HELE - Helen of Troy: Q3 Results Beat Expectations Shares Fairly Valued

2024-01-08 20:41:28 ET

Summary

- Osprey and Hydro Flask owner, Helen of Troy, traded higher following results that topped expectations.

- In particular, strength in the company’s Home and Outdoor unit and continued margin expansion were viewed favorably.

- Topline strength, however, was offset elsewhere, namely in the company’s Wellness unit, which faced headwinds from a softer start to the cold, cough, and flu season.

- Given current trading values, I remain neutral on the stock following results.

Helen of Troy ( HELE ), the owner of a diversified portfolio of consumer product brands including Osprey, Vicks, and Hydro Flask, ended Monday’s trading day nearly 5% higher following the release of its Q3 results, which came in ahead of expectations on both revenues and earnings.

In prior coverage of HELE, I expressed neutrality despite the stock’s 18% rise immediately following the release of its first fiscal quarter results. While I viewed margin expansion and strength in key brands favorably, I felt certain aspects of the business, such as HELE’s Home/Outdoor unit, were at risk of competitive threat in an environment with shifting consumer priorities.

Though results surpassed expectations in the current quarter, I still view declining overall sales as a key headwind for HELE. In my view, at about 13x forward earnings, the stock trades fairly in the current market environment.

HELE Stock Key Metrics

Shares in HELE have returned about 9.5% over the past month. Nevertheless, performance has been more muted over the past one year, with gains of under 4%. The broader S&P ( SPY ), meanwhile, is up over 20% in the same period.

Seeking Alpha - Basic Trading Data Of HELE Stock

{kind=link}

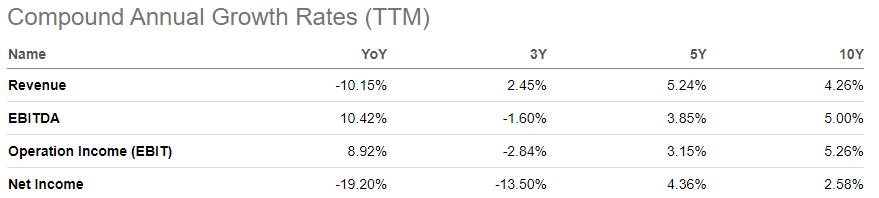

The longer-term underperformance could be attributable to overall sales weakness. Though results have surpassed expectations in recent periods, sales growth is still negative. This ultimately offsets strength elsewhere, namely margin expansion.

Seeking Alpha - HELE Stock Growth Rates For Key Reportable Operating Metrics

{kind=link}

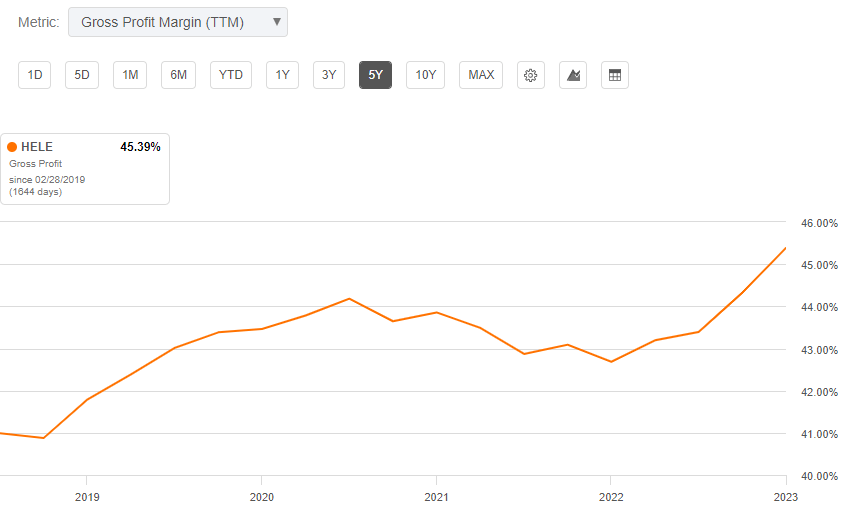

Promising progress in HELE’s operational restructuring strategy, known as Pegasus, has contributed to rising gross margins. Most recently, HELE reported a consolidated gross profit rate of 48% in Q3. This was 210 basis points (“bps”) improved from the same period last year.

Seeking Alpha - Chart Of HELE Stock Gross Margins Over Time

{kind=link}

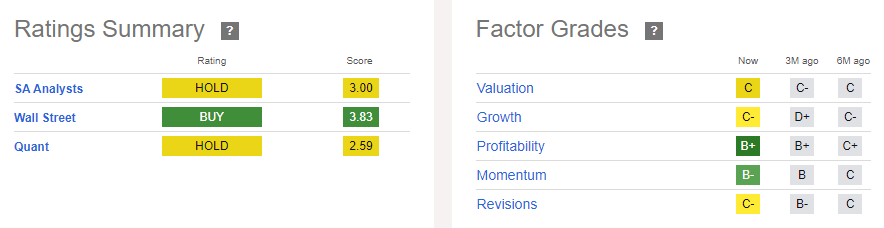

At about 13x forward earnings, HELE stock is viewed neutrally by both Seeking Alpha’s (“SA”) quant ratings and by most of the author community. Wall Street, on the other hand, is significantly more bullish, with an average price target of just under $150/share for the stock. The bullishness likely stems from the company’s expanding margin profile, as well as an improving consumer backdrop.

Seeking Alpha - Ratings Summary Of HELE Stock

{kind=link}

Recap Of HELE Q3 Results

For the fiscal Q3 reporting period, HELE reported a YOY decline in consolidated topline sales of 1.6%. Though down, the decline was less bad than feared considering HELE previously guided for a 2% to 4% decline.

Supporting the topline was a strength in HELE’s Home & Outdoor unit. Net sales in the segment increased 3.1%. This included organic growth of 2%. Driving sales was the club channel, as well as consumer interest in new product introductions, particularly surrounding Hydro Flask, which benefited from the rollout of HELE’s new travel tumblers. On a similar basis, Osprey continued to benefit from outdoor travel demand, resulting in a greater uptake of new product offerings during the quarter.

Offsetting sales strength in the Home & Outdoor unit was HELE’s Beauty and Wellness segment, which reported a net sales decline of 4.9%, driven primarily by lower sales of hair appliances. Additionally, commentary from incoming CEO Noel Geoffroy also indicated a softer start to the cough, cold, and flu season. This in turn negatively impacted sales of HELE’s humidification and thermometry products.

While momentum in sales continues to be a drag on overall results, HELE has made measurable strides in improving its margin profile. The positive strength continued in Q3, as HELE reported an overall gross profit rate of 48%, 210bps improved over the same period last year. Similar to others across various industries, HELE benefitted from a more favorable and accommodative freight environment.

And though an overall unfavorable sales mix provided a headwind to the margin rate, this was offset by a more favorable customer mix within the Home and Outdoor unit.

Within the bottom line, the margin performance was more mixed. While overall operating margins were up significantly in the current quarter, the margin rate was assisted by a large gain realized on the sale of HELE’s facility in El Paso. Barring the sale, adjusted operating margins were in fact down 30bps from last year to a rate of 16.3%.

Outlook For HELE Stock

Looking ahead, the HELE management team provided a refined outlook for both net sales and adjusted EPS. On the sales front, HELE expects continued uncertainty on consumer spending for discretionary product offerings to remain a headwind.

This headwind is compounded by a softer cold, cough, and flu season, which is expected to negatively impact HELE’s Health and Beauty segment. Better-than-feared YTD performance, however, enabled HELE to revise higher the low end of their net sales target to +$1.975B from +$1.965B previously. This somewhat mitigates the downward revision to the top-end from +$2.015B to the current +$2.0B.

Adjusted EBITDA was also lowered to reflect HELE’s lower adjusted operating income due to a less favorable overall sales mix and higher growth investments compared to initial expectations.

Despite the various adjustments to the outlook, the midpoint of the revised outlook for both net sales and adjusted EPS is still about the same as what was originally provided at the beginning of the fiscal year. This could be viewed in a positive light, given the deterioration in the operating environment since then.

Is HELE Stock A Buy, Sell, Or Hold?

Since my last update on HELE, results have come in ahead of my expectations. Previously, I had expressed reservation regarding the competitive threats facing HELE’s Home & Outdoor unit. Current results, which exhibited sales growth in the unit contradict my viewpoint. And an evolving consumer backdrop, which includes a lower inflationary environment, could bode well for the unit moving forward.

Despite the positive note, overall sales are still expected to decline in the low-single-digit percentage range. In my view, there needs to be a more pronounced shift in the sales environment to warrant a more bullish position on the stock. At about 13x forward earnings, HELE appears fairly valued in the current environment.

Notable progress in HELE’s restructuring program, which is providing a positive runway for margin expansion, as well as leadership transition provide HELE with the ingredients for medium to long-term success. But until there is further progress on overall sales growth, I would remain hesitant to initiate new or added positioning in the stock.

For further details see:

Helen of Troy: Q3 Results Beat Expectations, Shares Fairly Valued