HARP - Harpoon Therapeutics: A Well Undervalued Tri-Specific Oncology Player

Summary

- Harpoon Therapeutics is an oncology platform play developing tri-specific drug candidates.

- The company’s lead candidates HPN217 and HPN328 are in Phase 1/2 trials and have so far shown efficacy without compromising safety.

- HPN217’s main takeaway is its AbbVie backing in multiple myeloma, whereas HPN328’s target in solid tumors builds on the history of a failed $5.8 billion AbbVie acquisition.

- With a $57 million market cap and $90 million cash in hand, Harpoon Therapeutics is a bargain, and downside risk is limited.

- If AbbVie uses its option to further develop HP217, Harpoon will receive $200 million at once.

Thesis

Harpoon Therapeutics ( HARP ) has three drug candidate-generating platforms and two leading drug candidates, HPN536 and HPN328. After somewhat disappointing results of HPN424, the March 2022 development termination of this former lead drug candidate led to a sell-off that has Harpoon Therapeutics now selling at a very cheap price. The company trades at about a 35% discount to its cash value. That cash value may well grow with another $200 million or more in the coming months, if AbbVie ( ABBV ) would exercise its option to further develop HPN328 or other drug candidates.

HPN536 and HPN328 maintain activity even when tumors are expressing lower levels of antigens, and are independent of MHC expression. The latter is important as lack of MHC expression is a typical immune-evading characteristic of tumors. They furthermore allow for once-weekly dosing instead of continuous IV-infusion.

With the T-cell engager field looked at as promising, and a recent competitor $1.3 billion buyout by AstraZeneca , Harpoon is a strong buy for me at this time. Harpoon has two lead drug candidates that have shown efficacy in heavily pretreated patients, a long half-life, and avoidance of cancer immune-evasion. Even without the financial backing by AbbVie, Harpoon has enough cash to continue operations well into 2023. Downside risk is hence limited.

Interim date for drug candidate HPN217 in multiple myeloma is slated for the coming months. Data for HPN328 will follow in the first half of 2023.

The risk/reward ratio is currently very favorably skewed to the upside. Institutions and Wall Street analysts are seeing that. It is hard to imagine the stock facing much further downside over a sustained period of time at this point.

Company

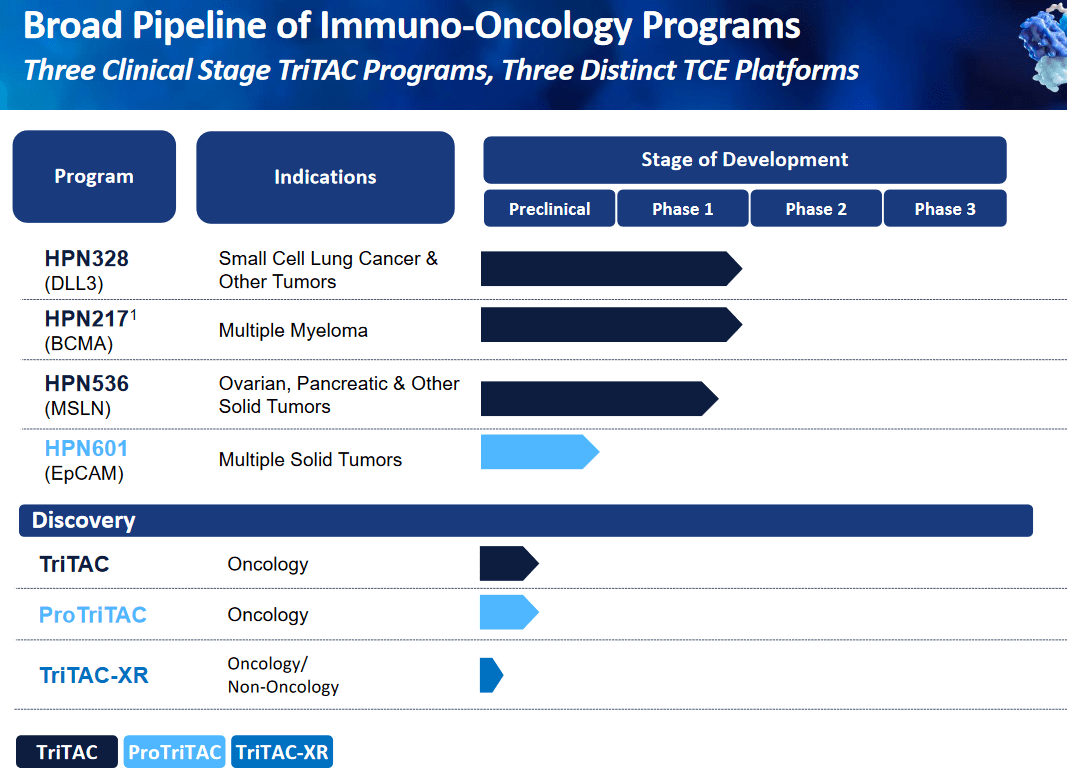

Pipeline

Harpoon has the following pipeline, with HPN328 targeting DLL3 in small cell lung cancer and other tumors, and HPN217 targeting BCMA in multiple myeloma as primary drug candidates. The company wants to find a partner for HPN536 and the rest of its drug candidates are in preclinical development.

{kind=link}

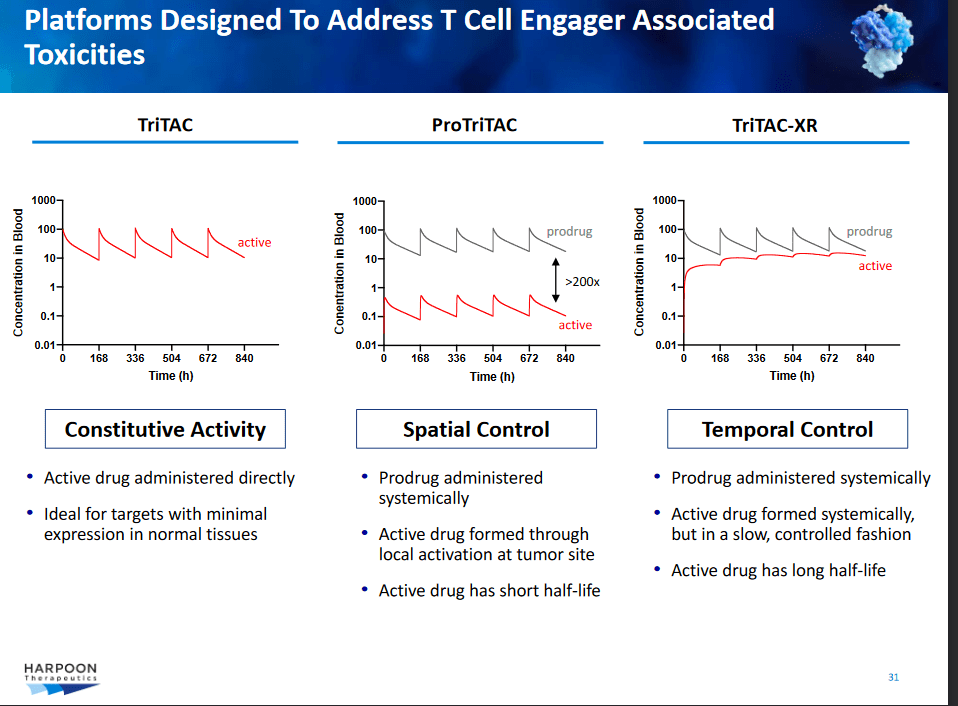

Harpoon's drug candidates are built around three Tri-specific T-cell Activating Constructs (TriTAC) platforms that may generate a number of drug candidates: TriTAC, ProTriTAC and TriTAC-XR. All of these platforms generate tri-specific T-cell engagers, meaning the drug candidate binds to a target on a killer T-cell as well as to a target on a tumor cell, to direct T-cells to engage in otherwise neglected tumor-killing, and to another target. So far, that third target, human serum albumin, allowing for extended stability, maintained efficacy and less frequent dosing instead of continuous administration. The different platforms aim to improve efficacy, half life and safety compared to approved bi-specific T-cell engagers. The ProTriTAC platform add a prodrug aspect which I have also covered in my coverage of NuCana ( NCNA ), with the goal of achieving more direct drug delivery paired with further reduced toxicity. The TriTAC-XR platform efforts to maintain efficacy while significantly lowering cytokine release.

Both TriTAC drug candidates HPN217 and HPN 328 have shown tumor-killing both in hematological as well as solid tumors. This is actually major. Immunotherapy candidates have not shown good results in solid tumors indications so far, and there is a strong desire for the immunotherapy field to expand to those indications. However, solid tumor efficacy is hampered by conditions related to the tumor micro-environment, making it hard for T-cell-based immunotherapies to show efficacy and durability without compromising safety. The solid tumor market is huge compared to the hematological tumor market, and good results here will be noticed by big pharma and the scientific field. In the oncology field, having been knocked down the worst within the biotech realm over the past months, this is the kind of opportunity that I do not want to let pass. Previous Seeking Alpha author Biologics already gave Harpoon Therapeutics a Buy rating two months ago, adding it to his BioBoom portfolio. With the share price having fallen another 25% since, I am rating it a Strong Buy at this point.

Insofar as reported, Harpoon's drug candidates HP328 and HP217 are still in a dose-expanding trial regimen, without the maximum dose having been found.

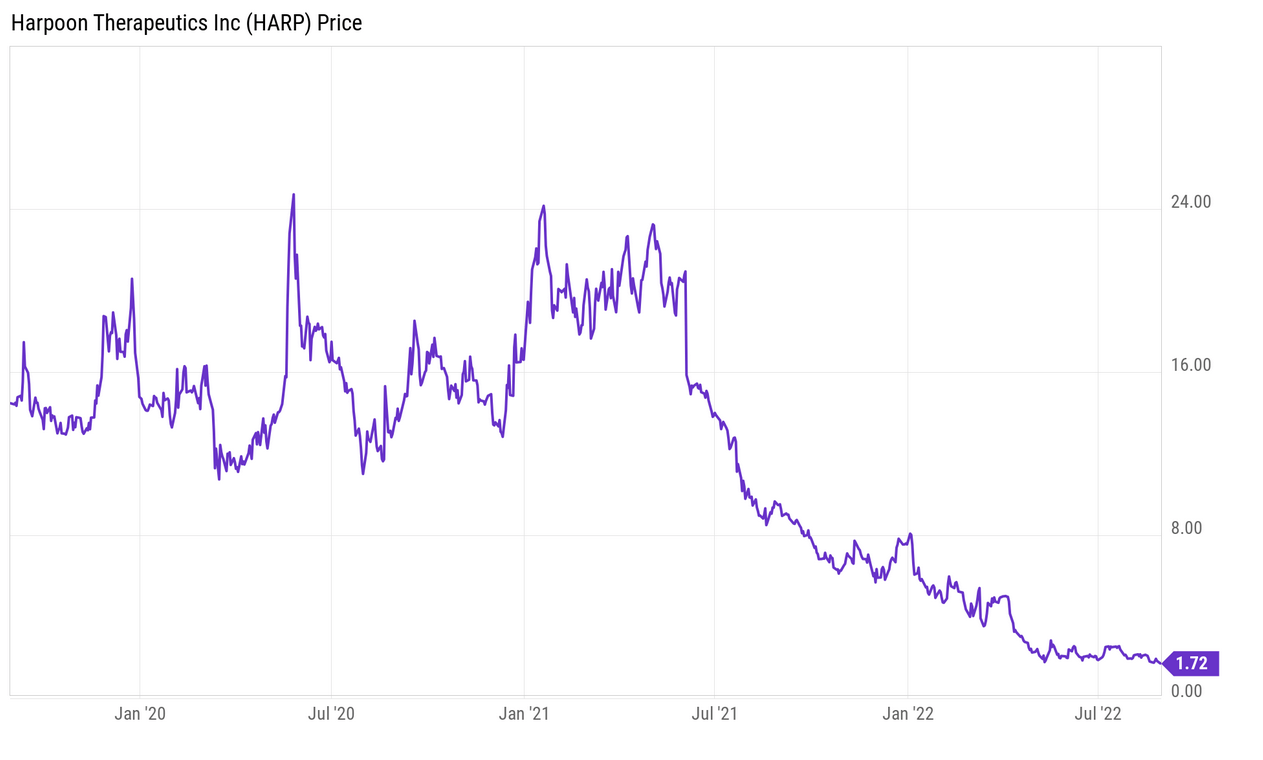

Share price

This is Harpoon Therapeutics' share price over the past three years. The stock took a cliff-dive on June 4, 2021, after the company had released suboptimal data on its HPN424 drug candidate. The stock continued to sell off during the biotech bear market, where even a well-received update on HPN217 on December 11, 2021 has not been able to change the downward price trajectory. Updates on preclinical developments , fast track designation and orphan drug for HPN217 and HPN328 respectively were disregarded by the market. Harpoon finally announcing the termination of HPN424 on March 10, 2022 made the price shake, and a leadership change announced on April 7, 2022 dealt it its final blow from $4.98 to $1.72 where it sits now.

{kind=link}

The article below will focus on the lead drug candidates at this point in time, which the market obviously and unduly does not give any credit anymore.

HPN217 for relapsed/refractory multiple myeloma and AbbVie's involvement

Introduction

Harpoon's drug candidate HPN217 targets BCMA, which is expressed in multiple myeloma. In 2022, the FDA has granted this drug candidate fast track designation.

AbbVie has been interested in this drug candidate and other possible drug candidates coming forth from either the TriTAC or ProTriTAC platforms. Parties have signed an option deal in 2016 , with an amendment in 2019 . Under that deal, AbbVie has already paid Harpoon $80 million, and has the right to develop and commercialize the asset against payment of royalties and a further $200 million. There are further milestones, with a total potential of $2.4 billion. Under the original agreement, AbbVie selected two further targets to be developed, and the 2019 restated collaboration agreement allows AbbVie to designate another two targets and to opt to expand that selection with another four targets. Clearly, the market is missing AbbVie's ongoing interest here at this point. AbbVie can exercise its option to exclusively develop HPN2017 any time, but the deadline to do so is unspecified - at a time after a prespecified package of Phase 1/2 trial data has been delivered. As the final readout of the Phase 1/2 trial is likely due some time in 2023 and further data will be due the coming months, the clock is ticking.

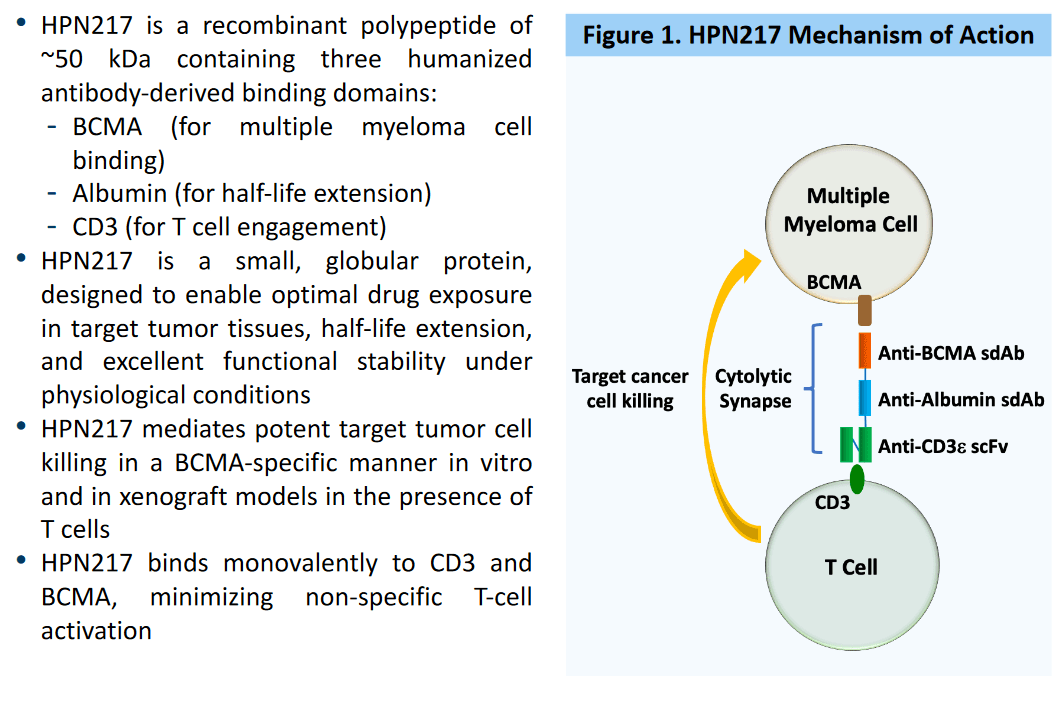

Mechanism of action

This is the mechanism of action of HPN217, with BCMA as the target on the cancer cell, CD3 the target on the T cell, and an anti-HAS antibody as the third part of the TriTAC. BCMA is a popular target, with two approved CAR-T therapies so far, Bristol Myers ( BMY ) Abecma and Janssen's ( JNJ ) Carvykti. These CAR-T therapies have as their downsides their high cost, high toxicity and repeat-dosing issues. HPN217 may be able to solve some of these, with less costs, less toxicity and less problems with frequent dosing.

{kind=link}

The market HPN217 is targeting has about 131,000 patients and 32,000 new cases annually. The 5-year survival rate is about 54%. The relapsed/refractory patient population has an unmet need, and is particularly composed of frail patients facing long-term side effects and tolerability issues.

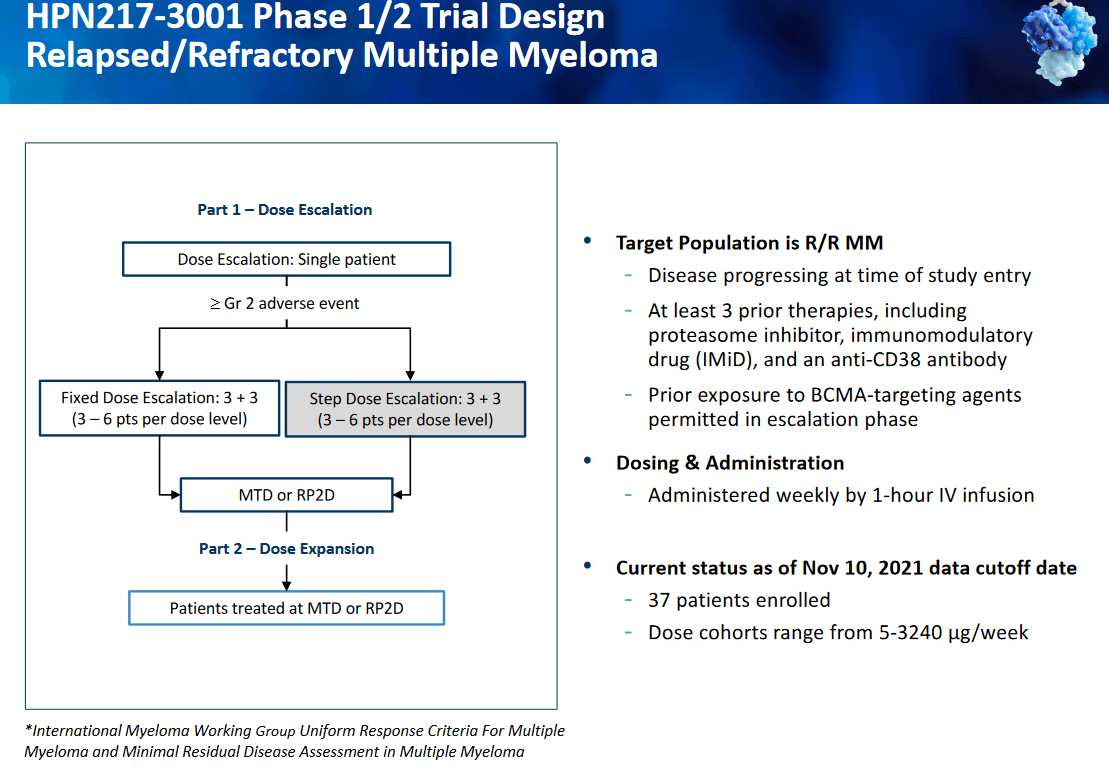

The Phase 1/2 trial so far

This trial has been started in 2018. The dose-escalating Phase 1 and dose-expanding Phase 2 trial design look as follows.

{kind=link}

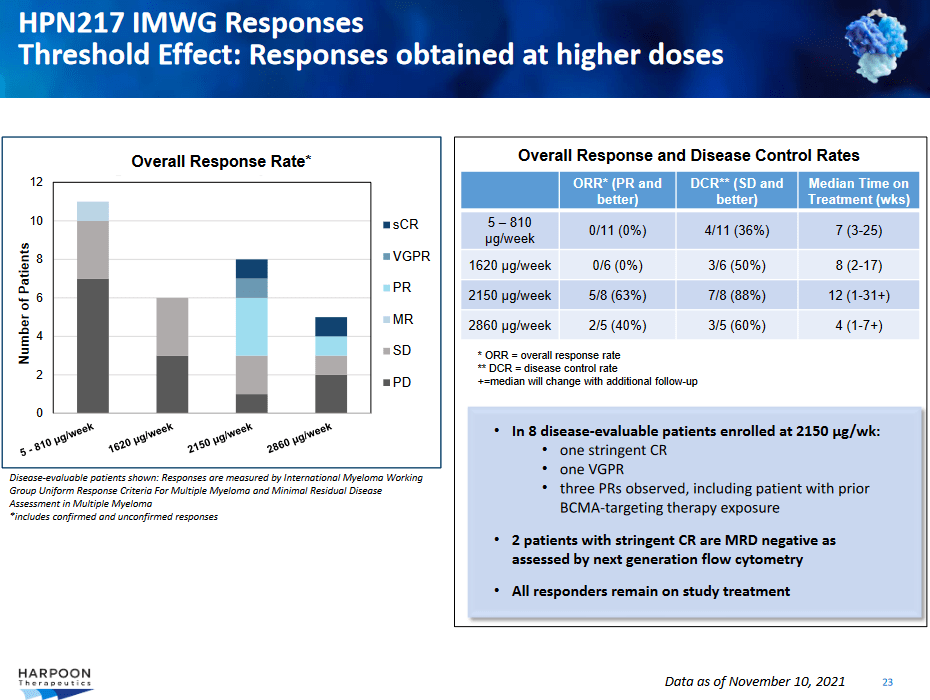

A first update has been provided on December 8, 2020 and a second update on December 11, 2021. At that time, 37 relapsed/refractory patients had been treated in a dose-escalating manner.

As always, in a Phase 1 trial, one treats patients that have no further options anymore, rather than those one wants to treat. In this case, patients were heavily pretreated, with a median of 7 prior treatments, 32% of enrolling patients having progressive disease prior to enrollment, and 24% of patients having already received a BCMA-targeted therapy.

HPN217 has a good safety profile so far. Transient low-grade cytokine release syndrome has been reported in 24% of patients, one grade 4 dose-limiting toxicity, and maximum tolerable dose has not yet been reached.

The higher doses showed clinical benefit. At 2150 µg/week, with 8 evaluable patients treated, an objective response rate of 63% was reported. There was one very good partial response and three partial responses. Disease control rate was 88%, meaning 7 out of 8 patients. At 2860 µg/week, with 5 evaluable patients, the objective response rate was 40% with a disease control rate of 60%. This included a partial response and a stringent complete response. All responders remained on treatment.

{kind=link}

The trial continues its dose escalation phase to find the recommended phase 2 dose, while at the same time exploring the possibility of less frequent dosing.

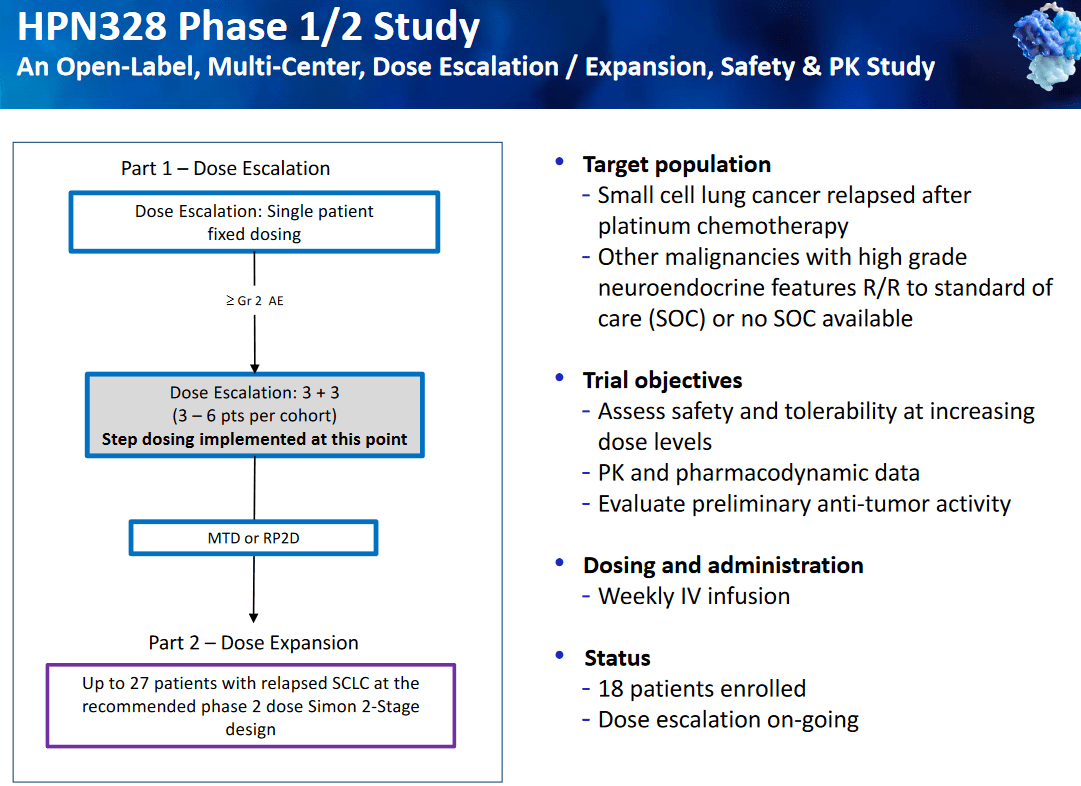

HPN328 for small cell lung cancer and other solid tumors

Introduction

HPN328, for which Harpoon has received Orphan Drug Designation in March 2022, is a drug candidate in a Phase 1/2 trial targeting DLL3 in small-cell lung cancer. DLL3 has been a target of previous drug development by Stemcentrx under the name of Rova-T. In small cell lung cancer, it is expressed by 80% of cells and not by healthy cells. It is expressed in more than 70% of small cell carcinomas. These include not only small cell lung cancer, but also neuroendocrine prostate cancer and other small cell neuroendocrine cancers. AbbVie had bought the rights to Rova-T when it had acquired Stemcentrx for $5.8 billion in 2016, with Rova-T as prime acquisition object. That acquisition story failed miserably, with AbbVie dumping Rova-T in August 2019 after a final failure in a lung cancer trial.

Harpoon is currently testing HPN328 in small cell lung cancer (SCLC), an aggressive and quickly metastasizing tumor accounting for 15% of lung cancers. SCLC belongs to the category of neuroendocrine tumors, originating from neuroendocrine cells which exist in different parts of the body, and as such other cancers can be targeted as well. The small cell lung cancer (SCLC) market HPN328 is targeting consists of about 60,000 new cases annually, with a poor prognosis. Diagnosis is mostly at a stage where disease is extensively present, and surgery options are limited. Patients have a median overall survival duration of 6 to 12 months, with about 6% having a 5-year survival. Most patients relapse in four to six months.

Mechanism of action

This is the drug candidate's mechanism of action, with the same anti-HSA antibody and CD3 as a target on the T-Cell, but DLL3 being the target on the tumor cell.

HPN328 MoA (Corporate Presentation)

The Phase 1/2 trial so far

The Phase 1/2 trial design looks as follows.

{kind=link}

Phase 1/2 trial results so far

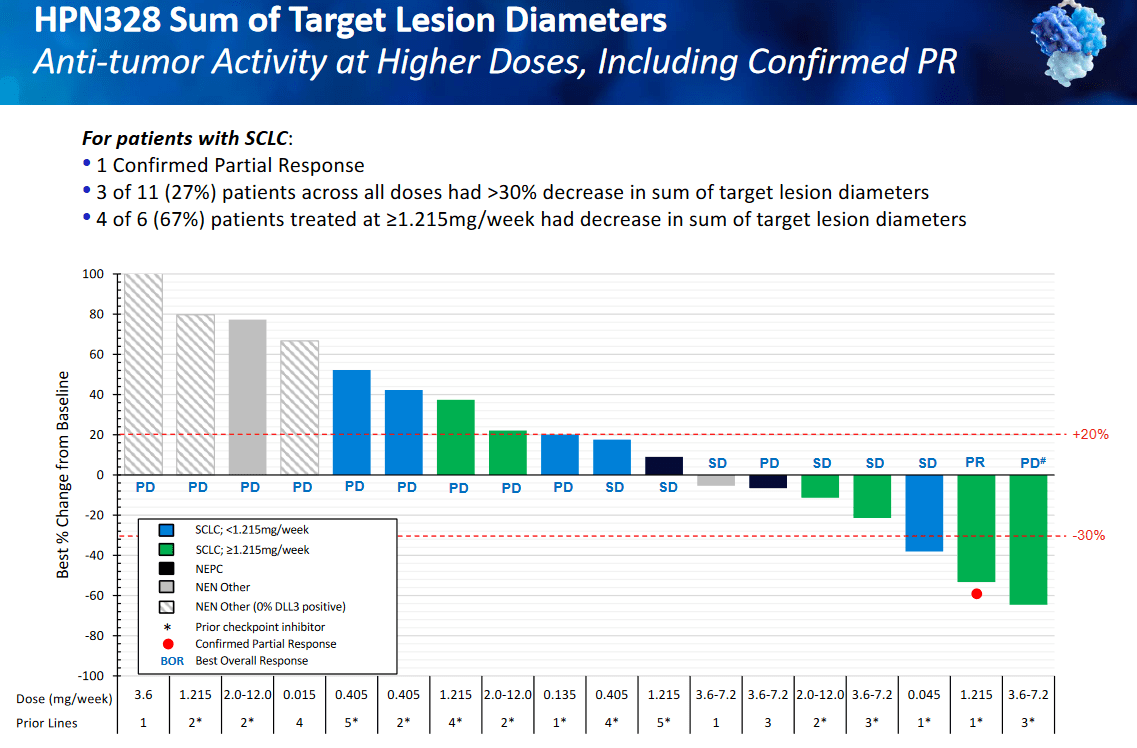

I repeat that in a Phase 1 trial, one treats the patients one has to treat. Phase 1 trials are primarily to assess safety and tolerability, not efficacy. The last update shared at ASCO 2022 showed that the drug had a median half-life of 71 hours and was safe and tolerable. The maximum-tolerated dose had not been reached, and no dose limiting toxicities had been reported. No neurotoxicity issues, and only grade 1 and 2 cytokine release syndrome had been reported, with no patients discontinuing treatment due to adverse events.

Six of 18 patients or 33% had been on treatment for more than 20 weeks, with treatment duration ranging from 4.1 to 41.4 weeks. Anti-tumor activity was shown to be present at higher dosage, with one confirmed partial response with a 53% decrease in sum of target lesions. In total, 39% of patients showed decrease in sum of target lesion diameters, 67% in the higher dosing, and 27% of the treated population showing a decrease of more than 30%. One patient showed a 65% reduction of lesion diameter beyond six months, after three earlier lines of treatment.

HPN328 sum of target lesions overview (Corporate presentation)

{kind=link}

As this is not the first update, and efficacy is clearly showing in the higher doses, deepening of responses over a longer period is well possible, and Harpoon already said that it had seen that in December 2021.

HPN536

HPN536 is a TriTAC drug candidate targeting mesothelin in several solid tumors. HPN536 is not Harpoon's lead drug candidate, and I have covered two promising competing mesothelin-targeting drug candidates in my coverage of TCR2 Therapeutics (TCRR). Harpoon is looking to partner HPN536, which is also in a Phase 1/2 trial in different solid tumors, such as pancreatic cancer, ovarian cancer and mesothelioma.

A total of 94 patients have been enrolled in this trial. HPN536 was well tolerated, and showed promising T-cell engagement. Nonetheless, Harpoon seeks to partner this drug candidate to optimize monotherapy and combination therapy settings.

Further platforms: ProTriTAC and TriTAC-XR

As mentioned above, Harpoon Therapeutics is essentially a platform play with two TriTAC lead drug candidates for the time being. Its ProTriTAC platform is equally promising but earlier stage, with the first ProTriTAC to enter the clinic being HP601 targeting EpCAM. An IND for HPN601 should be filed in the first half of 2023.

A Protidic drug candidate is essentially a prodrug version of a TriTAC, meaning it consists of the same working components, but adds a protease that allows improved efficacy and safety as the drug is delivered closer to where it is supposed to be active.

The Triatic-XR platform, for which Harpoon presented preclinical data in November 2021 and April 2022, pharmacodynamic effects similar to a TriTAC with significantly lower cytokine release, which should allow for more frequent dosing and essentially better efficacy.

{kind=link}

Financials

As of June 30, 2022, Harpoon had about $90M in cash and cash equivalents and no debt, which it alleges should allow ongoing operations into the second half of 2023. It had reported -$20.3 million net income and -$25.2 million cash from operations.

Ownership interests

There are 33.11 million shares outstanding, and the float is 17.99 million shares.

With 74% of Harpoon's shares held by institutions and 7.6% held by insiders, I would say institutions are well aware of the potential here.

Short interest stands at 2.46% of the float, with about 6 days to cover at the current average volume.

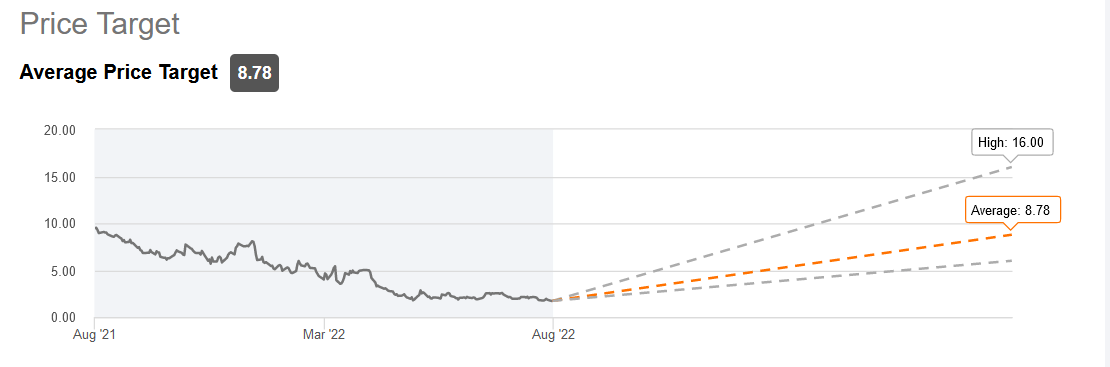

Analysts

The average analyst price target is $8.78, which shows an upside of about 500%, and that is based on information that is out there for a while at this point.

{kind=link}

For HPN217, the relapsed/refractory multiple myelome market that drug candidate is targeting has about 131,000 patients and 32,000 new cases annually. The multiple myeloma market has two recently approved CAR-T players, Bristol Myers' Abecma and J&J's Carvykti that was approved in February 2022. Estimated peak drug sales of the latter were expected to surpass $5 billion.

For HPN328, the SCLC market that drug candidate is targeting at this time consists of about 60,000 new cases annually. The small cell lung cancer market is expanding at a compounded annual growth rate of 19.4% per year, and is expected to be worth $3.4 billion in 2027. Further cancer indications expressing DLL3 can be added in case of success.

I believe that gives an idea of the level of undervaluation of this company.

Risks

Investing in biotech companies, particularly in market-uncertain times like these, can show to be volatile. Specific to Harpoon, risks are regulatory uncertainty and competition coming from the immunotherapy field, whether it be from CAR-T or CAR-NK constructs, T-cell infiltrating lymphocytes other T cell engagers, etcetera. One of these competitors is Amgen's ( AMGN ) tarlatamab targeting DLL3. The most recent update on tarlatamab of August 8, 2022, shows an objective response rate of 23%, with 31% of patients experiencing grade 3 or higher treatment-related adverse events, and 4% patients discontinuing treatment due to adverse events. The SCLC market is already larger, and could be expanded to further cancers expressing DLL3. Apart from Amgen's tarlatamab mentioned above, Allogene (ALLO) also has a preclinical immunotherapy candidate targeting DLL3 that could compete with HPN328.

Conclusion

Harpoon Therapeutics is first and foremost a platform oncology company, with TriTAC drug candidates in clinical trials, and ProTriTAC and TriTAC-XR drug candidates in preclinical development.

Lead drug candidates HPN217 and HPN328 do what they're supposed to, respectively in multiple myeloma as in small cell lung cancer. They have a favorable safety profile and show efficacy in heavily pretreated patients. For HPN217, there is the important AbbVie backing which may lead to AbbVie opting to develop the drug candidate in the coming months or year. The option expires at a given time point, after a predefined set of data from the Phase 1/2 trials has been reported. AbbVie opting in would lead to Harpoon Therapeutics' cash position tripling, with additional milestone payments and royalties further down the road.

As for HPN328, that drug candidate builds on a $5.1 billion AbbVie drug failure in solid tumors, targeting DLL3.

Both drug candidates have been shown to be sufficiently safe, and show good signs of efficacy with higher efficacy in higher dosing, even in heavily pretreated individuals.

After somewhat disappointing results over the past year, the sell-off of Harpoon Therapeutics' stock has it now trading at about a 35% discount to its cash value. The analysts' current average price target shows a +500% upside.

T cell engagers are being included in the pipelines of big pharma companies. The recent $1.3 billion buyout of TeneoTwo by AstraZeneca ( AZN ) underscores that. Harpoon Therapeutics is a leader in the field, and has sufficient cash to deliver on key catalysts in the coming months and in 2023.

At the current price, I see a lot of upside and little downside to this stock. Harpoon Therapeutics is a strong buy for me at this time, and I am thanking the bears for having harpooned this company's stock to the bottom of the investment ocean.

For further details see:

Harpoon Therapeutics: A Well Undervalued Tri-Specific Oncology Player