INVE - Headwinds At Identiv Should Gradually Clear

Summary

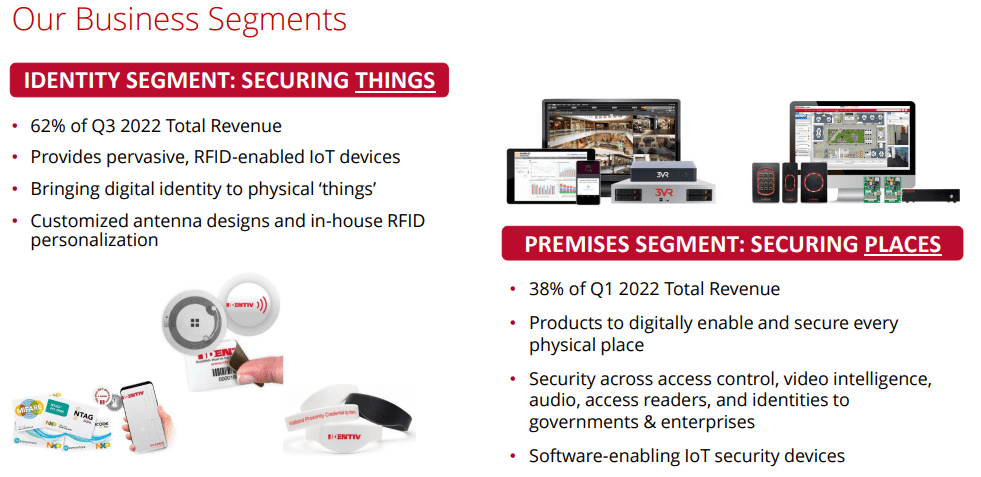

- The company produces cutting-edge solutions for two lines of growth businesses, premises and identity.

- The TAM of identity (RFID chips) is potentially huge as chips become cheaper and can do more.

- Premises produces nearly 60% gross margins and grows at 3x the market rate, winning share.

- The company is experiencing headwinds from supply chain problems but these should be sorted out at some point.

- The shares could revisit the highs at 3x the current share price when that happens.

Identiv ( INVE ) the producer of advanced RFID chips is going through a rough patch due to supply problems for which, in their own words, they were ill-prepared.

For a quick recap, the company has two segments ( December/22 IR presentation ):

{kind=link}

Supply chain problems

Well, during the Q1CC management touted their proactive supply chain management but now have to admit this faltered.

The problems are occurring in their Identity segment, the premises segment is experiencing fewer problems and grows at nearly 3x the market. That is a saving grace, as premises generates most of the gross profit dollars despite being smaller.

Their contingency planning failed as they experienced some problems. One of their customers realigned their supply chains, which cost Identiv almost $1.5M in postponed orders and component shortages produced a $4.5M hit.

They're fixing these problems through new operations and supply chain leadership and increased focus on supply availability, as well as redesigns producing component interoperability.

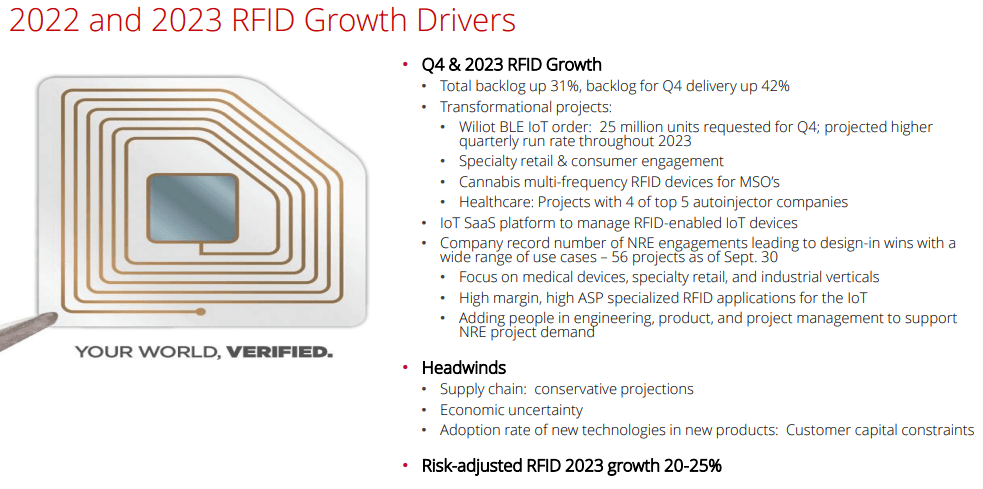

They didn't fill in the revenue gap with lower margin products like in Q4/21. All this caused a revenue shortfall of $5M. However, underlying RFID demand is still very strong, witness:

- Backlog +31% to $36.9M

- Backlog for delivery in Q4 +42% and +19% q/q to $16.6M

- Wiliot ordered 25M units (for an unnamed customer who can easily absorb these quantities), 10M of these can be met in Q4 but they said that their quarterly run rate will actually be higher than 25M units a quarter.

So there is little chance of lack of demand, should some customer scale back they can fill that with others, and win new logos as well.

They're not building the Wiliot order into their guidance until they are sure they can deliver it (that is, having the supply) and as a result they took FY23 guidance $30M down, assuming a base case for only supplying 10% of its needs (25M+ units per quarter at close to $0.30 per unit).

Identity

{kind=link}

The company has 100% retention in RFID customers, 18 new energy projects (for a total of 56), and additional developments in healthcare, cannabis, and other segments.

{kind=link}

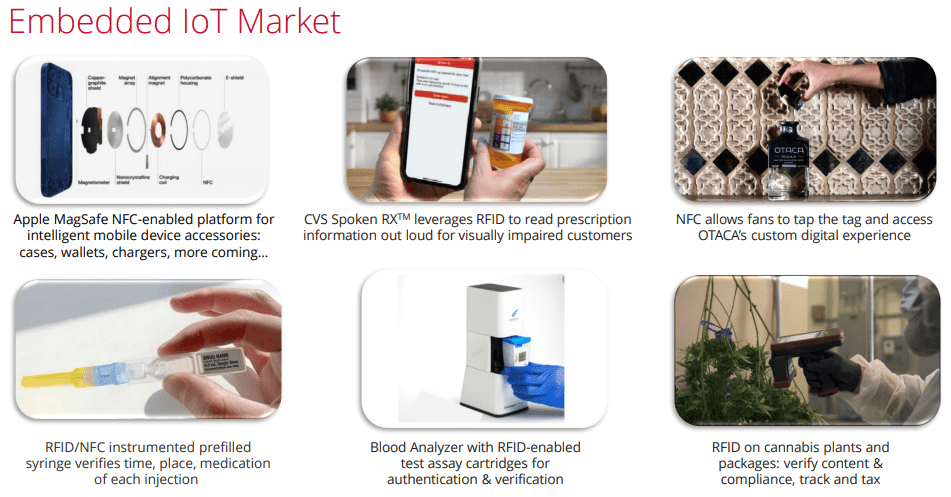

In our previous article, we described already some of their innovative uses for RFID in most of the products they have, like:

- FC Koln , a German football club where they're putting RFID chips in their fan scarves which do things like automatic entry, get real-time digital content and offers inside the stadium. They will take this to other football clubs with partner Collect ID.

- Wiliot: supply chain , a whopper 25M unit per quarter order for a big retail client of Wiliot.

- Cannabis ; smart tamper seals have a good shot at becoming standard.

- Medical auto injection which has a high ROI (compared to clinic visits) active projects with four of the top five global auto injector companies with one placing order for 500K units, will develop into a multi-100M unit category.

- Medical prescription pill bottle : from the Q3/CC: "The prescription pill bottle category now is consolidated under one of our partners Envision America, resulting in four of the top six pharmacy chains in the U.S. now active with spoken RX projects supported by our RFID devices. We're prioritizing this category for shipments in Q4 to make up about $600,000 that we didn't manage to ship in Q3."

- OTACA Tequilla smart packaging (Jul/22).

- They also build the bitse.io SaaS platform (Dec/22) to keep track of assets.

It gives some idea of how significant their market opportunity is but it remains to be seen how fast they can scale these, given the supply problems, possible headwinds in the economy, and customer adoption time for complex technology. And there is more to come:

{kind=link}

{kind=link}

Then there is the recent strategic partnership with Trace-ID to ( company PR ):

become the exclusive provider for Trace-ID’s complete line of specialty and industrial UHF RFID across North America. This partnership delivers best-in-class specialty and industrial UHF RFID at the most competitive price points and provides Identiv with access to a European manufacturing facility that has line-of-sight to 1 billion units of specialty UHF capacity.

What's in it for Trace-ID? Well:

Identiv has the commercial expertise to channel specialty UHF products much further into higher-value applications

Finances

Some data:

- Revenues +7% to $31M.

- Revenue for identity was $19.2 million at Premises was $11.8M.

- RFID unit shipment +17% to 45.4M, limited by component supplies

- Non-GAAP gross margin 37% versus 39% in Q3/21; LT target is 40-45%.

- Identity adj gross margin at 24% versus 29% Q3/21 due to product mix and legacy smart card readers (which are declining).

- Premises adj gross margin at 59% versus 58% in Q2/22 and Q3/21; LT target 55-60%.

- GAAP gross margin 36% versus 38% Q3/21.

- GAAP OpEx $10.6M vs $10.5M in Q2/22 and $9.2M in Q3/21.

- non-GAAP OpEx $9.5M (31% of revs) versus $9.2M Q2/22 and $8.2M Q3/21 (28% of revenues)

- Adj EBITDA $2M (7% margin) versus $1.4M Q2/22; LT target 15-20%

- Backlog +31% to $36.9M

- Backlog for delivery in Q4 +42% at $16.6M, +19% q/q

- $21.9M in cash, no debt

- Guidance FY22 $112M-$118M; FY23 +20-25%. this is risk-adjusted for macro headwinds, supply problems, and some customers moving slower, only 10% of Wiliot is factored into this (that is, only 10M of 100M+ possible units). At full-scale Wiliot would add 15 to 20 percentage points to this growth rate, pushing it above 40%.

- They see premises growing 205-25%

The supply problems took a bite out of cash flow:

But that's not immediately alarming, and while they have considerable CapEx in front of them (new machines, a facility in Indonesia) management expects little or no cash bleed going forward.

Valuation

There is more dilution on the way, from the 10-Q:

INVE 10-Q

So that's 32.78M shares fully diluted at $7 share price for a market cap of $230M and an EV of $208M. With $140M in guided revenue (with upside if they manage to do more for Wiliot) for FY23 the shares sell at 1.5x FY23 EV/S.

Analysts expect a 7 cent loss per share this year turning to a 16 cent per share profit. It's not cheap on an earnings basis, and this business needs to scale first, which I think it will do. Their premises business is very attractive on a stand-alone basis:

- $45M+ revenue growing at 15%-20% growth, 3x the market

- Over 15% of recurring revenues

- 59% gross margin

This could easily sell at 4x sales which would be almost the entire market cap of the company. The company is also delivering cutting-edge solutions for its identity segment, which is rapidly expanding as RFIDs are still in their infancy but here the company has a huge TAM to go after as ever new use cases are developed.

Conclusion

We see plenty of things we like:

- The company is a technology leader bringing innovative solutions to market.

- The RFID market is still in its infancy and sets to grow for years to come.

- The company's identity segment grows much faster than the market, generates high gross margins, and on a stand-alone basis could be worth a large part of its market cap.

- While the company experienced some temporary problems, underlying growth isn't gone, witnessed by the strong increase in backlog.

- Once the supply problems are gone, this is a business that can scale rapidly, the Wiliot order alone provides a huge opportunity but there are several more as RFID becomes cheaper and more versatile and the use cases expand.

- While at first sight there seems to be risk from the economy, but management has been very careful in its guidance and the substantial backlog should provide a cushion for any but the most severe economic downdrafts.

- The shares are still expensive on an earnings basis but when the business scales, which I think it will, this will be quite another matter.

For further details see:

Headwinds At Identiv Should Gradually Clear