GNS - Helbiz Will Likely Continue To Dilute While Riding The Coattails Of The Naked Short Squeeze Investigation From Genius

Summary

- Helbiz has gotten on the bandwagon of the "naked short war" led by Genius Group, but has taken no serious action.

- HLBZ's share count has recently exploded from ~50 million to ~140 million, mainly from a SEPA agreement with Yorkville.

- The shares were issued to Yorkville in the $0.11 to $0.16 range, giving the firm incentive to dump shares at large profits when the stock recently popped to over $0.50.

- The company's financial state is extremely precarious and HLBZ will likely need to continue diluting in the near future.

- The dilution theory is backed by the non-committal behavior of HLBZ's CEO Salvator Palella.

A few days ago, I wrote an article on Genius Group Limited (NYSE: GNS ) and how I believe that the company's investigation into naked short sellers is genuine. I briefly mentioned Helbiz, Inc. ( HLBZ ) as a company that is trying to ride the coattails of this movement. So far it has worked, with its stock price rising from $0.12 to briefly over $0.50 in the days since announcing its own fight into alleged naked short sellers.

I now feel compelled to write a focused article on HLBZ. The behavior undertaken by its CEO, particularly on Twitter and on the topic of dilution has made investors jittery. It is my opinion that HLBZ is making a mockery of the naked short investigation that Genius is making a serious attempt to undertake. Genius is trying to improve returns for shareholders. I believe that HLBZ's attempt - if at all serious - will fail due to its recent dilution. Dilution that will be extremely likely to continue given the poor financial state of the company. The reason why the CEO isn't committing to not diluting the stock over a long period of time is because he simply can't. The company has to finance operations until it can slow down its extremely high burn rate.

Background

I was the first person on Seeking Alpha to write an article on HLBZ back in October 2021. It was a play on the warrant arbitrage that worked for a few minutes before both the stock and warrants wildly tanked. However, I had kept following the company and even re-opened a speculative position on the warrants which ended as an unprofitable investment.

While Helbiz was clearly not performing well financially, one thing that kept my interest was the continued and considerable buying by the company's CEO, Salvatore Palella. I thought him aggressively throwing millions of dollars at his company was a sign that there was a plan to get to financial stability in the near term. I had made contact with the company's IR representatives asking questions about Helbiz's operating performance, hopeful that certain issues I saw on the income statement were a result of short term start up costs in the e-mobility space.

However, once it became clear to me that Helbiz's financials were not going to improve and that deteriorating market conditions for de-SPACs and startup companies were not going to make it easy for the company to survive, I exited my position and shelved my interest. It was obvious to me that this company was going to need a miracle to avoid insolvency, and that it would attach itself to anything that came along in order to do so.

Diving into the poor state of HLBZ's financials and the dilution that has occurred to keep it afloat

I'm an experienced microcap investor and researcher. So I have seen my fair share of companies in tenuous financial states. I can say the pace at which HLBZ's financials have deteriorated since I started following this company is one of the worst I have ever seen. The only one that I can think of that is worse was MoviePass from Helios and Matheson Analytics Inc. ( OTC:HMNY ).

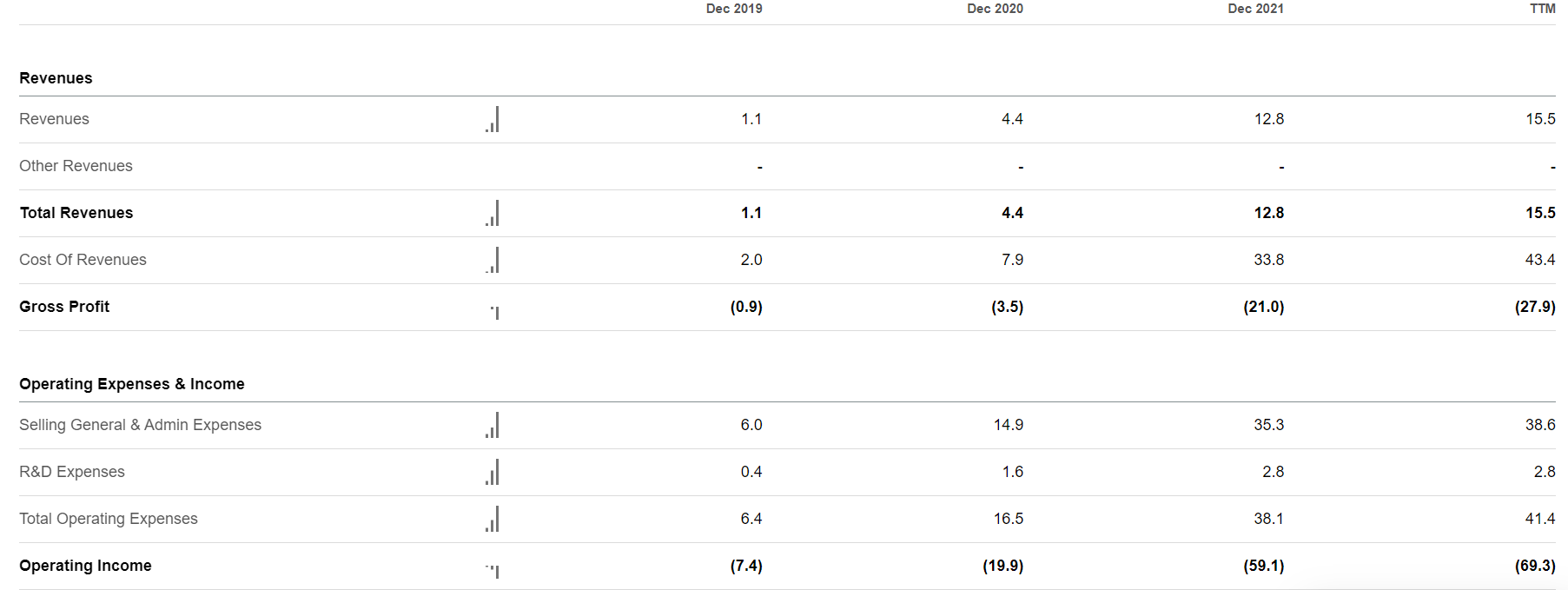

This is a snapshot of the operating income portion of the company's income statement:

{kind=link}

Seeking Alpha

The first thing I want to point out is that this company has always had negative gross margins. The cost of revenue is actually higher than the revenue itself. When I first made contact with the IR representatives, I assumed this was some kind of accounting issue related to purchasing the fleet for its e-scooter and e-bike rental business. But instead of getting better with time and revenue growth, gross margin has actually gotten worse. Back in 2020, the company had $7.9 million in cost of revenue on $4.4 million in revenue, -80% gross margin. Fast forward to the trailing 12-month numbers, and the cost of revenues is $43.4 million on $15.5 million in revenue, -180% gross margin.

Add in operating costs, and the result is a company that has a $69.3 million operating loss on $15.5 million in revenue over the previous four quarters. Interest expense is $7.6 million - nearly half of revenue alone - leading to an overall loss of $85.1 million during that time.

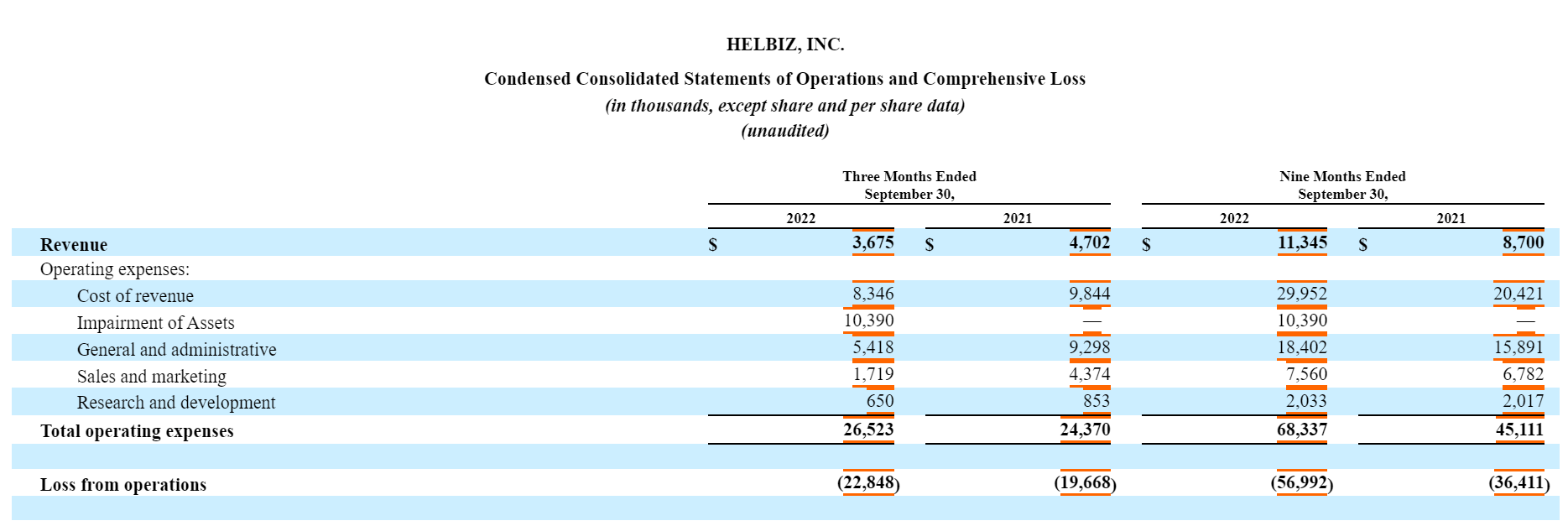

Quarterly results for Q3 2022 don't show much hope for a turnaround either:

{kind=link}

HLBZ Q3 Financials

The company reported only $3.7 million in revenue for Q3 2022, down 22% from Q3 2021. Margins actually improved slightly, as the company has started making a concerted effort to cut costs and exit unprofitable revenue streams and markets. With that being said, it still has a long way to go to reduce its burn rate which currently sits at ~$20 million a quarter.

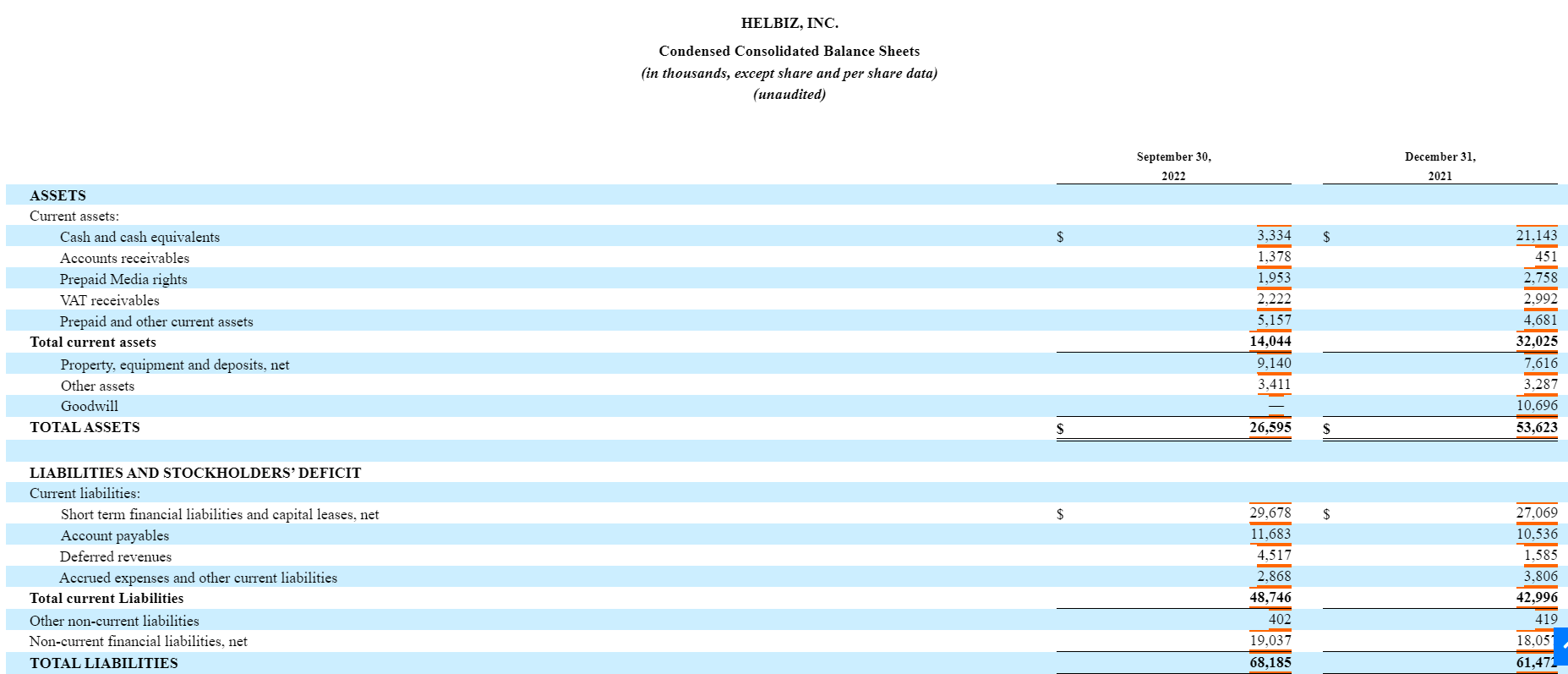

These major losses on minimal revenue have ravaged the balance sheet, as of September 30th, 2022:

{kind=link}

HLBZ Q3 Financials

HLBZ is almost out of cash, with only a little more than $3 million left and $14 million in current assets. Current liabilities are $49 million, so the company has a $35 million working capital deficit. Long term liabilities are $19 million, including a $14 million secured loan. Now consider that this was a snapshot from four months ago, and the company has had to fund its operating losses since then. The money to fund these losses have to come from somewhere, and so far it has come from the substantial issuance of shares.

This is a chart of shares outstanding over the past year. It has exploded from around 50 million at the end of September to 142 million today:

This increase in shares outstanding over the past few weeks has come in the form of a slew of shares being issued in the $0.11 to $0.16 range, with the latest one being 8 million shares issued at $0.1185. This is part of a $13.9 million Share Equity Purchase Agreement with YA II PN, Ltd., a Cayman Islands exempt limited partnership also known as Yorkville. I encourage investors to take a look at the performance of the companies that get into similar types of financing deals with Yorkville. That could be an entire article onto itself. But one can surmise from my tone that the performance is generally "not good".

The saddest part of issuing nearly 100 million shares since September at these low prices is that it does almost nothing to improve the company's financial fortunes. Let's assume the $13.9 million SEPA eventually gets exhausted. That may be just enough to fund one quarter of operating losses, assuming the recent cost cutting measures have resulted in some improvement from the $20 million per quarter burn rate. Helbiz is in no better shape now than four months ago, despite tripling its share count.

Dilution tracker shows the potential dilution to be up as high as nearly 220 million. Authorized shares are 285 million, so HLBZ has the ability to dilute up to this limit before it must seek an increase and/or a reverse split at a future AGM. This leads into the next problem. HLBZ is running out of shares to dilute. If it kept on issuing shares in the $0.15 range, it would be out of the ability to raise capital after $10 million or so. And as I showed above, $10 million doesn't take Helbiz very far. It was desperate for something, anything to come along in order to raise the share price so the company can raise funds at, say, $0.50 instead of $0.15. This leads me into my next point about the CEO's behavior in the Fintwit sphere.

The behavior of the CEO on Twitter is making investors nervous

The communication of Salvatore Palella on Twitter has made some investors nervous. A scroll through his Twitter feed shows his blatant overuse of the hashtag #nakedshortwar while avoiding legitimate issues being raised about the financial state of the company. But there are some particularly troublesome tweets which I would like to highlight.

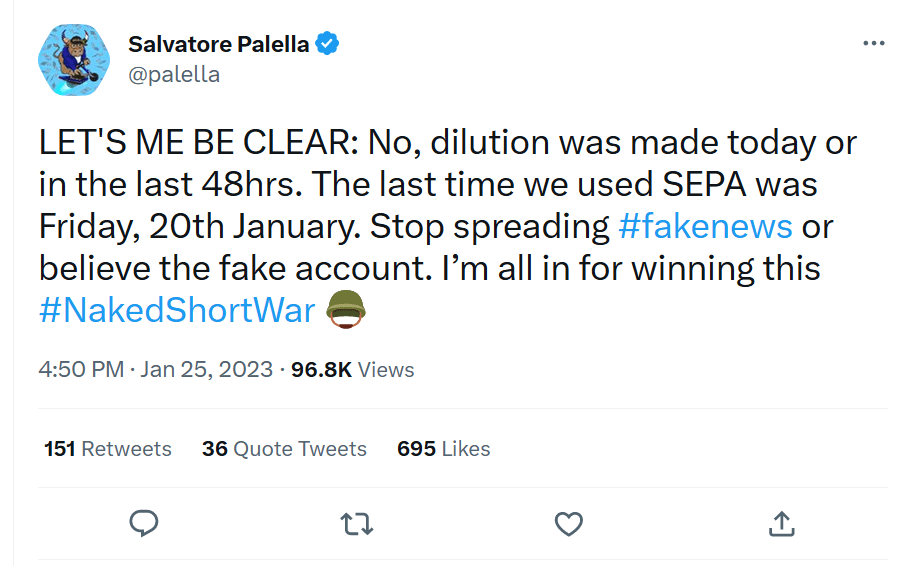

First this one sent on January 25th:

{kind=link}

Ignoring the unfortunately placed comma that implies the opposite, he is making light of the fact that the company did not dilute on January 25th when the last time they did dilute was January 20th. Does he expect shareholders to be bullish on a company that managed to stave off dilution for a whole two business days?

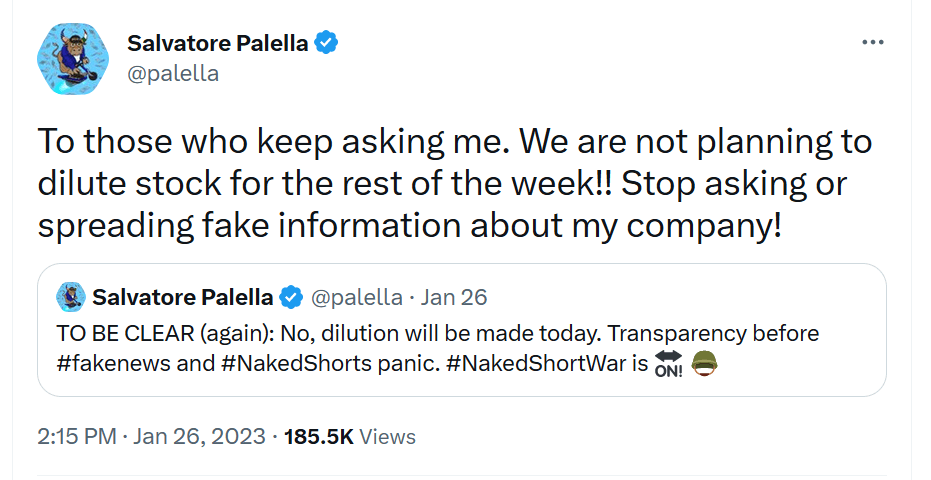

The next one I want to point out is this :

{kind=link}

He stated with great confidence that no dilution will be made for the rest of the week. Note that the tweet was sent at 2:16 pm on January 26th, or Thursday afternoon about two hours before market close. So he felt the need to reassure investors that no dilution will be undertaken for the next eight hours that the market will be open.

The last tweet I'd like to point out is about Yorkville:

{kind=link}

Even though these types of funds have ways of using related offshore entities in order to short shares, let's take him on his word and assume that Yorkville has not shorted any shares in its dealing with HLBZ. This is a total red herring. That does nothing to offset the fact any type of short squeeze thesis, whether real or manufactured, will be extremely hampered by the 10's of millions of shares issued to Yorkville at prices averaging in the low teens. Yorkville might never need to short sell in order to kill a rally. They can just sell their massive position accumulated over January through the SEPA.

Given the recent share issuance, the fact that HLBZ is still in a precarious financial state and that the company is nearing its authorized share count from which it can no longer issue shares, I believe that these conclusions can be reached with a fair amount of certainty:

1. Yorkville, regardless if it has shorted HLBZ shares in the past, has a very strong incentive to dump the shares it recently purchased through the SEPA between $0.11 and $0.16 at profits. Any short squeeze attempt led by retail traders will be greatly hampered because Yorkville is likely dumping into it. Retail investors aren't making rich naked shorts pay by buying up HLBZ stock. They are providing liquidity for easy profits for Yorkville, a rich fund that specializes in dilutive financing deals.

2. HLBZ is in desperate shape to raise as much funds as it can in order to continue operating. Riding the #nakedshortwar on the backs of others will enable it to a) maintain a good relationship with Yorkville and b) raise funds at $0.25 or $0.50 or $0.75 or whatever short term price pop allows it to. This is better than raising at $0.10 to $0.15 and hitting the authorized share count limit all for one or two more quarters of operations.

The CEO cannot commit to not diluting for more than a couple of days because he MUST dilute at any opportunity that offers a slightly better than worst case scenario. HLBZ has very few options to avoid this, and I strongly suggest to investors to make sure to see signs of these options being successfully undertaken before putting anything other than lotto money into this stock.

What must happen before a naked short investigation on HLBZ can be taken seriously

HLBZ has ridden the coattails of GNS's naked short investigation, but has been all talk and no action so far. HLBZ can start to be taken seriously by actually undertaking some of the actions of GNS's CEO Roger Hamilton. In my previous article, I pointed out that an updated forecast for 2023 and limiting of dilution would be two items I would like to see. Hamilton has since mentioned that no offerings are planned at the moment, though I have failed to get confirmation that the planned $7.5 at-the-market offering is being outright cancelled.

Genius announced guidance of $48 to $52 million in revenue, with EBITDA in the $0.5 to $1 million range. Given that this is a $5-$6 million improvement from EBITDA guidance of 2022, we can assume the net loss will also come down from its current run rate of ~$2 million per quarter. This will extend the company's cash runway, adding further confidence that dilution can be avoided for the foreseeable future. GNS has set a meeting for February 16th to vote on a share repurchase mandate. Finally, Roger Hamilton has provided an honest update to the planned special dividend for GNS.

Helbiz has not provided guidance showing improved financial performance, has not provided any real assurance of no dilution for any material length of time, and has made no serious steps in distributing a special dividend nor does it have the financial resources to do so.

Helbiz has much further to go to attaining breakeven operations compared to Genius, and will need financing in one form or another in order to continue operations. Instead of financing with equity, if the company was able to finance through non-dilutive methods such as a bank loan or long-term debt, that would increase the company's risk profile but would at least limit near-term dilution risk. A strategic partnership, joint venture or some other funding method by a larger player that didn't involve dumping tens of millions of HLBZ shares onto the market would also be acceptable. These are the things that investors need to look for before they can take any investigation into naked shorts by HLBZ seriously.

Conclusion: HLBZ will likely be diluting in the near future. If you want a company with a legitimate shot at short squeeze, stick with GNS.

I hope that my article has made it clear that HLBZ will very likely be diluting in the near future. The company hasn't undertaken any serious action to combat any perceived naked short attack. Helbiz's near term concern clearly lies with its ability to operate as a going concern. That involves raising funds for operations until it hits a point where it is self funding. Given that gross margins are negative, let alone adding in operating expenses, it has a very long and hard road ahead to get to that point.

Revenue stalled in Q3, and given that it is exiting unprofitable markets, we can assume revenue growth will continue to be stagnant in the near term. I outlined some ways the company can finance its operations without issuing shares, but all of these are long shots. I don't see any bank or lender issuing financing given the poor state of operations and balance sheet, nor do I see an easy near-term path to a partnership or joint venture in the e-scooter mobility space.

Helbiz will likely continue to dilute, which will completely negate any naked short war, if the company was even remotely serious with this initiative in the first place. On a final note, I challenge any HLBZ investors to confront the company with this article and see how it reacts. A positive and constructive reaction to the issues I raised and the challenges HLBZ is facing might be a sign to start taking HLBZ seriously. A defensive reaction will also show all that investors would need to know about this stock.

For further details see:

Helbiz Will Likely Continue To Dilute While Riding The Coattails Of The Naked Short Squeeze Investigation From Genius