HCAT - HCA Healthcare: Expect Performance To Meet Long-Term Target Over Time

Summary

- There are several underlying growth drivers further driving the adoption for HCAT solutions.

- HCAT differentiated product offering, strong M&A track record, and ability to further penetrate existing base of users are what drive top line growth.

- The better-than-expected profitability has kickstarted a market reaction to drive momentum in the stock price.

Description

I believe Health Catalyst ( HCAT ) is worth more than the share price today. Several factors such as the shift from volume-based to value-based payment models in the healthcare industry, the increasing complexity of healthcare data, and HCAT's unique offering, are growth drivers for the company. Additionally, HCAT has a strong track record in M&A, acquiring companies that can be integrated into its platform and increase its offerings to customers.

More importantly, there is a clearer path today for HCAT to reach positive profit levels, which is a good catalyst for valuation rerating.

Company overview

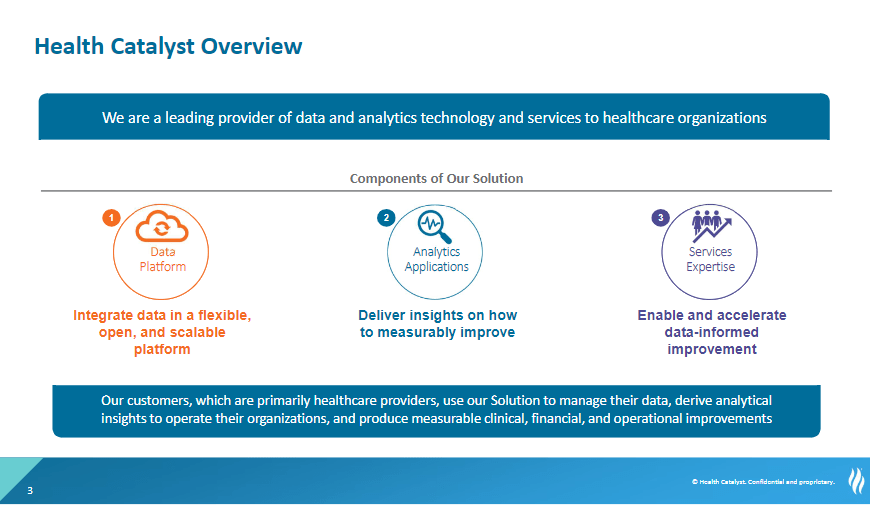

In order to help hospitals manage their administrative, financial, clinical, and research data, HCAT creates and distributes custom healthcare information management software.

{kind=link}

Several key challenges within the industry driving HCAT growth

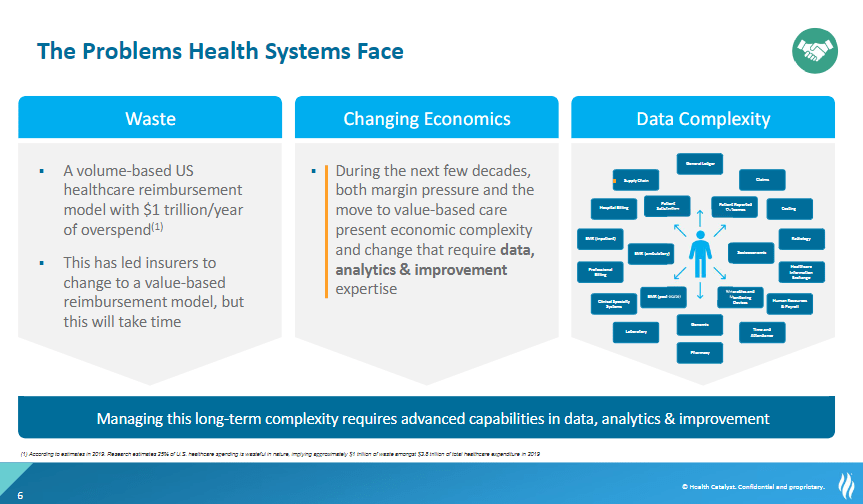

Healthcare organizations' use of data and analytics is changing as a result of multiple challenges and market dynamics. I think we have a once-in-a-generation chance to dramatically enhance healthcare's clinical, financial, and operational quality as a result of the confluence of healthcare waste, shifting economics, and complex data.

In my opinion, the economic shift brought on by the adoption of VBC is the primary motivator. Payors in both the public and private sectors have been decreasing their fee-for-service [FFS] reimbursement rates for a number of years, putting a strain on the bottom lines of healthcare organizations. In addition, providers are feeling the effects of the transition from volume-based to value-based payment [VBP] models. Rising costs and the transition to value-based care [VBC] models have created economic uncertainty and complexity for the healthcare industry, but these challenges can be alleviated with the right application of data and analytics.

Then there's the problem of data explosion. The U.S. healthcare system has spent billions of dollars over the past decade collecting massive amounts of data digitally. One such system is EHR, or electronic health records. Because of these expenditures, there is now an abundance of healthcare data, which I anticipated would grow at an exponential rate. Adding in socioeconomic, genomic, and telehealth data will further complicate matters. More and more regulations are being placed on the healthcare industry, further complicating the already difficult tasks of collecting, storing, and using data. On the other hand, both disease classifications and treatment methods are dynamic. Healthcare-specific data, logic, and analytics capabilities are difficult to implement in legacy software, which is why previous attempts have failed. Many hospitals and other healthcare facilities have also attempted to create their own solutions, only to realize that doing so would be prohibitively expensive. They've also looked to traditional EHR providers, but those companies lack the tools to efficiently compile and derive analytics insights from the many different data sources.

{kind=link}

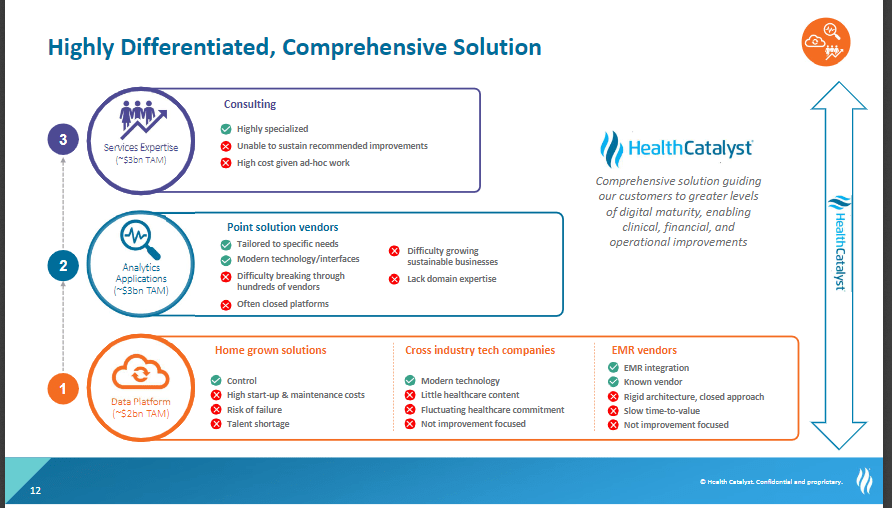

HCAT has a unique offering

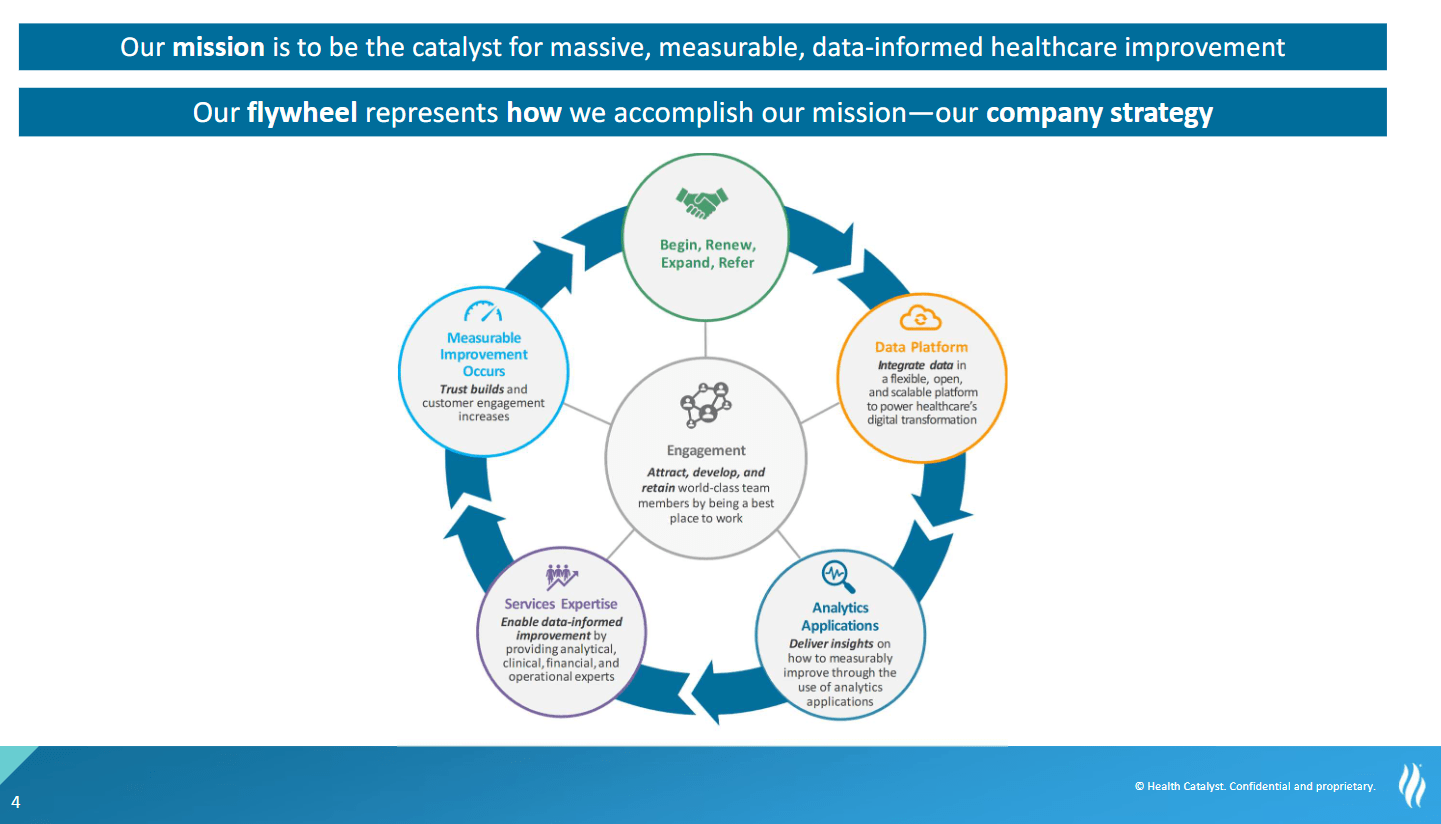

I believe HCAT's offering is highly differentiated for health systems, and the company has developed a solid go-to-market strategy to expand its customer base and keep its current customers happy. The integration of data feeds from all of the sources in a healthcare system is crucial to the success of any data operating system [DOS]. Due to HCAT DOS's open, flexible, and scalable architecture, integrating new data feeds or use cases into an existing system is a straightforward process. In addition, the "all-access" model is the most popular choice among HCAT's clientele because it allows for unrestricted use of all of HCAT's software. Most HCAT users have found the platform compelling enough to justify expanding their use of it without renegotiating contracts or reallocating funds. As a result, health system CIOs can implement DOS alongside alternative or homegrown enterprise data warehouse, with the option to gradually phase out support for the latter. In my experience, this is a typical development for HCAT's clientele. To complement its core technology offering, HCAT's professional services division supplies the company's clients with the strategic guidance and engineering talent they need to propel innovation.

{kind=link}

Continue penetrating current base of customers

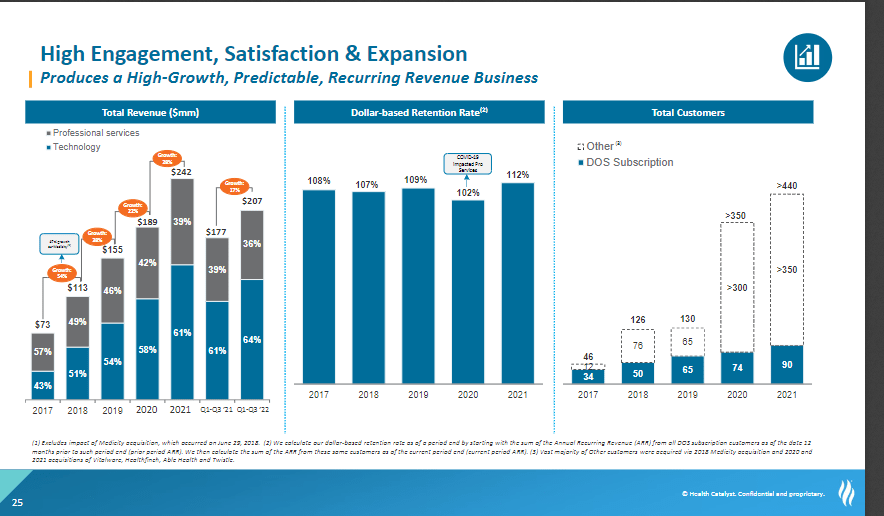

If history is any indicator, HCAT will keep working to strengthen and grow its connections with its current clientele. Typically, the customer journey begins with the implementation of a single metric-driven clinical, financial, or operational improvement through the use of focused analytics applications and services. Customers gain faith as HCAT consistently delivers on its promises, leading to increased usage and the purchase of new apps and services. Proof of this is the high dollar-based retention rate (>100 percent).

{kind=link}

As HCAT Solution's connections with its customers grow stronger, I expect HCAT to speed up the development of new features and the addition of new applications to its library. HCAT is able to identify new opportunities for further improvements and share that insight with other customers across core market because their platform is open and they partner with customers. HCAT will use these findings to inform the creation of new analytics software and services. In my opinion, this creates something of a flywheel effect, since the greater HCAT's customer base, the more information it is able to collect, which in turn aids in deciding which product innovations to pursue. That will have two results: (1) keeping current customers happy, since HCAT meets their needs, and (2) drawing in new ones. A virtuous cycle is formed as a result of this loop.

{kind=link}

Strong track record in M&A

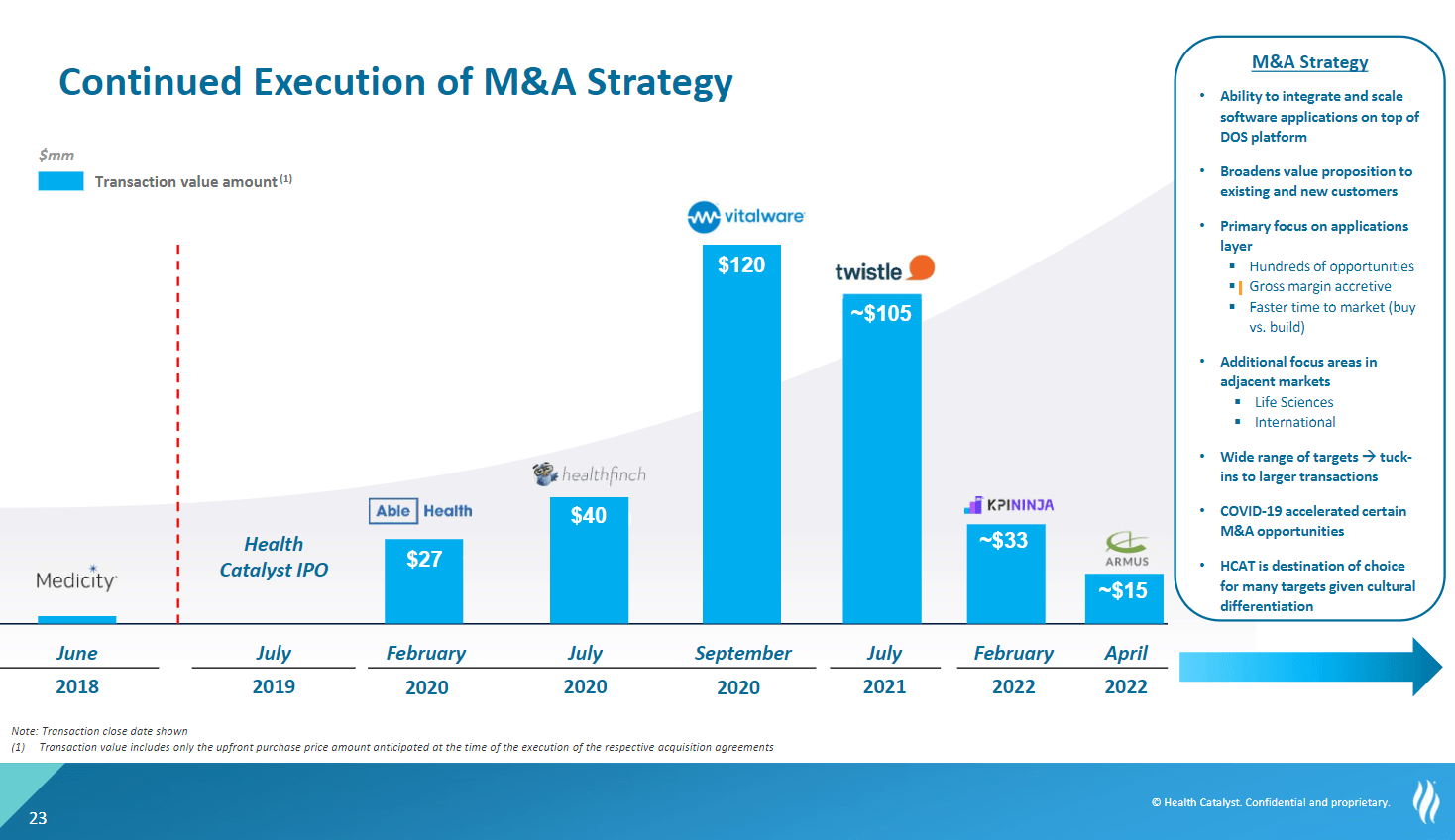

So far, I've been impressed with HCAT's M&A approach. Since its IPO in July 2019, HCAT has made a number of acquisitions with a total transaction value of over $300 million. These include the recent Armus for $15 million and KPI Ninja for $33 million. HCAT considers the software applications of a target company in an acquisition opportunity in light of how well they can be integrated and scaled on top of HCAT's existing DOS platform, thereby increasing HCAT's offerings to new and existing customers. As an illustration, after acquiring Medicity in 2018, HCAT gained access to Medicity's clientele of more than 60 healthcare organizations, allowing it to not only integrate Medicity's technology but also sell its own offerings to these new customers. In the future, I anticipate that HCAT will keep on the lookout for partnerships with businesses that will allow it to maximize profits and shorten the time it takes to bring its solutions to market.

{kind=link}

Better-than-expected profitability

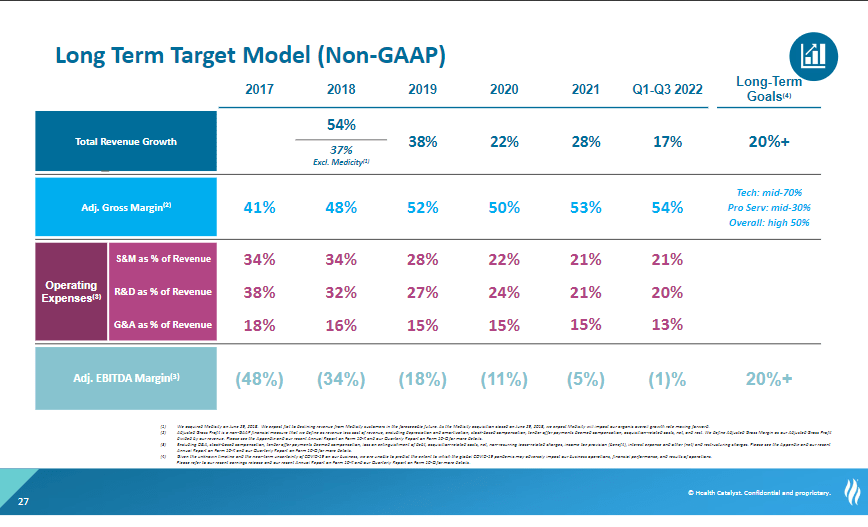

HCAT increased its guidance for the FY22 on the back of better-than-expected bookings, and it reported earnings for the third quarter that surpassed its revenue and adjusted EBITDA guidance. Moreover, management anticipates a better net dollar retention rate, up from their 2Q22 estimate of the mid-90s to a range of 97% to 101%. Despite the company's continued admission that 2023 will be difficult, management has been heartened by recent discussions with both new and existing clients. Despite ongoing challenges with budgetary constraints, attrition, and other issues, HCAT's services are still relied on by many hospitals. In the current economic climate, the significance of this has increased, as such I expect HCAT to have a somewhat insulated impact (less impact from churn).

Adjusted EBITDA projections are also ahead of schedule for the company. They are now projecting a loss of -$1.15Mn for 4Q22 and -$3Mn for FY22. Managers have stated that they anticipate an increase in adjusted EBITDA margin of somewhere in the range of 300 basis points by the end of FY23. And by 2025, management expects to see an EBITDA margin of around 10%, with longer-term margins of around 20%.

Valuation

The stock, which has suffered a substantial decline in value over the past two years, has finally rebounded thanks to improved guidance and a brighter outlook for profit growth. My analysis projects a target price of $17, representing a 23% increase, based on factors such as the company's FY22 guidance, modest growth in FY23 and a recovery in growth following a challenging macro environment. Although I have confidence in the company's long-term growth plans, I choose to play it safe by taking a more cautious approach to projecting growth.

As HCAT continues to improve profitability, I believe there is a path for valuation to go back to 5.5x forward revenue (historical average). However, as of the data right now, I believe the market is unlikely to attach a higher multiple.

Own estimates

{kind=link}

Key risk

Competition from EHR vendors

HCAT faces a significant long-term competitive threat from the large EHR vendors who have established rapport with the CIOs of hospitals and health systems. These companies have substantial resources to spend on interoperability and create an integrated data platform that can compete with HCAT. In addition to EHR providers, technology firms with experience managing data also have room to grow and innovate. When compared to its competitors, who typically focus on a single application, I believe HCAT still holds a significant advantage due to the breadth and depth of its offering.

Summary

In my opinion, HCAT is undervalued at the moment. Several factors, including the healthcare industry's transition from volume-based to value-based payment models, the growing complexity of healthcare data, and HCAT's distinctive offering, are propelling the company's expansion. HCAT also has a solid history of mergers and acquisitions, successfully incorporating target businesses into its own infrastructure and thereby expanding its product selection for existing and potential customers.

Even more importantly, HCAT now has a more defined route to profitability, which should serve as a catalyst for a positive rerating.

For further details see:

HCA Healthcare: Expect Performance To Meet Long-Term Target Over Time