OMAB - Grupo Aeroportuario del Centro Norte: Crisis Creates Opportunity

2023-10-09 01:02:55 ET

Summary

- Mexican airport regulator's potential change to tariff formula caused shares to plummet.

- The current share price incorporates an 18% tariff cut, which seems harsh.

- Two other scenarios suggest a potential upside from current levels, but the situation remains speculative.

Summary

In a surprise move, the Mexican airport regulator apparently changed the formula by which the three Mexican airport groups charge for services i.e. generate regulated revenue. Unfortunately, there is no more concrete information as to the scope of the tariff/revenue impact nor the legality of the unilateral concession contract changes.

For more depth on the Mexican Airport business model please refer to my article: Mexican Airports: I Prefer ASR Over OMAB And PAC .

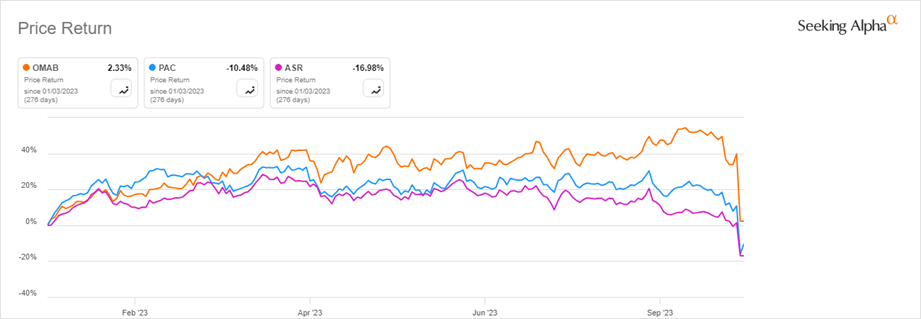

The market reacted negatively, selling off Grupo Aeroportuario del Centro Norte (OMAB) ("OMA") shares, at one point down 40% to US$50. On current estimates, which factor in the maximum regulated rates and fees that OMA can charge, the stock valuation declined to 9x PE, a level not seen in years.

OMA Share Price YTD (Created by Seeking Alpha)

{kind=link}

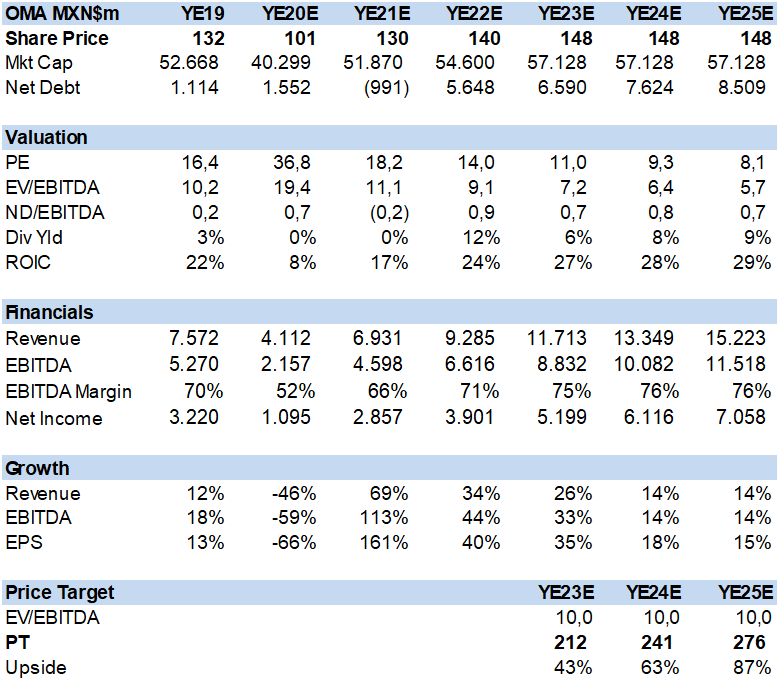

OMA Financial Summary and Valuation (Created by author with data from OMA)

{kind=link}

Four Scenarios

While the outcome of the "news" is far from resolved, conjecture and fear may continue driving share prices in the immediate future.

In order to attain some semblance of reality I conducted a simple sensitivity analysis.

- How much would tariffs need to decline for today's stock price to be considered fair?

- What if rates decline 8%?

- What if OMA is allowed to extend its concession contract for 50 years but acquires the abandoned Mexico City airports debt (20% or US$1bn)? This 3rd scenario has a political motivation behind the Government's arbitrary move.

Scenario 1: What is priced in

In order to back into a potential tariff cut estimate using OMA's current price I first need to assume a fair multiple post-event. Given the trauma of a govt bending or breaking of rules/laws, the fair or target multiple should decline from 10x to 8x EV/EBITDA.

Then I calculated that regulated rates would need to be cut by 18%, impacting revenue, EBITDA, and Net Debt, so that 8x EV/EBITDA results in today's closing price. Note that I do not assume a reduction in capex while traffic growth remains as estimated.

The result is a bit hard to imagine, most likely excessive and would damage the company's ability to execute growth infrastructure in the midst of an industrial boom i.e. nearshoring investment.

OMA Tariff Cut Scenario (Created by author with data from OMA)

Scenario 2: An 8% tariff cut

This 8% tariff cut would hurt but is manageable and can be recuperated with traffic gains and greater commercial revenue. However, the damage to valuation is more permanent and price recuperation to US$95 may take several years.

OMA Tariff Cut Scenario (Created by author with data from OMA)

Scenario 3: Adding US$1bn in debt

This third scenario requires a bit of game theory. The Mexican Government, in its infinite wisdom, cancelled the New Mexico City Airport that had commenced construction under the previous administration. This meant that the Mexican Federal government was left with about US$5bn in debt , mostly bonds, that had been secured to fund the project. I read in media sources that the Govt wanted to have this debt removed, transferred to the private concession groups. What better way to gain negotiating leverage than to threaten them with tariff cuts. True or not, it makes a good story and at least provides a reasonable motive.

Scenario 3 assumes OMA takes US$1bn in debt but gains the extension of the concession for another 50 years. I believe the market would not cut fair multiple valuations. Thus, the impact on the YE24 price target would be +30%, a good result.

OMA Debt Transfer Scenario (Created by author with data from OMA)

Scenario 4: Govt Backtrack

The government backtracks or is defeated in courts and the business model is unchanged. Which means that current estimates and valuation return.

Conclusion

Investors are in a very difficult situation; logic has been turned upside down by the Mexican Government. However, it seems the current price factors in an unlikely scenario, while the second and third provide upside potential. Finally, it is possible that nothing happens, and the government retracts an arguable illegal change to the contract and waits for the next master plan negotiation to obtain reasonable results. Those with a more speculative mindset may buy the shares. I am cost averaging down on my OMA shares.

For further details see:

Grupo Aeroportuario del Centro Norte: Crisis Creates Opportunity