GRFS - Grifols: I've Read The Short-Seller Report And I Mostly Disagree

2024-01-10 06:30:00 ET

Summary

- Grifols' position in the pharma industry has dropped due to a short-seller report, causing its stock to decline.

- The report questions the accounting treatment of M&As and consolidation of entities in Grifols' filings.

- I believe that the allegations in the report are not significant enough to warrant a 20% drop in the company's stock and plans to wait for a reaction before adding more to their stake.

Dear readers/followers,

My position in pharma company Grifols (GRFS) was up a nice 20% from several of my investment articles with a bullish perspective up until yesterday. After the short-seller-induced drop, my positions are mostly either only slightly in the green, or downright negative.

That is, of course, the natural consequence of something like a short-seller report that might contain a few nuggets or more than a few nuggets of truth. In this article, I'll go through with you the potential ramifications of what the report accuses Grifols of, and my determination whether there is any truth to what is being claimed here.

I will start this article by saying that I, unlike others did not sell my Grifols shares.

Nor did I add more - at least not yet (but there are reasons for that as well, and we'll get into them).

So let's look at what we have here.

Grifols - Looking at the latest results, and the allegations

One of the most common targets for short-sellers like Gotham, which is the author of the report we're looking at here, is the accounting treatment given to M&As and similar deals.

I can remind you in this article, that this is not the first short-seller report of a European company that I've covered where accounting treatments have been the core of the allegations or concerns. A few months back in August of 2023, Hexagon (HXGBY) was made a target for short-sellers, and part of what was said here was the treatment of transactions like Divergent Technologies, or using vehicles to front-run it's M&A as well as general accounting practices, which later proved to be fully compliant with IFRS.

Since that time, by the Way, Hexagon has recovered every inch of ground given up during the short-selling time, and I have recovered my position and enhanced my cost basis.

You should never be against short-sellers , is my view. In the vernacular of the TV show "Billions", these are essentially white blood cells. If there is merit to their claims, then it's good that they come to light. If there isn't merit, the stock will eventually recover.

Are there "bad actors" in this field that try to take short-term advantage based on flimsy allegations?

I would say yes.

Is this one of them?

I would say 'maybe'.

Let me first state that Grifols has not yet issued an official longer response detailing the various points made by the short seller. It may come, it also may not, and this may shed further light on things.

With things in their current state, all we have are the official filings.

However, I will say , that it seems to me, after having reviewed the short seller allegations, that the core of their arguments is how the leverage levels develop following the treatment of party transactions, and a key point made here is that "unconsolidated entities" represent a material or large portion here, specifically Haema and BPC Plasma, accounting for around 40% of company earnings from non-controlling interests.

I am not a CPA - or an accountant in any jurisdiction for that matter. But what I do know, and this is also based on reading Grifols filings in the matter, is that the transaction treatment given sales of entities such as Biotest or Haema have been fully endorsed by the company auditor KPMG.

What is also clear is that all material pertaining to these transactions has been communicated to relevant authorities in both Spain and the US, where the company is represented. I also have a hard time, meaning that I haven't found anything, that can be considered "hidden", or to be considered manipulated in a deceitful way.

My interpretation of the short-seller report is that they disagree with the way these transactions have been treated in terms of consolidation in the company's filings - and I admit that these are questions at least worth asking. There are some added curiosities, such as the $95M loan in 2018 - but even with the entirety of the supposed suspect loan transactions mentioned in the short-seller report, we're talking less than 2.5% of annual company revenues, looking at a projected €7B annual revenue for Grifols.

These sorts of things are actually something I work with on a daily basis. When things are open to interpretation and it's possible to do things in a number of different ways - as things always are in accounting - you're going to find people that say "You shouldn't do it that way", or "You should only do it this way".

The key point here is if the company has engaged in elaborate, fraudulent behavior to a degree where I would consider the company's future or investability in danger.

I say that I based on this short-seller report, find no evidence of this. At least not yet. The short-seller also isn't accusing Grifols of material and thorough accounting fraud, merely consolidation treatments for two, albeit relevant, parts.

But the fact that Grifols has made clear that the relevant auditor KPMG has signed off on this treatment means to me that it will likely become a question of interpretation - and if there in the end is a clear statement that "this" was the wrong way to go about things for Grifols, well, then that blame will likely partially fall on KPMG as well, and potentially result in some broader accounting changes.

But again, I doubt that.

Any argument such as this being made where unconsolidated entities represent this or that percentage is usually a timing concern . And whenever your short-selling report is based even in part on a timing concern - because this is subject to change, then I don't view it as being that relevant. It's completely normal to consolidate entities over 50% - and if that point falls, the remaining points the short-seller raises are circumstantial. Some are interesting, and with the Scranton vehicle behind a Grifols family-owned entity, these are questions worth asking. But as some others have already commented in the analyst community, none of these allegations are new. ( Source )

Are they things that warrant a 20% drop?

I would categorically say no.

It's important to realize that short-selling is a very dangerous occupation - in terms of loss potential. Companies and players in the field "have to" make money off violent markets and company movements, and this sometimes dictates their approaches and actions. As an example, short-sellers ended 2023A with paper losses of nearly $195B , losing money also in 2021 and 2020 to a total, of nearly $600B loss for those years, offset only half by a $300B gain in 2022 when the market routed (Source: Bloomberg). For a 3-year period therefore, it can be said that they're generally about $300B in the negative - though it's more complex than that, of course. Still - it's a good consideration and knowledge to have.

Most short-sellers lose money.

That's a large reason why I don't short. The fact that you usually just have to "wait" short-sellers out is another positive. I currently own significant stakes in two stocks, aside from Grifols, that are short seller targets, one of them over 10% shorted.

As I said, I do not mind short-selling. I have the utmost respect for some - like Hindenburg.

But in this case, I would say the market is overreacting.

My reaction & strategy

That's why my typical reaction is also for short-sellers to "bring it on". Because if I know my stuff, then I can get the company cheaper.

In this case, Grifols has already indicated that the company is planning a call to address some of the concerns made by the report (Source: Bloomberg ).

Because none of these allegations are new, my general strategy is to wait for this reaction to bottom - and once it has, add more to my stake in Grifols.

Grifols is a world leader in blood plasma annualizing over €6B in revenues and coming out with a double-digit operating margin. That the company has challenges is nothing new. But Grifols makes money. And that is more that can be said for a lot of biopharma businesses out there. And while margins for net have been declining since COVID-19, Grifols is a company with a track record of significant revenue growth.

Its challenges are not, as I see them, micro-oriented, but rather related to the international complexity of blood plasma donations. You see, the legality of donating blood for money is extremely complex - with most European nations not allowing such things.

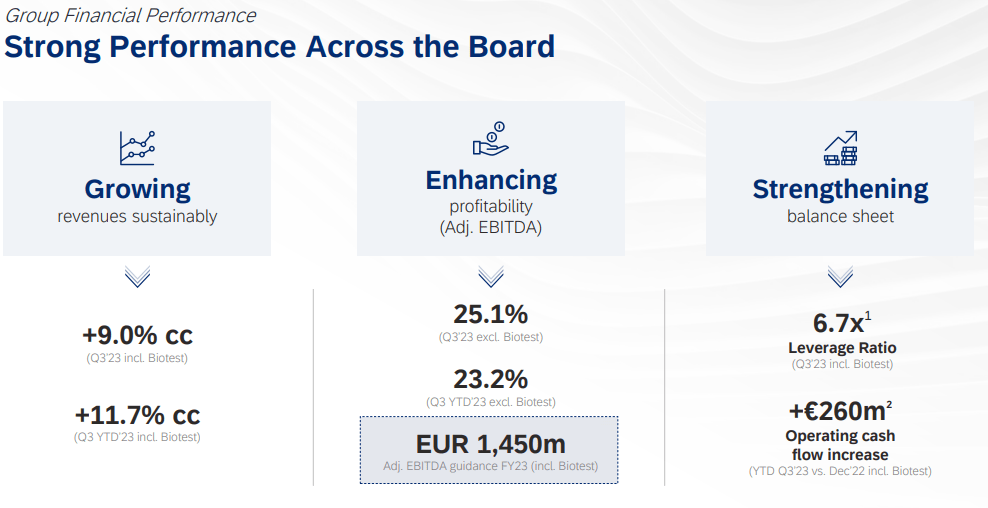

The company's latest results, which came out a few months back, to me confirm the overall upside of this company with double-digit revenue growth, expanding margins, over €450M in cost savings, growing plasma supply, and a confirmed FY23 EBITDA guidance of almost €1.5B.

The company's leverage, going by its, which also is my definition , is going down and is now 6.7x, down from 9x back in 2Q22, and it is targeted to reach 4x by 2024. There is also another deleveraging transaction coming.

{kind=link}

Now, is this the safest sort of company with the best sort of conservative upside and yield? No, it isn't - the company has plenty of challenges that it needs to work through, and it doesn't in fact even have a yield at this time.

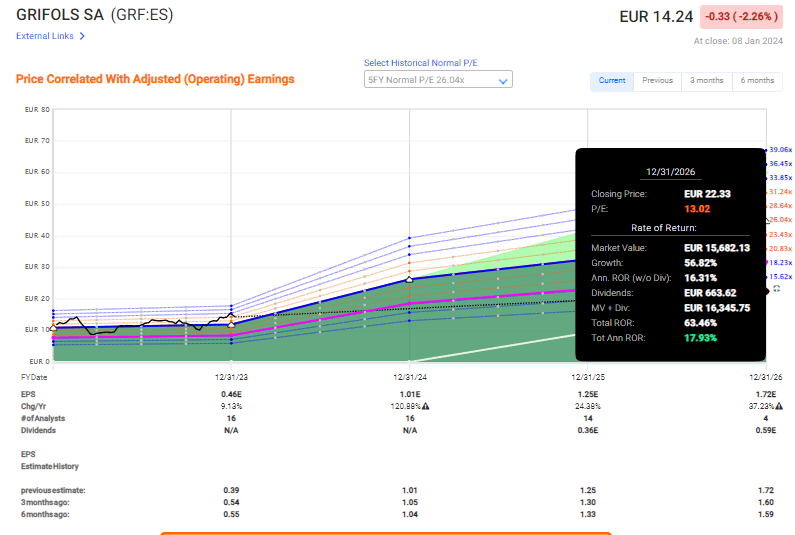

But it's a company that's set to grow significantly. Even with the B+ rating, because that's all it has, normalizing this company's multiple at 13x on a 2026E basis, which is less than half the typical 26x P/E , we get a 18% annualized RoR.

{kind=link}

And once we look at something like a more common 20-25x P/E upside, well, then we're looking at the potential for 200%+ RoR in 3 years for this company. Grifols mostly beats or hits its targets as well, it doesn't often miss them, giving me further conviction here.

Again, overexposure to Grifols is not something you'll want - I don't have it either. But whenever I see this sort of potential from a company with a strong moat-like Grifols, then I want at least some exposure.

Because I don't believe the short seller report holds much water here, even if I'm curious to see some of what the company says, I give you the following thesis on Grifols here.

Thesis

- Grifols is the world leader in Plasma and plasma-related biopharma. This gives the company a clear advantage. However, overleverage has driven credit rating to a B+ and canceled the company's relatively acceptable dividend, which impacts what we should pay for the company.

- I don't believe the latest short-seller report materially changes my thesis for Grifols, and still consider it an interesting potential at my previously-communicated share price.

- I can call this non-yielding business a speculative "BUY", despite an upside in the double digits and an "easily" forecastable upside of over 20% per year until 2026E if the company's expectations materialize.

- I'm still at a €17/share native PT , which means that I'm positive, and own the stock, but I'm staying very conservatively exposed to make up for the risk I see here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I argue that the only issue is really the dividend since the B+ cannot be said to be equal to not being conservative, given the company's market position. That makes it a "BUY".

For further details see:

Grifols: I've Read The Short-Seller Report, And I Mostly Disagree