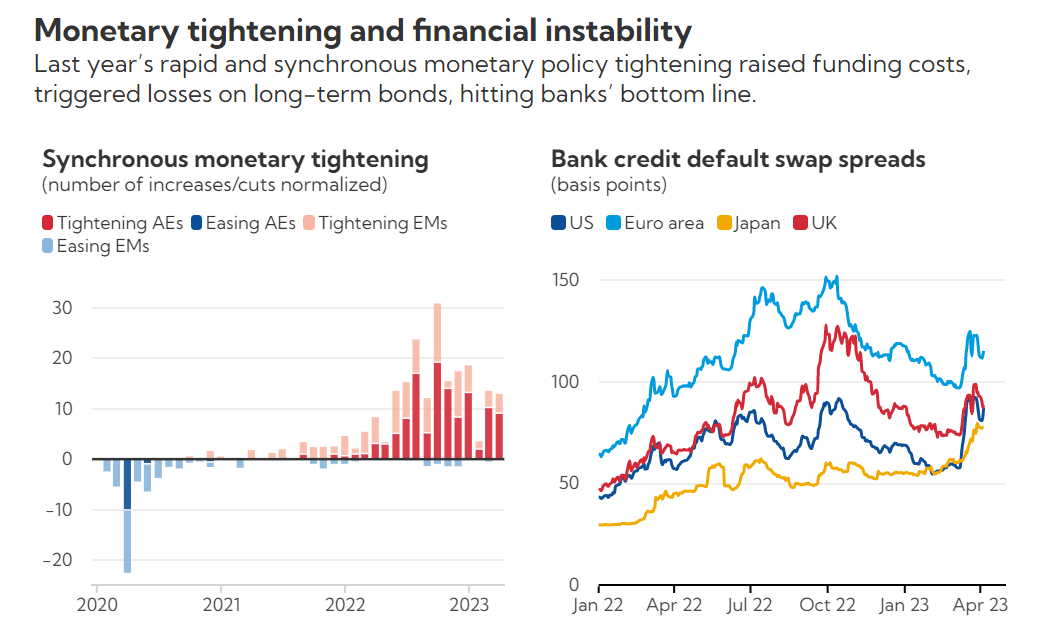

More worrisome are the side effects that the sharp monetary policy tightening of the last year is starting to have on the financial sector, as we have repeatedly warned might happen. Perhaps the surprise is that it took so long.

Following a prolonged period of muted inflation and low-interest rates, the financial sector had become too complacent about maturity and liquidity mismatches. Last year’s rapid tightening of monetary policy triggered sizable losses on long-term fixed-income assets and raised funding costs.

The stability of any financial system hinges on its ability to absorb losses without recourse to taxpayers’ money. The brief instability in the United Kingdom’s gilt market last fall and the recent banking turbulence in the United States underscore that significant vulnerabilities exist both among banks and nonbank financial intermediaries . In both cases, financial and monetary authorities took quick and strong action and, so far, have prevented further instability.

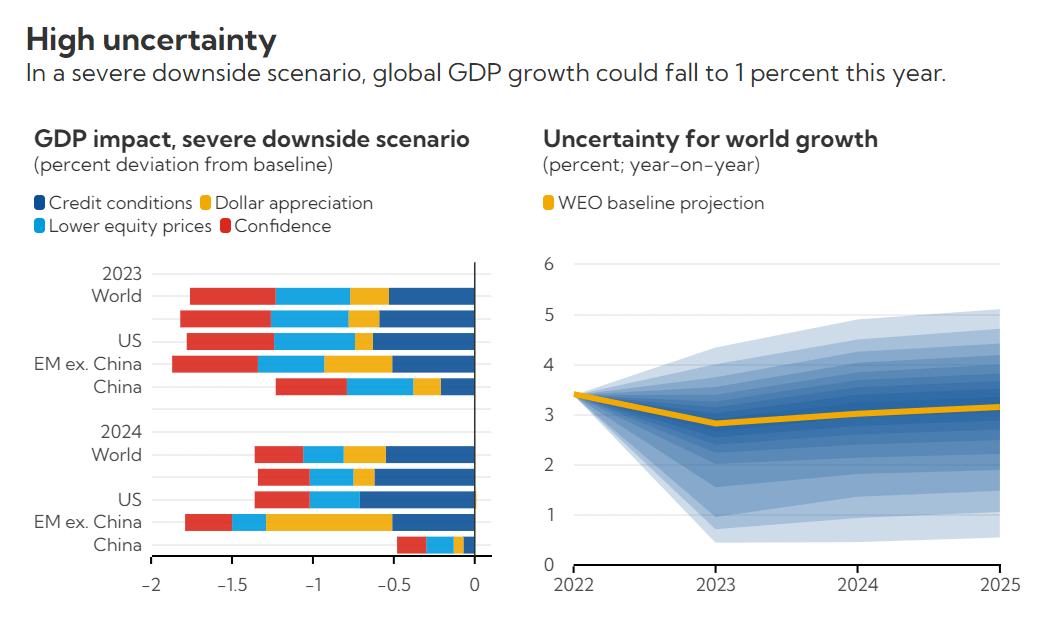

Our World Economic Outlook explores a scenario where banks, faced with rising funding costs and the need to act more prudently, cut down lending further. This leads to an additional 0.3 percent reduction in output this year.

Yet, the financial system may well be tested even more. Nervous investors often look for the next weakest link, as they did with Crédit Suisse, a globally systemic but ailing European bank. Financial institutions with excess leverage, credit risk or interest rate exposure, too much dependence on short-term funding, or located in jurisdictions with limited Fiscal space could become the next target. So could countries with weaker perceived fundamentals.

Sources: Bloomberg Finance L.P.; Haver Analytics; and IMF staff calculations. Note: Left panel ends March 31, 2023. Policy rate changes are normalized by size of average hike/cut. Right panel is the simple average of CDS spreads for 5-year senior bonds of largest banks. US: 10 banks; UK: 6 banks; EA: 19 banks; JPN: 4 banks.

{kind=link}

A sharp tightening of global financial conditions—a so-called ‘risk-off’ event—could have a dramatic impact on credit conditions and public finances, especially in emerging markets and developing economies. It would precipitate large capital outflows, a sudden increase in risk premia, a dollar appreciation in a rush to safety, and major declines in global activity amid lower confidence, household spending and investment.

In such a severe downside scenario, global growth could slow to 1 percent this year, implying near-stagnant income per capita. We estimate the probability of such an outcome at about 15 percent.

Sources: IMF, April 2023 World Economic Outlook; and IMF staff calculations. Note: The right chart shows the distribution of forecast uncertainty, with each shade of blue representing a five percentage point probability interval.

{kind=link}

We are therefore entering a tricky phase during which economic growth remains lackluster by historical standards, financial risks have risen, yet inflation has not yet decisively turned the corner.

Policies

More than ever, policymakers need a steady hand and clear communication.

With financial instability contained, monetary policy should remain focused on bringing inflation down, but stand ready to quickly adjust to financial developments. A silver lining is that the banking turmoil will help slow aggregate activity as banks curtail lending. In and of itself, this should partially mitigate the need for further monetary tightening to achieve the same policy stance. But any expectation that central banks will prematurely surrender the inflation fight would have the opposite effect: lowering yields, supporting activity beyond what is warranted, and ultimately complicating the task of monetary authorities.

Fiscal policy can also play an active role. By cooling off economic activity, tighter fiscal policy would support monetary policy, allowing real interest rates to return faster to a low natural level . Appropriately designed fiscal consolidation will also help rebuild much-needed buffers and help strengthen financial stability. While fiscal policy is turning less expansionary in many countries this year, more could be done to regain fiscal space.

Regulators and supervisors should also act now to ensure remaining financial fragilities don’t morph into a full-blown crisis by strengthening oversight and actively managing market strains. For emerging markets and developing economies, this also means ensuring proper access to the Global Financial Safety Net, including the IMF’s precautionary arrangements, access to the US Federal Reserve Foreign and International Monetary Authority's repo facility , or to central bank swap lines, where relevant. Exchange rates should be allowed to adjust as much as possible unless doing so raises financial stability risks or threatens price stability, in line with our Integrated Policy Framework .

Sources: IMF, April 2023 World Economic Outlook; and IMF staff calculations.

{kind=link}

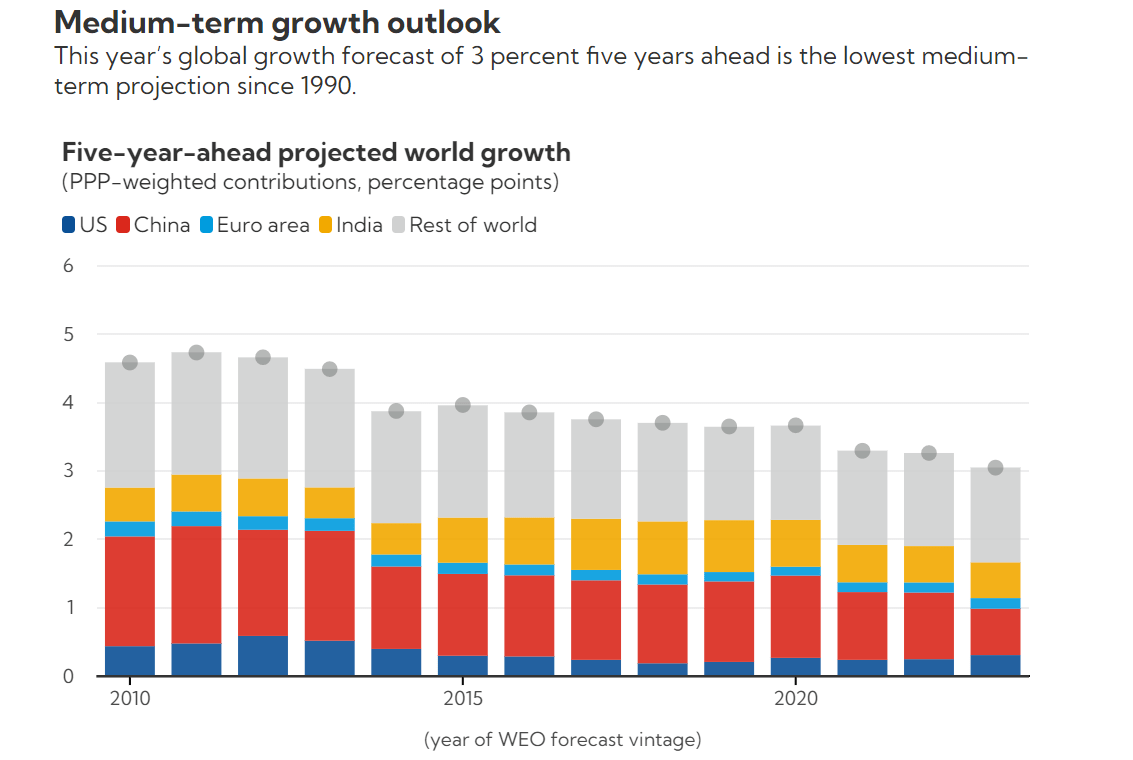

Our latest projections also indicate an overall slowdown in medium-term growth forecasts. Five-year-ahead growth projections declined steadily from 4.6 percent in 2011 to 3 percent in 2023. Some of this decline reflects the growth slowdown of previously rapidly growing economies such as China or Korea. This is predictable: growth slows down as countries converge. But some of the more recent slowdown may also reflect more ominous forces: the scarring impact of the pandemic, a slower pace of structural reforms, as well as the rising and increasingly real threat of geoeconomic fragmentation leading to more trade tensions, less direct investment, a nd a slower pace of innovation and technology adoption across fragmented ‘blocks.’ A fragmented world is unlikely to achieve progress for all, or to successfully tackle global challenges such as climate change or pandemic preparedness. We must avoid that path at all costs.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Global Economic Recovery Endures But The Road Is Getting Rocky