REIT - Hawks Still In Control

2023-07-09 09:00:00 ET

Summary

- U.S. equity markets slumped this past week while benchmark interest rates climbed towards the highest levels of 2023 after employment data showed enough labor market resilience to keep the "hawks" in control.

- After an end-of-quarter rally lifted the benchmark to its highest levels since April 2022 last week, the S&P 500 slipped 1.1% in the Independence Day-shortened trading week.

- Real estate equities were among the leaders for a second straight week, as the surge in benchmark interest rates wasn't enough to curb the sector's positive end-of-quarter momentum.

- While evidence of cooling inflationary pressures has become increasingly visible over the past several months, labor markets have yet to show the material softness needed to derail the Fed's adherence to its hawkish messaging and restrictive policy course.

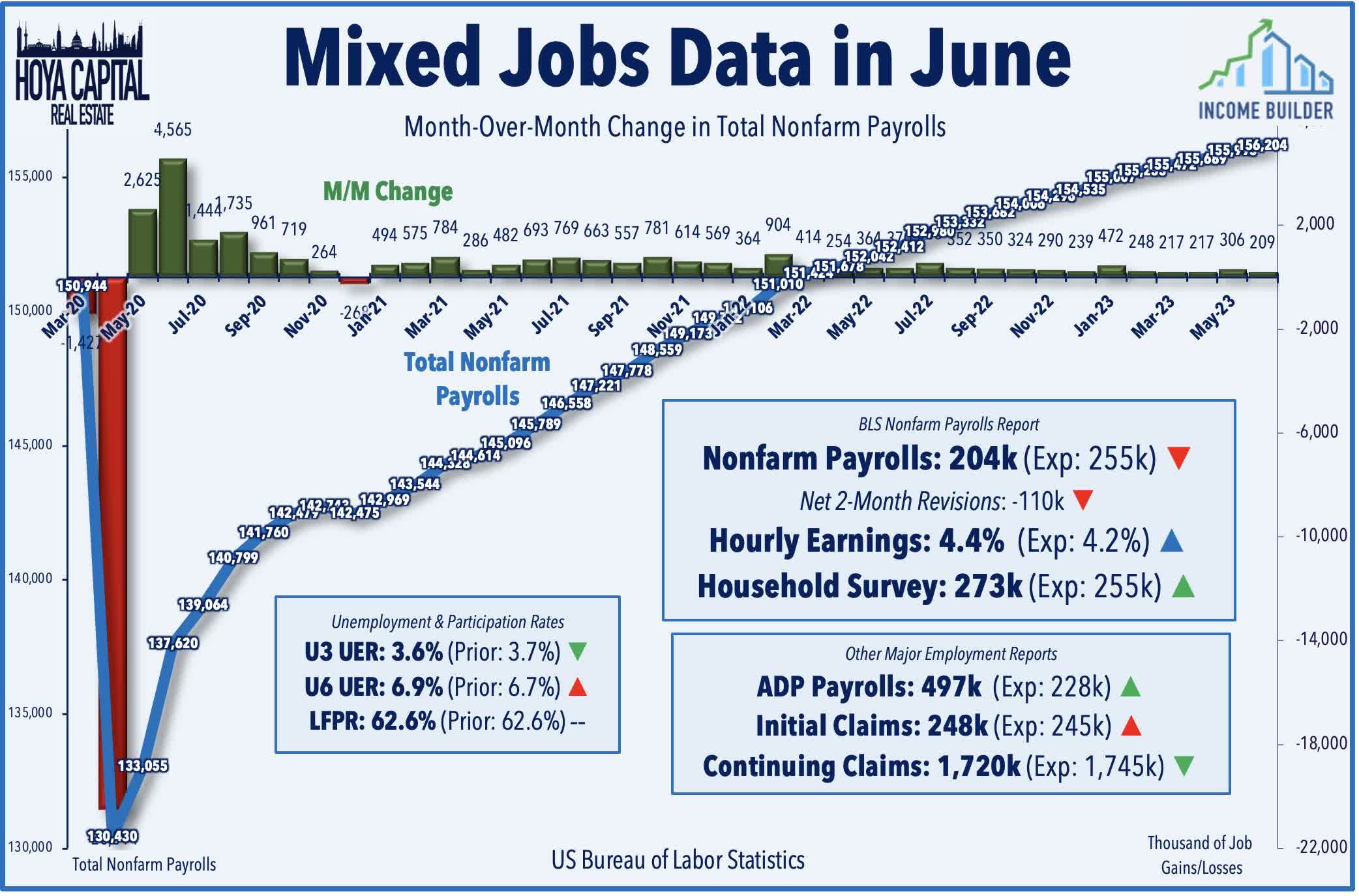

- The critical BLS nonfarm payrolls report showed that the U.S. economy added 209k jobs in June - the weakest month of job growth since December 2020 - which contrasted with relative strength seen across the other major employment reports this week.

Real Estate Weekly Outlook

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on July 8th.

U.S. equity markets slumped this past week while benchmark interest rates climbed toward the highest levels of 2023 after a busy slate of employment data provided enough evidence of labor market resilience for the Federal Reserve to continue their historically-aggressive tightening cycle. While evidence of cooling inflationary pressures has become increasingly evident over the past several months - and even more so this week - labor markets have yet to show the material softness needed to derail the Fed's adherence to its hawkish messaging and restrictive policy course.

{kind=link}

After an end-of-quarter rally lifted the benchmark to its highest levels since April 2022 last week, the S&P 500 slipped 1.1% in the Independence Day-shortened trading week. The other major equity benchmarks - the Mid-Cap 400 and Small-Cap 600 posted similar declines of around 1%, as did the tech-heavy Nasdaq 100 . Real estate equities were among the leaders for a second-straight week, as the surge in benchmark interest rates wasn't enough to curb the sector's positive end-of-quarter momentum. The Equity REIT Index finished higher by 0.2% on the week, with 10-of-18 property sectors in positive territory, but the Mortgage REIT Index fell 1.7%. Homebuilders slumped 5%, however, as mortgage rates rose highest levels of the year.

{kind=link}

Benchmark interest rates resumed their upward trajectory this week as traders parsed a critical slate of employment data along with minutes from the mid-June FOMC meeting in which most officials supported additional rate hikes in the coming months following a "pause" in June. The policy-sensitive 2-Year Yield climbed another 6 basis points this week to 4.96%, while the 10-Year Yield jumped by 23 basis points to close at 4.05% - each at the highest level since early March. Swap markets now imply a nearly 95% probability of a 25 basis point Fed rate hike this month and a nearly 25% chance of a second additional Fed rate hike by year-end. Ten of the eleven GICS equity sectors finished lower on the week, dragged on the downside by the Healthcare ( XLV ) and Materials ( XLB ) sectors. WTI Crude Oil prices rebounded by about 4% this week but remain more than 35% lower from last year.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

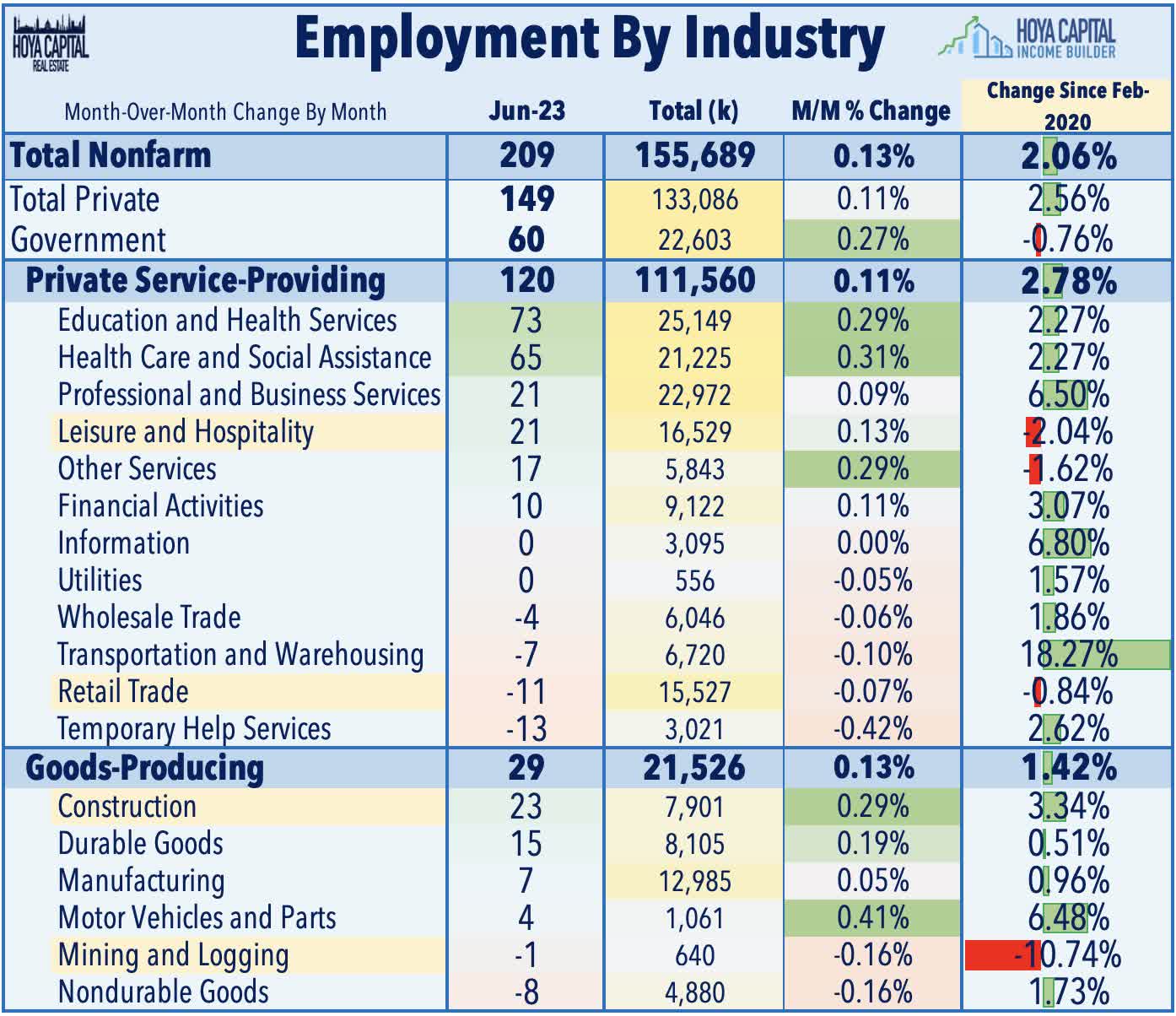

The critical BLS nonfarm payrolls report this week showed that the U.S. economy added 209k jobs in June - below expectations of 225k and marking the weakest month of job growth since December 2020 - which snapped a streak of fourteen-straight "beats" relative to consensus expectations. Job growth in April and May was also revised lower by a combined 110k. The soft report followed a surprisingly strong ADP private payrolls report earlier in the week, which showed job growth of nearly 500k - double the consensus estimate - and a decent slate of Jobless Claims data which showed a decline in continuing claims to the lowest levels since February. Conflicting signals were also present in the Household Survey, as the headline U3 unemployment rate declined to 3.6% - on the cusp of historic lows - while the so-called U6 under-employment rate increased to 6.9%, its highest level in nearly a year.

{kind=link}

Diving deeper, the report looks quite a bit softer under-the-hood with a notable slowdown in hiring seen in economically-sensitive industry groups including retail, hospitality, transportation, and professional services. Retail hiring has now been negative in three of the past four months, while hiring in leisure and hospitality has weakened rather considerably in recent months, averaging below 20k over the past three months compared to the 140k average in 2022. Notably, the hospitality sector remains 2% below pre-pandemic employment levels while the retail sector is now 1% below pre-pandemic levels, two of the four major industry groups alongside mining/logging and government that are below pre-pandemic employment levels. By contrast, transportation and warehousing employment is nearly 20% above pre-pandemic levels, while information technology and professional and business services employment are each more than 6% above 2019-levels.

{kind=link}

Average hourly earnings ("AHE") - a key inflation indicator - provided further evidence of normalizing labor market conditions following pandemic-era shortages. AHE rose 0.4% in June, which was slightly higher than expected but nonetheless continued the trend of moderation observed in the annual increase for both the 'All Employees' and 'Nonsupervisory Employees' indexes. Since the start of 2023, AHE for all employees has averaged 3.8% on an annualized basis - which is only marginally above the 3.3% increase in 2019 in a year that CPI inflation averaged just 1.8% - suggesting that concerns over wage-driven inflation are overstated. The average workweek, meanwhile, remained near three-year lows at 34.4 hours while the labor force participation rate stood at 62.6% for the fourth consecutive month, which remains stubbornly below the 63.0% pre-pandemic average from 2016-2019.

{kind=link}

We observed similar trends of cooling price pressures in the busy slate of PMI reports this week as well. Of note, the price indexes of both the ISM Services and Manufacturing PMI showed that inflationary pressures declined to the lowest-levels in more than three years in June to levels that are now below that of the 2016-2019 average - a period in which CPI inflation averaged less than 2%. Overall Manufacturing PMI dropped to 46.0 in June - the lowest reading since May 2020 - which marked the eighth straight month that the PMI stayed below the 50 threshold, the longest such stretch since the Great Recession. PMI reports from S&P Global showed similar disinflationary - and perhaps even deflationary - pricing trends, particularly in its manufacturing report. S&P highlighted one survey respondent who commented, "In this environment, pricing power is fading rapidly. Prices charged for inputs by suppliers are now falling at a rate not seen since 2009."

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

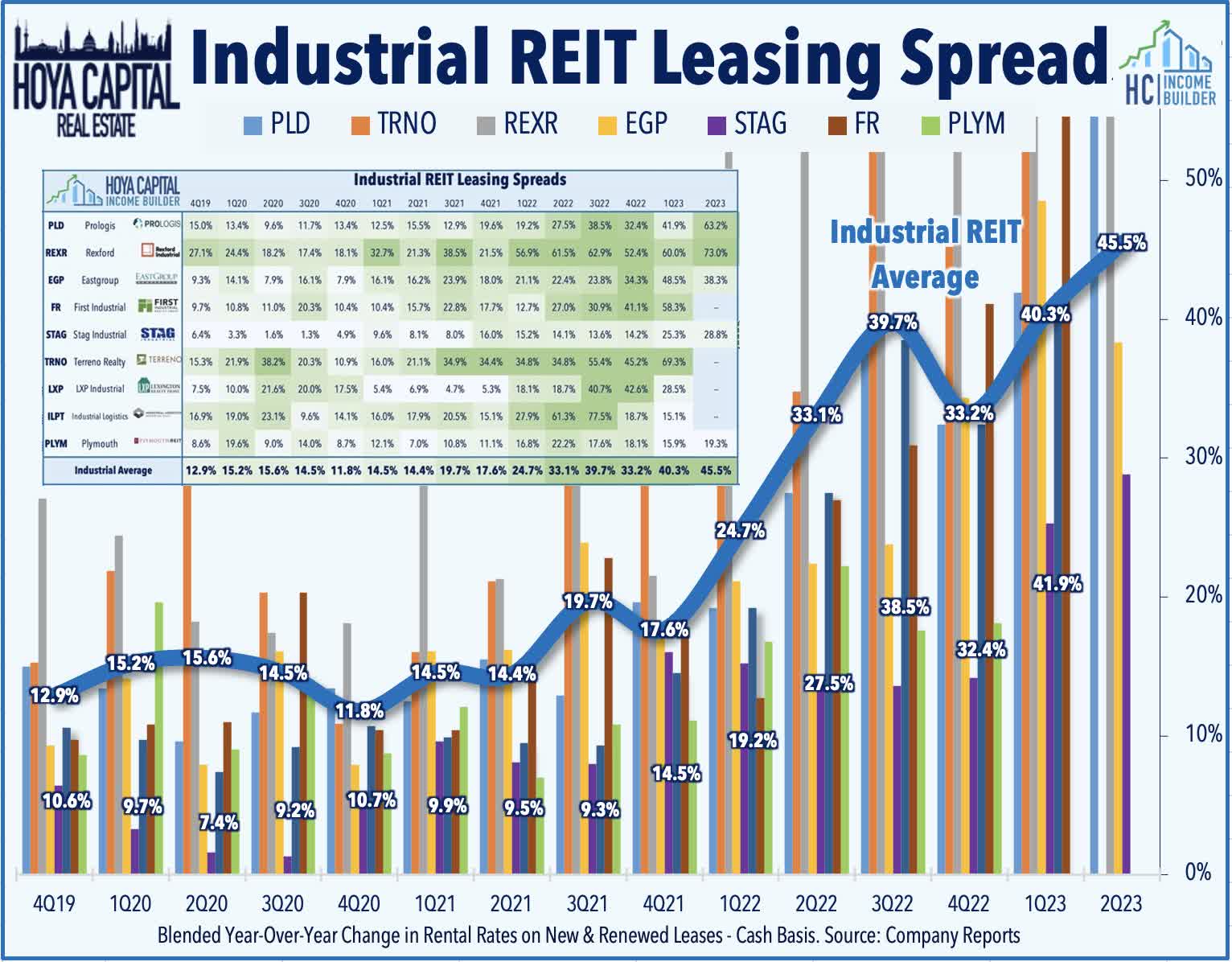

Industrial : Logistics-focused REITs lagged this week amid ongoing labor union disputes involving workers at UPS ( UPS ) and Amazon ( AMZN ), which threaten to again disrupt supply chains just as conditions were finally normalizing. In our latest Industrial REIT report, we noted that recent earnings results showed that logistics space demand continues to substantially outpace available supply. Rent growth has reaccelerated in early-2023, with rental spreads averaging over 40% so far this year, while occupancy rates climbed to fresh record-highs. Strengthening rent growth comes despite substantial downward pricing trends across other areas of the supply chain. Freight costs are now 80% below their 2021 peak, perhaps freeing-up capital for expanded logistics footprints. Plymouth Industrial ( PLYM ) slipped about 1% this week after it provided preliminary second-quarter operating metrics, noting that it achieved a 19.3% increase in cash rental rates - its strongest quarter of rent spreads since Q2 2022. Leasing volumes topped 2 million square feet in Q2 - more than double that of Q1 - which included 1.44M sf of renewal leases and 663k SF of new leases. PLYM's occupancy rate stood at 98.0% at the end of Q2, which is consistent with the company’s full-year 2023 forecast.

{kind=link}

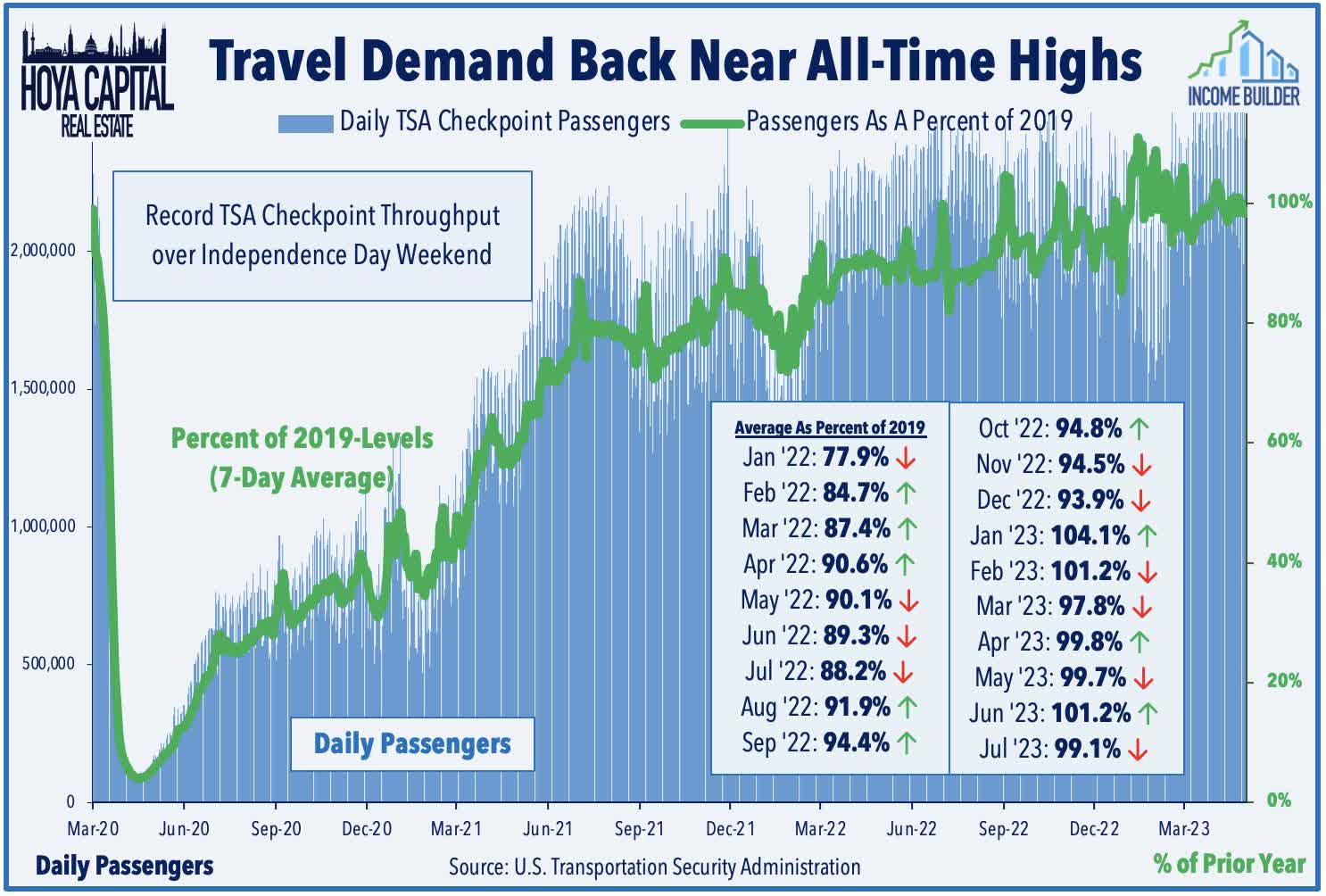

Hotels : The Transportation Security Administration ("TSA") reported this week that it processed record-high throughput at TSA checkpoints during the Independence Day week, peaking at nearly 3 million travelers for the first time. Sotherly Hotels ( SOHO ) gained more than 3% this week after it provided preliminary second-quarter operating metrics, noting that its Revenue Per Available Room ("RevPAR") increased to $131.16, which was 5% higher than last year and roughly 4% above pre-pandemic 2019-levels. SOHO commented that it has seen "sustained strength in demand for leisure travel and sequential improvement in group and business travel, with our urban markets fueling year-over-year gains." After hotel REITs relied heavily on room rate inflation to drive RevPAR growth for much of 2021 and 2022, recent RevPAR gains have leaned more heavily on improving occupancy rates while growth in Average Daily Rates ("ADR") has cooled back towards 'normal' levels. Elsewhere in the hotel space, Apple Hospitality ( APLE ) gained about 1% after it announced the acquisition of a newly renovated 154-room Courtyard by Marriott Cleveland University Circle for $31 million ($201k/key).

{kind=link}

Manufactured Housing : UMH Properties ( UMH ) gained about 1% this week after it provided a business update with preliminary second-quarter metrics. UMH noted that it had observed stronger MH sales trends in Q2 following a slowdown over the prior two quarters that mirrored the broader slowdown across the housing sector from mid-2022 through early 2023. UMH noted that it had rented 400 rental homes from its inventory of 700 unsold homes while 44 new homes were sold. This resulted in same property income growth year-over-year of approximately 8.6% and a 190-basis point improvement in occupancy. In our Earnings Recap , we noted that manufactured housing REIT results were generally in-line with expectations in Q1, with both Equity LifeStyle ( ELS ) and Sun Communities ( SUI ) maintaining their full-year FFO outlook. Both REITs cited strong pricing trends in their core manufacturing housing segment and their marina divisions - and each raised their property-level guidance for these segments - which was offset by some lingering softness in their RV segment - an area that higher fuel prices and a post-COVID normalization have impacted. Expense concerns - primarily related to weather and insurance premiums - have also been a recent headwind. MH REITs snapped an incredible streak of nine-straight years of outperformance over the broader REIT Index in 2022 and have remained laggards in 2023.

{kind=link}

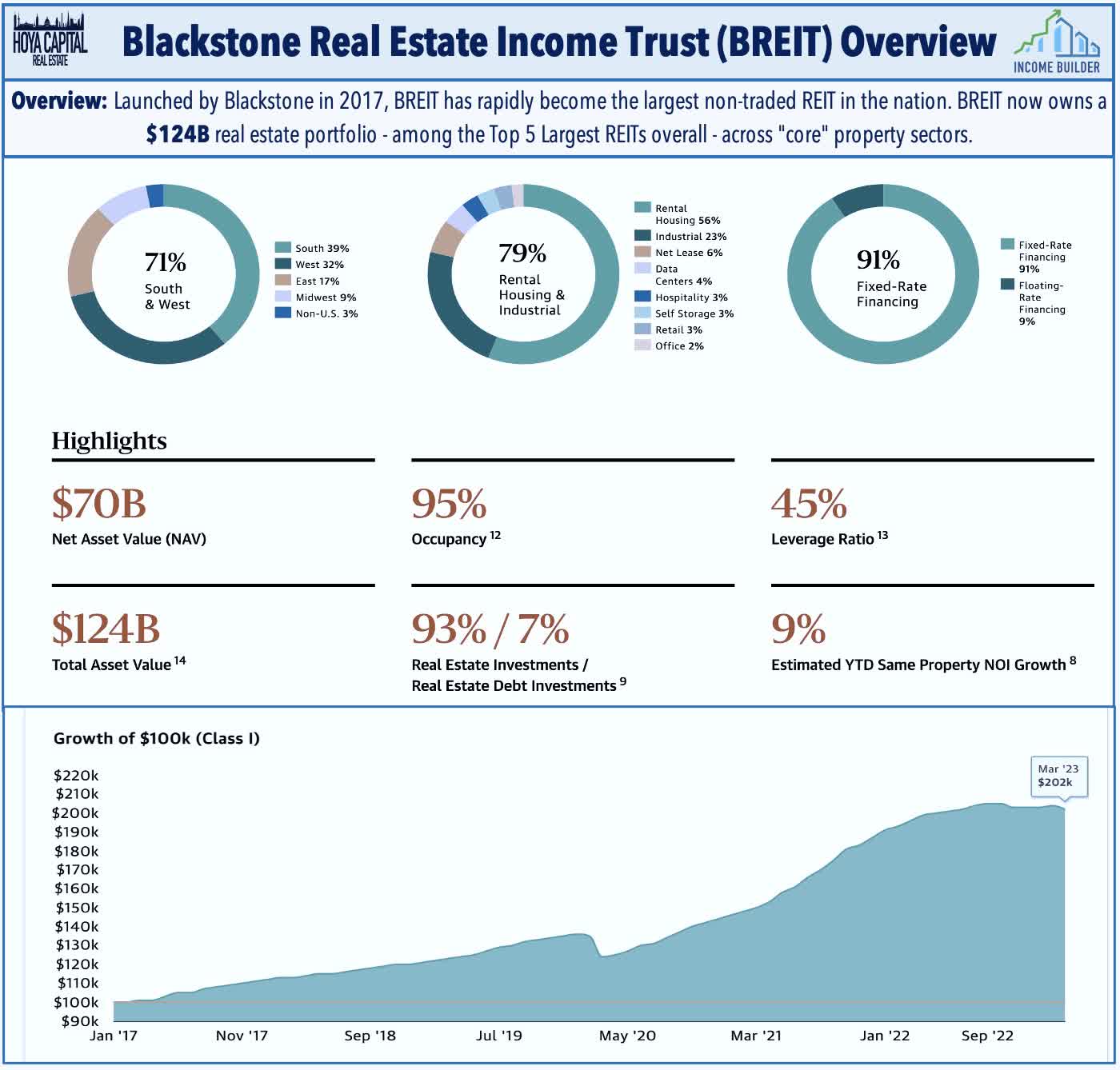

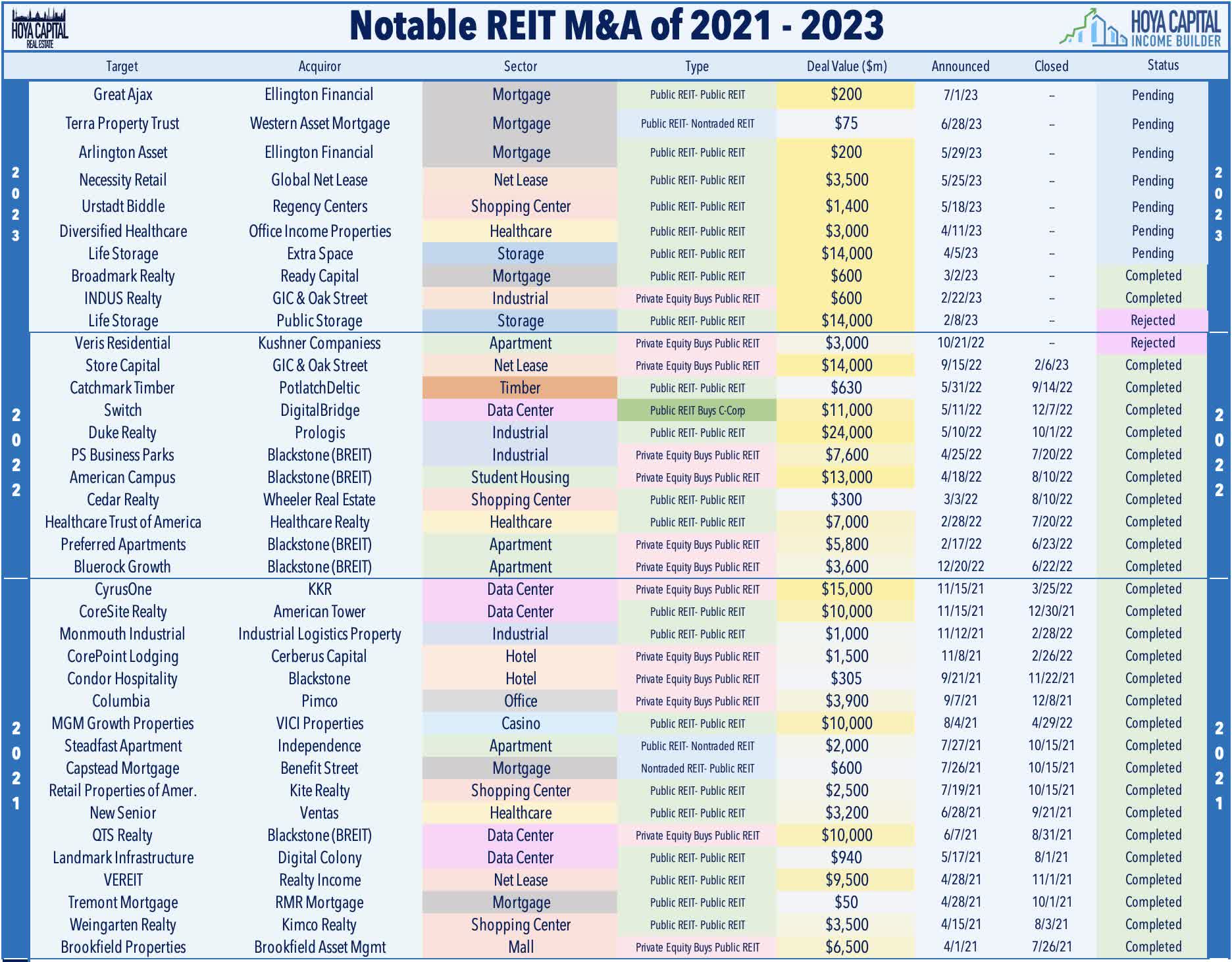

Asset manager Blackstone ( BX ) disclosed this week that it again had to limit withdrawals from its non-traded real estate platform in June - the eighth straight month that the firm's flagship fund limited redemptions. BREIT received $3.8 billion of redemption requests in June and paid out just 17% of those requests, down from the 30% in May and 29% in April. BREIT has paid out $8.1B to redeeming shareholders since November 30, 2022 when redemption limits began. BREIT noted that an investor that requested their money back beginning last November - and did so in every month since then - has received 90% of their money back - which BREIT cites as evidence that "the semi-liquid structure is working as intended." Blackstone - which was one of the most active buyers of real estate at the recent peaks of the market in 2021 - has become one of the most active sellers in the commercial real estate industry over the past year as it seeks to meet these redemptions. In late 2022, BREIT sold MGM Grand and Mandalay Bay - to VICI Properties ( VICI ) for $5.5B and is reportedly fielding offers for its stake in the Bellagio as well. Last month, BREIT sold a Texas report to Ryman Hospitality ( RHP ) for $800M in cash, and this month, Blackstone's opportunistic fund sold to Prologis ( PLD ) a $3.1B portfolio of industrial properties.

{kind=link}

Net Lease : A handful of net lease REITs also provided operating and acquisitions activity updates this week. Four Corners ( FCPT ) traded flat on the week after it announced that it had completed the acquisition of 71 properties thus far in 2023 for a total investment of $269.1M at a weighted average cap rate of 6.7%. By comparison, FCPT's average cap rate in the first-half of 2022 was 6.6% - during which time the benchmark interest rate increased by roughly 150 basis points - underscoring the relatively limited movement in acquisition cap rates - and thus tighter investment spreads - in the net lease space. Elsewhere in the net lease space, Global Net Lease ( GNL ) and Necessity Retail ( RTL ) - a pair of externally-managed REITs that plan to merge later this year - each gained about 4% on the week after providing preliminary Q2 operating metrics. RTL announced that it completed 686k sf of new and renewal leases during Q2, which total $9.06 million in annualized base rent with a weighted average lease term of 5.4 years. GNL announced 889k SF of leasing activity in Q2 totaling $4.6M in annualized rent at an average term of 5.7 years - an acceleration from the roughly 650k in leasing volume completed in the first quarter.

{kind=link}

Healthcare : Healthcare REITs were in-focus this week after healthcare data firm National Investment Center ("NIC") released its quarterly performance metrics for the senior housing and skilled nursing industries. NIC reported that the senior housing occupancy rate increased to 83.7% in the second quarter, continuing a slow-but-steady rebound from its pandemic lows of 77.8%. While occupancy rates remain below the pre-pandemic levels of around 90%, rent growth set another record-high in Q2 at 5.7%, strength that has been fueled, in large-part, by the nearly-9% increase in social security benefits, which has allowed SH owners to push rent increases. Positively for senior housing REITs, supply growth has finally cooled following a decade of elevated inventory growth, as NIC reported that units under construction amounted to 4.9% of total inventory, which is the lowest seen since 2014. The NIC report also showed a similar continued occupancy recovery and rent growth acceleration for skilled nursing REITs in Q2 with the average occupancy improving to 81.9% alongside record-setting rent growth of 4.3%, providing a much-needed lift for struggling operators that have pressured by elevated labor expenses and a dwindling of COVID-era government support.

{kind=link}

Mortgage REIT Week In Review

The recent wave of mortgage REIT mergers continued this week as Ellington Financial ( EFC ) announced its second merger deal in as many months. Following its announcement in May that it would acquire micro-cap Arlington Asset ( AAIC ) in an all-stock deal, Ellington announced that it will also acquire Great Ajax ( AJX ) - a credit-focused residential mortgage REIT which holds roughly $1 billion of first-lien residential re-performing loans (“RPLs”) and non-performing loans (“NPLs”) - in an all-stock deal for an equivalent of $7.33/share of Great Ajax common stock. The price represents an approximate 19% premium to AJX's prior closing price on June 30, but a 42% discount to AJX's last reported book value at the end of March. When the transaction closes, EFC stockholders are expected to own 84% of the combined company’s stock, while Great Ajax stockholders are expected to own the remainder. The company will assume EFC’s name and ticker symbol.

{kind=link}

More broadly, mortgage REITs traded mostly-lower this past week, with the iShares Mortgage Real Estate Capped ETF ( REM ) slipping 1.7%. Last week, we published Mortgage REITs: High-Yield Risk and Opportunity . Recovering from a sharp sell-off in the wake of the Silicon Valley Bank collapse, Mortgage REITs have rebounded since early April as turmoil across interest rate markets has calmed. We noted that distress in the commercial and residential real estate markets has been more isolated than the 'scary' magazine covers would suggest and outside of urban office properties, actual default rates remain near pre-pandemic lows. Dividend cuts have come as a 'ripple' rather than a 'wave' with 10 of 40 mREITs reducing their dividends this year, but industry-wide payouts are only down about 5% YTD versus the 60% dip seen in 2020. The squeeze on highly-levered private market portfolios is still in the early innings, however, but an orderly unwind remains the base case, with well-capitalized equity REITs likely to benefit from forced-selling in private markets.

{kind=link}

2023 Performance Recap & 2022 Review

Through the first half plus one week of 2023, the Equity REIT Index is now higher by 1.5% on a price return basis for the year (+3.6% on a total return basis), while the Mortgage REIT Index is higher by 1.0% (+5.3% on a total return basis). This compares with the 14.7% gain on the S&P 500 and the 7.3% advance for the S&P Mid-Cap 400 . Within the real estate sector, 10-of-18 property sectors are in positive territory on the year, led by Single-Family Rental, Data Center, Apartment, and Timber REITs, while Office and Cell Tower REITs have lagged on the downside. At 4.05%, the 10-Year Treasury Yield has risen by 17 basis points since the start of the year - up sharply from its 2023 intra-day lows of 3.26% - but still below its late-2022 closing highs of 4.30%. The US bond market has stabilized following its worst year in history as the Bloomberg US Aggregate Bond Index has gained 0.7% this year. Crude Oil - perhaps the most important inflation input - is lower by 6% on the year and roughly 35% below its 2022 peak.

{kind=link}

Economic Calendar In The Week Ahead

Inflation data is in the spotlight in another jam-packed week of economic data in the week ahead. The main event comes on Wednesday with the Consumer Price Index for June, which investors and the Fed are hoping will show a continued cooling of inflationary pressures. The headline CPI is expected to dip rather sharply to a 3.1% year-over-year rate as some of the "hottest" prints seen in mid-2022 begin to roll off. We've noted in recent reports that "real-time" inflation - as measured by the CPI-ex-Shelter Index - has averaged less than 1% since last July. We speculate that an inevitable "2-handle" on the headline CPI - which appears likely to occur by the July report - will be a key narrative-shifting threshold for even the most hawkish Fed officials. On Thursday, we'll see the Producer Price Index, which is expected to show an even more significant cooling of price pressures, with the headline PPI expected to slow to just a 0.4% year-over-year rate - down from the recent peak last March at 11.8%. On Friday, we'll see get the first look at Michigan Consumer Sentiment for July - a report which includes the closely-watched inflation expectations survey, which is indeed expected to print a "2-handle."

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Hawks Still In Control