GPP - Green Plains Partners: Growing Volumes Benefiting The High Yield

2023-07-02 04:07:52 ET

Summary

- Green Plains Partners LP has strong exposure to growing demand for ethanol.

- GPP has built up a solid balance sheet which can support the operations efficiently.

- The high yield is sustainable thanks to strong cash flows, making GPP an appealing long-term position.

Investment Summary

When you see a company that has a dividend yield of over 14%, or over 10% for that matter, it's often not a very good signal as it might be a one-time thing and not a sustainable amount. Often, the high yields result in a company share price that barely appreciates. I am covering one such company, Green Plains Partners LP ( GPP ), a company that provides fuel storage and transportation services in the ethanol industry. The company is the offspring of Green Plains ( GPRE ), which is one of the largest producers of ethanol in the US.

As a provider of fuel storage and transportation, it operates in the midstream industry in the ethanol sector. Now, GPP isn't a major player here, as revenues are $81 million in the TTM. The current relationship between the two companies is that GPRE owns 48.8% of the shares of GPP, and the rest remains open to the public. This partnership helps bolster the position of GPP, and I think there is a strong case to be made that FCF will remain strong and help fuel the high dividend yield.

Robust Outlook For Ethanol

The outlook for ethanol remains quite strong. Estimates suggest we will see an increased production volume in the US, which is noticeable in the last report from GPP. The product volumes for GPP increased by 5.5% YoY to 208.1 million gallons. The production levels of ethanol right now in the US are actually at their highest level since December 2022, and the trend is going upwards.

{kind=link}

Production peaked back in 2020 but is seemingly finding its new bottoms. But I think there are some challenges the industry will have to face, like the negative sentiment around the commodity. As more and more people are realizing the impact that ethanol has on the climate, I think more pressure will be placed on government officials to take action. This will in turn put pressure on ethanol companies, as the same amount of volumes might no longer be possible to achieve. But the US is exporting a significant amount of ethanol which provides a market for GPP still, and global demand doesn't seem to be halting or facing the same scrutiny as in the US.

Production Segments (Earnings Report)

As the outlook for ethanol remains relatively robust, it should help provide significant cash flows for GPP to continue to distribute to shareholders. The CEO Todd Becker said the following in the last report, “Consistent cash flow driven by reliable operations allowed the partnership to maintain its cash distribution to unitholders”. With the strong utilization rate at 87.5% of capacity, it seems there is still room for GPP to grow and meet demand. That would result in even stronger cash flows. To support operations and continue generating strong FCF, GPP has built up cash and cash equivalents, and restricted cash valued at $408 million and a further $159 million available under a committed credit facility. This will act as a cushion for when operations are facing challenges and GPP still wants to distribute its dividend.

How Sustainable Is The Yield

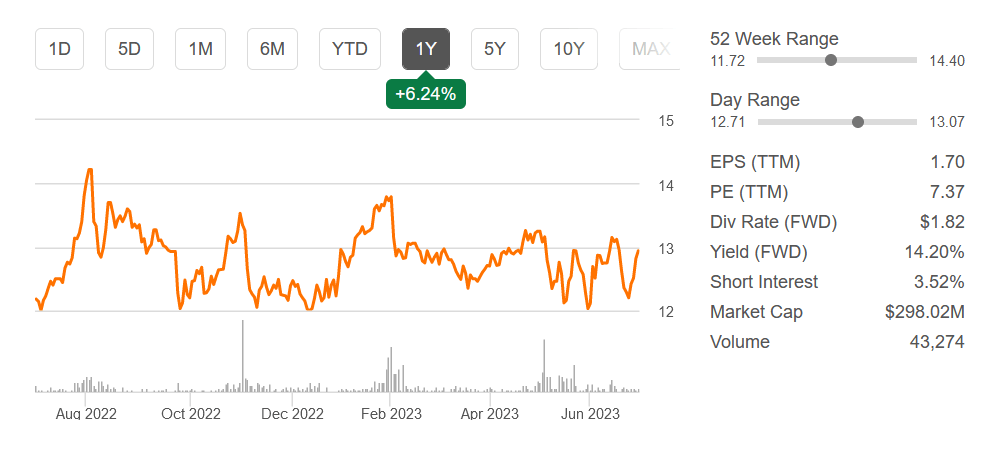

With a yield of 14.8%, GPP offers investors a solid return on their investments and a share price that has remained quite stable through the years. Back in the middle of 2015, the share price was around the $14.8 mark, or 21% higher than today. But over that period, investors will have collected a strong dividend that has helped offset some of the otherwise losses on an investment.

Dividend History (Seeking Alpha)

The dividend history has been very stable and remains around the same. I think that given the last quarter's utilization rate of 87.5%, it leaves room for improvement and in turn a reason to maintain the current dividend without the risk of lowering it. Where GPP has been susceptible is during unprecedented times like the pandemic, when the dividend yield had to be cut as global demand for energy plummeted.

As I have discussed above here, the outlook for ethanol remains quite strong, and recently permitted a higher blend of ethanol permitted by US EPA, which will increase demand for GPP. The results should be that GPP can maintain and even raise the dividend in the single digits.

Risks

The risk I associate with GPP isn't necessarily the negative sentiment that is put on the industry from people seeking renewable options, or that demand will diminish. Instead, that companies in the sector have to maintain very good margins as they aim to sell the byproducts from turning corn into ethanol to keep operations profitable. Where GPP has done good work is the large increase of Ultra-High Proteins sold, which increased by 333% YoY, as seen in their last earnings report. If they can log into markets like this to keep margins stable, then I think GPP offers even less risk.

Financials

In terms of the financial state that GPP is in right now, some improvements have been made. They have grown their current assets quite efficiently, up 9.5% YoY, seemingly a result of higher accounts receivables, which were $19 million in the last report.

Balance Sheet (Earnings Report)

In terms of debt for GPP, they have remained very disciplined here. Since 2021 it has not increased and sits at $58.6 million. I find the debt very manageable given that GPP is generated a levered FCF of $30 million in the TTM. GPP right now has a net debt/EBITDA ratio of 2 which is a decent number to be at. I don’t think debt will become an issue for them, and the growing demand for ethanol will help them build up the EBITDA even further. To conclude, I think that GPP is in an excellent position right now financially, and I think attention will be placed on the production levels and margins instead.

Valuation & Wrap Up

Having exposure to the ethanol industry I think is very appealing, the demand in the short - medium term certainly is there as discussed above. We have discovered here that demand seems strong from both the US market and the international one. As US exports of ethanol remain strong, growing from 1.24 billion gallons in 2021 to 1.35 billion gallons in 2022 it provides GPP with more opportunities to grow revenues.

{kind=link}

The biggest appeal of GPP is the high dividend yield. With the demand and outlook for ethanol, I think the yield is sustainable, and utilization rates have room to grow higher, which could result in a slight dividend raise. As far as valuation goes, I think paying around a 7x FWD earnings multiple is very fair given the industry it's in and the growth it's estimated to have. It's only slightly above its 5-year average p/e of 6.7 and boasts largely the same margins as the 5-year average too. Compared to a similar company like Summit Midstream Partners LP ( SMLP ), I think it's clear GPP comes out ahead. With a much lower valuation and better margins than SMLP. All in all, I think that GPP is at a very appealing entry point now to make it a long-term position.

For further details see:

Green Plains Partners: Growing Volumes Benefiting The High Yield