GRAB - Grab Holdings: SE Asia's FANG Has Formed

2023-10-04 08:30:00 ET

Summary

- While the market has fallen out of love with SE Asia's tech sector, in my view, the reality is that it is more attractive than it's ever been.

- I think you will read at least a couple novel ideas in this exploration of Grab Holdings Limited's Q2 2023 and its business broadly.

- Number one, the reality is that SE Asia is dominated by only three tech platforms: Sea Ltd., Grab, and GoTo. These are SEA's the most well-capitalized, most dominant tech platforms.

- Number two, SE Asia has been going through something akin to the U.S.'s early 2000s Dot-Com Bubble burst, resulting in slowing growth across the board and especially for the region's ecommerce growth.

- Eventually, SE Asia will emerge from this malaise, and Grab, Sea Ltd., and GoTo could certainly perform incredible feats of value creation in the decades ahead, by virtue of their exceptional resources, which have resulted in dominant competitive positions in the region.

Catching Up With Grab

{kind=link}

In 2021, I accumulated AGC (the Altimeter Capital SPAC that effectively took Grab public) at about $10-$12/share. I principally did this because I knew we were in The Everything Bubble, and I knew that AGC (which would eventually become Grab via a SPAC merger) could not fall below $10/share.

In mid-2021, AGC announced its merger with Grab Holdings Limited (GRAB).

By late-2021, AGC, ahead of its transition to ticker symbol Grab, which essentially meant Grab was to IPO as a standalone company (in a sense!), rallied into the mid teens, at which point I decided to sell most of my Grab holdings, which included warrants and equity.

I sold because we knew it would likely decline 50%+ below its $10/share IPO price based on the SPAC "IPO" valuation.

In the subsequent year (2022), it did fall below that price and then some as panic gripped markets on the heels of the fastest interest rate hiking cycle in American history, which spawned the 2nd, 3rd, and 4th largest bank collapses in American history.

But while it fell mostly due to valuation, the core business actually improved quite dramatically during the period in which I've, for the very most part, not owned the business.

With all of the contextualizing commentary in mind, I have spent a great deal of time doting on the company, and for good reason! I will delineate these reasons for you today. They are, indeed, good and numerous.

In my estimation, while this is rarely if ever articulated, SE Asia is actually dominated by three tech platforms:

- Sea Ltd. ( SE )

- Grab

- GoTo (Gojek is essentially Lyft in SE Asia. Grab is figuratively and literally Uber, as Uber sold its division in SE Asia, and this division became Grab. Tokopedia, which is a rival to Shopee in Indonesia, which is SE Asia's largest ecommerce market, merged with Gojek to create GoTo. GoTo trades on the Indonesian stock exchange, as an aside.)

Others may disagree with me, but it's worth noting that Pareto's Principle will ultimately dictate the economic outcomes of SE Asia's tech sector, and, from what I've gathered through studying Sea, Grab, and GoTo exhaustively, these businesses represent the 1-5% of the system that will account for 90-95% of the economic output and that will capture, correspondingly, 90-95% of the economic value in the region's tech sector, akin to FAANGM in the U.S.

As many of you have likely read in publication after publication:

To this end, the same will play out in SE Asia in the years and decades ahead, with most of the value creation concentrated into a very limited number of companies, which, in my eyes, will very clearly be Sea, Grab, and GoTo.

And, of course, this dynamic, i.e., Pareto's Principle, is found in all realms of "energy systems."

A small number of actors in any given energy system will account for the majority of that systems energy output, in whatever form that manifests (money, goals, cited research papers, cars sold, rebounds gotten, total stock returns generated, software sales, digital ad sales, etc.).

We should expect that, like America's FAANGM, i.e., Facebook (META), Amazon (AMZN), Apple (AAPL), Netflix (NFLX), Google (GOOG)(GOOGL), and Microsoft (MSFT), there will be a handful of tech platforms that capture and account for the majority of economic value in the energy system that is the SE Asian economy.

And, if one studies the energy system that is the SE Asian economy, they will find that Sea, Grab, and GoTo already operate in something close to a very powerful technology oligopoly.

In some sense, external capital preordained this structure: From Altimeter Capital to Tencent to many different venture capital firms, giant sums of capital have been given to Sea, Grab, and GoTo, with which these firms have exerted immense competitive pressure on smaller startups, creating the oligopolistic positioning that we see today.

As an aside, interestingly, the market understood this quite durably for Sea Ltd., until just about the last 12 months, during which time the market has seemed to experience a noteworthy bout of amnesia. I will say that SE Asia appears to have gone through a tech depression of sorts as well: a dot com bubble burst, if you will, but we will discuss that towards the end of this note.

It's An Oligopoly

In past notes on Grab, I communicated this oligopolistic positioning using the following data and logic:

Potentially The Most Interesting Component Of Grab's Investment Thesis

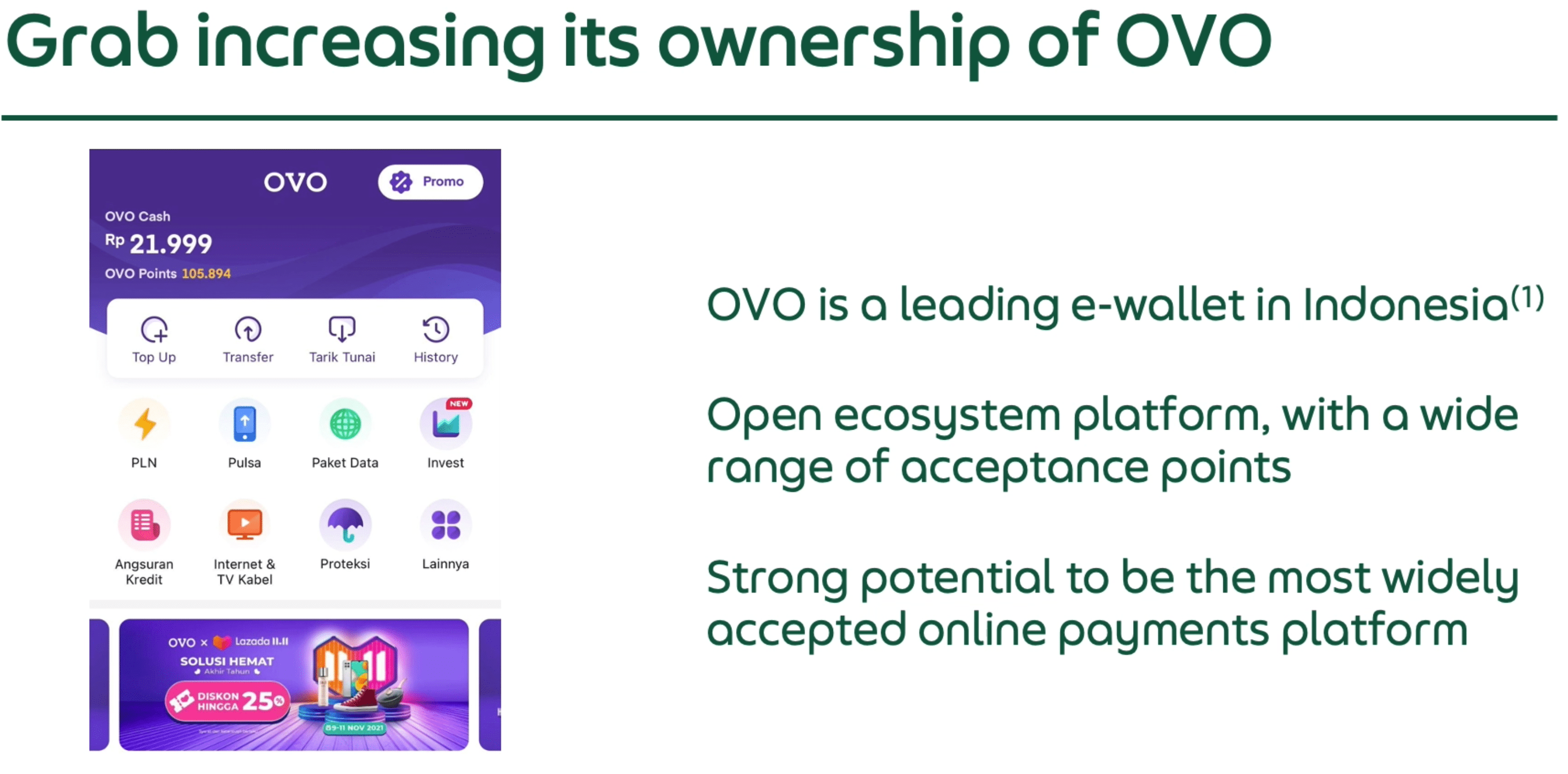

As of a couple months ago , Grab now owns 90% of OVO, which is an incredibly interesting FinTech platform in SE Asia with monopoly market share of mobile wallets in Indonesia. It also, curiously, powers digital commerce for three of the largest e-commerce platforms in SE Asia, i.e., Tokopedia, Lazada, and Bukalapak.

This article explored the OVO asset in saying,

When it comes to Indonesia's digital wallets, Go-Jek's Go-Pay captures many of the headlines. After all, Go-Jek is Indonesia's most prominent unicorn, valued at US$9-10 billion. It's battling Singapore's Grab across Southeast Asia, burning piles of cash as investors rush to join the next round of fundraising. Speculation about a Go-Jek IPO is mounting.

Yet Indonesian consumers prefer a different digital wallet, according to local research firm Snapcart. Data compiled by the Indonesia-based company show that Ovo, backed by Grab and the Lippo Group, is the top Indonesian mobile wallet by a wide margin. Ovo holds a 58% market share, compared to Go-Pay's 23% and Emtek Group and Ant Financial's DANA, a distant third at 6%.

At stake is an enormous potential market: Indonesia has a population of 250 million people, the largest in Southeast Asia and third in Asia overall after China and India. The Asian Banker has found that Indonesia's digital payments reached $3.32 billion transaction value by the end of 2018, up 380% year-on-year and more than double what analysts had forecast. Transaction value could nearly quintuple to $15 billion by 2020.

Analysts say that Indonesian consumers prefer Ovo because it is widely used by retailers, transportation companies, e-commerce platforms and bill payment services, which are among the top applications for digital payments in Indonesia.

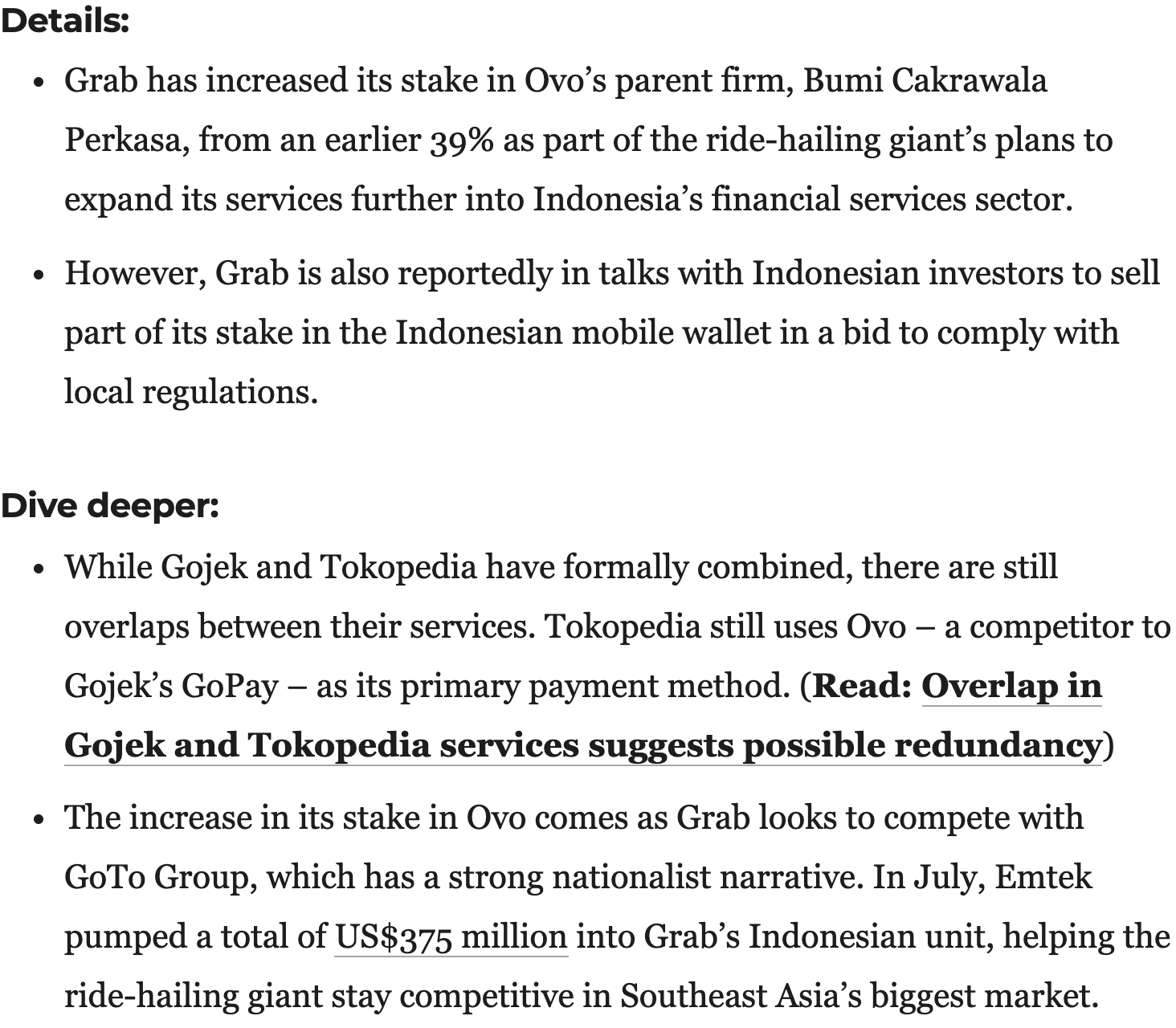

Interestingly, Grab will not acquire OVO, and has instead chosen to own 90%. And this is why we believe Grab has chosen this path:

OVO, Grab, And Gojek

What's interesting is that Grab purchased its OVO stake from Gojek...

Which is allegedly Grab's arch-rival and chief competitor...

With which Grab attempted to merge in 2020 before antitrust concerns in SE Asia effectively halted the merger...

Gojek then decided to merge with Tokopedia...

Which OVO powers from a digital commerce/payments perspective...

And Grab just virtually acquired OVO...

But likely couldn't fully acquire it due to antitrust concerns...

This article summarizes this interesting dynamic well:

From the article,

It all very much feels like these two companies are monopoly platforms with far too much power in the region... And as such, they are simply trying to position themselves such that their unmitigated monopolies are more digestible for regulators.

{kind=link}

{kind=link}

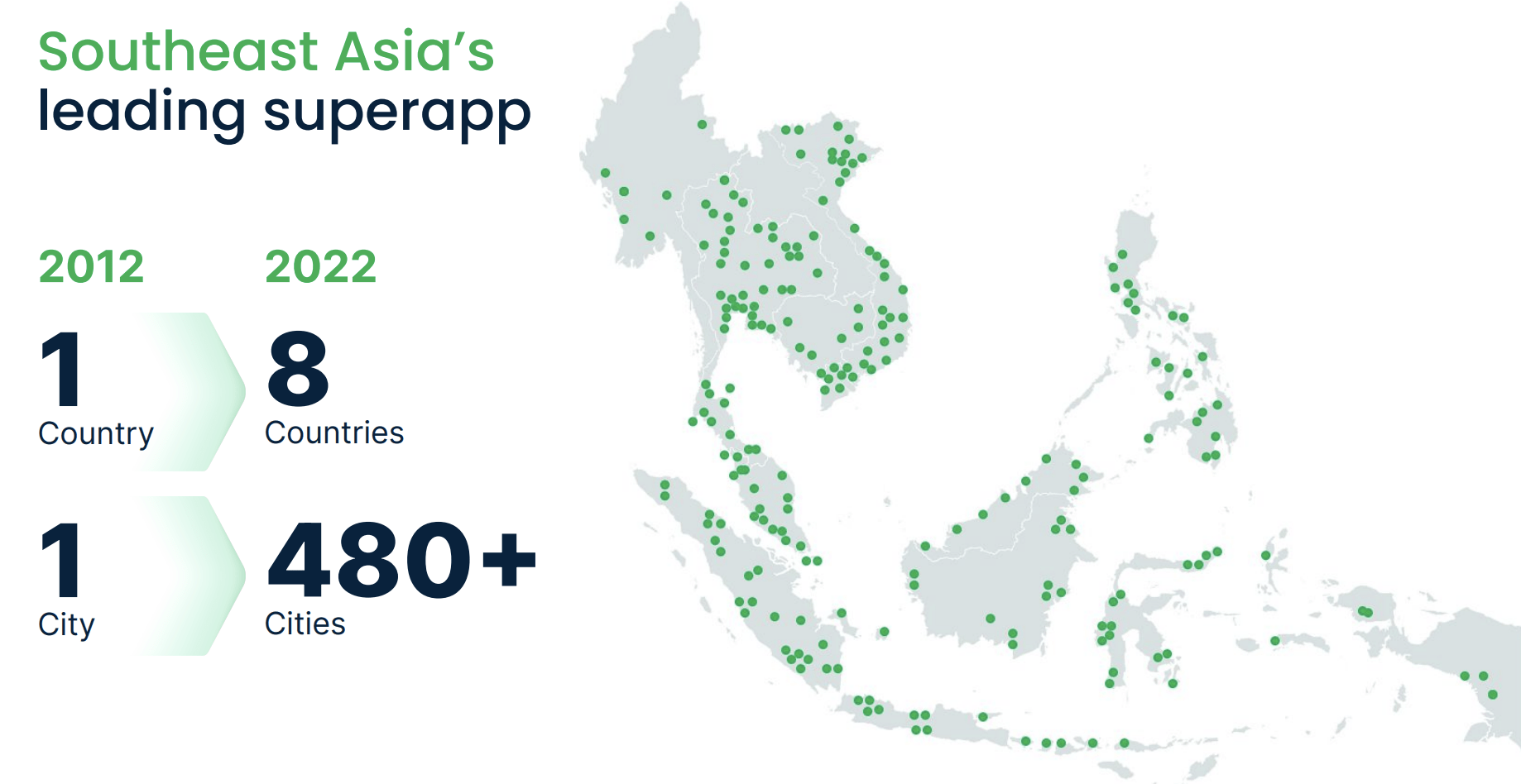

Sea Ltd., Grab, and GoTo Account For 67% Of Mobile Wallet Market Share In Indonesia (270M+ Citizens)

Tech In Asia

GRAB owns 90% of OVO. Sea owns Shopee. GoTo owns GoPay.

GoTo likely had to sell its OVO stake because of its GoTo offering and the antitrust situation that was arising. But the stake was sold to Grab, which, in my eyes, doesn't exactly alleviate antitrust-related market positioning considering how dominant Grab is in the region.

If we think FAANGM is bad in America... SE Asia is basically run by three tech companies at this point.

Sea, Grab, and GoTo represent a fairly scary oligopoly in my view. The market understood this for the last decade or so, but, incredibly, in the span of about 12 months appears to have forgotten this reality.

Later in my most recent deep dive into Grab, I summarized the thesis as follows:

In closing, let's review our Grab investment thesis:

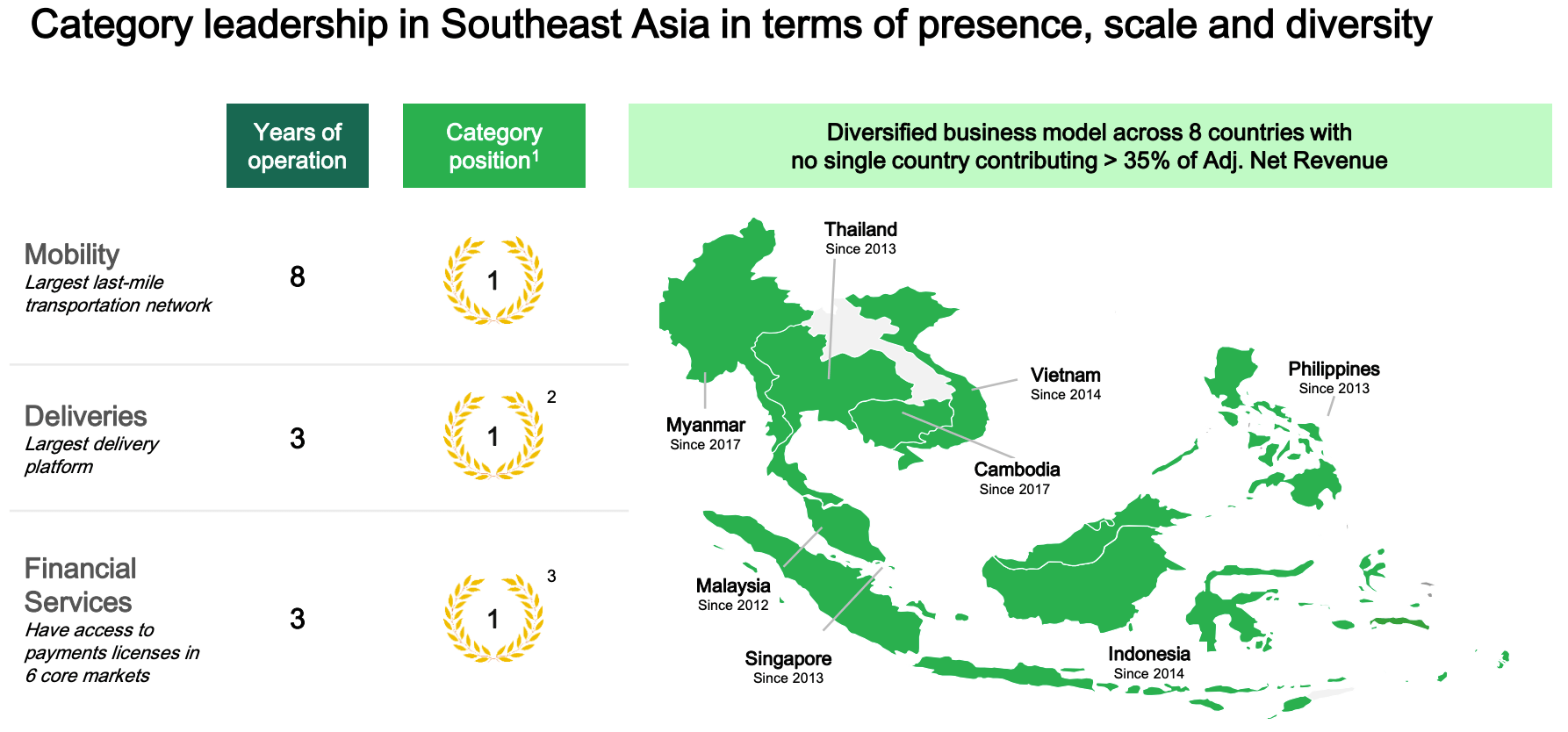

- Grab has monopoly market share of Mobility in SE Asia, where there will be 800M citizens by [2033].

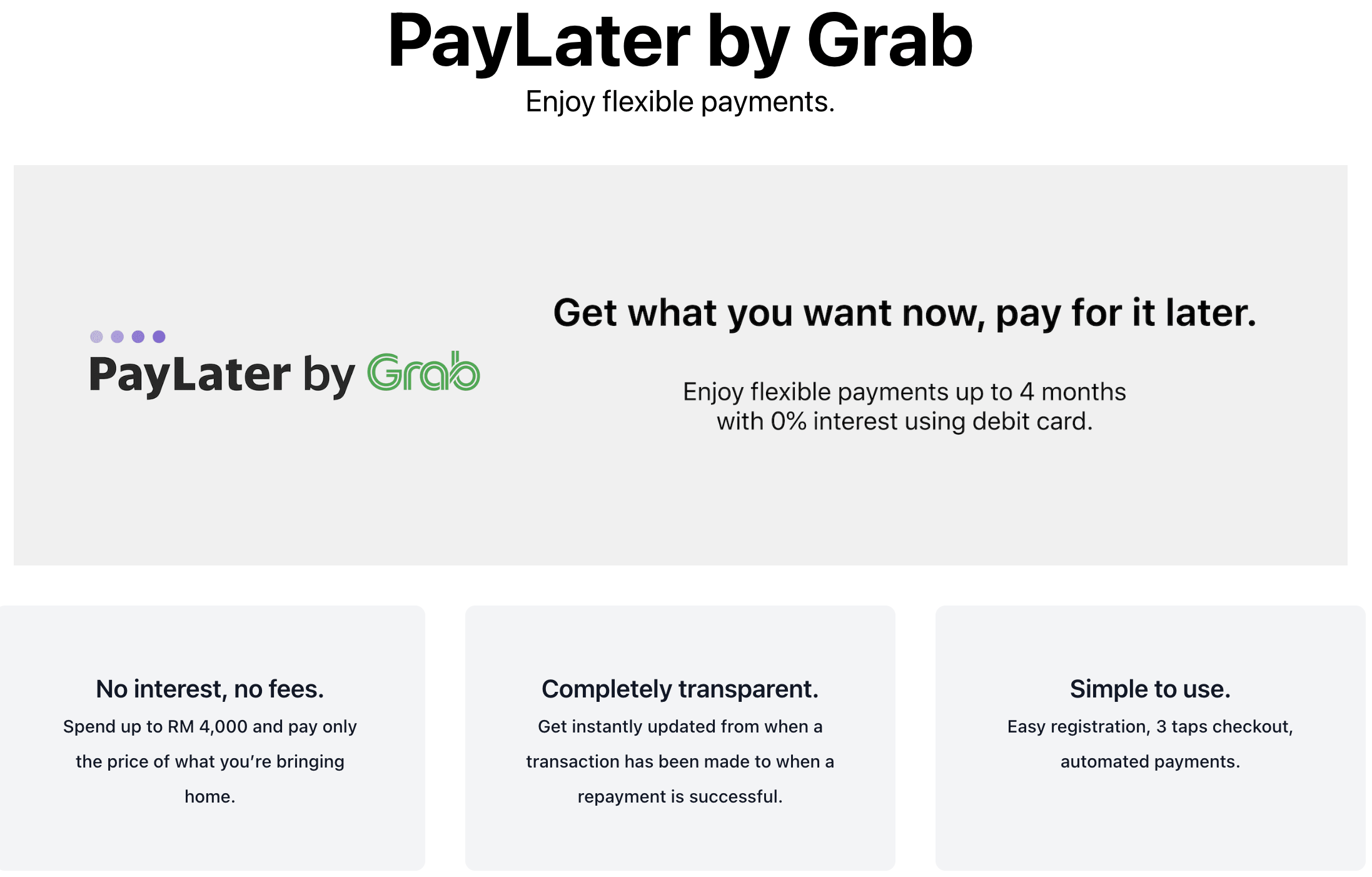

- Grab has monopoly market share for financial services and owns 90% of one of the most important FinTech platforms in the entire region (that powers commerce for the likes of Tokopedia and Lazada, which are two very popular ecommerce websites).

- Grab is not just Uber (and even if it were, it'd still be a pretty good investment!). Grab is Affirm/Afterpay, Square, DoorDash, Lemonade, Instacart, and PayPal bundled into one platform.

{kind=link}

Example of Grab's Diverse Product Offerings (Affirm-Like Product Depicted Below)

{kind=link}

Grab's Super App Driving Network Effects, Margin Expansion, and Customer Loyalty

By now, I hope that I've sufficiently illustrated the idea that Grab operates in, at the very worst, an oligopoly, and, at best, a duopoly, depending on the prism through which you view the business.

This dominant market positioning has served to create pricing power and robust margins for the various segments within Grab's conglomerate. We will review the financials of these segments in a moment.

Before we do that, outside of Grab's market position, which creates the aforementioned pricing power and corresponding robust margins, Grab's segments are uniquely fashioned and combined into a Super App, which creates synergies that drive overall usage of the app.

I believe this is worth noting and reiterating, especially for our U.S. and European folks, as we are not used to this style of business model. We use one app for mobility. We use one app for shopping. We use a few apps for finance. We use a few apps for entertainment.

Grab has successfully created a business model that combines multiple disparate products into one Super App, a description and the value of which you may read below (emphasis added):

Anthony Tan [CEO]: Longer term, we are seeing this multipronged approach across services. So as we evolve the services, whether it's saver deliveries, whether it's car-pooling options, we're seeing it reaches a broader range of users. Then you alluded just now as well paying to the outer city expansion. You're right. Now with more affordable services, we can reach better and we have better product market fit out of city, but how do we do it? As we are driving costs, we're passing that savings on to our consumers.

And then it's not just that, we also looked at increasing our product offerings and lending within the Financial Services segment and that really helps uplift our ecosystem partners.

So all that plus this constant product innovation on affordability and reliability has given us that long growth while even margin expansion is taking place more engagement, more loyalty, as Peter talked about as well.

So we are actually confident. We see still a large time Total Addressable Market. We see tremendous headroom to grow. We see given our power of our ecosystem and scale our platform and a multipronged approach, we're going to grow that user base.

In some sense, especially considering Grab is Uber's SE Asian unit rebranded as Grab, we can call Grab the Uber of SE Asia and look to Uber's current unit economics for guidance as to where Grab's economics will land long term.

But I believe this is insufficient. Grab has created a unique business model entirely. The synergies of its Super App have and will continue to create unique economic profiles for each of its segments and for the conglomerate as a whole. It will also provide a unique platform to launch new product offerings over time, furthering the divergence between Grab and what some, as a heuristic, would like to call its peer in Uber; further solidifying its position within a tech oligopoly in SE Asia.

Turning To Grab's Latest Business Update

Since 2021, two notable developments for Grab have occurred:

- SE Asia as a region has exited lockdowns, which has contributed to the incredible growth Grab has experienced in the last 12 months. The removal of lockdowns lasted into 2022 for SE Asia, and, alongside Grab's reacceleration of growth, we're also seeing the removal of lockdowns in reduced demand for ecommerce, which has created the panic in Sea Ltd.'s shares currently.

- Grab has brought its cash burn to about $0/quarter. Grab still has about $5.6B in total liquidity against about $775M in debt. Grab is profoundly well-capitalized.

In this section, we will briefly explore each of Grab's business segments which collectively make up the aforementioned Super App and its ecosystem.

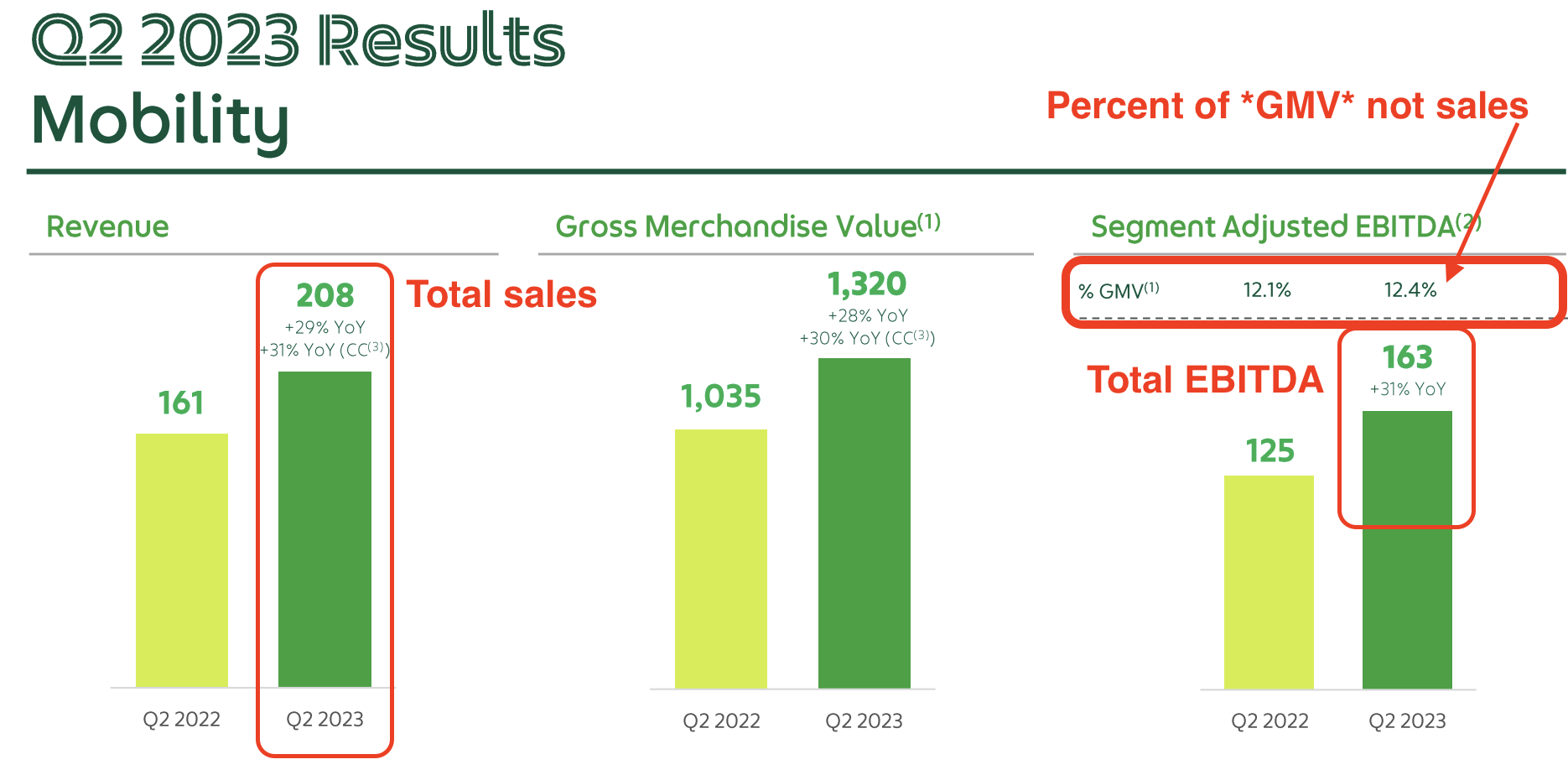

Starting with the "Uber of SE Asia," below, we can see that Grab's mobility segment currently grows at about 30%, with exceptionally healthy EBITDA margins.

{kind=link}

Grab's mobility segment is its core product offering, around which its other offerings have orbited over the years.

Within SE Asia, Grab has captured the majority of mobility market share, with its only real competitor, Gojek, which is now GoTo, holding the remainder.

As the dominant player in a duopoly, the above-illustrated margins, which are exceptional, make sense.

Management has guided for "12% steady-state long term margins as a % of Mobility GMV," and the above chart illustrates that Grab currently operates at about that margin profile.

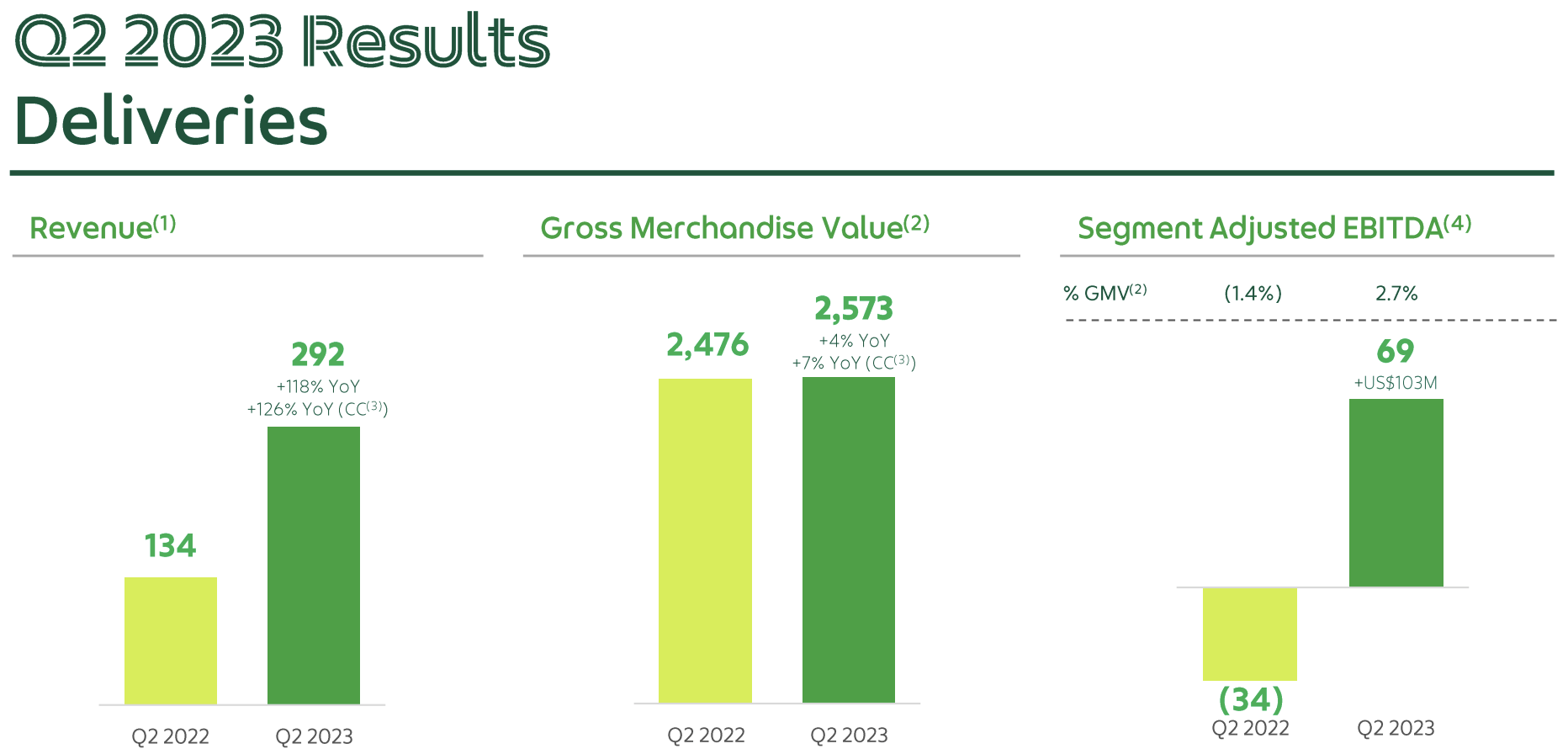

Turning to Deliveries, below, we can see that margins for Deliveries are not remotely as attractive.

{kind=link}

Management has guided to "3% steady-state long term margins as a % of Deliveries GMV," and, as we can see above, we're about there already.

Notably, the margin structure on this segment is far less attractive than the margin structure on the Mobility Segment, where Grab operates in a duopoly with Gojek (GOTO).

And, of course, this makes sense: less competition = greater pricing power = stronger margins.

More competition = less pricing power = weaker margins.

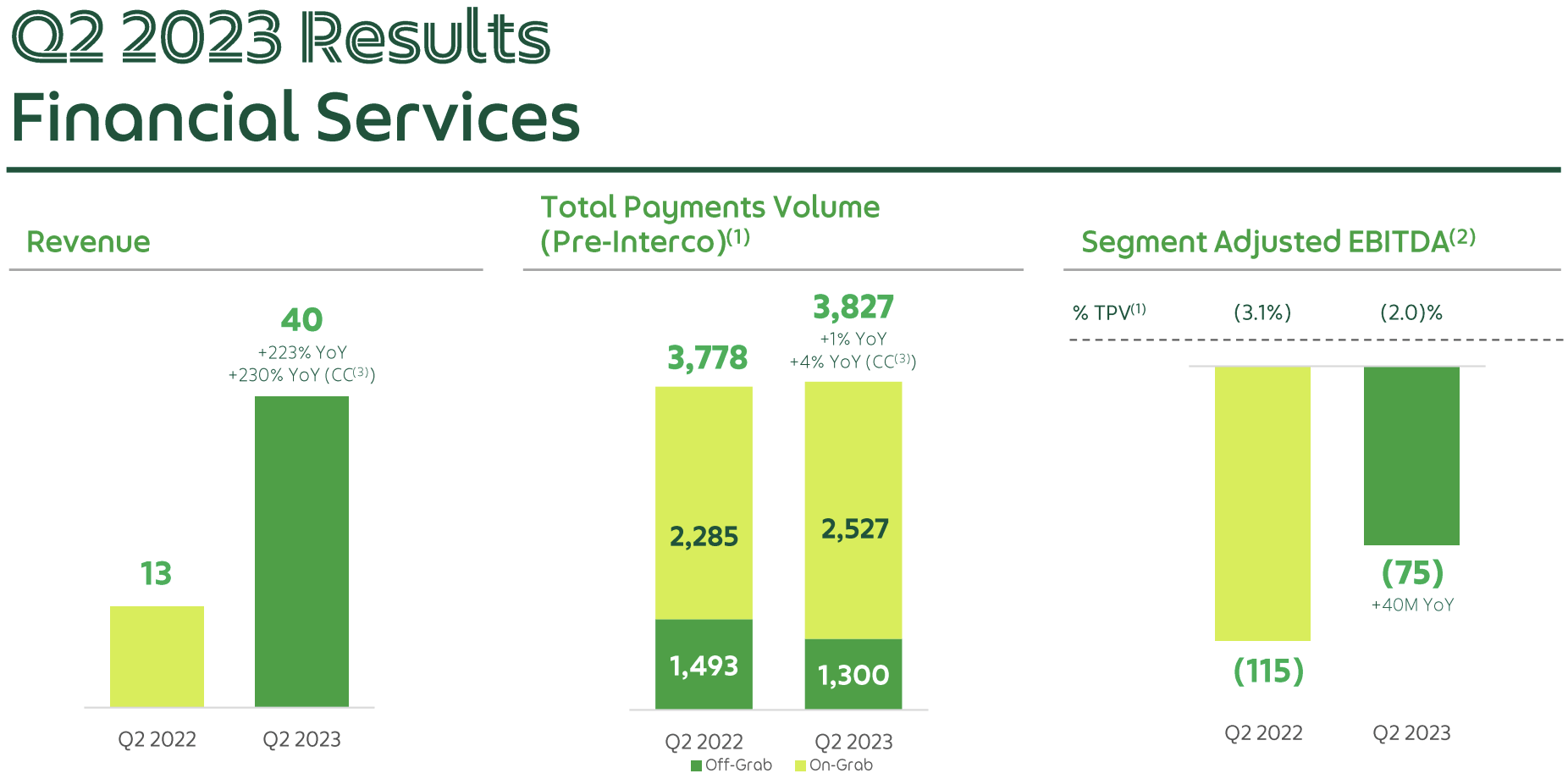

Turning to financial services, this segment of Grab's business is more nascent, and, as such, its margins are not yet profitable, i.e., the business is not generating free cash flow yet.

{kind=link}

But while margins are not yet positive, growth is fantastic about 200%+.

And, in light of SE Asia's still substantial underbanked population, there's very likely a long runway still ahead for this portion of Grab's business.

Grab's Payments TAM Growth

Mordor Intelligence

Digital Ads

As you know well, I have been very focused on investing in unique digital ad companies, e.g., MercadoLibre ( MELI ), Amazon ( AMZN ), and Coupang ( CPNG ).

I believe the growth of digital ads to be one of the "greatest secular growth trends" of our time, and it appears that Grab has fielded a fantastic digital ads platform for both marketers/merchants and consumers.

Below, we can see the growth of Grab's high margin digital ad business.

{kind=link}

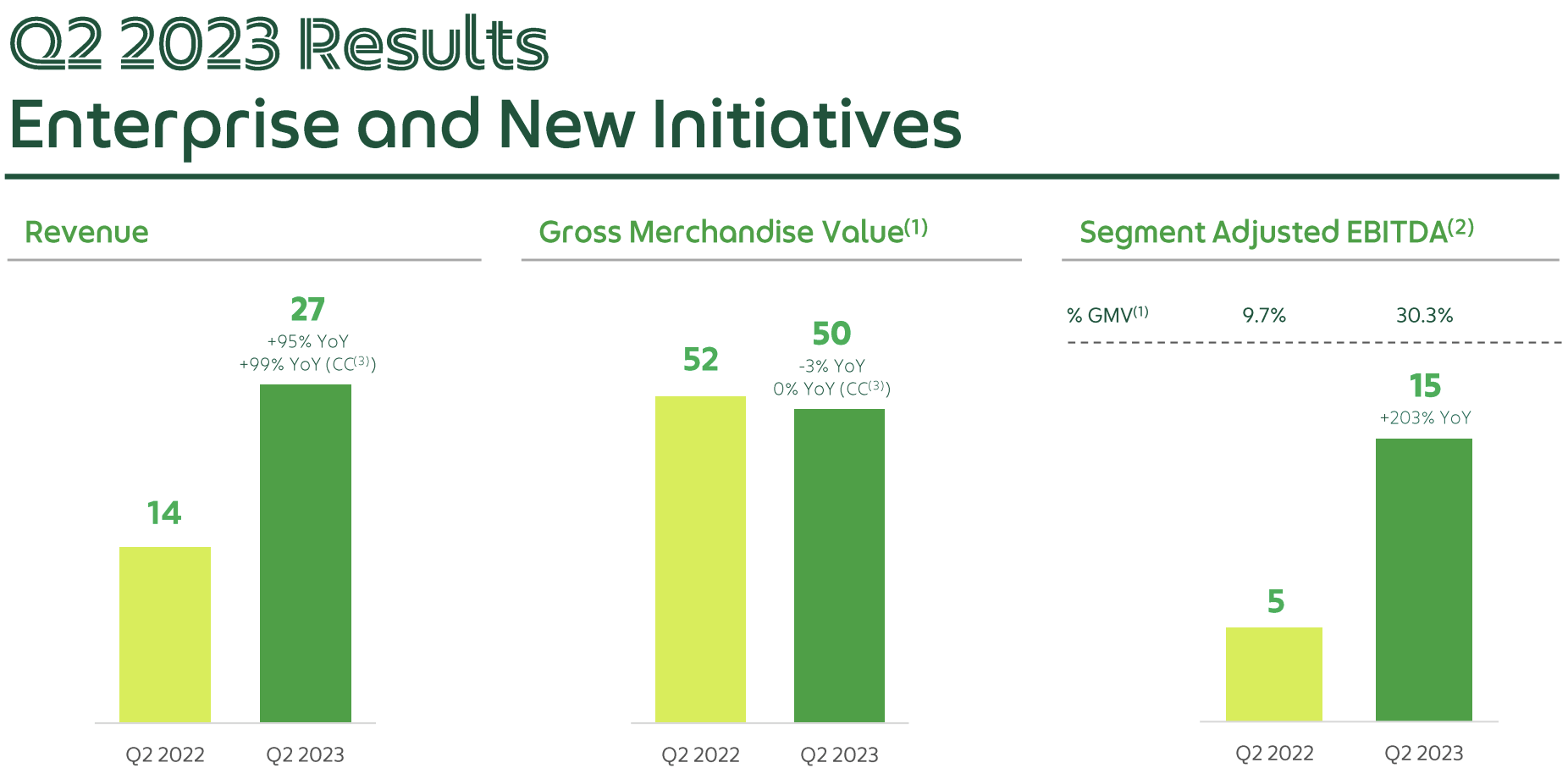

Finally, on our enterprise and new initiatives segment. Year-on-year revenues nearly doubled while segment adjusted EBITDA also tripled.

The strong performance was attributed to advertising underpinned by our efforts to increase advertising penetration among our merchant partners and to improve monetization. So we hit a new milestone in the second quarter with advertising revenues, as Anthony mentioned earlier, comprising around 1% of our deliveries GMV and attaining an annualized revenue run rate of more than $100 million. We remain confident in our advertising services and in driving value uplift for our merchant partners and other top brands.

Alexander Hungate, COO, Q2 2023 Grab Earnings Call.

The company added,

For advertising, we hit a milestone with advertising revenues scaling up to 1% of our deliveries GMV and achieving an annualized revenue run rate of over $100 million. Looking ahead, we will continue to increase ad penetration and improve the monetization of our ads platform.

Anthony Tan, CEO, Q2 2023 Grab Earnings Call.

On the subject of this segment's profitability,

Finally, for enterprise and new initiatives, segment adjusted EBITDA tripled year-on-year with margins expanding to 30.3% in the second quarter from 9.7% in the same period last year. The increase in profitability is mainly attributed to our efforts to improve monetization of our advertising services and to deepen advertising penetration with our active merchant base. For the second quarter, our regional copper costs improved to $192 million as compared to $214 million in the prior year period and $216 million in the prior quarter.

Peter Oey, CFO, Q2 2023 Grab Earnings Call.

Coming back to my comments around Grab as a Super App, we can see, via a study of this high margin segment, that this unique configuration of Grab's business model has afforded it the ability to capture opportunities such as digital ads, leading to a more profitable overall business.

Concluding Thoughts: An Oligopoly & The Bursting Of A Bubble

While reading through Grab's Q2 2023 data, it dawned on me that SE Asia just experienced its own version of the Dot Com Bubble bursting.

Ecommerce Demand Flatlines In Wake Up SE Asian Tech Bubble

Statista

I say that because Sea Ltd. is not the only platform with slowing GMV. Grab's GMV is effectively flat as well.

I don't have GoTo's data, but considering GoTo is a merger of two "second runs" (Shopee > Tokopedia and Grab > Gojek, by a while here), I am incredulous that GoTo is taking the big market share here.

Americans are expecting Nvidia-like performance from these young companies, forgetting what it was like for America when digital industrialization was just picking up in the early 2000s (lots of pullback in usage during that period).

Funding Of Asia Startups Collapses, Alleviating Downward Pressure On Margins For Sea Ltd. and Grab

{kind=link}

I believe we will emerge from this recessionary period for SE Asia's tech economy, and both Sea and Grab will materially accelerate growth in the years and decades ahead.

Thank you for reading, and have a great day.

For further details see:

Grab Holdings: SE Asia's FANG Has Formed