HGTY - Hagerty: Stuck In First Gear

Summary

- Hagerty is the world’s largest insurance agency specializing in classic cars with a captive reinsurance company and ancillary businesses designed to create an "automotive enthusiasts platform."

- The company went public in 2021 via a SPAC creating massive potential dilution from insider common stock and warrant sales.

- YTD 3Q 2022, operating income was negative, but GAAP non-cash valuation items allowed the company to report net income.

- Prices around $7.00 per share are intuitively appealing, but wait for a) operations and financial statements to stabilize and b) a substantial reduction in the uncertainty regarding the common stock and warrant dilution before considering an investment.

If you’re even remotely interested in classic cars, you’ve probably heard of Hagerty ( HGTY ), the world’s largest insurance agency specializing in classic cars, trucks, motorcycles and boats. As a classic car enthusiast, when I discovered Hagerty was now a public company, I had to investigate.

Hagerty was founded in 1984 by Frank and Louise Hagerty under the name Hagerty Marine Insurance Agency, Inc., to insure antique boats. In 1991, the company re-focused on the larger market of classic cars, trucks and motorcycles. The company’s motto became “Insurance For People Who Love Cars,” now updated to “Hagerty For People Who Love Cars.” In 2000, McKeel Hagerty , son of Frank and Louise, became CEO. As CEO Hagerty launched growth initiatives to create an “ automotive enthusiast platform ” including:

- Hagerty Media, print-based Hagerty Magazine and digital assets including a YouTube channel .

- Hagerty Valuation Tool, an online tool for valuing classic vehicles.

- Hagerty Drivers Club, a bundling of Hagerty products.

- Hagerty Events, owner and producer of various car shows and related events.

- DriveShare, a social media-based classic car rental service.

- MotorsportsReg.com, the world’s largest calendar of motorsports events.

- Garage + Social, club locations for the storage and maintenance of classic cars.

- Hagerty Marketplace, online auctions and classic car classifieds.

The company’s stated goal is “To save driving and car culture for future generations.”

A Word About MGAs

Hagerty is technically a Managing General Agency/Underwriter (“MGA” or “MGU”) with a captive reinsurance affiliate (Hagerty Re) rather than a traditional insurance company. An MGA is an agency authorized by an insurance company to issue binding coverage, underwrite and price policies, settle claims and appoint retail agents. As such, Hagerty earns commission and fee revenues for distributing and servicing insurance policies written through agreements with multiple insurance carriers in the U.S., Canada and the U.K. A well-known example of an MGA would be Marsh & McClennan (NYSE: MMC).

Driving a SPAC: Becoming Public Company

SPACs or “blank check” companies boomed during the last five years, but have a very mixed record . Often fronted by Wall Street luminaries, SPACs are shell companies that sell IPO units, typically for $10.00. Each unit consists of a common share and a warrant to purchase a common share at a strike price of $11.50. The SPAC is limited to two years to complete a shareholder approved acquisition. If no suitable deal is found, the funds raised are returned with interest.

In August, 2021, Hagerty announced a merger with a SPAC called Aldel Financial, Inc. Aldel was a very good fit for Hagerty. Aldel’s CEO was Robert Kauffman , former CEO of Fortress Investment Group, a $45.0 billion AUM private equity firm, and then - and now - a Hagerty board member. Kauffman is well-known as a classic car collector and for significant involvement with Formula One, NASCAR and Indy racing.

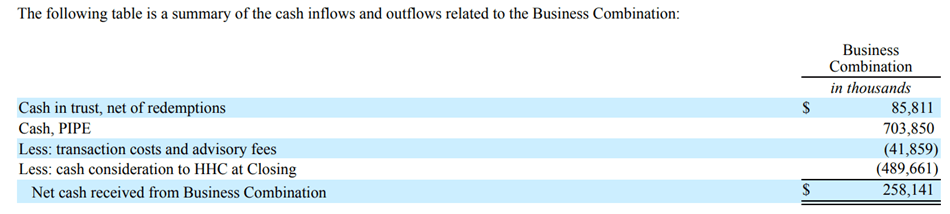

The transaction was completed on December 2, 2021 with the “new” company, Hagerty, Inc., valued at a pro forma $3.13 billion. The components were an $85.8 million cash contribution net of redemptions from Aldel, a PIPE offering wherein institutional investors including Markel (MKL) and State Farm bought approximately $703.6 million in stock and warrants and $2.5 billion from Hagerty stockholders rolling their investment into the “new” entity.

After all conversions and issuances of stock in connection with the SPAC IPO, there were 82,327,466 shares of Hagerty Class A stock, 251,033,906 shares of Hagerty Class V common stock and 20,005,550 warrants to purchase shares of Hagerty common stock outstanding. The Class V stock (with 10 votes per share, effectively maintaining control) was issued to the Hagerty family and Markel - the pre-SPAC owners of Hagerty Group - and was convertible to Class A stock. Class V stock neither trades nor has an economic interest in Hagerty until converted to Class A, thereby being a major source of potential dilution. The surviving corporation became Hagerty, Inc.

In addition to Kauffmann bringing relevant knowledge and expertise to the company, Hagerty’s SPAC IPO benefitted from its insurance company strategic partners, Markel and State Farm, taking significant positions in the company; 17.2% and 23.5%, respectively, as of December 2, 2021. Markel had owned 25% of the “old” Hagerty before the SPAC deal and State Farm invested $500.0 million through the PIPE offering. In addition, the Hagerty family retained a 52.8% position .

In cash terms, only $258.1 million or 32.7% of the total cash in the SPAC IPO trickled down to the Hagerty, Inc. balance sheet. Advisory and transaction fees and payments to the Hagerty family consumed $41.9 million or 5.3% and $489.7 million or 62.0% of the net cash raised, respectively.

{kind=link}

At deal close, the Hagerty family not only maintained 52.8% ownership and control of Hagerty, Inc., but also had received nearly $490.0 million in cash. The interests of the strategic partners and the Hagerty family remained closely aligned through their stock ownership.

Strategy: Supercharged Opportunity

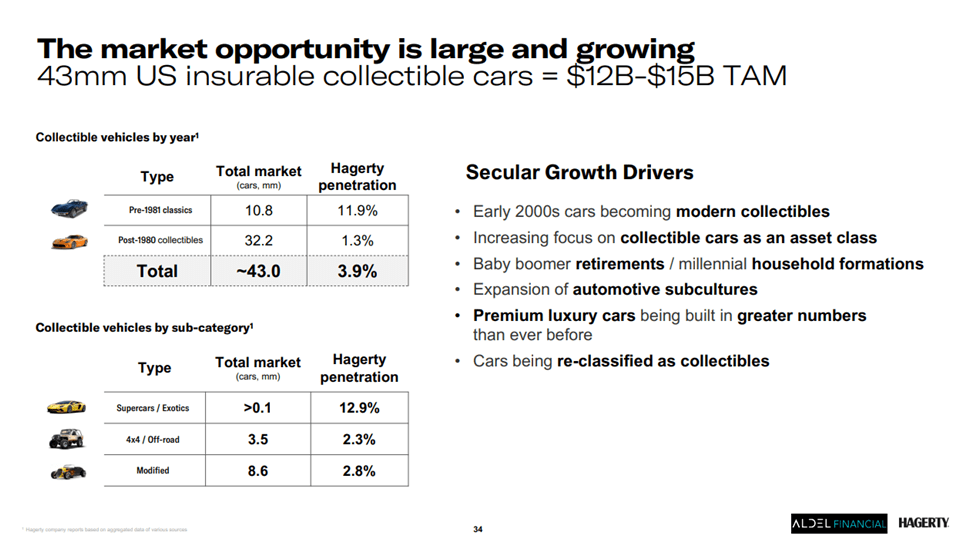

Hagerty estimates a total addressable market (“TAM”) of more than 500 million car enthusiasts worldwide. In the U.S., Hagerty estimates a TAM of more than 69 million car enthusiasts owning more than 43 million classic cars.

Hagerty 2021 IPO Investor Presentation

{kind=link}

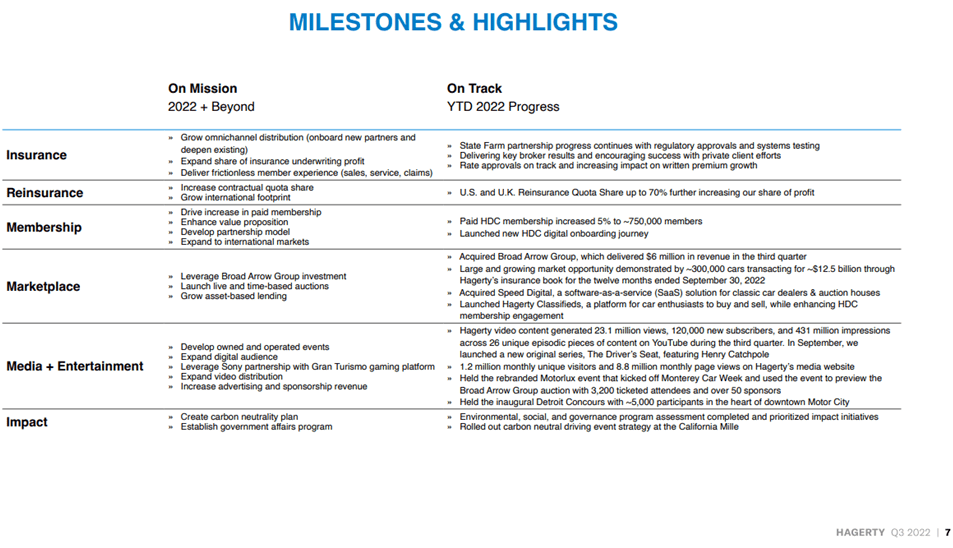

Hagerty considers its customers “members” who share - with management and employees - a deep enthusiasm for classic and collectible cars. The opening slide in the 2021 IPO Investor Presentation illustrates the favorite cars owned by CEO Hagerty (1967 Porsche 911 S), then-CFO Turcotte (2021 C8 Corvette) and board member Kauffman (1931 Bugatti Type 51). Per the 3Q 2022 10Q , here is how management described its progress in building out the “automotive enthusiast platform that engages, entertains and connects with car enthusiasts and its members.”

Hagerty 3Q 2022 Investor Presentation

{kind=link}

As the slide above indicates, management has had the “pedal to the metal” – forging strategic partnerships, making tuck-in acquisitions and allocating capital across every business segment.

As of the completion of the State Farm deal, for example, Hagerty maintained strategic partnerships or alliances with all ten of the largest U.S auto insurers.

In April 2022 Hagerty acquired Speed Digital, a “software as a service” provider serving collector car dealers and auction houses and an advertising and content syndication platform, for $15.0 million. Investors should note that Speed Digital was owned by Hagerty director and former Aldel CEO Robert Kauffman who, per the 3Q 2022 10Q , received “100% of the proceeds of the purchase price.” Hagerty had previously acquired 40% of collector car auction house Broad Arrow for $15.3 million and acquired the remaining 60% for $73.3 million in stock in August 2022.

Financial Results: Stuck in First Gear

Hagerty’s results for 2021 and 2022 are generally comparable as Hagerty is the surviving entity for accounting purposes, but the rapid-fire corporate development initiatives in the roughly 11 months since the SPAC IPO have not allowed the financial statements to stabilize.

Several more quarters will be required to gauge whether management’s plans will translate into the stable and growing earnings of similar but larger insurance agencies/brokers; Marsh & McLennan (MMC), Arthur J. Gallagher (AJG) and Brown & Brown (BRO). As of the date of this article, although Hagerty’s revenue growth has been impressive, the company’s expense growth has been even more impressive. As a result, investors have not been impressed.

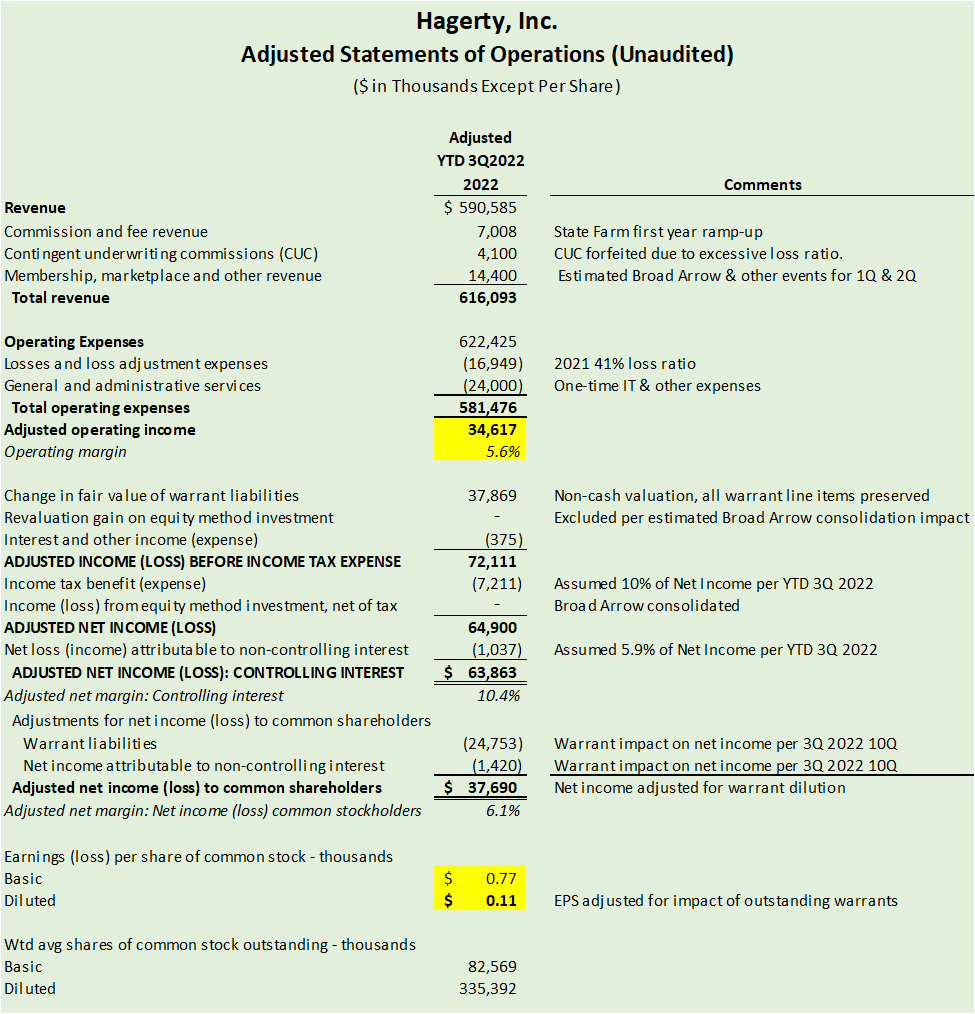

We’re going to take a critical look at the YTD 3Q2022 results presented below.

{kind=link}

Revenue

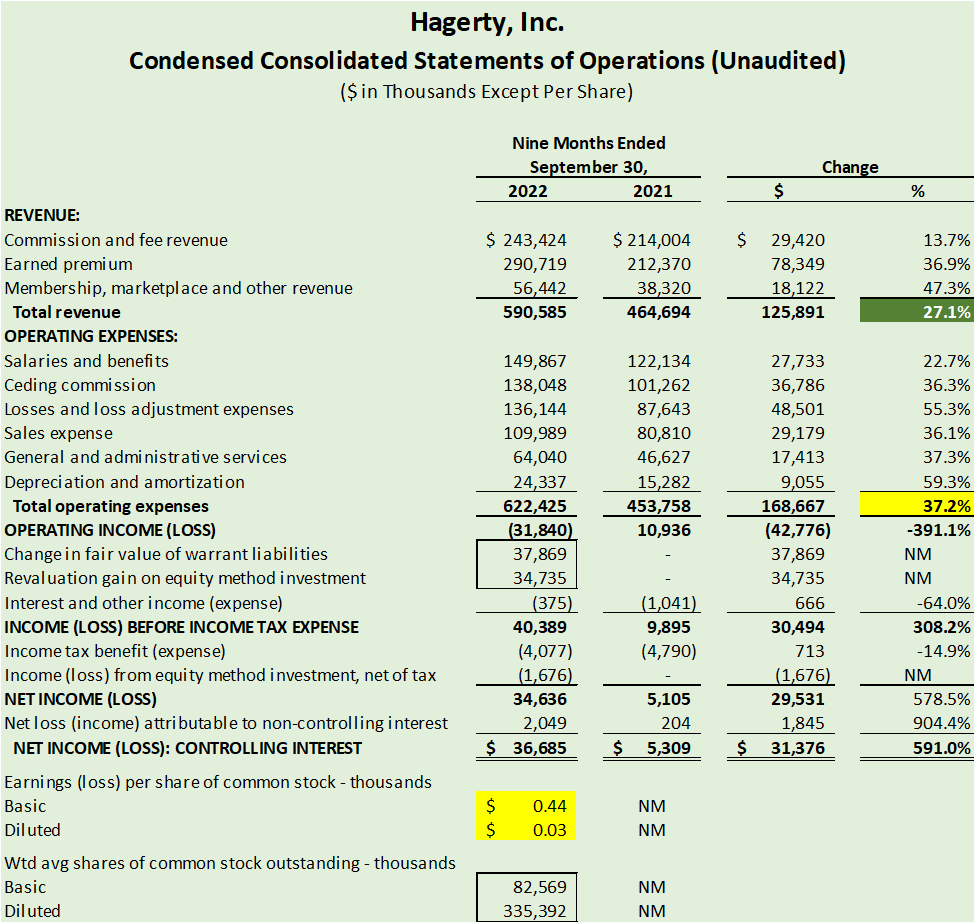

It’s early in Hagerty’s metamorphosis into an “automotive enthusiast platform;” 90% of the company’s revenue is still derived from insurance products. Any insurance executive, however, would be thrilled with YTD 3Q 2022 revenue growth of 27.1% - highlighted above in dark green. Hagerty’s total revenue increased $125.9 million to $590.6 million YTD 3Q 2022 from $464.7 million in 2021. Unfortunately, operating expenses increased $168.7 million or 37.2% - highlighted in yellow - to $622.4 million from $453.8 million over the same period, driving a $31.8 million loss from operations. Cash from operations has followed a steadier course; increasing $8.5 million or 9.6% to $93.5 million YTD 3Q 2022 from $85.5 million in 2021.

The executive team is aware of the need for better expense management. According to new CFO McClymont during the 3Q 2022 Investor Conference Call :

As a newly arrived CFO, one area I believe we can improve is our expense management and prioritization of resources. You can see this in our year-to-date results, where expense growth outpaced our top line. Much of this is due to the heightened investment in technology to support large-scale partnerships such as State Farm and the rollout of Marketplace. Some is due to our decision to go public, which comes with considerable new costs.

Additionally, we've added people to support growth in our traditional insurance and membership businesses and also in new areas such as events and Marketplace. It is imperative that we not just deliver the revenue growth we anticipated but carefully manage our costs so we can achieve profitability and positive cash generation in short order.

Revenue is not the problem. Earned premium, for example, the largest revenue item in 2022, was up $78.4 million or 36.9% to $290.7 million YTD 3Q 2022 from $212.4 million in 2021. Earned premium is the earned portion of premiums that captive insurance company Hagerty Re has assumed under quota share reinsurance agreements with insurance carrier partners. Hagerty’s insurance carrier partners include Markel in the U.S. (through wholly owned subsidiaries Essentia (underwriting) and Evanston (reinsurance)), Aviva Canada, Inc. in Canada and Markel International Insurance Company Ltd in the U.K. The increase in earned premium was driven by 15.0% written premium growth, 88.0% policy retention and an increase the U.S. contractual reinsurance quota share to 70% from 60% - which also increased ceding commission, the associated expense.

Commission and fee revenue, the second largest revenue item in 2022, was up 13.7% or $29.4 million to $243.4 million YTD 3Q 2022 from $214.0 million in 2021, about in line with the 15% written premium increase. Commissions from policy renewals made up 84% of the increase. The increase was split between $16.8 million from agents and $12.6 million from Hagerty direct sales. As State Farm’s 19,000 agents begin to sell Hagerty products in State Farm Classic + wrappers in 2023, the amount attributable to agent sources can be expected to increase.

As a final word on revenue from policies, a concern is that the number of new policies written (“new business count” per Hagerty) actually declined 5,892 or 3.1% to 190,997 YTD 3Q 2022 from 196,889 in 2021. Per the 3Q 2022 10Q , management views an increase in the number of new policies as “critical to achieving our growth objectives.” This trend only moderated slightly in 3Q 2022 as new business count barely increased by 484 or 0.7% to 68,561 over 68,077 in 2021. Price increases of 16% for new business policy premiums are driving the revenue contribution from new business written. Hagerty’s investments have yet to yield a significant number of new “members” for the core insurance business.

Membership, marketplace and other revenue, however, illustrates the traction Hagerty is beginning to achieve with its ancillary businesses. This category increased $18.1 million or 47.3% over the prior period, fueled by a strong 3Q 2022 which featured a $10.6 million or 80.4% increase consisting of $6.9 million in auction revenue from the newly consolidated Broad Arrow ($6.0 million from the Motorlux/Broad Arrow Auction in Monterrey, CA) and $2.1 million in sponsorship and admission income from recently acquired car shows and events.

Hagerty, Inc. Motorlux/Broad Arrow Auction Website

{kind=link}

Operating Expenses

The 37.2% increase in operating expenses was led by a $48.5 million or 55.3% increase in losses and loss adjustment expenses to $136.1 million YTD 3Q 2022 from $87.6 million in 2021. Losses are estimates of the company’s share under reinsurance agreements of claims paid, reserves, etc. net of estimated recoveries. Loss adjustment expenses are the costs of investigating and settling claims. The bulk of the increase in YTD 3Q 2022 losses and loss adjustment expenses is attributable to $60.6 million reported for 3Q 2022, an increase of $28.3 million or 87.6% over 2021.

Hurricane Ian made landfall in Florida on September 28, traversed the state to the Atlantic Ocean, then again made landfall on September 30 in South Carolina, placing most of the insured losses in Hagerty’s third quarter. Carfax estimated that the hurricane damaged at least 358,000 vehicles. Hagerty’s relatively small loss from an area known for classic and exotic car collections is indicative of effective risk management on the part of both the company and its customers. The storm was directly responsible for $10.0 million in claims paid and a required $6.5 million increase in U.S. auto liability reserves in the quarter. The loss ratio, including Hurricane Ian losses, was 56.4% 3Q 2022 compared to 41.0% in 2021. Excluding Hurricane Ian the loss ratio was still considerably higher at 47.1% for 3Q 2022 – still quite good compared to other auto insurers.

A very low loss ratio (losses plus adjustment expenses / net premiums written) remains a Hagerty strength. For 2021, per S&P Global the top ten auto insurers in the U.S. averaged a loss ratio of 66.09% with three companies, including State Farm, exceeding 72%. Hagerty’s loss ratio only was 46.8% - and management considered that high - and 41.3% for 3Q 2022 and 2021, respectively. Excluding the impact of Hurricane Ian the loss ratio was 43.4% YTD 3Q 2022. Hagerty’s loss ratio is lower than the typical auto insurer as most classic vehicles are garaged, well-maintained and driven only occasionally for short distances.

The second largest single increase in operating expenses was the $36.8 million or 36.3% increase in ceding commission to $138.0 million YTD 3Q 2022 from $101.3 million in 2021. $24.1 million of the increase in ceding commission was primarily due to an increase in Hagerty Re’s quota share of premiums from 60% in 2021 to 70% in 2022. An additional $9.9 million was accounted for by higher U.S. premium volume ceded to Hagerty Re from Markel’s Evanston subsidiary.

Ordinarily, based on the huge increases in operating expenses, every item of operating expense would be worthy of in-depth analysis; there were comparable period increases of 22.7% in salaries and benefits, 36.1% in sales expense and 37.3% in general and administrative expenses. Depreciation and amortization increased 59.3%.

Let’s deal with each line item briefly:

- Salaries and benefits increased as headcount rose to support strategic partnerships, continuing IT development and acquisitions.

- Sales expense increased as a result of a $19.3 million increase in travel and promotion costs from newly acquired events, increased advertising and $5.9 million in broker expenses to increase policies acquired through agents.

- General and administrative expenses rose primarily due to an $8.9 million increase public-company operating expenses, a $2.2 million increase in software subscription licenses and a $1.9 million increase in web-related consulting services.

- Depreciation and amortization increased as a result of $6.0 million in new depreciation from the company’s “digital platform development investment.”

Non-Cash Valuation Items

Just below operating income in the YTD 3Q 2022 column, I enclosed the $37.8 million change in fair value of warrant liabilities and the $34.7 million revaluation gain on equity method investment in a small box. I think investors should ignore these non-cash valuation numbers – and Hagerty’s $36.7 million reported net income YTD 3Q 2022 depended totally on these amounts.

Warrant liabilities declined primarily because Hagerty’s stock price remained below the $11.50 per share strike price shared by most of the company’s warrants. Until expiration or exercise prior to December 2026, their fluctuating estimated value will be reported in the income statement. The revaluation gain on equity method investment is a non-cash accounting oddity. Hagerty owned a $34.7 million or 40% equity method interest in Broad Arrow. During 3Q 2022 the company bought the remaining 60% - and the original 40% was re-valued to reflect Hagerty’s purchase price for the remainder per the GAAP treatment of step acquisitions.

Dilution: Common Stock & Warrants

Investors should note the weighted average shares outstanding in the second box highlighting the potential massive dilution of existing shareholders from the Class V shares and outstanding warrants. It is possible that an undetermined number of warrants will expire worthless, but per the “ Lock-Up Agreement ,” the Class V shares are currently free to convert. As a result, investors should rely solely on diluted EPS if analyzing per share earnings.

A Pro Forma Look Under the Hood

What can investors reasonably expect from Hagerty’s earnings? I estimated pro forma “normalized” YTD 3Q 2022 operating income and EPS by modifying a few items. Beginning with YTD 3Q 2022 revenue, I estimated the additional revenue from Broad Arrow auctions and other events – which only hit 3Q 2022 actual – at $14.4 million including a 20% reduction to account for event seasonality. I also gave Hagerty credit for $4.1 million in contingent underwriting commissions forfeited due to elevated loss ratios resulting from Hurricane Ian. Finally, I estimated 2023 revenue from the State Farm deal as 20% adoption of the State Farm Classic + policy at Hagerty’s midpoint estimated revenue of $97.50 per customer.

For operating expenses, I assumed a return to a normal 41% loss ratio - a $16.9 million addition - and that $24.0 million of expenses were one-time, or per Slide 10 of the Hagerty 3Q2022 Investor Presentation , “substantial pre-revenue costs related to scaling infrastructure, legacy systems and newly-developed digital platforms, human resources and occupancy to accommodate our alliance with State Farm and other potential distribution partnerships as well as to further develop our Marketplace transactional platform.” This is generous, as CEO Hagerty, in this presentation , suggested that these costs might actually be recuring annual expenses.

After all these positive changes, estimated adjusted operating income - highlighted in yellow - was $34.6 million for the pro forma three quarters, equivalent to a 5.6% operating margin.

As we’ve seen, Hagerty’s YTD 3Q 2022 $36.7 million net income depends totally on two non-cash valuation items, but Hagerty is generating cash. Cash from operations increased $8.2 million or 9.6% to YTD 3Q 2022 $93.5 million from $85.5 million in 2021. I decided to eliminate the equity method re-valuation as I am treating the pro forma as if Broad Arrow was consolidated for all three quarters. With some other minor adjustments, the changes to this point produced adjusted net income for the controlling interest of $63.8 million – the amount used for calculating basic EPS – and a 10.4% adjusted net margin for the controlling interest. Pro forma adjusted basic EPS was $0.77 – an annualized $0.93 and a very reasonable 10.3 PE at $9.62 per share on February 10, 2023, but this was a SPAC deal, and the diluted EPS is another matter.

Hagerty 3Q 2022 Form 10Q, Herding Value Analysis

{kind=link}

Adjusted EPS suffers from extremely heavy dilution that drives basic shares from 82 million to an incredible 335 million. Accordingly, in spite of all the positive adjustments to “normalize” Hagerty’s reported earnings, adjusted YTD 3Q 2022 net income available to common stockholders was just $37.7 million - $50.2 million annualized, corresponding to a net margin of only 6.1%, and adjusted diluted net income available to common stockholders – adjusted diluted EPS – of only $0.11 per share. Annualized that’s $0.15 per share or an adjusted PE of 64.

Two observations merit consideration:

- In my pro forma Hagerty returned to its pre-SPAC profitability. Quoting CFO McClymont during the 3Q 2022 Investor Conference Call , “For historical context, our EBITDA margins from 2012 to 2017 exceeded 10%.” Pro forma adjusted EBITDA was an annualized $85.4 million, equivalent to an adjusted EBITDA margin of 10.4%.

- The huge overhang of common stock and warrants issued in connection with the SPAC IPO presents an incredible source of dilution that can potentially wreak havoc on investors in Hagerty common stock.

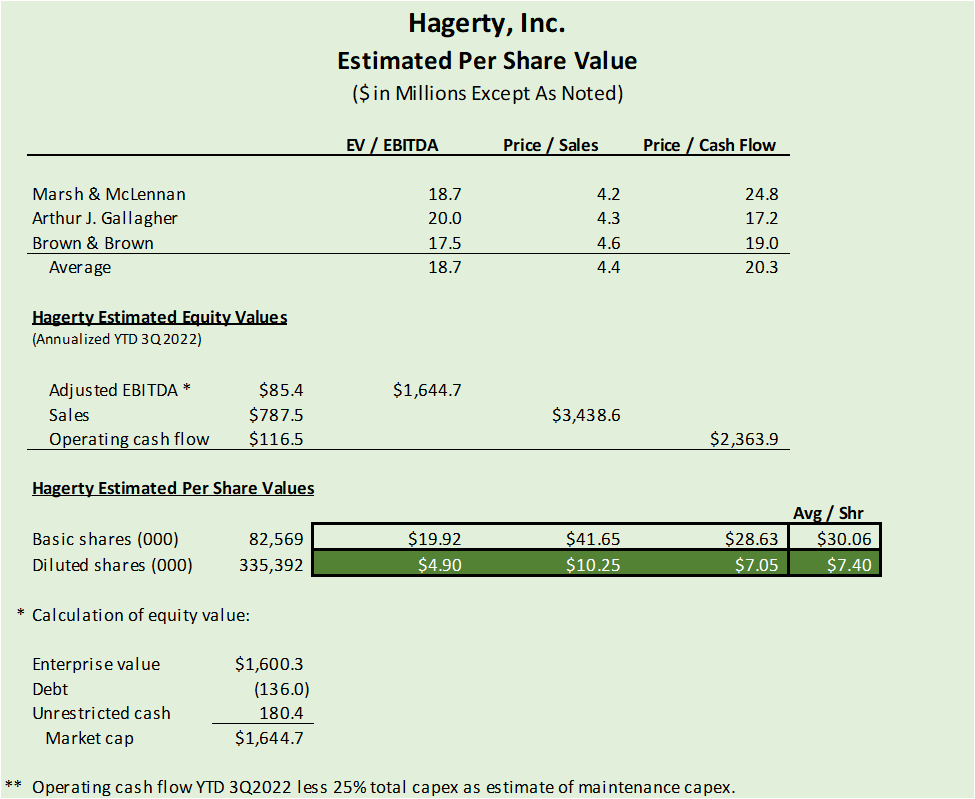

Valuation

As of February 10, 2023, investors were willing to pay $9.62 per share for Hagerty common and $2.91 for the few warrants that traded hands. The implied market cap is about $3.2 billion, not far off the pro forma $3.13 billion on December 2, 2021.

It's obvious that no one is valuing Hagerty based on GAAP earnings or EPS. The schedule below presents three alternate ways to derive a value for Hagerty per diluted share.

Seeking Alpha, Herding Value Analysis

{kind=link}

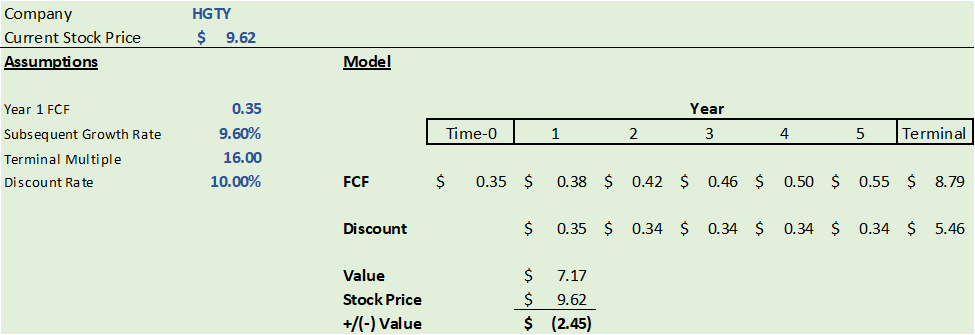

The results vary widely, but the price to cash flow result of $7.05 per diluted share is intuitively appealing as it is based on the ability of the company to generate cash flow and requires minimal manipulation of reported earnings. Let’s check to see if we can validate it with my “quick and dirty” DCF model:

Seeking Alpha, S&P, Herding Value Analysis

{kind=link}

I derived the free cash flow per share as annualized YTD 3Q 2022 operating cash flow less 25% of capex as an estimate of maintenance capex. The 9.6% cash flow growth rate is the percentage change in operating cash flow between YTD 3Q 2022 and 2021. The 16x terminal multiple is the long-term PE of the market per S&P. The 10% discount rate is my personal hurdle rate for stock investments. The result, again cash flow-based, is also intuitively appealing at $7.17 per share.

Conclusion

As a car enthusiast, I was hoping to discover an undervalued “barn find” in Hagerty, a company whose products I respect, but instead found a daily driver undergoing restoration. Stripped to bare metal, Hagerty is an insurance agency serving a niche market with a captive reinsurance company and some ancillary related businesses. Management deserves credit for its efforts to differentiate the company from competitors like Heacock, Grundy and American Collectors through its “automotive enthusiast platform,” but the road to GAAP profitability has been bumpy.

There are many positives, but there also some concerns:

- Investors confront extreme dilution.

- Limited public-company operating history reduces the accuracy of financial projections.

- There is no dividend.

- Hagerty is closely-held; investors are de facto passengers along for the ride:

- Speed Digital; owned by board member and SPAC CEO Kauffman, was acquired for $15.0 million in cash.

- Insiders retained control post-IPO with 52.8% ownership plus almost $490.0 million while the company only received $258.1 million.

While prices around $7.00 per share are intuitively appealing, I won’t invest at this time. I am looking for a) the company’s operations and financial statements to stabilize and b) a substantial reduction in the uncertainty regarding the potential common stock and warrant dilution before I consider an investment - and so should you.

For further details see:

Hagerty: Stuck In First Gear