GRFS - Grifols: Cheap For A Reason

2023-09-21 13:56:01 ET

Summary

- Grifols is a Spanish pharmaceutical company focused on blood plasma products, with a strong market position and an attractive growth pathway.

- The shares have underperformed peers and yielded negative returns over the last five years.

- We believe the equity is fairly priced - although optically cheap, the company has a massive debt burden that needs to be addressed.

We present our note on Grifols ( GRFS ), a Spanish international pharmaceutical and chemical company focused on blood plasma products, with a Hold rating. While we like the oligopolistic market structure and Grifols’ strong positioning as well as the long-term potential of the plasma market, we are concerned about the high leverage and believe the equity is fairly priced. We will provide an overview of Grifols and its business, analyze the leverage situation, and present our valuation and investment verdict.

Introduction to Grifols

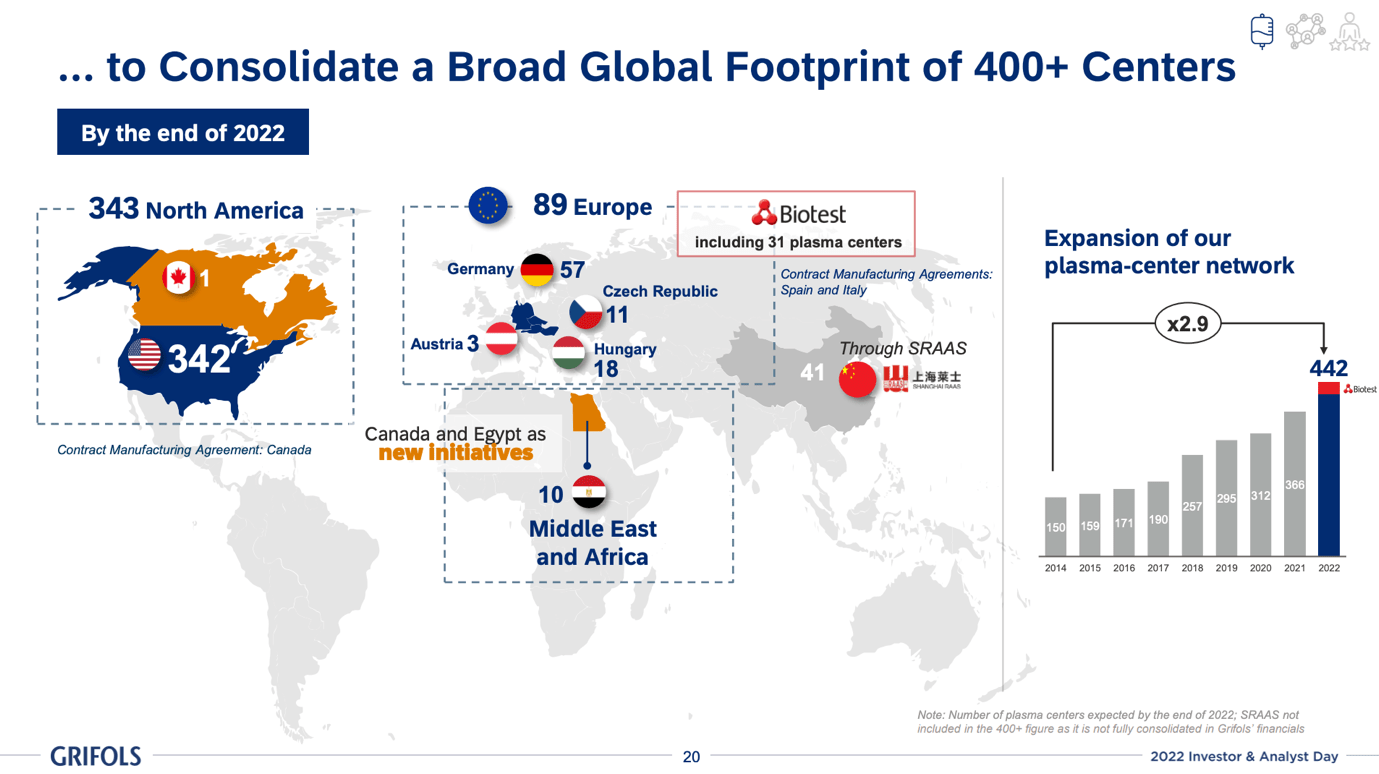

Grifols is a leading global healthcare company based in Spain, providing plasma derivatives (a top-3 international player) and other innovative biopharmaceutical solutions. Grifols’ products are used to treat patients across a wide range of therapeutic areas including immunology, hematology, hepatology, etc. It has a large network comprising more than 400 centers across Europe, North America (generating two-thirds of revenue), the Middle East, Africa, and China, offering a variety of solutions with a focus on safety. Grifols also runs a diagnostic unit and is a leader in nucleic acid testing. The company is controlled and managed by the Grifols family, which owns around 30% of the shares through various vehicles. Grifols is an IBEX35 constituent and has a market capitalization of ca. €8 billion.

{kind=link}

Favorable industry structure

Grifols’ plasma centers take in paid plasma donations and separate the proteins for medical use. In the US (where 75%+ of centers are located) donors are paid around $50 for an average donation of 750ml. More than half of the biopharma segment revenue (focused on plasma) comes from IG (immunoglobulins), a mix of antibodies present in donors’ plasma. IGs are critical in the immune response to antigens such as bacteria and viruses. IGs are administered to patients to treat immune deficiencies in low doses and to treat autoimmune conditions in higher doses. Grifols is a leader in the intravenous IG (IVIG) space. In addition, less than a fifth of biopharma segment revenue comes from albumin administered mainly to hepatology and intensive care patients. Moreover, 15-20% of segment sales come from AAT, administered to patients who lack the protein needed for the normal functioning of the lungs. The diagnostics segment comprising 15% of group sales is focused on blood donor screening, blood typing, and other biochemical tests.

The plasma industry is oligopolistic with four companies: CSL, Takeda , Grifols, and Octapharma, controlling around three-quarters of the market share. Grifols owns around 30% of plasma centers globally and processes a quarter of global plasma volume donations. Barriers to entry are high as substantial know-how and investment are required, given the capital intensity, regulation, expertise, and branding. Moreover, there is no potential for tangible competition/disruption from pharma pipelines as of now.

The industry is set for an attractive growth pathway supported by various structural tailwinds. Over the last decade demand for IG (the predominant driver) grew by high single digits CAGR, driven by population growth, higher diagnosis rates, and better healthcare standards. Despite the notable improvements, many patients remain undiagnosed. Grifols also expects significant growth coming from secondary immunodeficiency-related demand coming from higher oncology and autoimmune disease patients. Competitors such as Takeda expect IG to grow by close to 10% annually, while CSL, the industry’s #1 player, expects high single-digit plasma demand growth over the midterm (including IG, albumin, AAT, etc.).

High leverage and continued underperformance

Despite being a top player in a growing industry with a moat, Grifols has failed to generate satisfactory equity returns over the last five years – the stock is down 46% during this span – widely underperforming CSL. Margins are significantly lower than CSL due to a worse mix, lower pricing power as a result of less innovative product offerings, and higher costs. We believe there is untapped potential for self-help measures to improve profitability. Moreover, the company has been highly active in the M&A market, executing many deals that have generated little to no value, and causing leverage to balloon to nearly 7.5x Net Debt / EBITDA.

High leverage is a major issue not allowing us to be comfortable buying the stock even at seemingly low multiples. The negative performance of the shares can be largely attributed to the high debt burden amid a backdrop of rising rates. Although around two-thirds of the debt is fixed, and the earliest debt maturities are in FY2025 the situation is concerning and, in our view, there is a substantial risk of an equity raise if organic deleveraging fails for any reason. Management has expressed unwillingness to pursue an equity raise at current share price levels and is instead focused on organic deleveraging and potential asset disposals. An equity raise would have a major dilutive effect on the controlling family’s ownership, and we believe there is a certain reluctance on their side to pursue a raise unless all other options are exhausted. We believe the stock will not rerate until leverage comes down either organically or inorganically.

Valuation and investment verdict

We value Grifols using an EV/EBITDA multiples approach, as PE ratios do not make sense for such a leveraged company. We forecast €7.1 billion of sales in FY2024e, growing 8% from FY2023. This forecast is in line with consensus expectations. We assume an EBITDA ratio of 26.5% similar to normalized levels pre-2020, and at a significant improvement vs. the current year, attributable to operating leverage coming in from the rise in volumes post-Covid, and we arrive at an EBITDA of €1.9 billion. Adding €9.6 billion of net debt and other EV adjustments, Grifols is trading at an implied forward EV/EBITDA ratio of 9.2x. While this is much lower than the lower-mid teens multiples pre-2020, we believe this discount is fair for a highly levered company with a net debt / EBITDA ratio of around 7x. As leverage declines, Grifols should trade closer to its historical higher multiples and close the gap with CSL. At around 3x net debt / EBITDA, we believe Grifols should trade at a 15-20% discount to CSL, or at 12-13x EBITDA. We believe there is significant execution and financial risk and do not see a compelling case for going long Grifols shares at this price.

Risks

Risks include but are not limited to high dependency on donors leading to higher donor fees and lower margins, inability to attract donors in the future, innovation from plasma center peers and the wider pharma industry, adverse regulatory changes increasing friction and costs, delays in new launches, operational risks given the complexity and safety requirements, high leverage leading to the need for an equity raise and dilution of shareholders, suboptimal capital allocation such as value destructive M&A, governance risks given the control by the Grifols family, etc.

Conclusion

While shares look optically cheap, we believe Grifols is cheap for a reason. We will monitor the company and we could find the shares appealing at a significantly lower leverage ratio (potentially after an equity raise, or after organic deleveraging). We currently rate Grifols as a “Hold”.

For further details see:

Grifols: Cheap For A Reason