GPP - Green Plains: Agreement With Shell Affiliate Could Ignite The Price

2023-09-14 07:32:54 ET

Summary

- Green Plains Partners signed a technological collaboration with a large oil and gas corporation, potentially enhancing stock demand.

- The global decarbonization market is expected to grow at a double-digit rate, which could benefit Green Plains' decarbonization strategy.

- Ultra-high protein production and lower dependence on the largest shareholder could lead to net sales growth and increase the company's valuation.

Green Plains Partners LP ( GPP ) recently signed a contract with a company associated with a large oil and gas operator, offering stable FCFs and a decarbonization strategy. I believe that the largest risks come from relying heavily on business agreements with the parent company. With that, the current valuation does not seem to be fair at all with the performance of GPP. Successful development of ultra-high protein production, acquisition of new business interests, and lower dependence on the largest shareholder could enhance the stock price.

Green Plains Partners Signed A Technological Collaboration with A Massive Oil And Gas Corporation

Green Plains Partners is a master limited partnership engaged in providing fuel storage and transportation services. It was formed by its parent company, Green Plains Inc. (GPRE), in March 2015, and it completed its initial public offering in July of the same year.

Green Plains Partners specializes in the ownership, operation, development, and acquisition of ethanol and fuel storage facilities, terminals, transportation assets, and other related assets. Its primary objective is to support the marketing and distribution activities of Green Plains, a vertically integrated ethanol producer.

{kind=link}

{kind=link}

Green Plains Partners' business model is based on tariff-based commercial agreements with Green Plains Trade to provide services for the receipt, storage, transfer, and transportation of ethanol and other fuels. These deals are backed by commitments of minimum volume or ability to pay, ensuring stable revenue streams. The company does not assume ownership or receive payments based on the value of the fuels it manages, thus avoiding direct exposure to fluctuating raw material prices.

I believe that having a look at Green Plains makes a lot of sense, primarily after the recent information given in the most recent quarterly report. Green Plains announced a collaboration with Equilon Enterprises LLC to combine fermentation and fiber conversion into one platform. Closer research about Equilon reveals ties with Shell plc (SHEL), a massive oil and industry conglomerate. I believe that more investors will most likely have a look at Green Plains as soon as they learn about the technological collaboration with SHEL.

{kind=link}

Decarbonization Could Accelerate Stock Demand

Considering the recent increase in the global decarbonisation market size, which is expected to grow at the double digit, Green Plains seems a great idea. The global decarbonisation market could grow at more than 14% CAGR from 2022 to 2032. Note that the company continues to disclose that financial growth will most likely be benefited from the company’s decarbonization strategy.

Source: Investor Presentation Source: Investor Presentation

The Global Decarbonisation Market Size is estimated to reach USD Multi-Billion by 2032, growing at a CAGR of 14.27% from 2022 to 2032. Source: Global Decarbonisation Market Size, Forecast 2022 – 2032

Ultra-high Protein Production May Also Bring Net Sales Growth

I also believe that Green Plains will most likely receive more attention considering its efforts to produce more ultra-high protein. In my view, if management can successfully communicate why ultra-high protein can be a good substitute for other corn, ethanol, or renewable corn oil, I think that we may see demand for the stock.

Source: Investor Presentation

Stable Cash Flows And Perhaps Further Acquisition Of Strategic Assets Would Most Likely Be Appreciated By The Market

Green Plains Partners' business strategy is based on generating stable cash flows through fee-based trading arrangements, avoiding exposure to fluctuating commodity prices. I believe that further communication about stable FCF would most likely lead to further interest from market participants.

Likewise, the acquisition of strategic assets that complement and diversify its existing operations was proposed in recent reports, especially in fuel storage and terminals. With that, it is worth noting that the company has to respect a certain consolidated leverage ratio that was noted in the last quarterly report.

As of the end of any fiscal quarter, the maximum consolidated leverage ratio required is no more than 2.50x and the minimum debt service coverage ratio required is no less 1.10x. The consolidated leverage ratio is calculated by dividing total funded indebtedness by the sum of the four preceding fiscal quarters’ consolidated EBITDA. Source: 10-Q

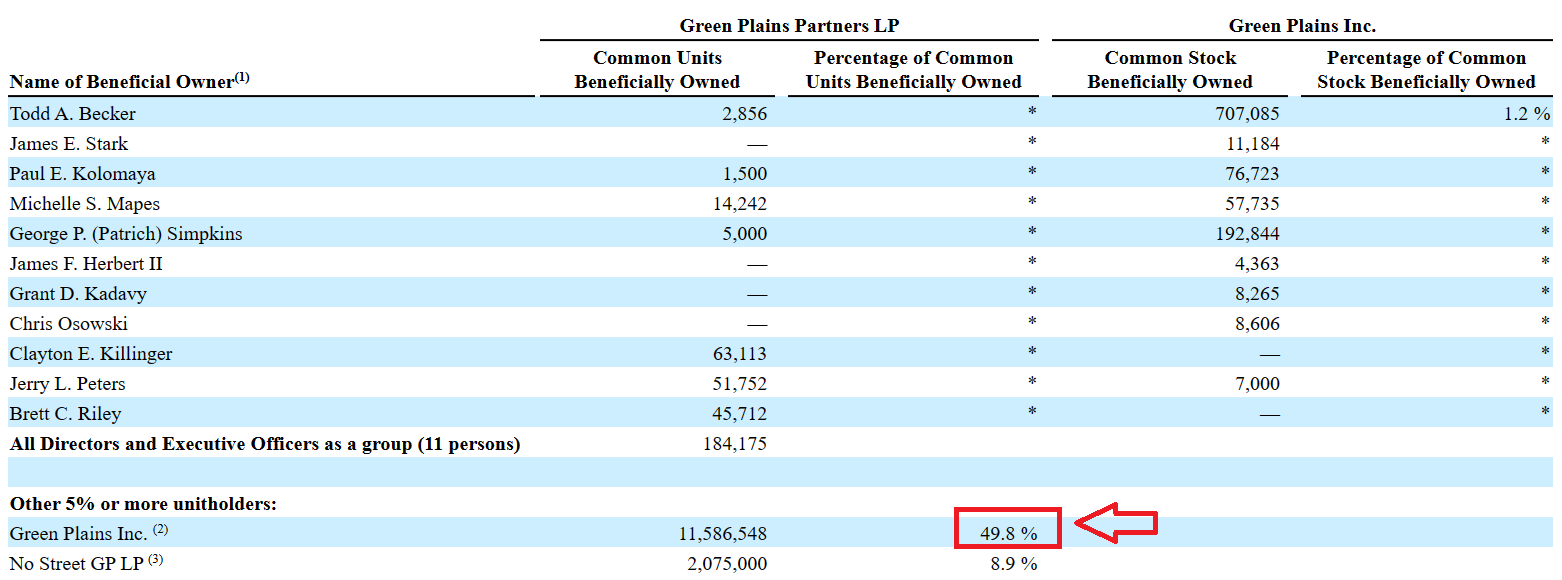

Sale Of Some Stakes To Other Shareholders Would Most Likely Enhance The EV/FCF and The Valuation

In my cash flow model, I assumed that Green Plains Partners would successfully sell more shares to shareholders other than directors and Green Plains Inc. With the new support received from an associate of Shell, perhaps more investors would decide to have a look at the decarbonization plans of the company. As a result, I think the valuation of the company would increase. Considering the current valuation of 7x FCF, I believe that the company is already trading undervalued.

{kind=link}

Balance Sheet

As of June 30, 2023, the balance sheet showed less assets than liabilities, which is not ideal. With that, management reported a good amount of cash and FCF generation. I believe that most investors would not be that worried about the total amount of liabilities. Cash and cash equivalents stood at close to $15 million, with accounts receivable from affiliates worth $14 million, total current assets of about $32 million, property and equipment of $25 million, and total assets of $127 million.

Source: 10-Q

The list of liabilities includes accounts payable worth $3 million, operating lease current liabilities of about $17 million, and total current liabilities worth $28 million. In my view, the most relevant from the balance sheet are the long-term debt of about $57 million and the interest being paid.

Source: 10-Q

Green Plains Operating Company has a $60.0 million term loan, due July 20, 2026. Interest is based on three-month LIBOR plus 8.00%, with a 0% floor on LIBOR. No principal payments are required, but the partnership can prepay $1.5 million per quarter. The loan obligations are backed by assets of the company and the equity interests of its subsidiaries.

Source: 10-Q

I could find more information about the interest rate that Green Plains pays. I believe that the interest rate being paid may change the results of the cash flow models being prepared by most investors out there.

Principal prepayments totaling $1.5 million were made during the three and six months ended June 30, 2023. The partnership repurchased $1.0 million of the outstanding notes during the six months ended June 30, 2022. The term loan had an outstanding balance of $57.5 million, $0.4 million of unamortized debt issuance costs, and an interest rate of 13.52% as of June 30, 2023. Source: 10-Q

Expectations

In order to make my own forecasts, I took a look at the numbers delivered by Green Plains. With negative net sales growth, the company reported FCF/Sales close to 56% and net income/sales of about 51%. Considering the business model as well as the previous stability of FCF margins and profit margin, I assumed that the numbers would most likely not change a lot in the near future.

Source: Ycharts

My expectations include an average net sales growth of -1%, with net sales close to $65 million including non-affiliate revenue and affiliate revenue. I believe that figures are in line with previous financial figures.

{kind=link}

Average numbers from 2023 to 2033 include average net income close to $39 million, with the following adjustments to reconcile net income to net cash provided by operating activities. Average estimated depreciation and amortization stands at $5 million, with no accretion, amortization of debt issuance costs.

Source: DCF Model

Besides, I also included changes in operating assets and liabilities before effects of asset dispositions of average accounts receivable close to -$1 million, average accounts receivable from affiliates close to $2 million, and average prepaid expenses and other assets of close to -$2 million. Finally, with an average operating lease liabilities and right-of-use assets between 2023 and 2033 of about $1 million, CFO would be about $45 million. I also included an average capex of about -$2 million and average FCF of $43 million.

Source: DCF Model

In the past, the company traded at about 7x-12x FCF, so I tried to use terminal EV/ FCF of close to these figures in my cash flow model.

Source: Ycharts

Using a variation of WACC of close to 7%-12% and EV/FCF of 9x-14x, the implied forecast price would be close to $16 and $25 per share. Besides, the internal rate of return would be approximately close to 1% and 8.1%. In my view, considering the total amount of debt and the interest rate paid, I believe that shareholders will most likely not receive double digit stock returns. With that, I think that Green Plains offers stable FCFs and a solid model. The company may be suitable for very conservative investors.

Source: DCF Model Source: DCF Model

{kind=link}

Risks And Competitors

Among the risks observed, the most significant was the heavy dependence on commercial agreements with Green Plains Trade. Additionally, Green Plains Trade may suspend, reduce, or terminate its obligations under the trade agreements, which could result in a decrease in its obligations, and affect its operations and distributions.

There is also a risk of not having sufficient cash to pay quarterly distributions due to operational and financial factors as well as restrictions and expenses. The ethanol business is highly competitive and subject to changes in market demand and regulatory environments, which may affect its financial results and its ability to make distributions to investors. These risks could have an adverse impact on its financial condition and the ability to generate returns for investors.

The company competes with independent fuel terminal operators and main fuel producers. The company’s advantage lies in strategic location, services, security, and costs. Although there are other similar operators, many do not focus on third-party services. Its experience in logistics and third-party terminals positions it favorably in a growing market. Although competition from new entrants and transportation restrictions may affect their competitiveness, the barriers to entry, such as capital costs, complex permits, and required expertise, could mitigate these risks.

My Takeaway

In my opinion, Green Plains Partners is a well-established company. I find its business strategy of focusing on generating stable cash flows through fee-based commercial arrangements and pursuing organic growth through asset development and acquisition interesting. However, there are risks associated, such as relying heavily on business agreements with the parent company, exposing it to business risks from the company and its parent. Additionally, competition in the fuel storage and distribution market is challenging, although Green Plains Partners is positioned favorably due to its expertise in logistics and terminal services. With that all being said, I believe that investors fail to understand the future production of stable FCFs. I believe that the company could be trading at $18-$20 per share.

For further details see:

Green Plains: Agreement With Shell Affiliate Could Ignite The Price