EADSY - Hexcel Stock Is Overvalued

2023-04-26 10:41:01 ET

Summary

- Hexcel stock shows appreciable growth in aerospace and defense revenues while industrial revenues remain underwhelming.

- Hexcel stock has run ahead of its revenue and earnings recovery.

- Enterprise-to-EBITDA valuation shows that Hexcel at best is valued fairly and overvalued in most other cases.

I have been following Hexcel Corporation ( HXL ) for some years. I believe that the company has a promising product portfolio, but partially due to the pandemic value generation has been underwhelming. In this report, I explain why I am not upgrading from Hold to Buy but do see long-term value for HXL shares. I will also comment on the company’s latest earnings release.

What Does Hexcel Company Do?

For those not familiar with Hexcel, it might be good to provide an introduction to the company’s operations. Hexcel Corporation provides composite materials and structures. These days the reduction of greenhouse gas emissions plays an important role. Composites provide lower-weight solutions, thereby reducing fuel consumption in, for instance, cars and aircraft. Furthermore, the company provides material solutions for the wind energy market. So, with greenhouse gas emission reductions in mind, there are significant opportunities. On each of these sectors where Hexcel could provide solutions, there are remarks to be placed, which I will do when discussing my investment view on Hexcel Corporation.

Aerospace and Defense Boost Revenues

{kind=link}

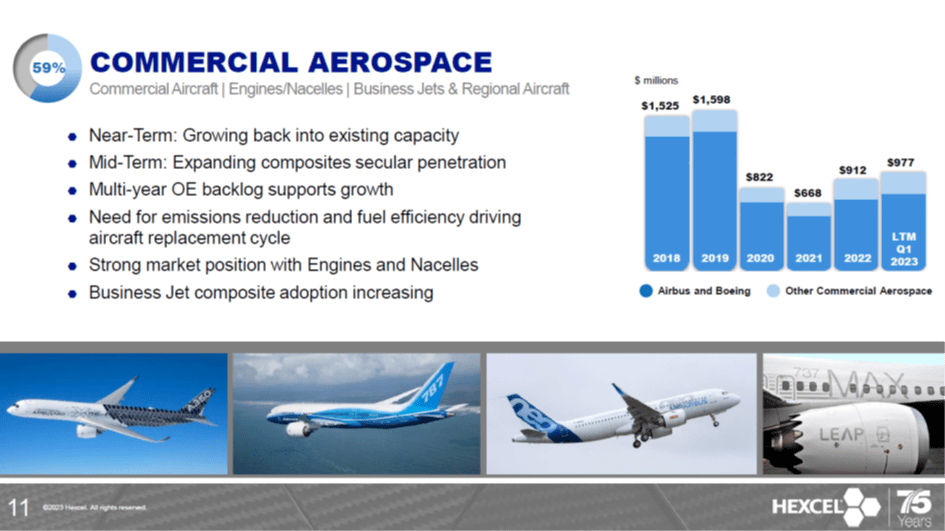

On any normal day, the commercial aerospace segment provides the company with 70% of the revenues. However, we haven’t had a normal year since 2019. In 2019, the Boeing 737 MAX crisis sparked a reduction in the production rate. Hexcel provides the materials used to manufacture the acoustic inner barrels. While the reduction in production was significant, the relatively low shipset value and the strong production rates for other commercial aircraft programs did not lead to a reduction in revenues at the time. The subsequent year, however, was different as production of the Boeing 737 MAX was halted and the pandemic eroded demand for airplanes and the ability to manufacture commercial aircraft, and in 2021 things did not get much better.

However, since 2022 the recovery has started with a 37% increase in revenues and the latest twelve-month trailing numbers show another 7% increase in sales. The twelve-month trailing numbers mask the actual year-over-year improvements, so I will also be highlighting these numbers. The Q1 2023 revenues for the commercial aerospace segment were $284.5 million up 30% year-over-year accounting for 62.2% of the revenues. So, we do see that from revenue perspective the company is closing in on the 70% revenue share that commercial aerospace normally has.

LTM Q1 2023 revenues still are only 61% recovered. As Boeing ( BA ) and Airbus ( EADSF ) increase single aisle production we will be seeing things improving and those improvements are happening now but it won’t be until mid-decade before production has recovered. Possibly the bigger step ups in revenues will come from higher wide body production but that just like single aisle production is something that will probably happen around mid-decade on the condition that air travel demand does not decelerate such that air travel demand falls significantly. So, we do see the sales improvement and we see the drivers for higher revenues but those will take around 3 years to recover and even then, it remains to be seen whether wide body production will truly be back at previous levels.

{kind=link}

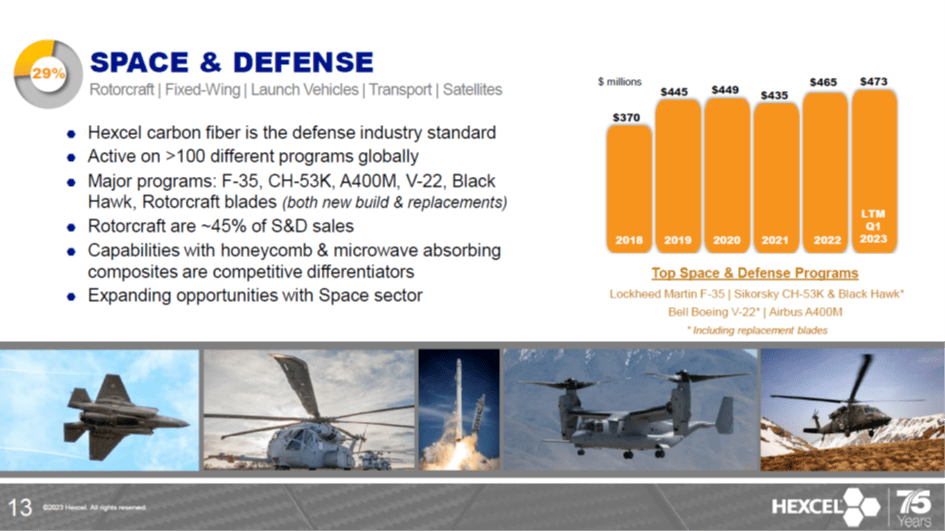

The recurring story for Defense is that it is the stable factor in the revenue mix with modest growth opportunities and the LTM Q1 2023 of $473 up less than 2% portray this. With demand for defense equipment increasing, this could very well be a growth opportunity. However, before the first interests in defense equipment results in contracts it will likely already be 2024 and after that a delivery position needs to be available. As a material supplier, Hexcel is positioned well to benefit the earliest from this uptick, but it will likely be years before we see a translation from demand to supplier toplines. Hexcel has some growth platforms such as the CH-53K and Future Vertical Lift that can add to the revenues. The F-35 is high in demand internationally, but it remains to be seen whether that can actually be a longer-term layer on top of existing production plans.

Looking at solely the first quarter, we saw 6.8% higher sales and 7.6% on constant currency as some growth platforms are already pushing sales higher.

{kind=link}

The Industrial segment remains the ugly duckling of Hexcel with a 3.5% sales decline. The big driver of the industrial used to be wind energy led by supply work for Vestas, but ever since that work has been lost Hexcel is busy reinventing its industrials segment. The company is pivoting away from wind energy to other markets such as consumer electronics, marine, and automotive, but we are not given any kind of insights on the trajectory of those sales segments and this pivot won’ happen overnight. The quarterly revenues of $47 million marking a 9.1% constant currency decline with wind energy sales declining partially offset by other parts of the segment also show this.

Hexcel Stock Runs Ahead Of Recovery Curve

{kind=link}

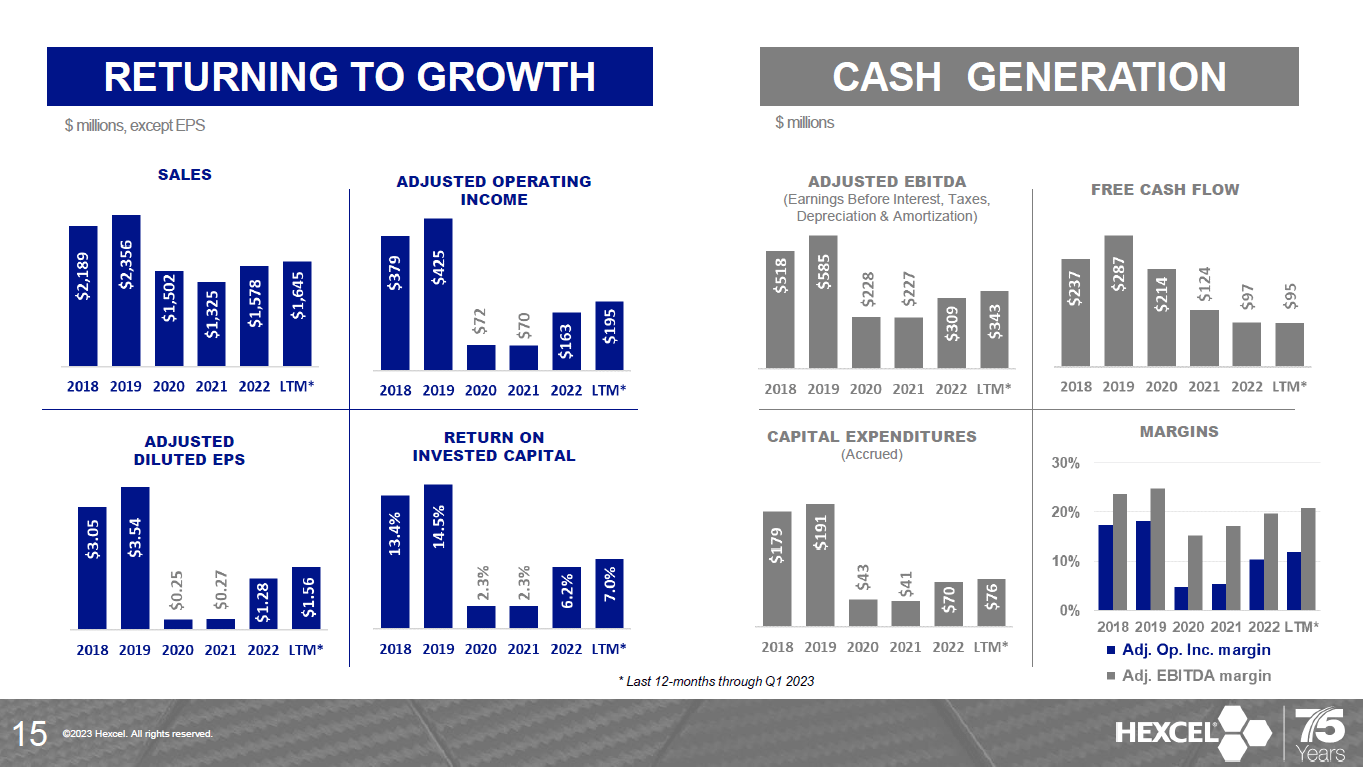

Revenues have recovered 70%, while adjusted operating income is 46% recovered and adjusted EBITDA is 59% recovered and free cash flow has recovered 33%. So, realistically Hexcel is still years away from recovering to pre-pandemic levels. That is the case when we look at the recovery pace and that is the case when we look at when certain commercial programs start ramping up revenue contributions and defense equipment demand can start translating into purchase orders for suppliers. The pre-pandemic share price for Hexcel was in the $80-$85 range and its current share price is $72.40. On nearly identical share counts, the share price has recovered by 85 to 90 percent far ahead of revenue or earnings recovery. To me that indicates that a lot of the future growth is already priced in.

{kind=link}

For the full year, Hexcel maintained its guidance of $1.725 billion to $1.825 billion in sales. Commercial sales will be around 58% of the sales at roughly $1 billion to $1.06 billon, pointing at 16% sales growth, while defense will have 29% of the pie valued at $500 million to $530 million, pointing at 14% sales growth. The Industrial segment will be around 13% of the sales, indicating $224.25 million to $237 million in sales and indicating a year-over-year growth of 18%. The markets like the Q1 results that showed 17.2% higher sales and adjusted operating income doubling which was ahead of the 9% to 16% guidance that Hexcel has provided. The positive surprise next to the higher sales were the improved margins of 13.8% compared to 8% last year. So, the 2023 Q1 results were good but it was not met with a guidance improvement. So, either the company is saving that up for later this year or despite a strong start of the year the remainder of the year will not be equally strong. It does seem that the market has pre-sorted for a guidance improvement later this year but to me it seems like that is pulling a lot of future results and recovery forward while the share prices are already running ahead of the recovery progress.

So, I see the value, but Hexcel Corporation shares have gotten a bit ahead of the results, I believe. That creates some risks, especially since the gap from 2023 sales for commercial aerospace segment to pre-pandemic sales of $1.6 billion is one that needs to be filled, with uncertain production plans depending primarily on wide body production rates.

Is Hexcel A Good Stock To Buy?

| Valuation Hexcel |

| Market Capitalization [$ bn] |

| $ 6.10 |

| Total debt [$ bn] |

| $ 0.77 |

| Cash and equivalents [$ bn] |

| $ 0.11 |

| Total Enterprise Value [$ bn] |

| $ 6.76 |

| EBITDA 2023 [$ bn] |

| $ 0.36 |

| EV/EBITDA |

| 18.6x |

| WACC |

| 8.5% |

| Current price |

| $ 72.40 |

| Median |

| Current |

| Industry |

| EV/EBITDA |

| 13.34 |

| 18.62 |

| 15.42 |

| Price target |

| $ 47.92 |

| $ 66.88 |

| $ 55.39 |

| Upside |

| -34% |

| -8% |

| -23% |

A valuation of Hexcel gives us a $6.8 billion enterprise value and with $1.78 billion in expected sales at an EBITDA margin of 20.5% gives an EBITDA of $364 million and an enterprise-to-EBITDA multiple of 18.6x which is in line with the current traded multiple indicating that the company is valued fairly and slightly overvalued when incorporating a weighted average cost of capital 8.5%, the stock is overvalued by 8%. Compared to its median, it is even 34% overvalued and 23% overvalued when comparing the EV/EBITDA multiple to the aerospace and defense industry. I will hand it to Hexcel that their products are high in demand and basically every big commercial or defense program will use their product so an elevated multiple might be justified but that still means that means that the company at best is fully valued for 2023 and slightly overvalued when we correct the share price with WACC.

Conclusion: Hexcel Is A Great Company With A Not So Great Stock Price

I like Hexcel, when I look at the company’s presentations and having an aerospace background I can understand why people are invested in the company. However, at the same time the stock price has run ahead of its revenue and earnings and its actually valued fairly and perhaps overvalued with 2023 earnings in mind. Which really indicates that from fundamental point of view there is no reason to buy the company’s stock for its 2023 results. If you buy, then you buy it at a premium and perhaps that is a premium that the company deserves based on its products.

Either way, looking at what Hexcel Corporation offers to the market, I do believe that for the long term this can be an extremely rewarding opportunity but you just have to be OK with buying the stock at a higher price than is justified by the fundamentals as the stock seems to be excessively forward-looking, meaning that fair value won’t be reached unless the stock corrects somewhat.

For further details see:

Hexcel Stock Is Overvalued