REIT - Good News Is Bad News

2023-10-08 09:00:00 ET

Summary

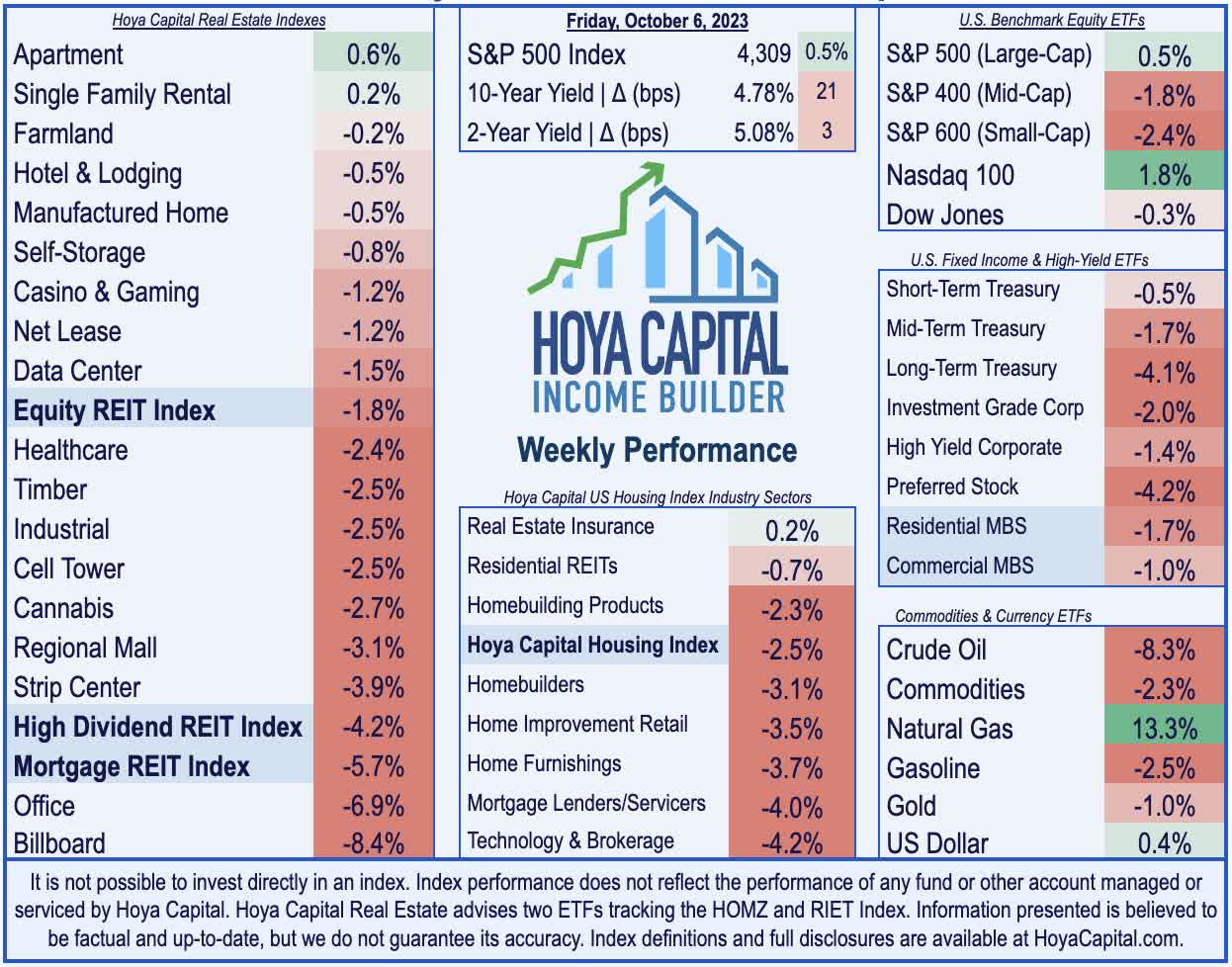

- U.S. equity markets remained volatile this week as benchmark interest rates surged through multi-decade highs after employment data showed resilient labor market trends, bolstering the Fed's case to remain hawkish.

- Narrowly avoiding a fifth-straight week of declines, a late-week rebound lifted the S&P 500 to gains of 0.5%. Mid-Caps and Small-Caps, however, posted 2% declines this week.

- Yield-sensitive segments of the equity market remained under particularly sharp pressure this week as benchmark interest rates surged to the highest levels since before the Great Financial Crisis.

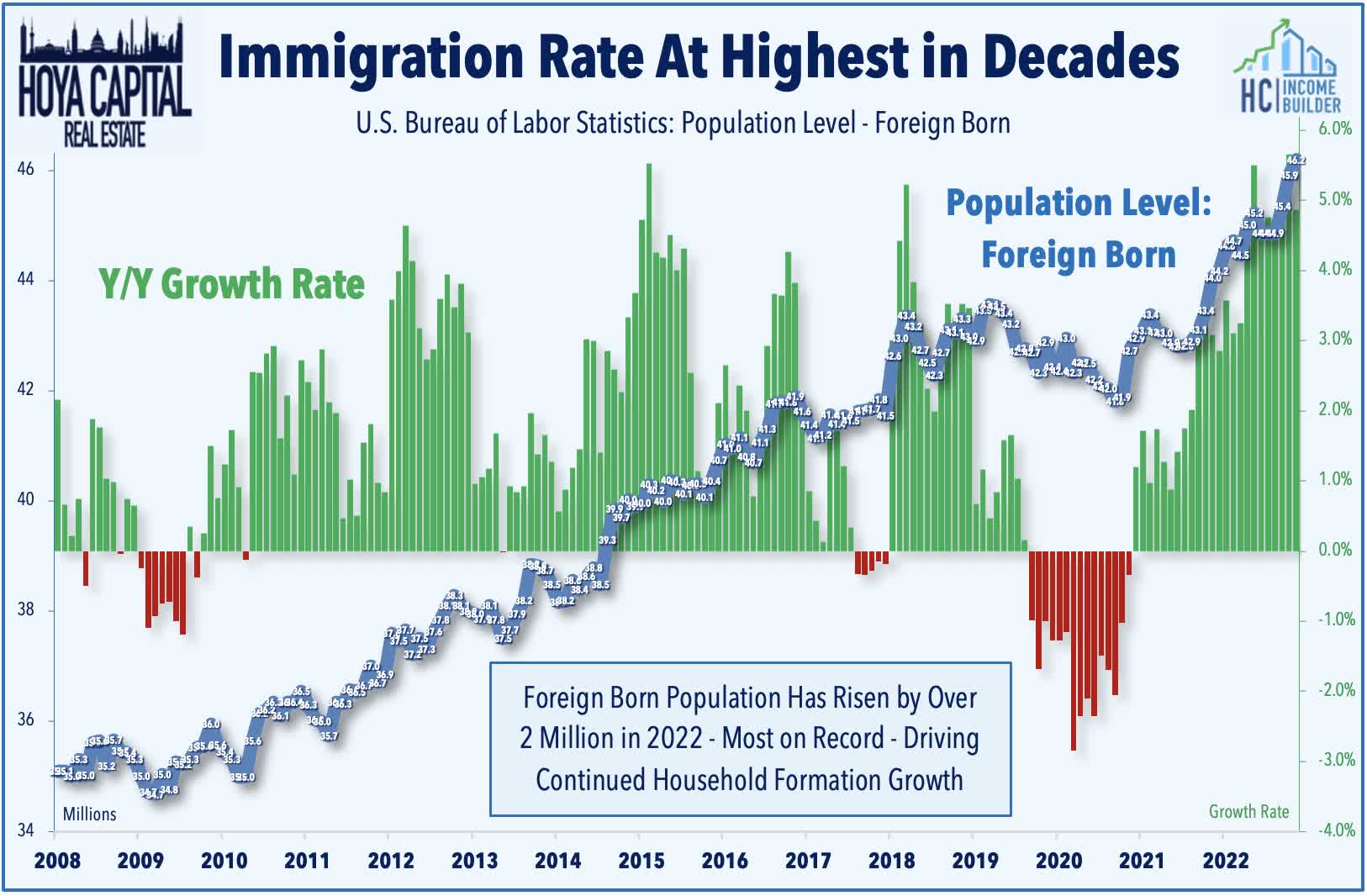

- Inbound immigration and favorable millennial-led demographics appear to be a driving force behind some of the recent hiring strength, as the Household Survey showed that the Population Level in the United States posted its largest year-over-year increase in over a decade in September.

- Average hourly earnings - a key inflation indicator - provided encouraging evidence of normalizing labor market conditions following pandemic-era shortages. AHE rose 0.2% in September and 4.2% from last year, the lowest since June 2021.

Real Estate Weekly Outlook

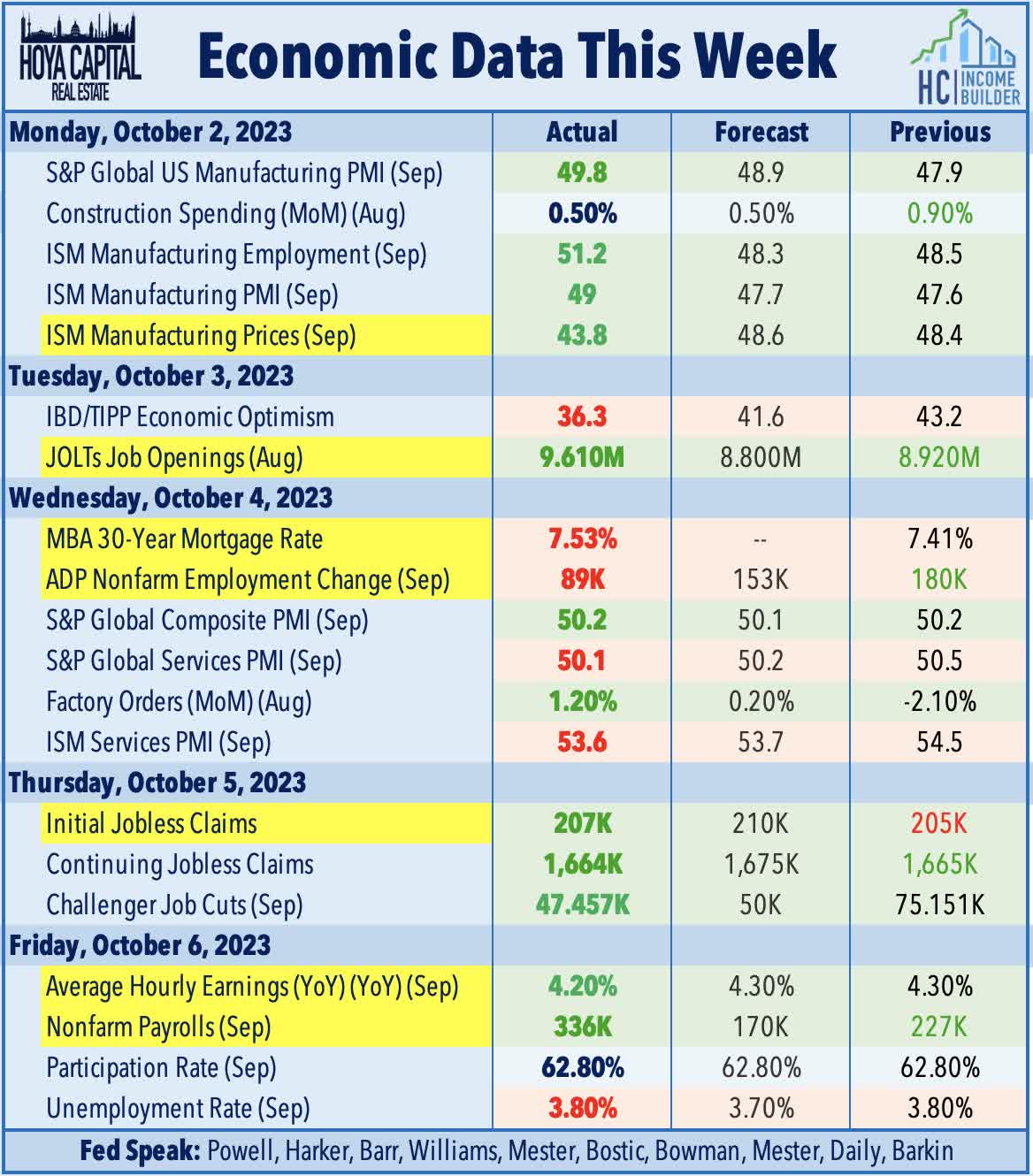

U.S. equity markets remained volatile this week as benchmark interest rates surged through multi-decade highs after employment data showed resilient labor market trends - with some caveats - bolstering the Fed's case to continue their historically aggressive monetary tightening path. 'Good news' was 'bad news' across the busy slate of employment data this week, underscored by the blowout headline job growth print of 336k in the critical nonfarm payrolls report, which lifted the market-implied probabilities of another rate hike to nearly 50% - up from roughly 30% last week.

{kind=link}

Narrowly avoiding a fifth-straight week of declines, a late-week rebound and strength from mega-cap technology stocks lifted the S&P 500 to gains of 0.5% on the week. The other major benchmarks remained under pressure this week, however, with the Mid-Cap 400 and Small-Cap 600 each posting declines of 2% on the week. Yield-sensitive segments of the equity market remained under particularly sharp pressure this week as benchmark interest rates surged to the highest levels since before the Great Financial Crisis. The Equity REIT Index declined another 1.8% on the week, with 16-of-18 property sectors in negative territory, while the Mortgage REIT Index dipped by nearly 6%. Homebuilders declined another 3% this week as mortgage rates approached 8% for 30-year conventional loans - the highest in over 23 years - which sent mortgage application demand to the lowest since 1996.

{kind=link}

Relief from a last-minute deal to avoid a government shutdown over the weekend was short-lived as the Treasury rout intensified, fueled in part by another wave of hawkish Fed rhetoric, including a call from Fed Governor Bowman that "multiple" additional interest-rate hikes may be required to get inflation down to the central bank’s goal. The 10-Year Treasury Yield surged another 21 basis points this week to close at 4.78%, but the more policy-sensitive 2-Year Treasury Yield rose only three basis points to close at 5.08%. Crude Oil - a key contributor to the rate resurgence since June - posted its worst week since March after OPEC+ retained status-quo production plans, while EIA data showed a sharp decline in gasoline demand and significant inventory build. Natural Gas futures, however, surged by over 13% this week to nine-month highs. The U.S. Dollar strengthened for a 12th straight week. Eight of the eleven GICS equity sectors finished lower on the week, with Energy ( XLE ) and Utilities ( XLU ) stocks dragging on the downside.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

The long-awaited cooldown in labor markets - which most Fed officials have pinned their "pivot" upon - remains stubbornly elusive, according to the latest BLS nonfarm payrolls report this week. The U.S. economy added 336k jobs in September - well above consensus estimates of 170k - while net revisions added 110k jobs to the prior two months. Surprisingly, job growth in September was driven by several of the most economically sensitive categories, including leisure and hospitality - which added 96k jobs in September - and food services and drinking places - which added 61k for the month. The strong report followed a relatively solid slate of reports earlier in the week, including "beats" on the JOLTs report and on both Initial and Continuing Jobless Claims. However, ADP private payrolls report earlier in the week showed job growth of 89k - below expectations of 170k - while the Household Survey showed disappointing job growth of 86k.

{kind=link}

Inbound immigration and favorable millennial-led demographics appear to be a driving force behind some of the recent hiring strength, as the Household Survey within the BLS' report showed that the Population Level in the United States posted its largest year-over-year increase in over a decade in September. The increase in the U.S. civilian noninstitutional population eclipsed 3 million for the first time since December 2012. The Census Bureau reported that net international migration added more than a million people to the U.S. population last year - the largest single-year increase since 2010 - while the CDC reported that U.S. birth rate increased for the first time since 2014. The labor force participation rate remained at 62.8% - matching the highest level since the start of the pandemic - but still stubbornly below the 63.0% pre-pandemic average from 2016-2019.

{kind=link}

Average hourly earnings ("AHE") - a key inflation indicator - provided encouraging evidence of normalizing labor market conditions following pandemic-era shortages. AHE rose 0.2% in September, which was lower than expected, and continued the trend of moderation observed in the annual increase for both the 'All Employees' and 'Nonsupervisory Employees' indexes. Since the start of 2023, AHE for all employees has averaged 3.7% on an annualized basis - which is only marginally above the 3.3% increase in 2019 in a year that CPI inflation averaged just 1.8% - suggesting that concerns over wage-driven inflation - and the feared "wage-price spiral" - are likely unwarranted at this point. Earlier in the week, ADP reported that pay increases for job switchers fell to 9% in September, the slowest rate of growth since June 2021 and well below the peak of roughly 16% in June 2022. Pay increases for job stayers increased by 5.9% in September, which was the lowest since September 2021.

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

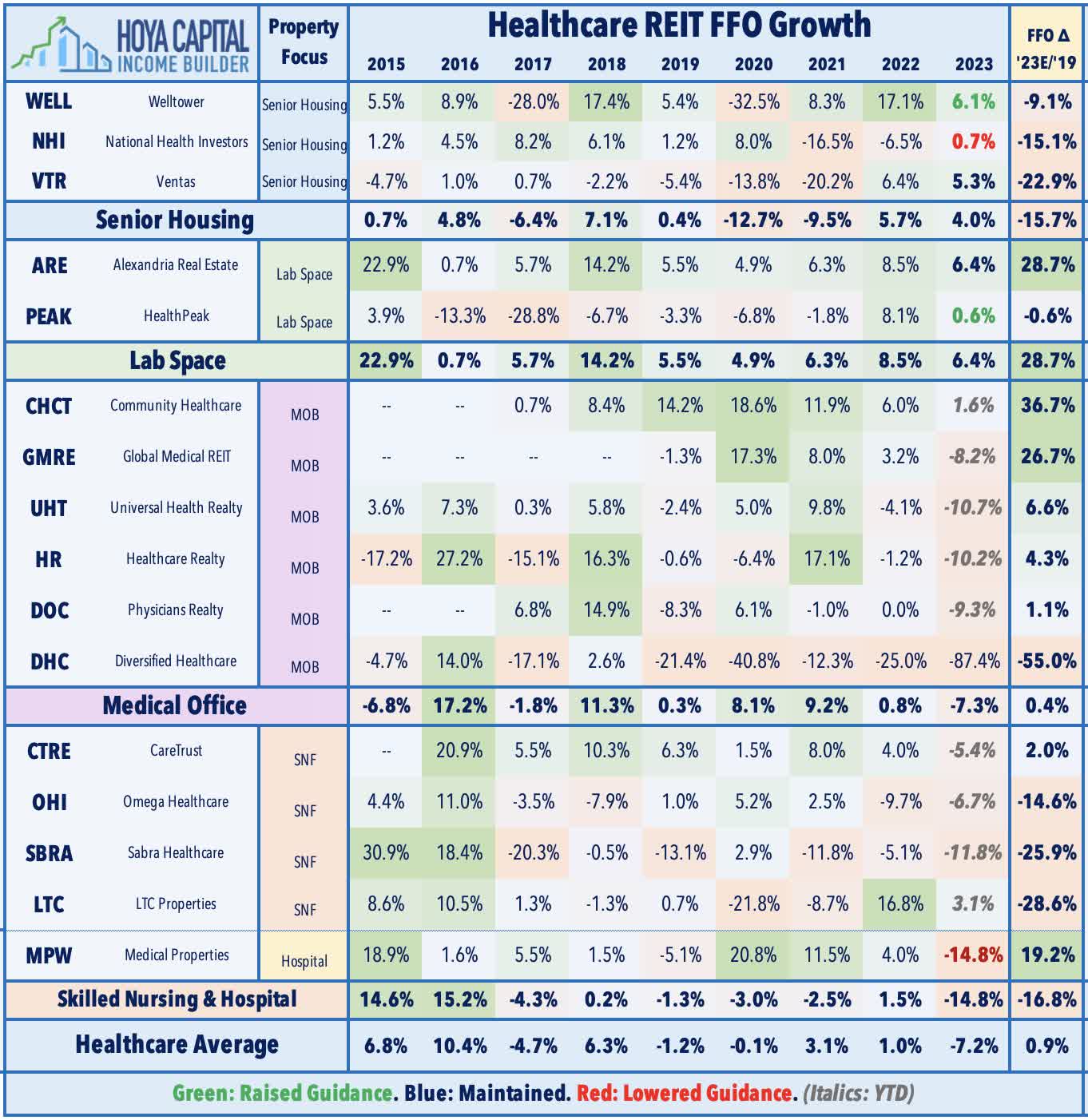

Healthcare : Embattled hospital owner Medical Properties ( MPW ) slid another 6% this week after it was named in a class action lawsuit alleging that MPW "made false or misleading statements and/or omitted material adverse information" related to the timing of the disclosure that its recapitalization deal with Prospect Medical faced a regulatory halt imposed by State of California regulators. At issue is the lack of disclosure in its Q2 earnings report, which occurred three weeks after the regulatory order and came to light through a Wall Street Journal article. MPW released a video message to shareholders in which MPW Chairman and CEO addressed the company's financial position and its recent business dealings that have come under scrutiny. MPW expects its FFO to slide nearly 15% this year amid pressure from higher interest rates and tenant operator rent collection difficulty. Last week in Healthcare REITs: Recovery and Relapse , we noted that public-pay segments - Hospital and Skilled Nursing - have seen a re-intensification of tenant operator issues amid pressure from soaring labor costs and waning government support, triggering some missed rents and lease renegotiations. MPW pared declines later in the week after Australian regulators approved MPW's AUD$470 million sale of four Australian facilities to HMC Capital.

{kind=link}

Healthcare : Sticking in the healthcare space, medical office building ("MOB") REIT Healthcare Realty ( HR ) declined 5% this week after it provided a business update with preliminary third-quarter operating metrics. Among the highlights, HR reported that it achieved record new leasing volumes totaling 447k square feet in the third quarter, improving from 376k in Q2 and 240k in Q1, citing "particularly strong momentum" in volume in the "legacy" properties acquired through its acquisition of MOB REIT peer Healthcare Trust of America. HR noted that occupancy was flat in Q3, but is expected to increase in 2024 based on recent leasing volume. HR also noted that it completed $209M in asset sales since June 2023, bringing its year-to-date dispositions to $318M. The Company affirmed its 2023 dispositions guidance of $400M at the midpoint with an expected cap rate range of 6.5% to 7.0%. In aggregate, HR's closed and pending asset sales total over $600M, which HR notes will "increase the portfolio exposure to higher-growth, multi-tenant, on-campus medical outpatient buildings." Proceeds from these sales are expected to fund development obligations and repay floating-rate debt.

{kind=link}

Billboard : Outfront Media ( OUT ) dipped over 15% this week after JP Morgan cut its price target, citing comments from management regarding third-quarter trends and concern over the impact of the Hollywood writer's strike on its transit advertising division. Billboard REITs have been considerable laggards over the past quarter after reporting weaker-than-expected second-quarter results in which both REITs reduced their full-year earnings outlook, citing a late-quarter slowdown in business advertising spending and continued weakness in their public transit segments. Outfront ((OUT)) reported last quarter that it booked a substantial $500M non-cash impairment on its New York MTA transit segment, an ill-timed 15-year deal signed two years before the pandemic that has proven to be a substantial drag on its otherwise solid billboard business. Lamar ( LAMR ) - which has about 10% of its portfolio in transit advertising vs. nearly 25% for Outfront - also lowered its full-year FFO growth outlook to -2.4% last quarter versus +1.3% previously, citing recent weakness in national brand spending - especially on the West Coast.

{kind=link}

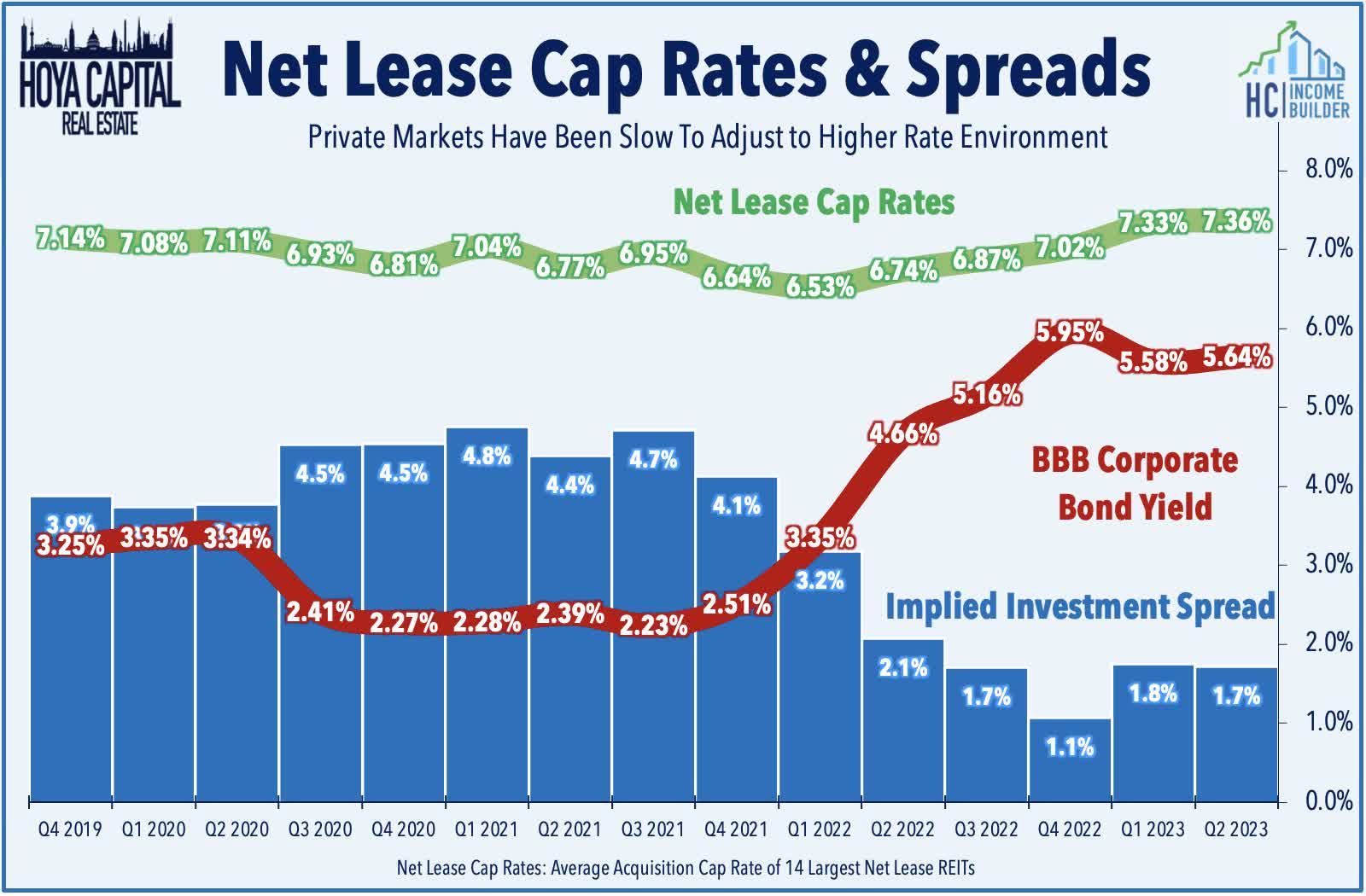

Net Lease : Ground lease-focused Safehold ( SAFE ) was also hit by a JP Morgan downgrade this week, dipping 10% after the JPM REIT team lowered its earnings estimate, citing higher cost of capital and lower deal volume. The selloff came despite a credit rating upgrade from Moody's, which raised its long-term issuer and backed senior unsecured ratings to “A3” from “Baa1” and revised its outlook to stable from positive. Last week, we published Net Lease REITs: Fighting The Fed. Net Lease REITs- one of the most "bond-like" and interest-rate-sensitive property sectors- have lagged in recent months as investors come to grips with a potential "higher-for-longer" interest rate environment. Thriving in the "lower forever" environment, the industry has been reluctant to acknowledge the higher-rate regime, keeping private-market values and cap rates surprisingly "sticky" and resulting in compressed investment spreads. Despite the tighter investment spreads, acquisition activity has slowed only modestly for some REITs- paying top-dollar for recent purchases - a strategy that could prove costly if rates remain elevated.

{kind=link}

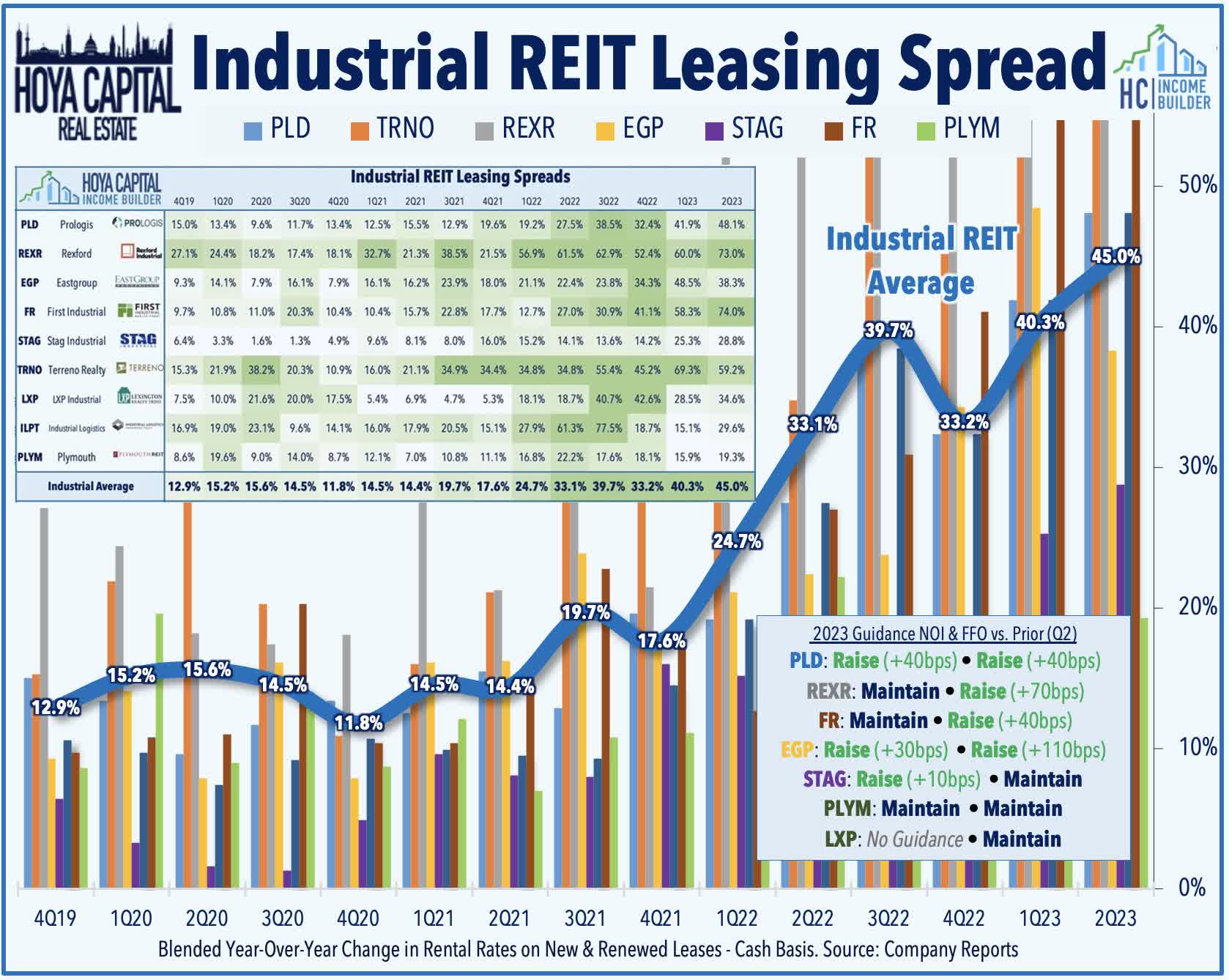

Industrial : Small-cap Plymouth ( PLYM ) was among the better performers this week after it provided a business update that included preliminary third-quarter metrics. Among the highlights, PLYM reported that it achieved blended cash leasing spreads of 24.2% in Q3 across 1.76M SF of new and renewed space - up from the 19.3% increase achieved in Q2 across 2.10M SF of space. PLYM noted that its total portfolio occupancy was 97.6% at the end of Q3, while same-store occupancy stood at 98.7% - each down marginally from Q2. PLYM reported that it completed a 180k SF industrial building in Atlanta along with a 41k SF building in Jacksonville. Overshadowed by the bankruptcy of shipping giant Yellow - and the potential impact on the logistics industry - industrial REITs reported a very strong slate of earnings reports last quarter. After a rent growth moderating in late 2022 - which many expected to continue throughout this year - rent spreads have actually reaccelerated in early 2023, perhaps credited to a moderation in cost pressures for tenants in other areas of the supply chain, specifically freight costs, which are as now much as 90% lower than their peak in September 2021. Five of the seven REITs that provided full-year guidance raised their FFO outlook.

{kind=link}

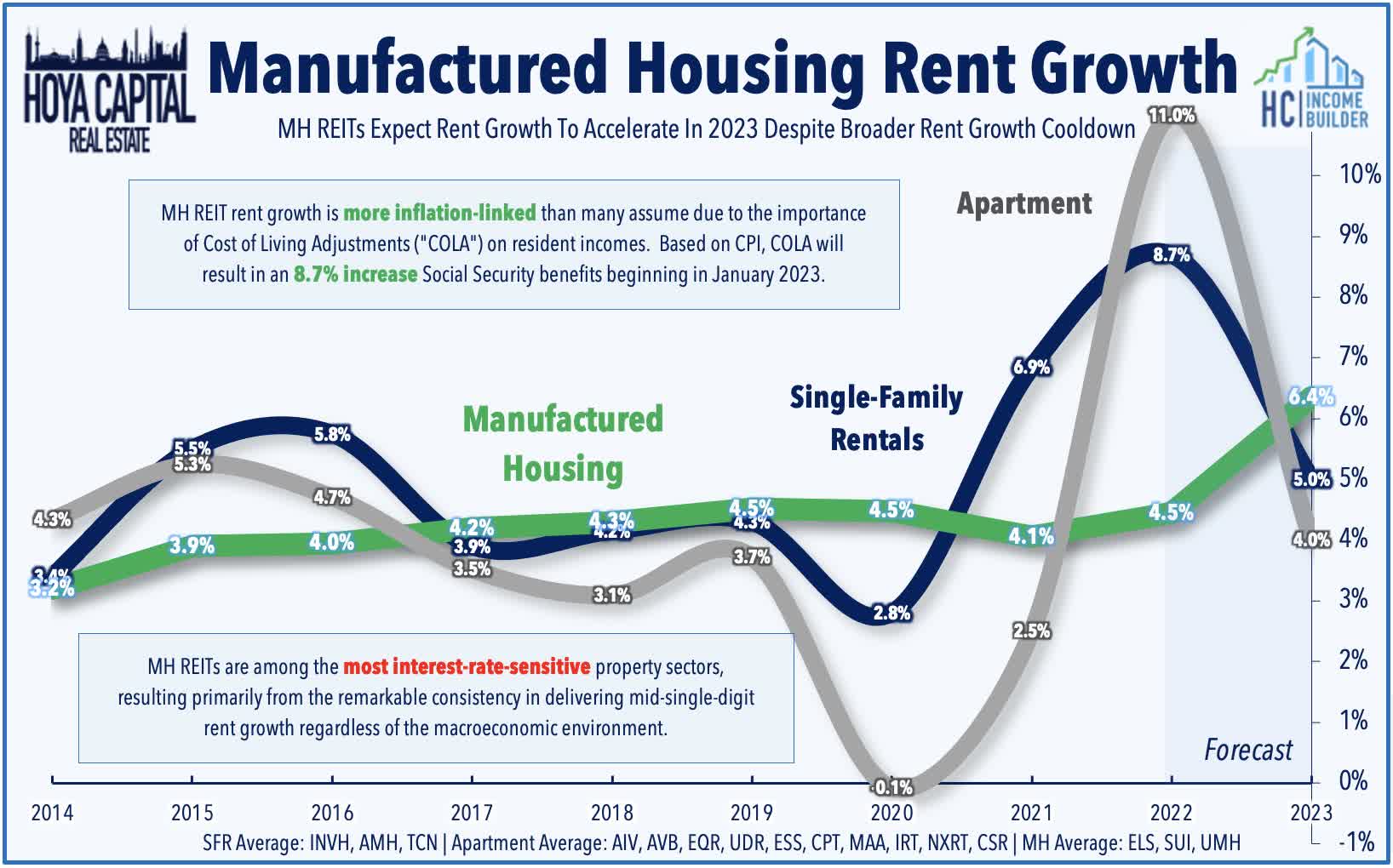

Manufactured Housing : UMH Properties ( UMH ) was among the leaders this week after it provided a business update with preliminary third-quarter operating metrics. UMH noted monthly rental revenue being billed to residents has increased 9.7% compared to its January 1 st rent roll. UMH also reported that year-to-date, it has rented 900 new homes and sold 124 new homes, including the 289 new homes rented and 42 new homes sold in Q3. In our recent sector report, we noted that MH REITs have uncharacteristically stumbled over the past year, pressured by the direct and secondary effects of higher interest rates. Interest rate-related risks have been compounded by concerns over "climate risk" exposure and the effects of a post-COVID demand normalization in the recreational vehicle and marina business segments. Domestically, fundamentals within these REITs' core manufactured housing segment are as strong as ever. Propelled by COLA effects - which has provided a sizeable percentage of its resident-base with 9% income boosts, rent growth has accelerated this year even as broader residential rents have moderated.

{kind=link}

Single-Family Rental : Invitation Homes ( INVH ) was also among the best performers this week after Evercore upgraded the SFR REIT to Outperform from In-Line, citing improved supply-demand trends in the single family residential market and expectations that rent growth will outpace traditional apartments. Evercore noted, "we expect the SFR space to hold up better in an economic slowdown given the affordability gap vs. home ownership and limited new deliveries." One of just two property sectors in positive-territory this year, Single-Family Rental REITs have rebounded as the dire predictions of a "hard landing" in rental markets have been rebuffed in recent months by steadying rental rates and relatively strong occupancy trends seen across the major rent indexes. While multifamily markets face supply headwinds over the next year, single-family builders have pulled back from an already historically supply-constrained single-family market, fundamentals that support sustained inflation-beating rent growth. These REITs have played it safe - a privilege earned through disciplined balance sheet management - but tighter financing conditions will be a catalyst to drive further market share gains to larger institutions that have access to cheaper and deeper capital.

{kind=link}

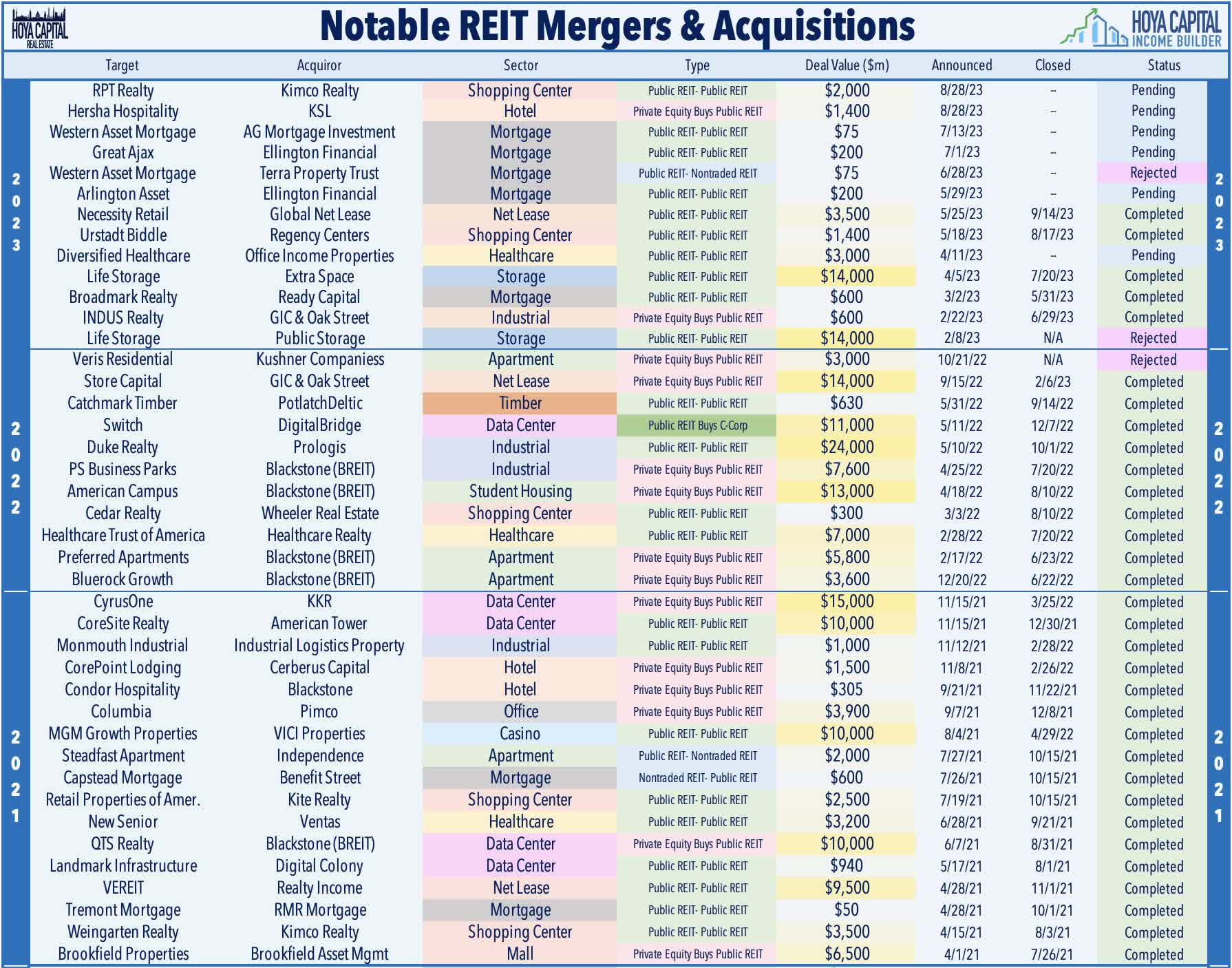

Hotel : Hersha Hospitality ( HT ) announced that it will hold a special meeting of shareholders on November 8th for the approval of its previously announced acquisition by affiliates of KSL Capital Partners, LLC. Following a wave of REIT privatization in 2021-2022, the Hersha acquisition is one of just two such deals thus far in 2023, along with the acquisition of Indus Realty by Centerbridge Partners and GIC Real Estate. Instead, we've seen a revival of M&A activity from within the public REIT sector itself, with a record-setting pace of nine public REIT-to-REIT mergers thus far this year. The largest of these REIT-to-REIT mergers is the deal between Extra Space ( EXR ) and Life Storage , which combined to form the largest storage REIT. We've seen two mergers in the strip center space: Regency Centers ( REG ) closed on a deal to acquire Urstadt Biddle earlier this month, while Kimco Realty ( KIM ) announced last quarter that it would acquire RPT Realty ( RPT ). We've also seen four mREIT mergers led by Ellington Financial ( EFC ), which has scooped up a pair of smaller mREITs: Great Ajax ( AJX ) and Arlington Investment (AAIC).

{kind=link}

Mall : Small-cap mall REIT CBL Properties ( CBL ) was among the upside leaders this week after announcing that it closed a new $79.3 million loan ($39.7M at CBL’s 50% share) secured by The Outlet Shoppes of Atlanta, noting that the new non-recourse ten-year loan bears a fixed interest-only rate of 7.85% and replaces two loans with an aggregate balance of $69.5M (at 100%) that were set to mature in November 2023. With recent distress across office markets seizing the headlines, Mall REITs are no longer the "Problem Child" of the REIT sector, particularly after weaker players and lower-tier malls closed shop. Following three years of rental rate and occupancy declines, the supply-demand dynamic has recently favored retail landlords, rewarding many retail REITs with some long-elusive pricing power. Store openings have outpaced closings by nearly 2x since 2021, which has helped mall REITs regain some footing and repair balance sheets in anticipation of tougher times ahead.

{kind=link}

Mortgage REIT Week In Review

Mortgage REITs were under significant pressure for a third-straight week amid a rebound in interest rate volatility, as the closely-watched MOVE Index surged to the highest levels since May this week, which pressured many of the more highly-levered mREITs. The iShares Mortgage REIT ETF ( REM ) dipped another 5.7% on the week, dragged on the downside by a sharp 30% decline from renewable energy-focused Hannon Armstrong ( HASI ) after JP Morgan slashed its price target by nearly 25%. Rithm Capital ( RITM ) was among the best performers after it announced a $720M deal to acquire Computershare Mortgage Services, which will add a mortgage servicing rights portfolio of about $136 billion in unpaid principal balance (UPB) to the company. It also includes $85 billion in third-party servicing and the Specialized Loan Servicing’s MSR portfolio. Rithm expects to close the acquisition in the first half of 2024 and intends to use a mix of existing cash, available liquidity on the balance sheet, and additional MSR financing to finance the Computershare deal. The acquisition is the second major acquisition for RITM in recent months, following a deal to acquire Sculptor Capital for $639m, which has faced challenges from a competing shareholder group.

{kind=link}

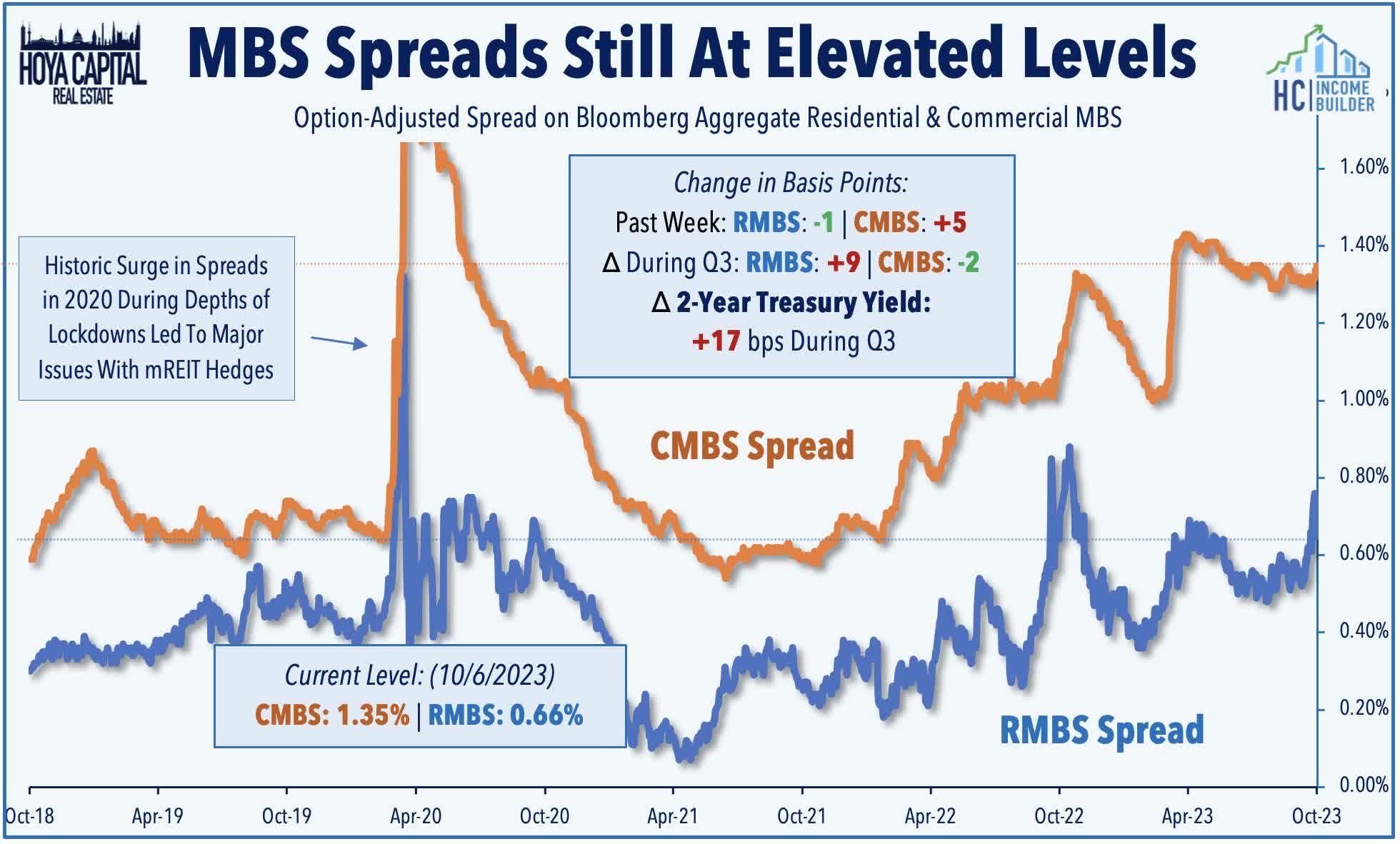

Book Values remain in focus amid the recent resurgence in interest rate volatility and broader weakness on CMBS and RMBS valuations ahead of the start of third-quarter earnings later this month. The iShares MBS ETF ( MBB ) - an un-levered benchmark tracking RMBS valuations - declined another 1.7% this week - among the sharper single-week declines we've seen in recent years - which follows a 3.7% during the third quarter. The iShares CMBS ETF ( CMBS ) declined 1.0% this week following a third-quarter decline of 1.2%. Spreads on mortgage-backed bonds ("MBS spreads") - an important input into Book Value models - have trended higher over the past three weeks. Since the end of Q2, RMBS spreads have widened by 8 basis points to 0.66%, while CMBS spreads have widened by 3 basis points to 1.35%. Benchmark interest rates - the other critical input affecting Book Values - have also increased during this period, with the 2-Year Yield higher by 16 basis points.

{kind=link}

2023 Performance Recap & 2022 Review

As we enter the final quarter of 2023, the Equity REIT Index is now lower by 9.9% on a price return basis for the year (-7.4% on a total return basis), while the Mortgage REIT Index is lower by 4.7% (+0.2% on a total return basis). This compares with the 12.3% gain on the S&P 500 and the 1.3% advance for the S&P Mid-Cap 400 . Within the real estate sector, just 2-of-18 property sectors are still in positive territory on the year, led by Data Center and Single-Family Rental REITs, while Billboard and Cell Tower REITs have lagged on the downside. At 4.78%, the 10-Year Treasury Yield has increased by 91 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% in April - and now hovering at 15-year high. Following the worst year for bonds in decades, the Bloomberg US Bond Index is lower again this year, producing total returns of -2.4% thus far. WTI Crude Oil - perhaps the most important inflation input - is higher by 6% this year and remains roughly 25% below 2022 peaks. Natural Gas prices are lower by 45% this year.

{kind=link}

Economic Calendar In The Week Ahead

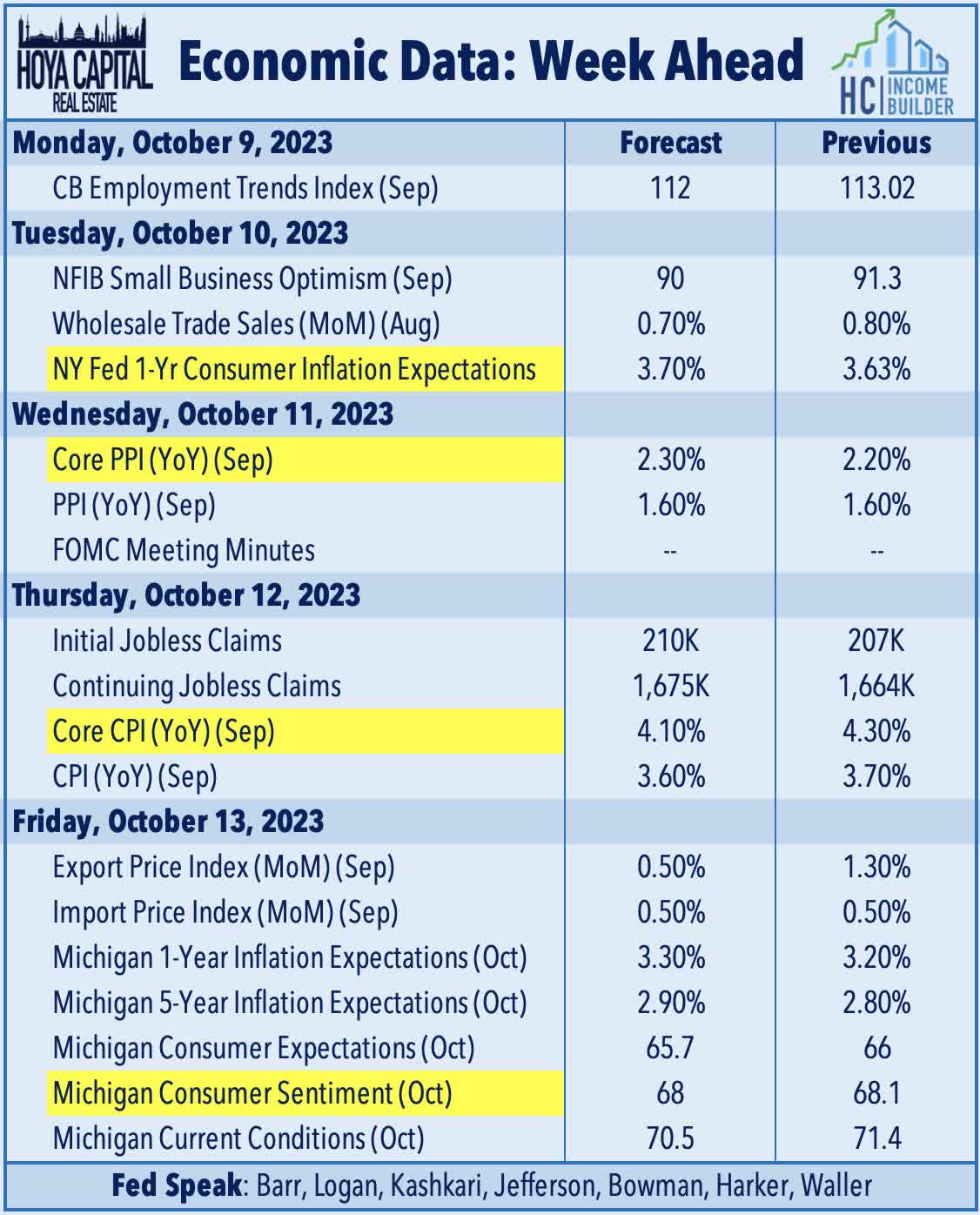

Inflation data is in the spotlight in a jam-packed week of economic data in the week ahead. The main event comes on Thursday with the Consumer Price Index for September, which investors and the Fed are hoping will show a continued cooling of inflationary pressures. The Core CPI is expected to moderate to a 4.1% year-over-year rate - down from 4.3% last month - while the headline CPI is expected to cool slightly to 3.6% from 3.7% as some of the "hottest" prints seen in mid-2022 begin to roll off. Gasoline prices - which drove a modest reacceleration in inflation in August - were roughly flat in September compared to the prior month. We've noted in recent reports that "real-time" inflation - as measured by the CPI-ex-Shelter Index - has averaged only 1% since last July as significant goods deflation has offset stickier services inflation. On Wednesday, we'll see the Producer Price Index, which has recently shown an even more significant cooling of price pressures. The Core PPI is expected to increase modestly to 2.3% from 2.2% in the prior month, while the headline PPI is expected to show a 1.6% annual increase - down from the recent peak last March at 11.8%. On Friday, we'll get the first look at Michigan Consumer Sentiment for October - a report which includes the closely-watched inflation expectations survey.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Good News Is Bad News