PARA - Google: Dominant Innovative And Adaptable - Yet Recession Risk Remains

2023-09-06 14:00:16 ET

Summary

- While Alphabet Inc.'s stock is at risk of a significant decline due to recession risks, Google is situated well for a stagflation environment and long-term growth.

- Google's moonshot projects and investments in new technologies offer potential long-term growth opportunities.

- Balancing the risk of recession with the potential benefits of long-term growth is difficult with limited data.

- I share the three ways I'm thinking about Google stock in relation to my personal investing strategy despite the lack of historical recession data.

Introduction

It's a difficult task to write articles that warn investors about the stocks of great businesses like Alphabet Inc. ( GOOG , GOOGL ) aka Google . It's an even more difficult task to make a habit out of it as I so often do. But, it is precisely because it's difficult to do that it is so important that somebody does it. Often, as investors, it's when we are right about the quality of a business we stand to lose, or at least underperform, the most. In the words of Warren Buffett:

For the investor, a too-high purchase price for the stock of an excellent company can undo the effects of a subsequent decade of favorable business developments."

Taking this a step further, if an investor is like me, and is aiming for better-than-average returns over the long term, then usually we not only have to avoid paying too much for a stock, but we actually need to underpay for it. Convincingly framing this sort of thinking for readers is tricky business. I'm often warning about risks that I think have a high probability of materializing, but that doesn't mean they always materialize. And just because they might not, doesn't mean the risk didn't exist. For example, we ultimately got COVID-19 vaccines pretty quickly following the onset of the pandemic, but I don't think investors should have counted on vaccines when making investments during that time. There ended up being just enough Democratic Senators elected in 2020 to pass trillions more dollars in stimulus, but I don't think, as narrow as those election victories were, investors should have counted on it. Over time, it's best to recognize potential risks and rewards and try to keep the odds comfortably on your side because, over the long run, the odds will win out.

With that context in mind, I first wrote about Alphabet on February 24th, 2022 with my warning article " Apple & Alphabet Will Not Side-Step A Deep Bear Market ." In that article, I warned that the earnings boom caused by stimulus money stopping would likely turn into a bust for Alphabet's earnings, and likely send the stock price significantly lower.

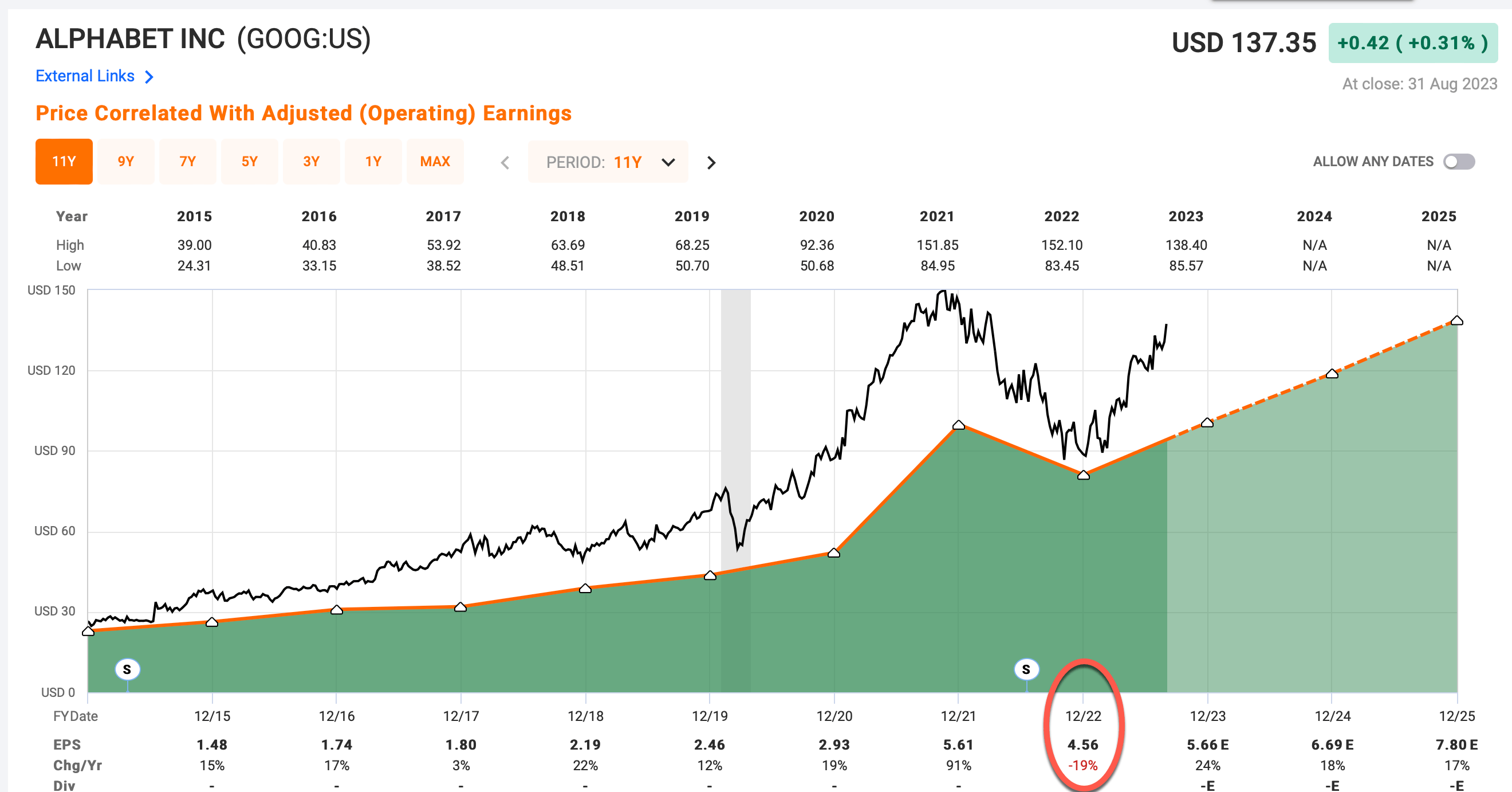

I estimate that without COVID stimulus Alphabet's previous EPS trend would have had them earning about $75 [$3.75] per share in 2022, and right now analysts are expecting about $116 [$5.80] per share. As with Apple, these additional stimulus earnings will likely help adjust the previous trend upward a bit, and that money will continue to circulate in the economy for a while, so, perhaps EPS won't fall all the way down to the previous trend line, but I think for analysts to expect $134 [$6.70] per share of earnings in 2023 is wildly optimistic.

An additional consideration for investors is that during the last recession of any length in 2008, Google managed to grow EPS at over 40% per year because they were then still a relatively small and fast-growing business. Now they are a $1.7 trillion company. Most of Alphabet's revenue comes from advertising, and advertising has a long history as a cyclical industry. Investors should expect that EPS growth will be deeply negative during a "normal" recession. Now add on top of that a recession that is preceded by an advertising boom fueled by what is likely to be one-time stimulus money, and it sets up GOOGL stock for a potentially very steep decline. The stock price will almost certainly fall far enough to reach bear market territory, and I probably wouldn't consider buying it until it was -40% or -50% off its highs.

(The [brackets] contain the split-adjusted numbers.)

And I went on to clarify in the comment section regarding the odds of various drawdown scenarios:

While I think a -50% drop is possible, and investors should know it's possible, and while I think a -20% has an extremely high probability of occurring, I would say a -30% to -40% drop is probably the most likely scenario. It's not that Apple and Google aren't great businesses. It's that the market expects them to be greater than great. Greater than great businesses rarely see EPS decline from one year to the next, and I think there is a high probability of that happening with both of these businesses within the next two years.

Part of my thesis at the time was the resumption of student loan repayments, which actually hasn't happened, yet, so some of the potential risk during this period was delayed, but Google stock did fall about -35% after the publication of that article in 2022 until climbing its way back to even this year.

{kind=link}

We can see in the FAST Graph above that Google did experience a "bust" following the boom in earnings last year as was my thesis. However, the delaying of student loan repayments along with it taking some time for excess pandemic savings to be spent down, meant the earnings decline wasn't as deep as it could have been if all those adverse effects had hit at the same time.

I wrote two additional articles during the 2022 price decline where I shared the price I would be willing to step in and buy Google stock myself. The first one was "Google Missed Earnings As I Expected; Here Is The Price I'll Start Buying."

The price at which it would cross the 12% 10-year CAGR expectation and achieve a margin of safety is $74.85, and I would likely be a buyer if the stock hits that price. Right now, I would give it about a 50% chance of falling below that price if we have a recession next year, which is my base case. I plan to stick with this $74.85 buy price through the current quarter, and then I'll make adjustments after the next earnings report for 2023.

The share price came close to those buy prices near the trough of $83.45, but never quite had the margin of safety I wanted late last year before the current rally started. This actually isn't too unusual for me, occasionally a stock will go from overvalued enough to sell to undervalued enough for me to buy. It happened with Stryker ( SYK ) in 2019 and 2020, and I was able to warn investors of the high valuation, then buy it during a downturn, and take a 60% profit in less than a year after the recovery. But usually, it takes longer for a high-quality overvalued stock to become undervalued, unless we have a recession, and we haven't had a recession, yet. Still, Google got very close last fall to becoming a buy. After earnings and inflation both came in higher than expected at the end of last year, I updated my buy price for 2023 to $84.58 per share, and haven't updated it since.

What makes Alphabet stock so difficult to gauge?

Usually, I only write articles about stocks I would consider buying myself, and I have a pretty high minimum quality threshold. The only exception to that is if I see a specific danger I think other investors might be missing, I will sometimes write articles that explain the quality-related reasons I'm avoiding a stock. So, when I was writing bearish articles on Alphabet in early 2022, I was never bearish on the long-term prospects of the business, I was just bearish on short-to-medium-term earnings which I thought investors would want to know about, and which I thought had a high probability of pushing the stock price lower. We have managed to avoid a recession since late 2022, and that saved Google stock from dipping lower, but recession risk is definitely still on the table in the near future, so that risk hasn't gone entirely away.

What makes Alphabet difficult to gauge is that most of its core business is dependent on advertising and advertising has traditionally been a cyclical business. As Alphabet states in the risk section of their 10-K :

We generate a significant portion of our revenues from advertising. Reduced spending by advertisers, a loss of partners, or new and existing technologies that block ads online and/or affect our ability to customize ads could harm our business.

We generated more than 80% of total revenues from online advertising in 2022. Many of our advertisers, companies that distribute our products and services, digital publishers, and content providers can terminate their contracts with us at any time.

While Alphabet is mostly referring to competitive risks in advertising, having 80% of revenues dependent on advertising makes earnings susceptible to declines during times of economic weakness like recessions. My typical method of estimating what sort of earnings declines we might expect during a recession is to look at past recessions and see what a particular business's earnings did previously. But Google's last real recession was 2008/9 when it wasn't a fully mature business, yet, and much of the advertising landscape has changed dramatically since then anyway, so I honestly don't think anyone knows what an average recession would do to Google's earnings. I feel confident earnings growth would be negative, but I don't know by how much. Additionally, since we didn't get a recession last year, Alphabet has had time to cut spending fairly dramatically this year, so they have a head start mitigating some of the earnings damage of a potential recession might cause.

All that said, I think analysts' earnings estimates for Q4 2023 have been very optimistic all year.

{kind=link}

Analysts are expecting 50%+ EPS growth in Q4. Alphabet did have good 2Q earnings so I suppose it's possible, but let's look at revenue growth.

Google's trailing twelve-month revenue growth is only about 4%. And while last quarter did see some acceleration, my gut tells me that there will be a limit to what Google can do via cost-cutting if the economy weakens in Q4, or if advertising significantly weakens in Q1 after the holiday season. This means over time earnings growth is likely to follow revenue growth more closely, and revenue growth is slow. A recession would almost certainly tip both revenue and earnings growth significantly into negative territory.

Looking ahead to 2024 and 2025, analysts expect EPS growth in the high teens. Unless we avoid a recession over the next 2.5 years entirely, expecting that sort of earnings growth is very optimistic. The stock is trading at about a 25 P/E ratio, so if analysts end up being correct about medium-term earnings growth, then the stock looks reasonably attractive here, particularly on a relative basis. The catch is, that everything would likely need to go right, and I don't like to buy stocks with the expectation of everything going right without interruption. The Fed has dramatically raised interest rates over the past 18 months. Saved stimulus money is running out. Student loan repayments are resuming. Estimating the timing of when these economic drags hit Google's earnings is difficult, but seeing that recession danger is there, isn't.

So, we have a great business that has a high probability of hitting, at the very least, a soft patch, potentially, also experiencing a more significant earnings decline. How should an investor who is aiming for better-than-average returns approach this stock? What strategy makes sense to maximize the current medium-term risk reward?

I'll share my thoughts and my personal strategy in the remainder of this article.

Alphabet's "Other Bets": The Wildcard

One of the things I love about Alphabet's business is they have a combination of a fantastic current business, but they also continue to invest in new technologies, often outside of advertising. We have Waymo, their self-driving car service. Some people think electric vehicles are the future because they don't use gasoline. I have a slightly different view. I think electric vehicles are the future because they can more easily become nearly fully autonomous. In the end, it's about productivity, and EVs themselves aren't necessarily going to make society or the people in it more productive. Self-driving cars, however, once they are improved enough, will be the next great leap in human productivity and they stand to massively reshape society for the better. Being a leader in this area is a great way to supplement Alphabet's core businesses over the long term. While it is difficult to place a value on it today, I think it does offer a window into how such a large company might sustain value and growth over the long term.

Then, on top of this, we have Google's research with AI and their Cloud businesses. My approach, as an investor, when thinking about AI is probably different than most investors who are looking for positive beneficiaries of AI like Nvidia ( NVDA ) (especially the large language models that were popularized this past year). I'll be short and to the point here. This sort of AI will fundamentally change businesses and almost certainly improve productivity in the aggregate.

But, I don't think we know right now what the best AI investments will be for stock investors, yet. It is still in the very early stages of adoption. In the year 2000, if we were going to bet on "search" in its early stages of adoption and use, we would have bet on Yahoo! Everyone who did that ended up being wrong. So, I think it's too early to pick positive AI winners in the market.

However, as Alphabet announced during their recent "Cloud Next" event, they have all kinds of initiatives and partnerships with AI developers in place, and "More than half of the generative AI startups are using Google's Cloud." The way I view this, as a relatively conservative investor, is that Google is going to be a significant part of and integral to the AI revolution, which means, if nothing else, it stands a good chance to mitigate potential competitive threats to its core business.

My very early take on AI from an investor's standpoint is it will probably continue the trends we have seen with social media platforms, and investors should probably be on the lookout more for those businesses that might be disrupted by AI efficiencies than to look for positive bets on AI winners. I think AI will increase the value of platforms and increase the efficiency and reach of smaller businesses. Just as targeted advertising has allowed smaller businesses to market more efficiently and compete better with large established brands, I think AI will not only improve this type of marketing but also allow businesses to run quality marketing campaigns with fewer people, especially during the early life of the business. Generative AI might not be able to run outreach and marketing by itself, yet, but if it reduces the time and expense by 50% to 80%, which I think is a very reasonable estimate for some businesses, the moats of many mega-brands will be much narrower than they have been historically.

The big-picture dynamic is smaller businesses partner with the Alphabets, Microsofts, Amazons, and Metas of the world to effectively reach their target audience with extreme efficiency. So, I would be cautious with large cap businesses that rely mostly on legacy branding, especially if they have relatively high valuations, and I've warned about Estee Lauder ( EL ), Nike ( NKE ), Proctor & Gamble ( PG ), Brown-Forman ( BF.B ), and many more. The combination of high valuation and decreased moat from their brands, could spell trouble for stock investors in these types of businesses. We are seeing it now with legacy media too, like Disney ( DIS ), Paramount Global ( PARA ), Warner Bros. Discovery ( WBD ), and Comcast ( CMCSA ) where YouTube and TikTok, with creator-created content, are delivered directly to viewers, largely cutting out the gatekeepers and middlemen. AI will only make this content faster and easier to produce going forward. It creates a moat for Alphabet that many alternative stock investments simply won't have going forward.

We also have Alphabet's healthcare data and technology business, both of which will almost certainly be areas of future long-term growth. Basically, as long as the world continues to progress and move forward, the odds are very high that Alphabet will be part of that progress. As I've said before, it's hard to place a value on a business that brings some of the smartest people on the planet together to solve problems.

My Strategy

This section will be a little personal as to my own investing strategy, and those I use in my Investing Group, The Cyclical Investor's Club, which is the perspective I usually write from anyway (I don't rate stocks "Buys," for example, unless I've actually bought them myself). Hopefully, there will be some broader food for thought presented in this section that can be adapted and applied by those using different strategies as well.

I'll frame this by pointing out that in terms of starting weights of initial positions, I usually use 1% portfolio weightings, but I will let winners run for as long as the valuations don't get too extreme, so I don't rebalance for rebalancing sake. We've had an interesting development with the market indices lately in which a great deal of the market capitalization of stocks has become increasingly concentrated in a handful of mega-cap stocks like Alphabet.

Above is a chart of the 5-year returns of the S&P 500 ETF ( SPY ) compared to the equal-weighted S&P 500 ETF ( RSP ), and the Russell 2000 ETF ( IWM ). We can see a fairly massive divergence that has occurred simply because of the growth of a small number of mega-cap stocks. Alphabet, for example, would have an approximate 0.20% to 0.25% weighting in the equal-weighted RSP, but has roughly a 4.00% weighting in SPY, about 20x bigger.

On one hand, such a large weighting might be concerning, but most of the mega-cap stocks are composed of several different businesses. In that sense, the business concentration risk isn't as high as the stock concentration suggests. And so even if a person has an unconcentrated strategy as I do, they could overweight a mega-cap position and still be underweight relative to the index. For example, I would have to start 4 positions with a 1% weighting to equal Alphabet's current weighting in the S&P 500. Traditionally, I rarely start positions with more than a 1% weighting and I basically never go above a 2% weighting. But I think what Alphabet shows, is an investor could go higher than that even while carrying out a strategy like mine.

Next, I want to take this thinking and layer in the fact that I employ multiple investing strategies at the same time, and sometimes they can overlap. I have four main strategies; a strategy for deeply cyclical businesses, one for GARP-like stocks, one for fast-growth businesses that might be earlier in their development and riskier but potentially offer a higher long-term reward, and a REIT strategy. What is interesting, is that Alphabet could potentially fit into 3 of the 4 strategies, but the historical data is limited, so it can be tricky to identify and classify.

As I noted earlier, advertising is usually a cyclical business, but we haven't really had a down cycle since Google's ads business was mature, so we don't really know how cyclical it will be. Recently, in articles over the past two years, I have mostly treated Google stock as a moderately cyclical growth-at-a-reasonable price stock that had stimulus boom/bust risk. But I think a case can also be made that Alphabet's moonshots and other bets might fit my fast growth strategy...I just don't have enough data to tell for sure. We do have a situation where there is room for multiple approaches to buying the stock that mostly keep within the framework of my current investing strategies (which is something I have a strong preference for doing when I can).

I've had a couple of recent stock examples that might offer some guideposts for how to potentially approach Alphabet. One of them is Advanced Micro Devices, Inc. ( AMD ), which I wrote a series of articles about this past year. And the other one is Netflix ( NFLX ). I bought both these positions when the stocks were near their lows in 2022. Netflix, I actually had a double position because I bought one position using my fast growth strategy and one using the GARP-like strategy. AMD, I was prepared to buy a second position, but only the first buy price hit near the lows last fall. Both of these stocks more than doubled off their lows and I ended up taking profits in half my AMD position (which I wrote publicly about here ) and 2/3rds of my Netflix position. Selling partial positions is something I almost never do, so these moves were not normal for me.

AMD and most semiconductor businesses right now have two overlapping earnings patterns. On one hand, their earnings fluctuate a lot and are deeply cyclical, but on the other, their industry is currently in a secular growth phase, which means both the earnings troughs and earnings peaks are higher than the cycle before. I bought AMD as a deep cyclical, and that position quickly doubled, partly on AI speculation. Usually, if a deep cyclical rises on speculation (especially in the middle of a downcycle) the odds are it will fall deeply again. But because of the underlying secular growth, just how far the stock will fall is difficult to determine. So, I sold half, treating it as a deep cyclical in danger of a downcycle, and kept half (a 1% weighting), holding it long-term for the secular growth potential. This was a way to combine the cyclical and secular growth aspects together while keeping within the bounds of my larger investing framework.

Netflix was a little different, it combined one position of my fast growth strategy in March of 2022, which is a buy-&-hold strategy, with a second position using my GARP strategy which is more valuation sensitive, and that second position was purchased near Netflix's lows in May 2022. These positions were separate from the start, and I was able to sell the more valuation-sensitive position entirely earlier this summer for a +121% gain, while continuing to hold the fast-growth position for the long term as a bet on Netflix's continued dominance in streaming for years to come.

Both of these adjustments were made, in different ways, but it offers a rough framework for how I might go about creating an investment framework for Google, even though I lack much of the historical data I would typically like to have. Importantly, having an investing framework isn't just about establishing "buy prices." It is also about having a plan and understanding the conditions under which I would sell a stock as well. For deep cyclicals, I usually know the price I will sell before I even buy the stock. For GARP stocks, usually, the potential future sale only happens if the valuation gets exceptionally high, or the business fundamentals deteriorate. For fast-growth businesses, those are almost always "buy-and-hold" for the very long term unless something unusual happens that shows my initial thesis was deeply flawed or an error. So, these different categories are very important. As I tried to show with AMD and Netflix, one strategy can signal a sell while another says to hold. The important thing is they remain generally consistent with the given strategy.

Alphabet as a GARP stock

I've been tweaking my standard GARP valuation strategy (which I call "Full-Cycle Strategy") this summer to account for an environment I call "Fragile Stagflation" in which inflation and interest rates remain relatively high, but in which the economy remains pretty fragile, so that a spike in energy prices or normal trade relations or a debt crisis could send the economy into a recession. This is basically what we have been in for the past 18 months. Alphabet benefits from this on a relative basis because they don't have a lot of debt while many other businesses in the S&P 500, and especially the Russell 2000 do. This makes Alphabet's valuation more attractive on a relative basis.

Unfortunately, we don't have good recession data for Alphabet, but I can now use 2022's earnings decline as a rough guide for what we might expect during a mild recession, so there is at least a fuzzy guidepost where none existed before. When I put this all together I get about a 13% expected long-term earnings growth rate for GOOG, and a buy price of about $92.69 per share if we get a mild recession or significant economic slowdown at some point over the next year or so.

Alphabet as a Deep Cyclical

Again, we don't have good historical data to go on, but let's look at the 2022 drawdown as a potential guide.

For deep cyclicals, I typically look at historical price cycles as a guide for future downcycles because earnings can fluctuate a lot and make traditional valuation techniques unreliable. Even without a recession, we saw GOOG stock fall almost -45% off its highs in 2022. Usually, with deep cyclical stocks, I don't buy them unless they are at least -50% off their highs, and I try to buy only the ones I think will recover within 5 years for a 100% gain. If we take this approach with GOOG, we get a deep cyclical buy price of $76.05 during a recession.

Alphabet as a Fast-Growth Business

This is the trickier of the three strategies to make a case for and establish a good price to buy because it's largely based on speculation and forecasting over the very long term. And because Alphabet is already so large it makes it difficult to confidently forecast very fast growth over a very long period of time. But it's possible they could do something like spin-off several successful businesses while the ads business holds its own over the next couple of decades. The way I would think about it is Google probably needs to grow earnings at 20% compounded for 10 years in order to qualify as a long-term "fast growth" business and I would want to 5x my investment over that time period. If you think some of Alphabet's moonshots will pay off in a big way over the long term, then buying around $100 per share and simply holding long-term rain or shine is a reasonable strategy.

Personally, I don't see enough evidence yet to say Alphabet is a good fit for that strategy. I wouldn't assume more than 15% earnings growth long term, but that could change as time goes on if one of their moonshots hits.

Conclusion

It is very important if we want good returns as long-term investors to develop processes, principles and strategies that we can consistently and confidently implement so that we don't primarily take our cues from stock price movements and financial media. But, we also need to remain flexible around the edges and try to adapt to the world as it is. Within the dozen or so mega-cap stocks that have been driving the S&P 500 higher this year, there are probably over 100 smaller businesses. This can make it hard to get some of the data we would like to see in order to make good decisions, but we have to adapt, if we can, to the way it is.

I seem to have become known for maintaining stubbornly low buy prices at times. That's partly because I'm seeking higher returns than most investors, but it's also because I have a strong preference for the availability of certain data before I buy a stock. I think it's good to have enough flexibility to do the best one can to adapt even while understanding that sometimes we might have to write a stock off as "too hard" even if it is a major component of the overall market. Hopefully, readers found the framework I've shared useful, and can adapt some of it to their own situations.

For further details see:

Google: Dominant, Innovative And Adaptable - Yet, Recession Risk Remains