HELE - Helen of Troy: Conservatively Priced For A Reason

2023-12-14 05:10:30 ET

Summary

- Helen of Troy manufactures and sells a wide range of consumer products with a large portfolio of brands.

- The company has achieved stable growth organically and through acquisitions, maintaining very stable margins over the years.

- The company has had several very weak quarters in terms of revenues, raising concerns about future growth.

- At the moment, the stock seems to be priced conservatively, in line with my expectations.

Helen of Troy (HELE) manufactures and sells consumer products in Home & Outdoors and Beauty & Wellness segments with products ranging from coffee makers, child seating, and food containers to shampoos, blood pressure monitors, and humidifiers - the company's offering is very complex. With the wide range of products, Helen of Troy also operates multiple brands , such as OXO, Hydro Flask, Osprey, Drybar, Braun, Honeywell, Revlon, and Curlsmith.

The stock has had an acceptable return in its past years. Over a ten-year period, the stock has appreciated at a CAGR of 8.2%. Helen of Troy hasn't been able to pay out dividends, as the company utilizes its cash flows in acquisitions and in the company's recent investments - keeping up and expanding such a range of products takes up a ton of capital.

{kind=link}

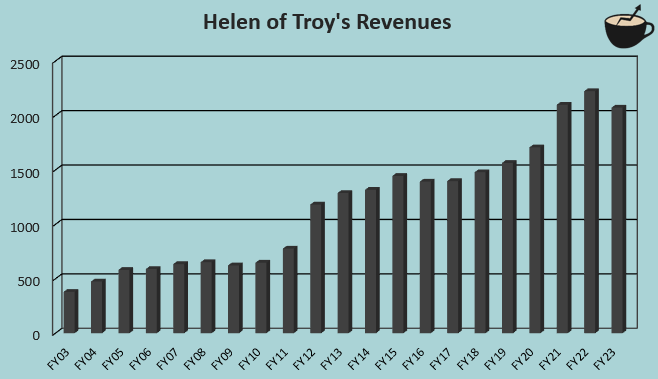

Long-Term Stability

As the company has held leading brands and expanded operations through acquisitions, Helen of Troy has mostly achieved stable growth. From FY2003 to FY2023, Helen of Troy's revenue CAGR is 8.9%, multiplying revenues in the past couple of decades.

{kind=link}

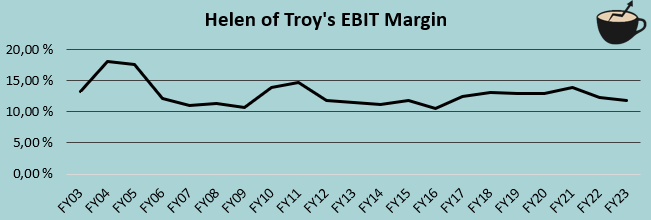

Along with the modest growth, Helen of Troy has achieved incredibly stable margins especially in the last decade. In the past decade from FY2014 to FY2023, the company's average EBIT margin has been 12.3%, with a current trailing EBIT margin of 12.6% . I believe that the stable margins are valuable for investors, as the predictability lowers Helen of Troy's risk levels.

{kind=link}

Lacking Growth in Recent Times

Helen of Troy has had significant acquisitions in the past couple of years. In the first half of 2022, the company completed two acquisitions, including the acquisition of Recipe Products , known for its Curlsmith haircare brand, for a consideration of $150 million, adding around $40 million to $42 million in revenues to Helen of Troy. A more significant acquisition was Helen of Troy's acquisition of Osprey Packs , an outdoors product manufacturer, for $414 million in cash. The Osprey acquisition added an estimated $155 million to $160 million in revenues, a meaningful amount to Helen of Troy's revenues of around $2 billion.

Despite the acquisitions, Helen of Troy's growth has been very bad in recent quarters - in FY2023, revenues decreased by -6.8%, and the negative momentum has continued into FY2024 with a H1 revenue decrease of -6.1%. Helen of Troy has attributed the weak revenue performance in past years mainly to supply chain disruptions, weakening consumer demand, and retailers' inventory balancing. In Q2/FY2024, revenues still decreased by -5.7%, but in the earnings call for the quarter, no mention of the previously mentioned factors were mentioned; rather, CEO Julien Mininberg seems enthusiastic about the achieved level. I suggest to keep a close eye on the revenue performance - if the reason for revenue declines are partly due to a fundamentally weak product portfolio, the revenue decreases could continue far into the future. Adding to the concerns, Helen of Troy has spent an increasing amount in capital expenditures from FY2021 forward without achieving meaningful organic growth.

A small part of the reason to decreasing revenues in past years seems to be due to the company's divestment of 12 personal care brands in FY2022, but it doesn't seem to be the main reason - Helen of Troy only seemed to gain around $45 million from the divestment, as can be seen on the company's cash flow statement in FY2022. Comparison figures already haven't included revenues from the divestment for several quarters, but the revenue declines have continued regardless.

The company held an investor day in October, where the company guided for an annual organic growth of 3% to 4% in sales, along with 30 bps to 40 bps in adjusted EBITDA margin expansion - Helen of Troy's management seems to have a good belief in future earnings growth. Currently, the company is at the end of its long-term strategic plan's phase 2:

2023 Investor Day Presentation

In the investor day, Helen of Troy seems to praise its brand portfolio, which the company plans to utilize for future growth through international expansion and other initiatives. The methods for achieving growth seem partly unconvincing until the targeted financials show progress, though - for example, being customer obsessed and extending brands don't seem like cutting-edge tactics for achieving a competitive advantage.

2023 Investor Day Presentation

The company does guide that revenues should scale back to a 3.5% growth in Q4 of FY2024. If achieved, the quarter could signal a turn back to growth. For the time being, I am quite conservative about the company's revenue growth.

Valuation

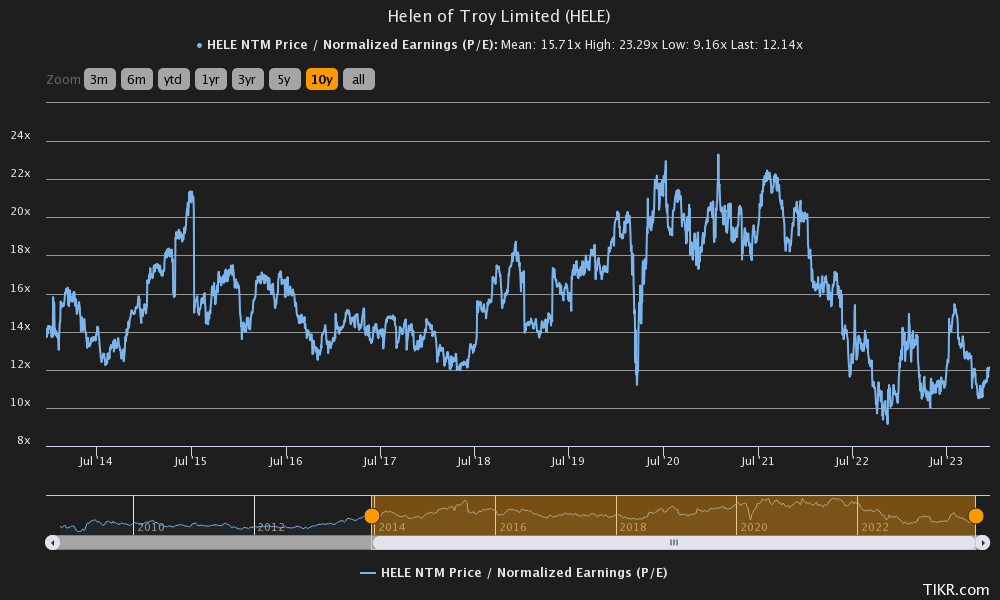

Helen of Troy's stock price seems to price in quite weak expectations - the stock trades at a forward P/E multiple of 12.1, near the company's ten-year bottom:

{kind=link}

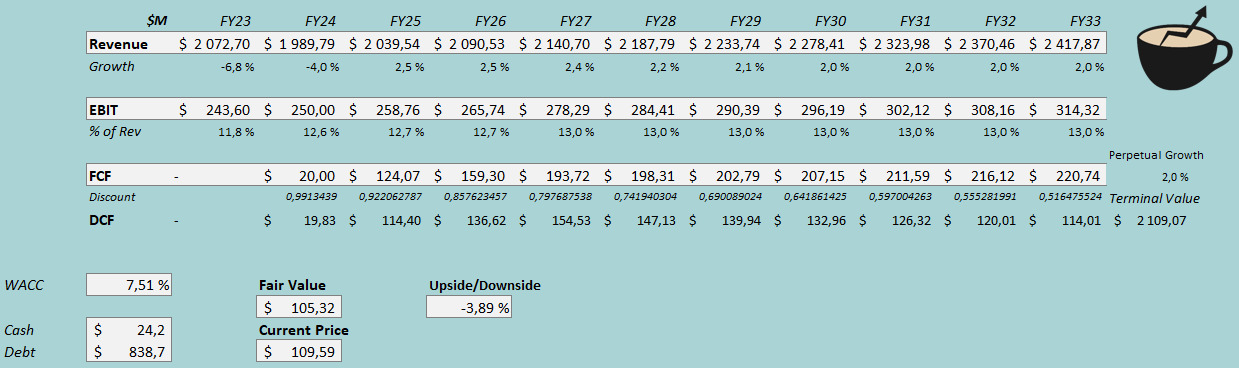

To estimate a rough fair value for the stock with given prospects, I constructed a discounted cash flow model as usual. In the model, I estimate a stable performance in the future - after a FY2024 revenue decrease of -4%, in line with the company's guidance, I estimate a revenue growth of 2.5% that slows down into a perpetual growth of 2% in steps. For margins, I estimate very slight leverage - after a FY2024 EBIT margin estimate of 12.6%, I estimate the margin to rise by 0.4 percentage points into a sustained level of 13.0%. Helen of Troy has had significant capital expenditures in recent years, and I estimate the investments to continue decreasingly into FY2026, after which the company's cash flow conversion improves into a good level.

With the mentioned estimates along with a cost of capital of 7.51%, the DCF model estimates Helen of Troy's fair value at $105.32. The estimated value is very near Helen of Troy's stock price at the time of writing - the stock seems to be priced for a stable future.

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2/FY2024, Helen of Troy had $13.7 million in interest expenses. With the company's current amount of interest-bearing debt, Helen of Troy's annualized interest rate comes up to 6.51%. The company leverages a good amount of debt with around $839 million currently in long-term debt . For the long term, I estimate a debt-to-equity ratio of 40%. For the risk-free rate on the cost of equity side, I use the United States' 10-year bond. The equity risk premium of 5.91% is Professor Aswath Damodaran's latest estimate for the United States, made in July. Yahoo Finance estimates Helen of Troy's beta at a figure of 0.71 . Finally, I add a small liquidity premium of 0.2%, crafting a cost of equity of 8.57% and a WACC of 7.51%.

Takeaway

Helen of Troy seems to be priced for a stable financial future. The company recently held an investor day, where the company underlined its modest growth ambitions. After a weak revenue performance in recent quarters, I am personally careful about the company's growth - after several quarters with negative growth, the company's capabilities don't seem too great. Still, as Helen of Troy has proven great margin stability and guides for revenue growth beginning in Q4, I don't see the company as a very weak investment - my DCF model estimates the stock to be roughly fairly valued. For the time being, I have a hold rating.

For further details see:

Helen of Troy: Conservatively Priced For A Reason