VSAT - Gogo: Still A Hold But Getting Interesting

2023-09-03 05:11:05 ET

Summary

- Gogo faces increasing competition in the in-flight connectivity market from providers like Viasat and SpaceX.

- Gogo's current Air-to-Ground network has limitations in speed and coverage compared to satellite networks.

- Gogo is investing in new technologies like 5G and LEO satellites to improve its offerings and expand internationally.

- Gogo is still a hold as it doesn't offer a wide margin of safety, but it's worth keeping an eye on it.

Editor's note: Seeking Alpha is proud to welcome Andes Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Introduction

Gogo ( GOGO ) is one of the leading providers of in-flight connectivity ((IFC)), whose shares plummeted in the last month (-33%) after lowering its guidance and due to the constant delays in implementing 5G. After the stock crash, Gogo is fairly valued given the risk of new entrants (SpaceX), tough competition from Viasat (VSAT), and more delays. However, adopting new satellite technology and 5G can accelerate revenue growth in the following years and improve Gogo's competitive position.

This thesis will examine the competitive landscape of the IFC market, with a focus on Gogo. The thesis will also discuss Gogo's financials, new technologies, and international expansion plans. The thesis will conclude with an assessment of Gogo's prospects.

Current And Future Competitive Landscape

Gogo specializes in offering in-flight connectivity through its Air-to-Ground ((ATG)) network across the United States and satellite narrowband through providers. Gogo currently relies on its cell sites network (almost all are leased) to provide 3G and 4G services, but the ATG internet has two critical disadvantages relative to satellite networks. First, according to Wikipedia, ATG may offer 3 Mbps per plane, that is, 3 Mbps for all passengers who paid for internet service; second, its use is limited by land, so this service cannot be offered on ocean flights. Meanwhile, satellite internet can reach 70 Mbps and have broader coverage.

However, it has two key advantages: it's cheaper for customers and airlines, as it neither requires satellites in orbit nor heavy antennas on the aircraft. But I don't think someone can be happy paying for an internet connection so slow, even if it's almost free (which is not the case). For that reason, I believe satellite internet is better suited for in-flight connection now and in the coming years. According to CNBC , Delta Air Lines (DAL) didn't doubt moving toward satellite Wi-Fi with an alliance with Viasat to adapt its Delta 737 Max Ten airplanes to the satellite internet connection. Delta wants to offer free Wi-Fi on all its future flights through Viasat, and it doesn't think it can be possible with Gogo. Moreover, according to Mike Freeman, Southwest (LUV) recently signed a contract with Viasat as an IFC provider for its new 350 airplanes, and now Viasat is included in JetBlue Airways (JBLU), American Airlines (AAL), Delta Airlines, Southwest Airlines, and Virgin Airlines. I believe this has and will have detrimental effects on Gogo's growth as there are switching costs because aircraft need to carry an antenna, which is heavy and cannot be installed while the airplane is flying, so airlines won't be willing to add another heavy antenna (which leads to more fuel consumption) and lie an aircraft on the ground if Gogo does not offer a significant improvement in internet quality.

To fight against rising competition, Gogo had planned to launch 5G by the middle of 2023, but the launch has been delayed by a year due to chip issues, by RCRWirelessNews . The introduction of 5G will potentiate the inflight internet speed, which Gogo estimates will be 25 Mbps for its ATG network. This continues to be lower than the current speed obtained by satellites. Nevertheless, we must remember that 70 Mbps is distributed among every aircraft in the covered region, so the actual bandwidth is lower than 70 Mbps. Moreover, Geostationary Earth Orbit ((GEO)) satellites, which are the ones that Viasat owns, suffer from high latency because they are too high from the ground. In this scenario, rather than having a few large GEO satellites, it is better to have many Low Earth Orbit ((LEO)) satellites, which have lower latency and do not share speed internet among many aircraft. In this sense, Gogo is expanding to global markets through an alliance with OneWeb to provide IFC services through its LEO satellite network of 634 satellites, which is far more than the 4 GEO satellites owned by Viasat (plus the 14 GEO satellites acquired from Inmarsat). Gogo expects to offer LEO satellites and 5G services by late and mid-2024, respectively.

In addition, Gogo and Hughes developed a small electronically steered array ((ESA)) antenna so it can be carried by smaller airplanes. As it is lighter than current antennas, Gogo will offer higher value for airlines than other IFC providers. I think this is going to be the growth fuel in the future and the reason why Gogo may overtake Viasat. Nevertheless, a new entrant is threatening the competitive environment in the industry, SpaceX, which has already signed a contract with Hawaii Airlines to provide in-flight internet in 2024 and might provide an internet speed of 500 Mbps per plane. Like Gogo, SpaceX uses lighter antennas than the current in use in the industry. Even Viasat is open to allying with LEO companies, by SpaceNews .

However, I don't think more new entrants will appear as the industry enjoys high barriers to entry due to changing costs, large amounts of required capital, stiff competition for leasing satellite and tower capacity, and dependence on developing economies of scale to be profitable.

Financials

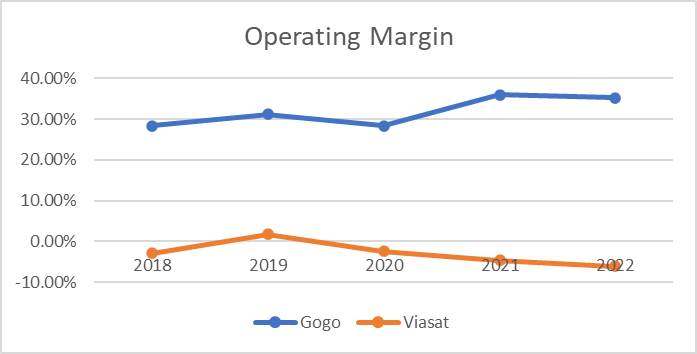

Since the divestiture of the CA business segment, Gogo has recorded positive operating profits and, in the two previous years, a positive net income. Unlike Viasat, Gogo's business model has shown to be profitable after a significant reduction in interest payments since 2021. This expense decreased as debt was paid off or converted into shares.

Author's Elaboration with data from QuickFS

{kind=link}

I expect in the next year better profitability from Viasat as Inmarsat was a company with solid performance before being acquired. However, Gogo has better profitability as of August 2023.

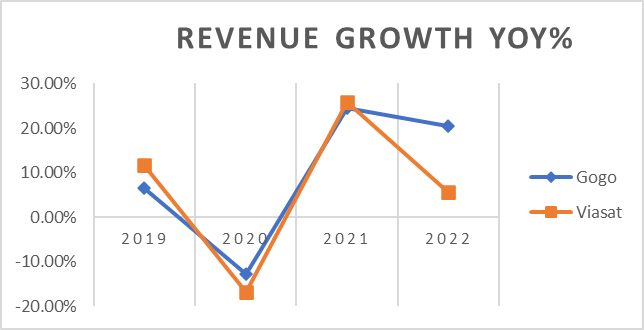

Moreover, in the last four years, Gogo's revenue rose with a CAGR of 8.63% and Viasat's revenue with a CAGR of 5.44% (not including the revenue increase due to Inmarsat acquisition). The reason is that in the last year, Gogo kept a double-digit growth while Viasat only grew at a high single digit.

Author's Elaboration with data from QuickFS

{kind=link}

The solid growth has resulted from a steady increase in the number of airplanes since 2018. However, planes with satellite equipment have been slowly reducing due to the stiff competition from Viasat, in my opinion. Nonetheless, I believe the tendency will revert after 2025 or 2026 when Gogo can implement its satellite services with LEO satellites.

Author's Elaboration with data from 10K Reports

Author's Elaboration with data from 10K Reports

In addition, it's noteworthy that ATG units sold have been increasing since 2020, which may result in customers expecting to implement 5G technology. Moreover, more units sold today means more revenue in the future.

Industry Opportunity

The IFC industry is expected to increase in the next decade due to more demanding customers in the airline industry, as it represents a way for airlines to compete away from pricing. Euroconsultant report estimates that the number of aircraft with IFC will double in the next decade. Moreover, Business Future expects an industry growth of 15.9% annually. Meanwhile, Business Research Insights set the annual increase at 16.9% annually. Grand View Research contemplates a gain of 8.4% annually.

I think Gogo will be capable of capitalizing on this growth completely soon after it makes 5G and LEO satellites commercially viable, as they will offer more high-quality products than GEO satellite competitors. Moreover, the LEO connection can be installed easily in airplanes with Gogo equipment, which, as we saw above, has risen steadily in the last five years. This is another competitive advantage, as airlines prefer to install only the new Gogo ESA rather than install completely other competitors' equipment. Additionally, the expansion to the international market will boost sales growth in the following years, but it will face stiff competition with Viasat and Panasonic (PCRFY).

However, I think as long as Gogo does not offer 5G and LEO satellites, it is playing at a disadvantage compared to Viasat.

Risk

Tough competition

As we saw above, the IFC industry has experienced technology disruptions in recent years, passing from ATG as the sole technology to LEO satellites. It's unknown what the next technology will be or when it will arrive. But I expect LEO satellites will be around at least for the rest of the decade because of their advantages relative to GEO and ATG networks. However, shareholders can suffer more delays, which have become normal when implementing 5G; if delays continue, I expect Viasat to keep gaining market share from Gogo and more suffering for shareholders.

Large Debt

According to its last 10-Q Report, Gogo has a long-term debt of 590 million and cash reserves (including short-term investment) of 97.2 million, meaning the net debt is approximately 492.8 million. Given last year's free cash flow of 59.491 million (CFO-CAPEX), we have a debt-to-FCF ratio of roughly 9.92 (and 8.28 if we use net debt), which is worrisome when the debt is due in 2028. That means the company must refinance its debt, likely at higher interest rates. However, CAPEX may decrease after the total installation of 5G.

Suppliers' Bargain Power

Gogo Galileo bet is the best shot for Gogo to potentiate its sales, but there are two crucial drawbacks for me. First, OneWeb, as the sole supplier of the LEO constellation, has a unique bargaining power toward Gogo because, as stated in its last 10-K report, Gogo estimates it would take up to two years to replace OneWeb as its satellite narrowband provider. Likewise, Hughes is the sole provider of ESA antennas needed for implementing the narrowband into the airplanes, so any disruption in its production can lead to delays similar to those experienced in implementing 5G. Second, the list of LEO satellites is limited due to the cost of maintaining such a network, as can be seen in the graph below:

Congressional Budget Office

Dilution

Due to the debt and possible delays and costs in implementing 5G and LEO satellites, I expect dilution to keep the tendency of the last ten years. Albeit, the company, in the previous two years, has demonstrated its capacity to generate positive free cash flow, which can revert the tendency soon.

Valuation

Seeing the last quarter results, the firm is recovering from disastrous Q1 results with the number of AVANCE (its latest equipment) and equipment sales declining. In the Q2 announcement, revenue grew at 6%, driven by a strong demand for services (8% growth), but with a slight decrease (2%) in equipment revenue. In addition, AVANCE AOL is rising fast with a YoY% of 24%, but the ARPU (Average Monthly Revenue per ATG aircraft online) has remained flat compared to 2022.

The management announced they expect revenue growth between 15%-17% until 2027, but I wonder if they can achieve that growth with the constant delays in 5G and without Gogo Galileo. Moreover, they lowered the guidance from 17% to 15-17% revenue growth until 2027.

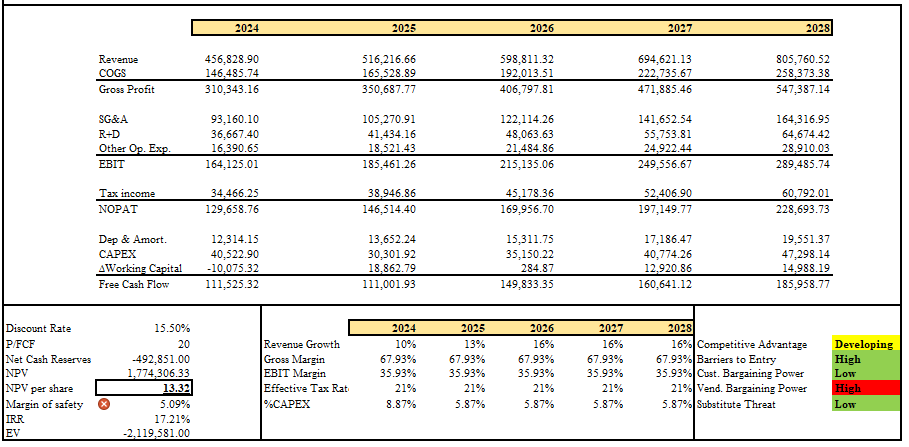

In my DCF model, I estimate revenue growth of 10% during 2024 (beginning with a revenue of 415.30 million in 2023), 13% for 2025, while the firm begins exploring international markets and 5G starts to pay off, and 16% until 2028.

The value of perpetuity will be gauged using a P/FCF of 20 as the company in 2028 will be growing at double digits. Finally, due to the abovementioned risks, I used a 15.50% discount rate.

{kind=link}

Conclusion

Gogo is exploring new technologies to potentiate its growth in an industry with strong tailwinds. Still, constant delays, significant debt, and the entrance of SpaceX into the industry are adding uncertainty to future cash flows. I think Gogo shares are reasonably valuable as my DCF returned a fair value of $13.32 per share. I believe this is a conservative valuation as the perpetuity value could be higher given that the company would be growing around 16% annually. Moreover, the discount rate could be slightly high, but I prefer to be prudent rather than optimistic.

Notably, the revenue growth is based on expected industry growth, Gogo guidance, and delays. Thus, I think selected revenue growth is plausible and not too optimistic.

Finally, I will wait for lower prices to buy as the current price doesn't offer a wide margin of safety (>30%) to protect investors against delays, competitive threats from SpaceX and Viasat, and supplier bargaining power, which together may shrink the bottom line. I would consider buying if the price falls to around $9, as the margin of safety would be approximately 35%.

For further details see:

Gogo: Still A Hold, But Getting Interesting