CA - Gran Tierra Energy: Too Many Red Flags To Be Bullish

2023-08-17 00:48:37 ET

Summary

- Oil and gas microcaps offer great investment opportunities due to their low valuations and lack of institutional interest, but there are simply better companies than Gran Tierra Energy.

- GTE has major red flags, such as jurisdiction risk and a capital allocation dilemma.

- The Colombian government has already banned fracking and is looking to further restrict the industry.

- Colombia has a windfall profits tax on oil and gas companies which brought the company's effective tax rate to 140% for a period of time.

- Gran Tierra Energy has high CAPEX to maintain production and a large debt burden.

As an investor who likes to buy dollars for pennies, oil and gas microcaps are a great place to stock pick, as bear markets in both 2016 and 2020 beat the sector down to the point where very few institutions invest or lend in it, and due to its past lacklustre performance valuations are some of the cheapest in the market with stocks regularly going for less than 2x earnings and I've even seen some trade for less than 1x forward earnings.

As with any market that has a lot of value stocks, there are also value traps and companies that trade cheaply but might trade even cheaper due to the idiosyncratic risks.

In the case of Gran Tierra Energy ( GTE ), even though the valuation from the outset looks cheap with a low P/E and low P/B, there are many red flags I see which would stop me from buying this company when there are others in the same industry going at similar valuations without as many red flags.

Last Quarter's Earnings Report

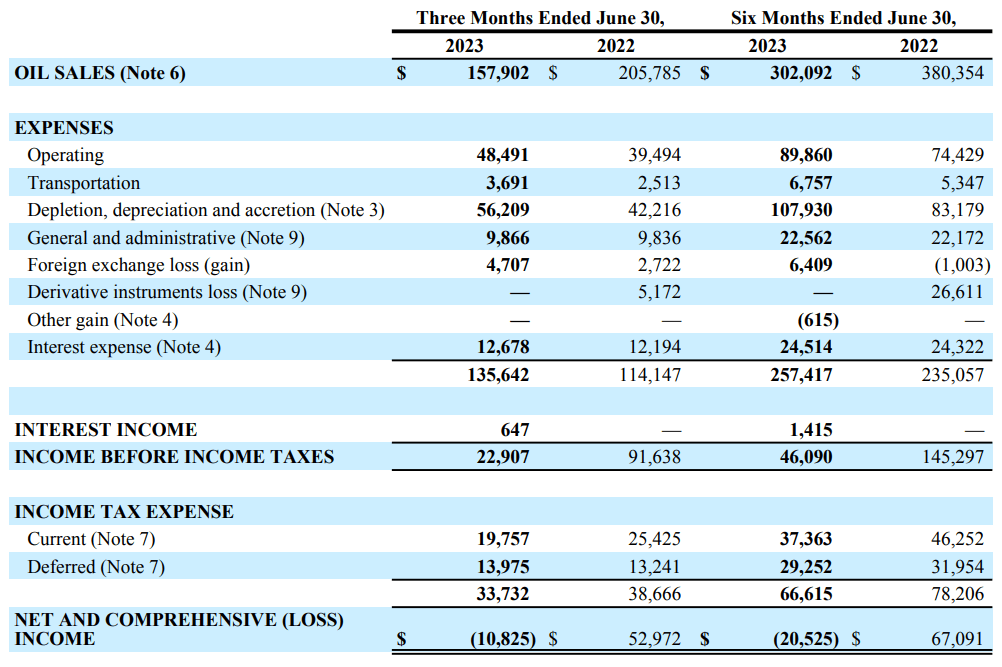

The stock initially dropped after the earnings report due to Q2 being an unprofitable quarter. Below is an overview of the financials:

{kind=link}

As can be seen, sales are down and expenses are up compared to the year prior; most importantly, the company now has negative net income.

I'll break down the multiple reasons why earnings are lower and what risks it entails.

Unpredictable Jurisdiction

Gran Tierra Energy operates out of Colombia. While I have nothing against emerging markets and in fact I'm bullish on many companies in emerging markets, Colombia does present some major risks for private-sector energy companies.

First off, when looking at last quarter's financials the "income before income tax" is $22.907mm while the "net and comprehensive (loss) income" is -$10.825mm. As a general rule of thumb, a company shouldn't be paying more in taxes than it made in EBT. In this case, some of the taxes are deferred taxes, but even if we only use current taxes the effective tax rate is around 86%.

Colombia has very high taxes (35% corporate tax) and as of November 2022 Colombia has instituted a windfall profits tax on oil and gas companies; Reuters the tax as the following:

The new law states that oil companies will be taxed an additional 5% when international prices are between $67.3 and $75 per barrel. That then becomes an additional 10% when prices are between $75 and $82.2 per barrel and then 15% if they climb any higher.

This could essentially tax the company at 50% per year. Even this explanation doesn't take into account why the company is paying a current tax of 86% and a current + differed tax rate of more than the EBT.

When looking through the most recent 10-Q for the company they have the following explanation:

The Company's effective tax rate was 145% for the six months ended June 30, 2023, compared to 54% in the comparative period of 2022. Current income tax expense was $37.4 million for the six months ended June 30, 2023, compared to $46.3 million in the corresponding period of 2022, primarily due to a decrease in taxable income.

The deferred income tax expense for the six months ended June 30, 2023, was $29.3 million primarily as a result of tax depreciation being higher than accounting depreciation and the use of tax losses to offset taxable income in Colombia.

The deferred income tax expense in the comparative period of 2022 was $32.0 million as the result of tax depreciation being higher compared to accounting depreciation in Colombia. For the six months ended June 30, 2023, the difference between the effective tax rate of 145% and the 50% Colombian tax rate was primarily due to an increase in non-deductible foreign exchange adjustments, the impact of foreign taxes, non-deductible royalties in Colombia and non-deductible stock-based compensation. These were partially offset by a decrease in valuation allowance.

For the six months ended June 30, 2022, the difference between the effective tax rate of 54% and the 35% Colombian tax rate was primarily due to an increase in the impact of foreign taxes, foreign translation adjustments, increase in the valuation allowance, non-deductible third-party royalties in Colombia and non-deductible stock-based compensation.

While the company did provide an explanation here it actually makes the tax situation look worse. A lot of expenses that would be deductible in the U.S. or Canada aren't in Colombia, such as royalties, foreign taxes (which a company based in the U.S. or Canada directly selling its production within the same jurisdiction wouldn't have to pay), FX exchange adjustments etc. While I'm no expert on Colombian taxes, some base-level research shows that Colombian corporate taxes are extremely high and unpredictable in comparison to U.S. and Canadian taxes; on top of that, a company like Gran Tierra Energy has to deal with multiple jurisdictions complicating this further.

One of the key rules of investing is to not invest in what you don't know. Most Western investors including myself are scratching our heads in confusion when it comes to the taxes for this company. Even if the tax situation is completely legitimate I wouldn't invest in this company unless I had a good idea of how Colombia taxes energy companies. Also, there are few resources here to help investors; unlike in the U.S. where most equity research firms will have a corporate tax expert on the team who can distil the information for investors, here investors are largely left on their own to fill in the gaps.

On top of the tax issues here, there are other jurisdiction-specific risks. The biggest risk is that the Colombian president wants to phase out fossil fuels by stopping all new production and the government has already put a moratorium on fracking :

Petro has also made it clear (Spanish) that hydraulic fracturing, known as fracking, and the exploitation of unconventional hydrocarbon deposits will not be permitted in Colombia. Colombia's highest administrative tribunal, the State Council, has already placed a moratorium on fracking , although pilot projects are allowed.

Essentially the goal of the government is to allow current producing reserves to still produce but reserves that are undeveloped wouldn't be developed.

Positive: Reserves Are High

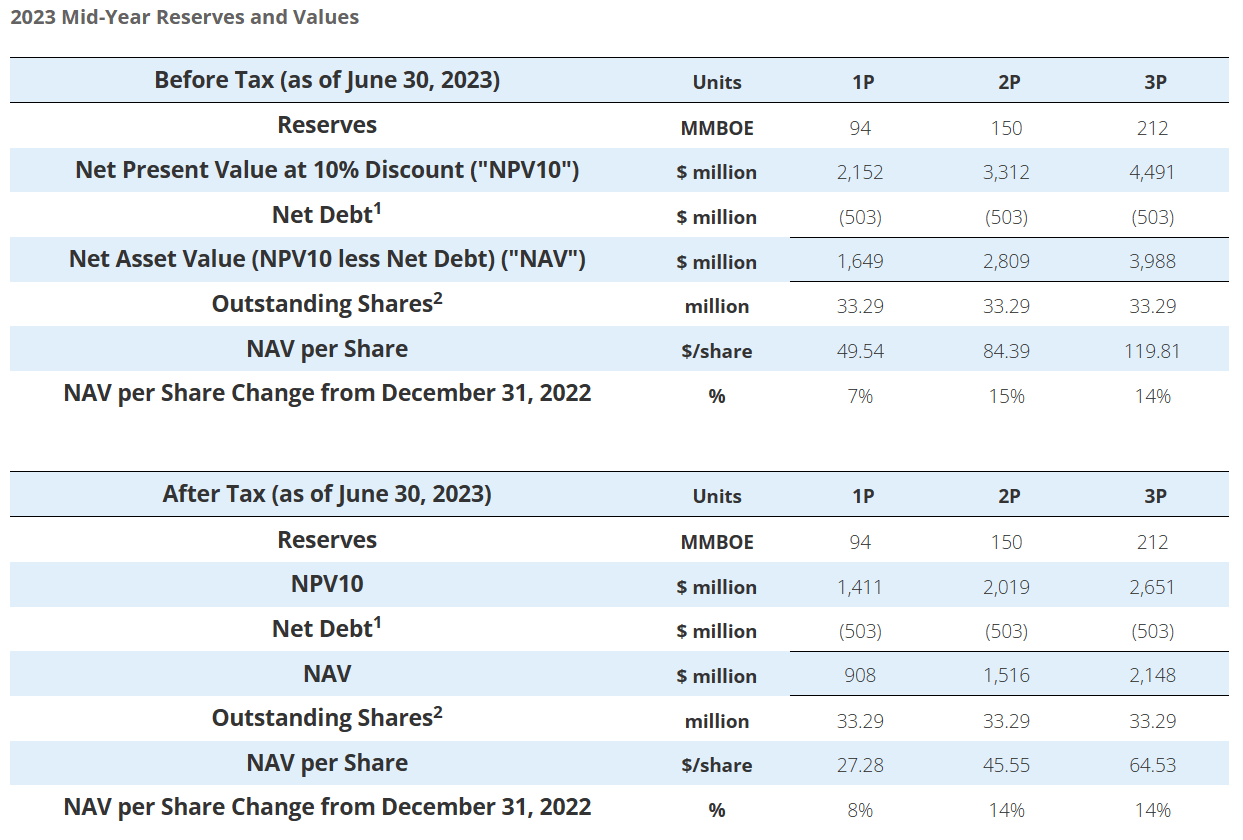

On the flip side, the reserve runway is long. Below is an overview of current reserves:

{kind=link}

As can be seen, the P1 reserves are 94 million. The company is currently producing BOPD of 27,204 which annualized is 9,936,261 BOE per year. This means that current P1 reserves offer a 9-year runway in reserves. The management looks to do more drilling to increase this, although I'll discuss later on why this capital allocation strategy could be problematic.

The Debt Is A Major Issue

Gran Tierra's debt level is very high compared to its profitability and if it doesn't quickly pay off its debt it will have to refinance at a far higher rate.

We can build out our own P&L and see how a higher interest rate would impact the bottom line.

The BOPD is around 30000 . If we take out a royalty of 25% then we're left with 22,500 barrels. Multiplying that by the price of Brent crude (roughly averages $80 on the strip for the next two years) *365.25 leaves us with a netback of $657,450,000.

Annual general and administrative expenses are very stable at around $42mm per year.

Depreciation and amortization have gone up as the company has expanded its production; last quarter it was at $66.1mm, which is $264.4 annualized. This would make for total operating expenses of $306.4mm per year. This makes for an EBIT of $351,050,000.

Now we come to the challenging part which is interest and taxes.

Gran Tierra was able to issue USD-denominated bonds for 6.25 % and 7.75 % back in 2018 and 2019. This was when the Fed Funds rate was around 1.5-2%.

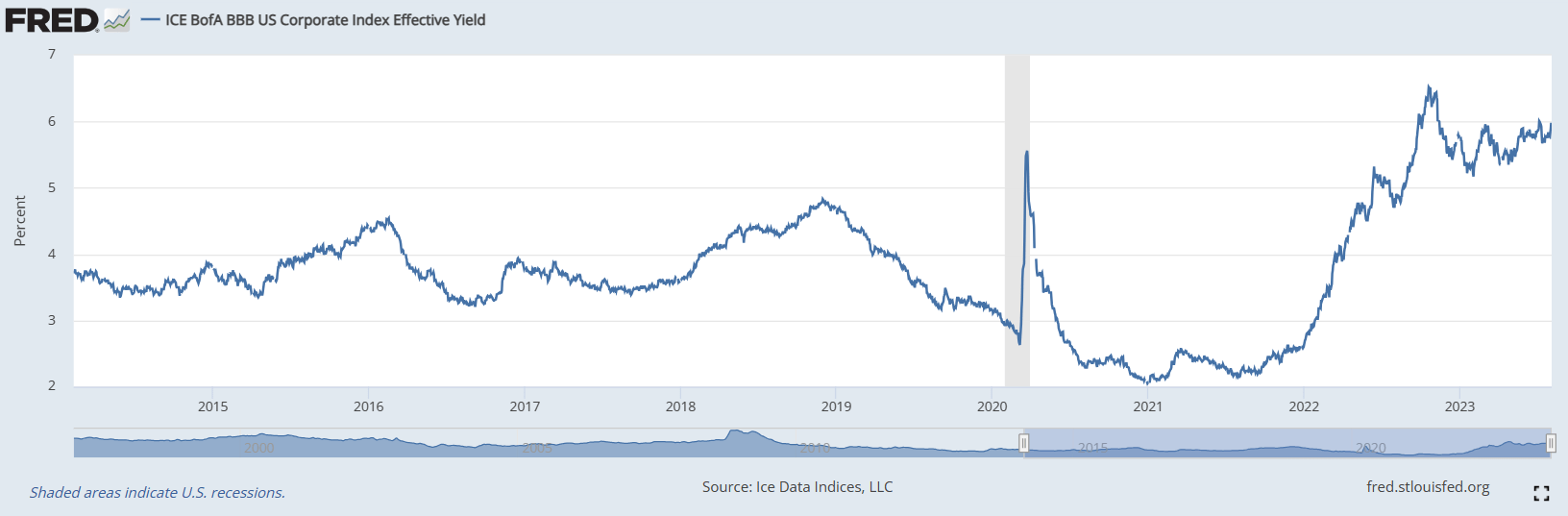

Below is a chart of the ICE BofA BBB Corporate bond index yield:

{kind=link}

As can be seen during 2018 and 2019 corporate borrowing rates were lower than they are now. The only time that rates spiked was in Q4 2018 and Q1 2019 when the Fed raised rates and then pivoted in Q2 2019.

Now that rates are higher and credit spreads have widened, the rate at which Gran Tierra will refinance will have to be a lot higher.

The US 5-year was around 2% when Gran Tierra originally issued the bonds and BBB grade bonds at around 3.5%. Gran Tierra issued at an average of 7%. This makes for a credit spread of 1.5% between risk-free and BBB and 3.5% between BBB and Gran Tierra's rate. Currently, the US 5-year is at 4% with BBB slightly above 6%, so the credit spread between risk-free and BBB has widened slightly. If we were to apply the same basis point spread on the BBB then Gran Tierra's new rate would be 9.5%.

But in reality, the rate would be far higher than this. First off, when the Fed does a rate hiking cycle it always widens the credit spread with lower-quality credit the most. So the spread between BBB and Gran Tierra Energy's effective rate would have widened a lot since 2018 and 2019. Secondly, after energy prices crashed in 2020 many creditors permanently left the space and ESG concerns have increased over the last couple of years. This means the yield will likely need to be even higher.

The current Gran Tierra Bonds are rated as B by Fitch . Since any new bond issuances would have a far higher interest rate making for higher risk, we could presume that rating agencies would rate it lower than B, likely at CCC.

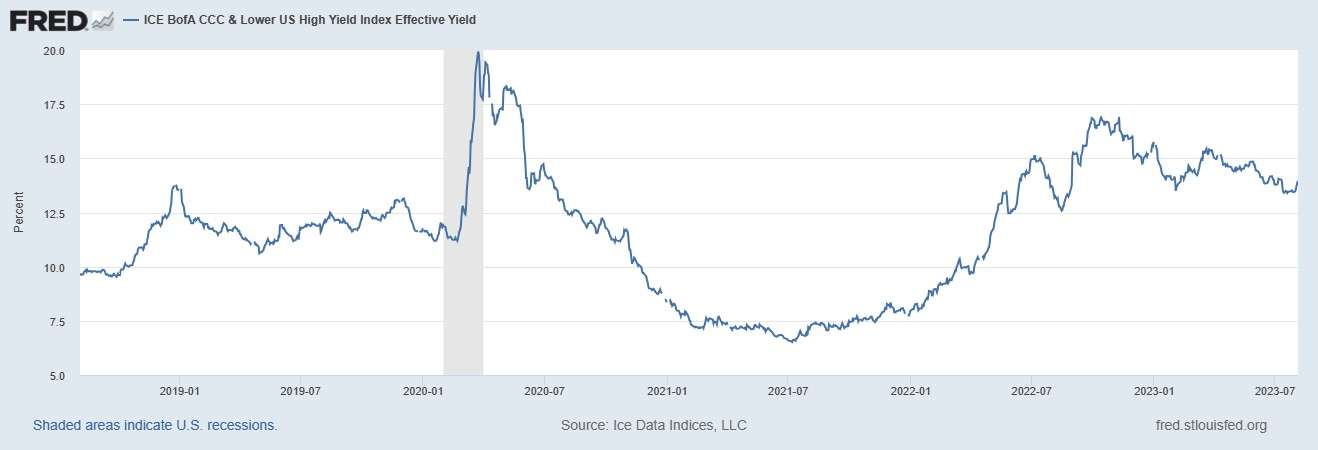

Below is the ICE BofA CCC Corporate Bond Index Yield:

{kind=link}

As can be seen, CCC bonds are currently yielding 14%, and just a couple of months back were yielding around 17%.

A 14% rate on $566.1mm of debt is $79.254mm per year in interest expense. This makes for $271.796mm in pre-tax earnings.

At the 50% tax rate we discussed earlier, the after-tax earnings would be $135.898mm. With the current market cap that is a 1.67x earnings.

While that might sound cheap we have to take two things into account. The first of which is that we used a very bullish scenario here in regard to how much production the company will have, oil prices, and the uncertainty around the company's taxes. The other is that the whole micro-cap E&P space is dirt cheap and I will often find TXS-listed companies going for the same or lower multiple without the high leverage and emerging market issues that this company faces.

The above example is of course the optimistic view. If we were to change just two of the variables, oil price and BOPD, then the earnings would be vastly different.

Let's plug in $60 Brent, which is possible seeing as though we had $70 Brent just two months ago, and let's reduce production down to 25,000 BOPD, which is a realistic scenario if the company had to stop future CAPEX (which keeps the production high) to pay down debt.

Revenue: $547,875,000

Netback: $410,906,250

EBIT: $104,506,250

EBT: $25,252,250

Earnings: $12,626,125

As can be seen, a slightly lower oil price and a lower amount of production brings the company close to breakeven earnings, so the risk is extremely high in just a minor downturn.

Capital Allocation Dilemma

My view is that there's a major capital allocation issue with Gran Tierra Energy.

The company is currently using retained earnings for the following:

1: CAPEX to raise production

2: Share Repurchase

3: Bond Repurchase

As we reviewed prior the company has a lot of debt and it would be prudent to buy back bonds before the company has to refinance at higher rates. The issue with this is that if the company focuses purely on debt buybacks then it wouldn't be putting anything toward CAPEX which is a necessity to keep production high; if no CAPEX happens then production will quickly decline which causes an issue of collapsing revenue; as I highlighted in the last section using the example of 25k BOPD instead of 30k BOPD, a small downturn in production quickly brings the company's earnings yield from very high level to around breakeven.

Based on the projections we did earlier, the company will do around $135mm in earnings at $80 Brent and 30k BOPD. Current long-term debt is $561.1mm. That is a debt to earnings of 4.156x, meaning that if every penny of earnings was put into paying off debt then it would take 4.156 years to pay off the debt. While this is bad enough, keep in mind that earnings would go down as there is no CAPEX to keep production up.

The company could put operating cash flows towards CAPEX, but then little would be left to pay down debt. Here's what the 2023 guidance said about CAPEX relative to operating cashflows:

2023 Capital Expenditure Budget of $210-250 Million, Expected 2023 Cash Flow 1 of $270-320 Million in Base Case

Above it shows that around two-thirds of operating cashflows are used in CAPEX. This means that there is very little left over to pay down debt.

In fact, there's actually a negative amount left over because of how taxes are calculated. If operating cash flows are $295mm and CAPEX is $230mm then FCF before taxes is $65mm.

If CAPEX of $230mm is straight-line depreciated over 5 years, then that is $46mm in yearly depreciation.

$295mm (operating cash flows)-$46mm (depreciation) = $249 (EBIT).

This makes for earnings before taxes of $209mm as there's about 40mm of interest expense based on an average interest rate of 7% on $561mm of debt.

Since taxes are 50%, that makes for $104.5mm in taxes. Since FCF before taxes is only $65mm, this actually makes for a negative FCF after taxes.

*Keep in mind that this is rough back-of-the-envelope math, but it does a great job of highlighting that the company is between a rock and a hard place where it can either spend on CAPEX or pay down debt, but it is hard to do both.

Key Takeaways

The crux of this write-up on Gran Tierra Energy is that there are simply better E&P companies to invest in which don't have the same risks but are still going at low valuations.

To sum it up, below are the key risks we discussed:

The first key risk is from the jurisdiction itself. Colombian taxes are already high and the windfall profits tax makes it even higher. On top of that the current administration brings a lot of risk to the industry as a whole.

The second major risk is the high debt burden. If Gran Tierra doesn't focus on paying down debt then it will be refinanced at a significantly higher rate. At the same time, the company is facing a capital allocation dilemma whereby it has to either buy back debt or do CAPEX, but it would be hard for it to do both, even though both are major necessities.

Since I mentioned that are better E&P companies to invest in, the following is a list of E&P companies which are going at incredibly low valuations yet don't have the risks that Gran Tierra has:

Journey Energy ( JOY:CA )

Vital Energy ( VTLE )

Callon Petroleum Company ( CPE )

SilverBow Resources ( SBOW )

Southwestern Energy ( SWN )

SM Energy Company ( SM )

Vermilion Energy ( VET )

SandRidge Energy ( SD )

Petrobras ( PBR )

Antero Resources ( AR )

Saturn Oil & Gas ( SOIL:CA )

I would like to note that the above list is a quick pick of stocks that I believe are better value for money than Gran Tierra, but in no way does it constitute a buy recommendation; the list is simply made up of other companies I would look into as alternatives if you're interested in investing in companies like Gran Tierra without the same risks.

For further details see:

Gran Tierra Energy: Too Many Red Flags To Be Bullish