GRAB - Grab Q4 Results: Remains Highly Speculative But Is Getting Closer To Profitability

Summary

- Grab has been focusing on improving profitability by reducing partner and consumer incentives, which has helped improve its adjusted EBITDA margin, but resulted in slower growth in Gross Merchandise Value.

- The company has significant liquidity, including billions in cash and short-term investments, which gives it a decent chance of being able to fund losses without having to raise additional capital.

- Valuing Grab is difficult, but we make a few comparisons to show that the current price appears reasonable. Still, we continue to believe that shares are highly speculative.

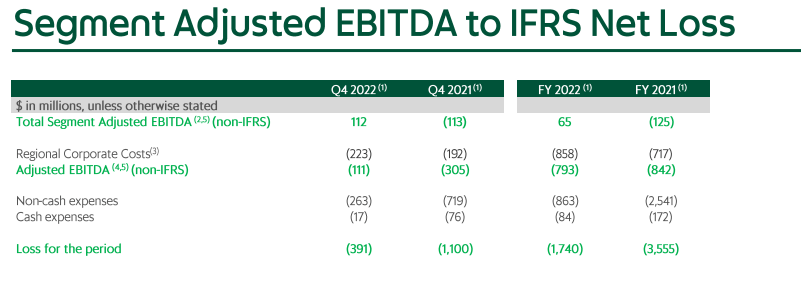

As a leading "Super App" in South East Asia, Grab (GRAB) is a very promising company. The problem with the company has been the significant losses it has incurred to capture as much of the market as possible. In recent quarters, however, the company has been paying more attention to profitability and has made significant improvements to its profit margins, even if it continues to lose money. In Q4 2022 the company reduced partner incentives by ~20% y/y and consumer incentives by ~35% y/y, which clearly helped improve the adjusted EBITDA margin. As can be seen below, it made a 454 bps improvement, which is very significant, but still not enough to make the company profitable. The downside of the increased focus on improving profitability has been slower growth in Gross Merchandise Value (GMV), which grew only ~11% y/y in Q4, or ~20% in constant currency. This was a deceleration compared to the ~24% y/y growth in GMV during FY2022, or ~30% in constant currency. Still, we believe the company is right in focusing on improving its profitability, even if has to slow down growth to do so.

Grab Investor Presentation

Financials

One of the big expenses for Grab is its significant stock-based compensation. This is one of the main components of its non-cash expenses. While it is great to incentivize employees with shares, we believe the company has to moderate the amount it gives out in the future.

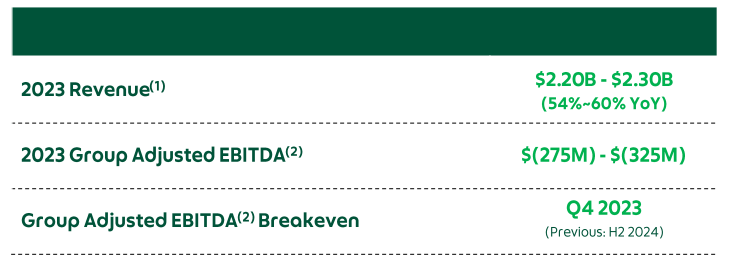

For example, in Q4 adjusted EBITDA was a loss of $111 million, but the real loss for the period, when including the non-cash expenses and some other minor cash expenses, was actually $391 million. Still, even looking at the total loss for the period, we see a significant improvement compared to Q4 of the previous year. The company is moving in the right direction, but still has significant distance to cover. One of the pieces of good news that the company shared with the Q4 results release was that it now expects to reach Group Adjusted EBITDA breakeven by Q4 2023, sooner compared to its previous guidance of second half 2024. Investors should be aware that the company is not talking about IFRS profitability, and that one is probably much further away.

{kind=link}

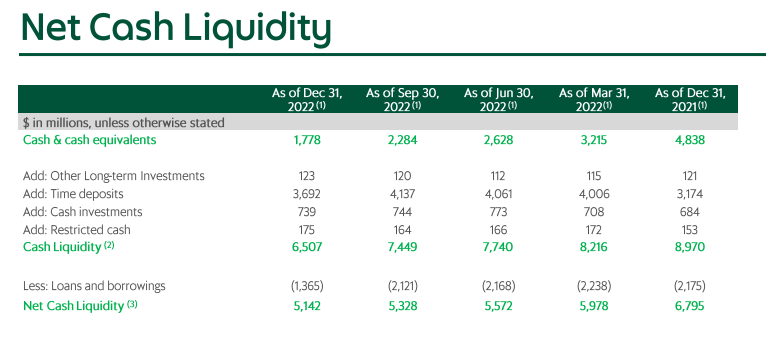

The good news for Grab investors is that the company continues to have significant liquidity, including billions in cash and short-term investments. That means that it has a decent chance of being able to fund losses without having to raise additional capital, if it continues on its current path to profitability and meets its Q4 2023 group adjusted EBITDA breakeven target. The company had a net cash position at the end of the year of ~$5.1 billion.

{kind=link}

Guidance

Another reason for optimism is the positive guidance that the company provided. As Seeking Alpha reported , revenue guidance for 2023 is meaningfully above analyst estimates, and the estimated Group Adjusted EBITDA loss is much lower than what analysts were expecting on average. Importantly, Grab can continue to be considered a high-growth company with revenue growing at 50%+. Given the valuation premium at which it is trading compared to Uber ( UBER ), high revenue growth is necessary to justify the current stock price.

{kind=link}

Valuation

As we've mentioned in previous articles, valuing Grab is quite hard given that it is not yet profitable, and that there is a lot of uncertainty as to its future revenue growth rates and profit margins. That said, we can make some useful comparisons to get an idea of whether the current valuation is reasonable.

Grab is currently trading with an enterprise value of ~$9 billion, and it current gross merchandise value reached a run-rate in Q4 of ~$20 billion. Its EV to GMV is therefore ~0.45x, and it is not rare for platform companies to trade at ~1x GMV once they are profitable. To deserve a 1x multiple of GMV, however, we believe Grab would have to prove they can be sustainably profitable and maintain a healthy growth rate.

Another interesting comparison is with Uber, which is trading with a forward EV/Revenues multiple of ~2x, while Grab is at ~4.7x. One of the reasons for the big difference is that Uber is expected to grow revenue in 2023 by ~15%, while Grab is expected to grow almost 4x faster.

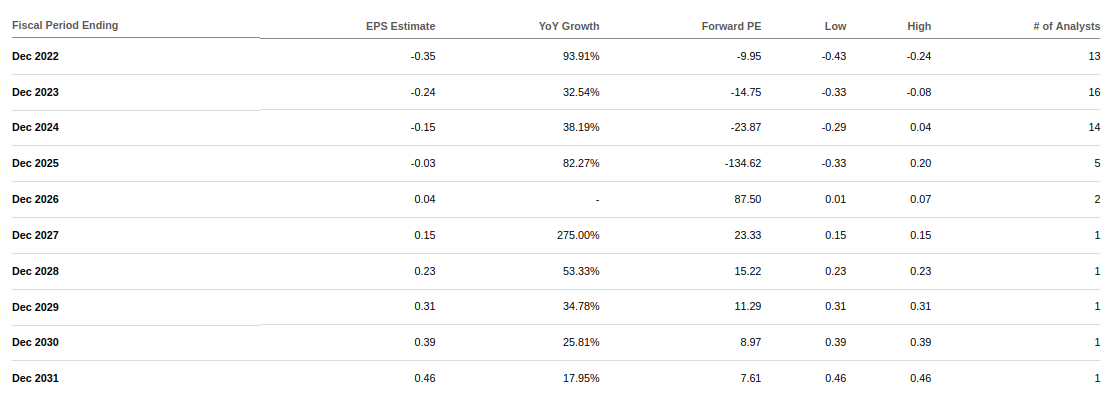

Looking at analyst earnings estimates, they turn positive until FY2026. We believe, however, that given the strong guidance by the company analysts will probably adjust their models and bring breakeven forward.

{kind=link}

Risks

After reviewing Grab's Q4 and full year 2022 results, we continue to believe shares remain highly speculative. Overall we see results as positive, with the company providing strong guidance, and showing good progress on its path to profitability. The big risk for investors is that the company continues generating very significant losses, and that there is no guarantee that their current financial resources will be sufficient to give the company enough runway to become profitable.

Conclusion

While Grab has made significant improvements to its profit margins, and is on track to reach Group Adjusted EBITDA breakeven by Q4 2023, the company still has a long way to go before achieving sustainable profitability. The increased focus on profitability has resulted in slower growth in GMV, which may impact Grab's valuation. However, the company's positive revenue guidance for 2023 and significant liquidity position are reasons for optimism.

For further details see:

Grab Q4 Results: Remains Highly Speculative, But Is Getting Closer To Profitability