GPP - Green Plains Partners: Generate Significant Alpha From The MLP Discount

Summary

- Green Plains Partners LP sports a very high circa 14% distribution yield that would normally be considered a red flag for an impending cut.

- Whereas in this case, it sees adequate free cash flow coverage with further support from very low leverage.

- I suspect the reason for their low unit price stems from the discount often seen with MLPs, which do not necessarily have a good image in the market.

- This leaves their present unit price almost half their intrinsic value of circa $24, which even assumed zero distribution growth in the future.

- Green Plains Partners LP provides a very desirable opportunity to generate significant alpha whilst limiting downside risk, which means that I believe maintaining my strong buy rating is appropriate.

Introduction

The process of selecting investments is a very daunting task with there being thousands of options and thus far more than anyone can realistically assess. Unsurprisingly, investors lean into stereotyping or generalizations to ease the burden, whereby they tend to ignore certain sectors or attributes, one such group falling victim is master limited partnerships, hereon referred to as MLPs.

Whilst somewhat understandable, it creates situations where otherwise desirable investments such as Green Plains Partners LP ( GPP ) are caught up unfairly and overlooked. Despite hindering their unit price, it actually brings a very desirable opportunity for other investors to generate significant alpha from the MLP discount.

Background

When faced with the Covid-19 pandemic back in 2020, management took the difficult but ultimately sensible choice to cut their distributions dramatically to deleverage, which left unitholders enduring their former quarterly rate falling from $0.475 per unit to a mere $0.12 per unit. Whilst I was originally wary of whether their plan would succeed, thankfully fate ultimately proved management correct with 2021 seeing their quarterly distributions almost completely reinstated to $0.435 per unit, after which they progressively edged them to $0.455 per unit, where they have now seemingly paused.

{kind=link}

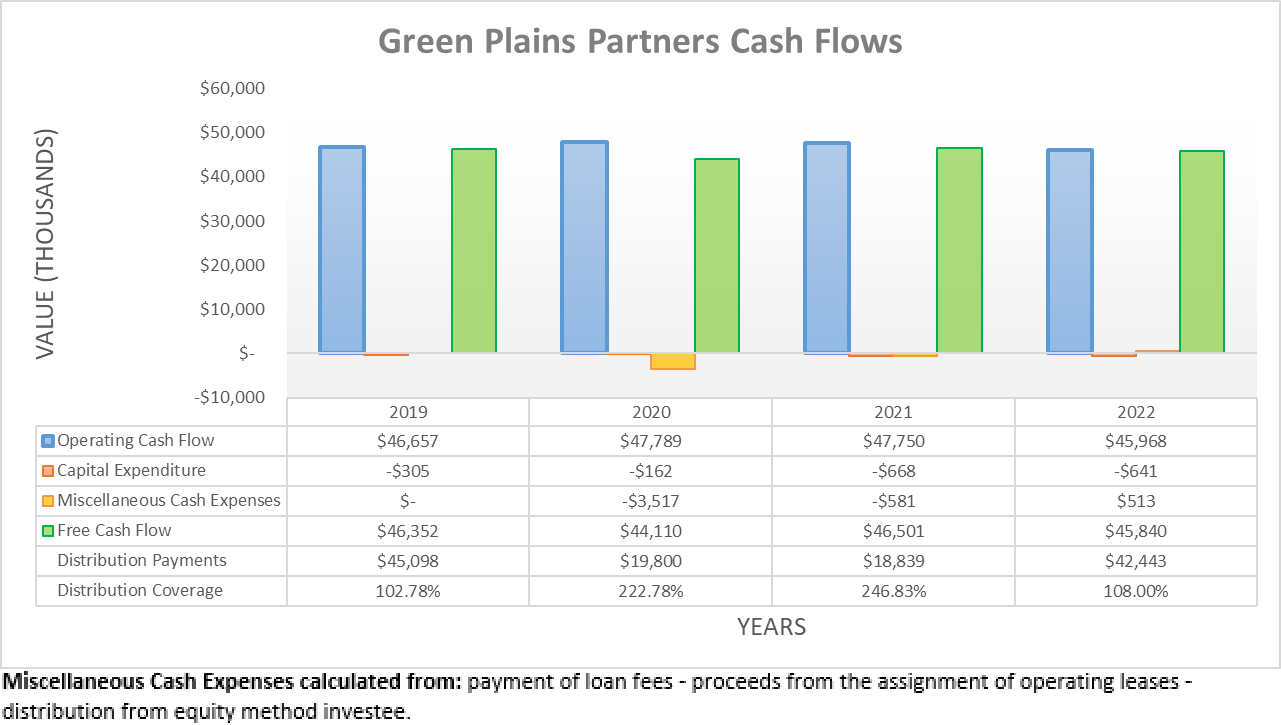

Upon reviewing their cash flow performance, they clearly have no issues funding their distribution payments thanks to their almost non-existent capital expenditure. To this point, 2022 saw the partnership generate $45.8m of free cash flow from their operating cash flow of $46m, which in turn provided adequate coverage of 108% to their accompanying distribution payments of $42.4m. Whilst this technically leaves a little room for distribution growth in the future, the margin of safety would be minimal and thus, in my eyes, it is prudent to exclude growth from any future scenarios.

When looking elsewhere, 2022 ended with debt of $58.6m along with a cash balance of $20.2m, which leaves their net debt at $38.4m, as per their 2022 10-K . Since this is obviously less than their concurrent operating cash flow, it leaves their leverage very low and thus, capable of supporting their distribution payments that consume almost the entirety of their free cash flow. If interested in further details regarding their outlook, cash flow performance or their financial position, please refer to my previous article , which covered these topics in detail, whereas the focus today is more so upon their valuation.

Despite these otherwise very positive fundamentals that leave their distributions looking safe, Green Plains Partners LP units still trade with a very high circa 14% yield, which is seemingly too high. Speaking from my time in the market, both as an investor and as a contributor here on Seeking Alpha, MLPs do not necessarily have a good image so to speak, which can see them often overlooked, especially the smaller ones such as in this case.

Part of their problem stems from the more complicated tax paperwork for unitholders, which itself is outside the scope of this article as I am not a tax advisor, but this topic can be found elsewhere via Googling “MLP tax.” Worse yet, there were instances where they were not run with the best interests of their public unitholders in mind. One that springs to mind is the now-delisted Höegh LNG Partners, as my other article discussed. Due to being under the control of their parent company, public unitholders are sometimes left second fiddle with little control and less corporate governance enjoyed elsewhere with company structures.

Whilst yes, there have been some bad apples in the bunch, it does not automatically mean every MLP is rotten or a value trap, especially when it sports rock-solid fundamentals. That said, it is hard to change a bad image in the market, but thankfully, income investors still have an avenue to profit and most importantly, generate significant alpha.

Discounted Cash Flow Valuations

Due to their distribution payments already consuming most of their free cash flow, it leaves minimal scope for growth, barring any presently unknown debt-funded acquisition. This means their intrinsic value is heavily dependent upon the future income they can provide their unitholders and thus can be estimated by utilizing discounted cash flow valuations that replace their free cash flow with their distribution payments. If interested, further details regarding the inputs utilized for these valuations can be found in the relevant subsequent section.

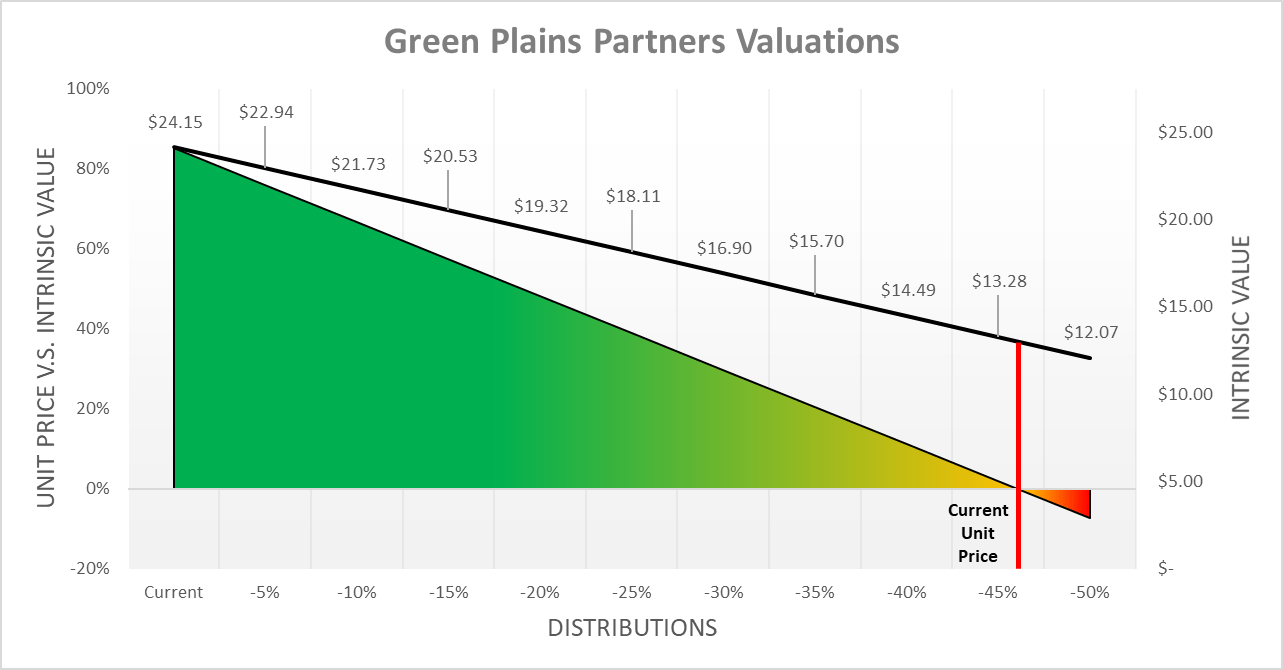

When it comes to approaching valuations, there are normally numerous ways due to the infinite number of imaginable future scenarios. Whereas in this situation, it is partly simplified because their distribution payments already consume almost the entirety of their free cash flow, which rules out any significant growth in the foreseeable future. In my view, the bullish scenario sees their present quarterly distributions of $0.455 per unit sustained perpetually into the future, albeit with zero growth. Conversely, the comparable bearish scenario sees their quarterly distributions cut in half to $0.2275 per unit before once again seeing zero growth perpetually into the future. Meanwhile, the remaining scenarios residing in between this range see distribution cuts at 5% intervals to represent a range of scenarios, all of which once again subsequently see zero growth perpetually into the future.

{kind=link}

Once reviewing the results, it shows their present unit price of $13.04 aligns closest with the scenario whereby their distributions are cut a massive 45%, which saw an intrinsic value of $13.28. Since their free cash flow and financial position can support their present distributions, I feel the bullish scenario is more likely to eventuate, which sees an intrinsic value of $24.15 that is approaching twice their present unit price. Whilst this may seem almost too good to be true, please bear in mind this would still see a high distribution yield of circa 7.50%, which is certainly still desirable and thus does not appear overvalued with any basic rule of thumb approach.

It is important to remember the relationship between risk and reward, whereby higher rewards are in theory correlated with higher risks and vice-a-versa. Whereas in this situation, it effectively says investors can take the risk normally associated with a high circa 7.50% distribution yield but due to the MLP discount, they can instead receive a very high circa 14% yield. Apart from significantly limiting downside risk, this also means that investors have a very desirable opportunity to generate significant alpha from the market overlooking this MLP.

By providing a variety of results, readers can cross-reference their own views with these valuations as they may vary from my own. In my mind, a very desirable investment is when their units are still appealing under a range of scenarios with minimal downside risk from even a bearish scenario, as is clearly evident in this situation.

Valuation Inputs

When conducting these discounted cash flow valuations, they utilized a cost of equity as determined by the Capital Asset Pricing Model. The inputs were a Beta of 1.01 (as per Barron’s ), an expected market return of 7.50% and risk-free rates per year that track the United States Treasury yield curve on February 13 th 2023, as the table included below displays.

Author

Conclusion

Even though the Green Plains Partners LP unit price may never increase sufficiently to reflect their intrinsic value given the MLP discount often observed, it does not necessarily mean that unitholders cannot win. More so, it means they are unlikely to make quick profits via capital gains but instead, they can acquire a very high circa 14% distribution yield for the risk otherwise associated with a high circa 7.50% yield. In turn, they could generate significant alpha via sitting back and collecting a hefty income and thus, I believe that maintaining my strong buy rating on Green Plains Partners LP is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Greens Plains Partners’ SEC Filings , all calculated figures were performed by the author.

For further details see:

Green Plains Partners: Generate Significant Alpha From The MLP Discount