XLU - High Interest Rates Are A Gift To Dividend Investors

2023-10-21 08:30:00 ET

Summary

- High interest rates are a gift for long-term dividend investors, as it allows them to buy high-quality dividend stocks at lower prices and higher yields.

- Many income investors have sold dividend stocks to invest in bonds, but this is short-sighted as bonds offer flat income with no protection from inflation.

- There are three reasons why interest rates are likely to fall in 2024: inflation has already been tamed, consumer spending is weakening, and the housing market requires lower rates to break the impasse.

- I highlight four of my favorite dividend stock buys right now in four sectors that investors are underweight.

High interest rates seem like an unalloyed negative for most dividend stocks. But in reality, they are a gift for long-term dividend investors.

That is especially true for investors like me who are focused on generating the safest and fastest-growing passive income stream possible.

Many dividend stocks have sold off heavily as the market frets over increased costs of debt and income investors dump stocks in exchange for the ostensible safety of bonds.

However, as I'll argue below, the market's fretting over surging interest expenses looks to be overdone, as there is strong evidence that we are actually in a "not-that-much-higher-for-not-that-much-longer" environment. What's more, income investors' newfound favor toward bonds over dividend stocks strikes me as short-sighted, and there will almost certainly be a reversal here if and when interest rates and bond yields start coming down.

The Short-Sightedness of Choosing Bonds Over Dividend Growth Stocks

A great many income-oriented investors have sold dividend stocks in the real estate, utilities, regional banking, and consumer staples sectors over the last year in order to invest in bonds instead.

The two hardest hit sectors in terms of investment outflows have undoubtedly been real estate and regional banks. See the chart below, showing the total percentage change in AUM for various ETFs since April 1, 2022:

- iShares 20+ Year Treasury Bond ETF ( TLT )

- SPDR Consumer Staples ETF ( XLP )

- SPDR Utilities ETF ( XLU )

- Vanguard Real Estate ETF ( VNQ )

- SPDR S&P Regional Banking ETF ( KRE )

AUM has declined by 41% for VNQ since April 1, 2022, compared to a 34% drop in price/market cap, meaning that 7 percentage points of the drop in AUM was caused by outflows.

For KRE, there has been about a 42% drop in price/market cap since April 1, 2022, which means 11 percentage points of the 53% drop in AUM came from outflows.

Meanwhile, XLP has dropped about 12% and XLU has dropped 23% in price/market cap since April 1, 2022, compared to a 6% increase and 13% decreased in AUM, respectively, which means that there have been investment inflows into these consumer staples and utilities ETFs.

Lastly, compare this to TLT's 86% increase in AUM on top of a 37% drop in price/market cap since April 1, 2022. Clearly, there has been a massive investment inflow into bonds, or at least certain bonds.

While everyone's situation, goals, and risk tolerance is different, I think investors selling dividend stocks at 3-5% dividend yields and reinvesting into bonds are being short-sighted.

Yes, bond coupons are safer than common stock dividends, but they are also guaranteed to stay flat . This means that they have zero protection from inflation.

Consider, for example, that lending your money to Uncle Sam for 10 years may come with it a nearly 5% nominal yield, but if you assume an inflation rate of about 2.5%, your real yield drops to about 2.5%.

Even this does not accurately capture the slow purchasing power erosion of inflation, because bonds pay a fixed amount of income while inflation is the rate of change in consumer prices . Inflation slowly whittles away the purchasing power of bonds' fixed income streams over time.

Dividend stocks, on the other hand, typically raise their dividends at a faster rate than inflation over time.

To cherry-pick one of the best dividend growth ETFs for the sake of illustration, take the Schwab US Dividend Equity ETF ( SCHD ), which has grown its dividend payout at a rate many times faster than inflation over the last decade.

To be clear, SCHD doesn't just own any and all dividend stocks. Its methodology seeks to systematically pick the best dividend-paying companies through various quality and dividend growth metrics.

That's why I have previously argued that SCHD is "A Dividend Growth Investor's Dream ETF."

Unlike directly owning a bond, which offers only a fixed income (the coupon), dividend stocks offer a growing income stream through two mechanisms:

- Dividend increases given by the company as it grows its earnings

- Reinvesting dividends immediately, which you can't usually do with bonds

Granted, retirees withdrawing 100% of their portfolio income for living expenses can't take advantage of that second mechanism of income growth (reinvestment of dividends), but that is why I advocate retiring only once one's passive income* reaches at least 125% of one's desired living expenses, if possible.

*Including non-investment sources of income such as Social Security, pension, etc.

Reinvestment of dividends is a powerful mechanism for income growth that should be continued at least partly into retirement if at all possible.

The bottom line here is that, in my humble opinion, income-oriented investors choosing bonds over dividend stocks are making a short-sighted tradeoff that they will reverse if and when bond yields begin falling.

" But the Fed keeps saying 'higher for longer! '" you vehemently object. " The selloff in dividend stocks has only just begun! "

The Fed has certainly managed to raise rates higher than I thought they could and keep them there longer than I thought they could. But I believe "higher" won't be that much higher at this point, and "longer" won't last that much longer.

Three Reasons Interest Rates Should Fall in 2024

As I argued in " Buy REITs Before Everyone Else Does ," the Fed has an atrocious track record of achieving soft landings.

It's not that they are necessarily bad at their jobs or that someone else could perform monetary policy better. (I certainly couldn't!) It's that no single person or coterie of people, however smart, can accurately predict where the economy is going or even how their policies will impact the economy. It's too complicated an ecosystem for humans to master.

Here are three stark reasons I see that the Fed's policy rate and other interest rates will likely fall next year, probably sooner than most think.

1. Inflation Has Already Been Tamed

As I've explained multiple times in the past, such as in the article linked just above, the Fed is looking at old data when it comes to housing or "shelter" inflation. The Bureau of Labor Statistics' shelter inflation metric lags real-time changes in housing costs by about a year.

This is a big reason why the Fed was so late to begin raising interest rates. The rest of America knew inflation was taking off, but the Fed's data wasn't showing any significant uptick in inflation. That's because 35% of the headline CPI and ~40% of core PCE comes from the "shelter" component, which lagged real-time housing cost changes by about 12 months (see the bottom chart below).

If you exchange the BLS shelter inflation metric with real-time housing price changes, inflation is already back below the Fed's 2% target for both headline and core.

David Schwartz via X

This isn't an attempt to manipulate inflation data to get a number that I would prefer. It is manipulating the inflation data to get a more accurate picture of reality.

Unless non-shelter consumer prices surge higher in the coming months/quarters, this lagging shelter component of the CPI/PCE will put increasing downward pressure on inflation metrics going forward until inflation overshoots the Fed's target and ends up somewhere well below 2%.

2. Consumer Spending Is Weakening

There is good reason to believe that non-shelter consumer prices are unlikely to rise significantly from here. That is because, despite all the talk about a "strong consumer," the trends make clear that the American consumer is weakening.

The massive consumer spending spree over the last few years didn't come from a naturally healthy economy. It came from unprecedented levels of government stimulus (artificially high aggregate demand) sloshing through the system at a time when output and imports (aggregate supply) were lower than usual for pandemic-related reasons.

This was the primary cause of the surge in consumer prices, not a strong labor market or wage growth.

That's why total personal income is 22% higher today than it was 5 years ago (just a touch higher than CPI's 21% increase), while total employment is only 1.7% higher.

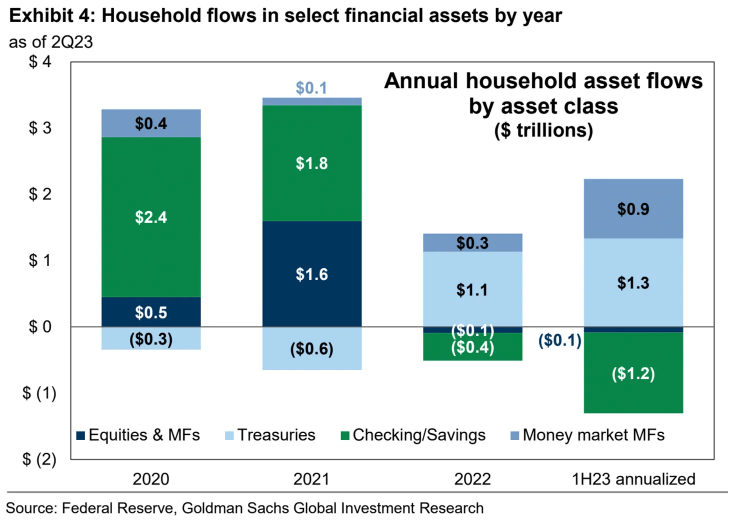

You can see the big spikes in disposable income in 2020 and 2021 from government stimulus.

Most of that stimmy money went into households' bank accounts in 2020 and 2021, as you can see in the chart below.

{kind=link}

But in 2022 and 2023, there has been an outflow of that money as households have spent it or invested it in bonds and money market funds.

Almost exactly in line with recent data showing that roughly 60% of Americans live paycheck to paycheck, 59% of Americans say that they have depleted all or most of their pandemic-era savings, while 41% (overwhelmingly from higher-income households) have hardly even touched it.

Daily Chartbook

This ~60% of Americans living paycheck to paycheck are the reason why credit card debt is soaring to new highs and will continue to do so as the holiday shopping season approaches and student debt payments resume.

The bottom line here is that the inflationary surge of the last few years was fueled by cash-rich consumers who are now largely becoming quite cash poor. This means that demand will soften, giving businesses less room to raise prices.

The inflationary surge is over, folks. This ain't the 1970s.

3. The Functioning of The Housing Market Requires Lower Rates

As I explained in "' Higher For Longer' Is Totally Unsustainable ," the housing market has become largely frozen in a stalemate between potential buyers and potential sellers.

Potential buyers have been effectively locked out of the market, unless they enjoy very high incomes or have very large down payments.

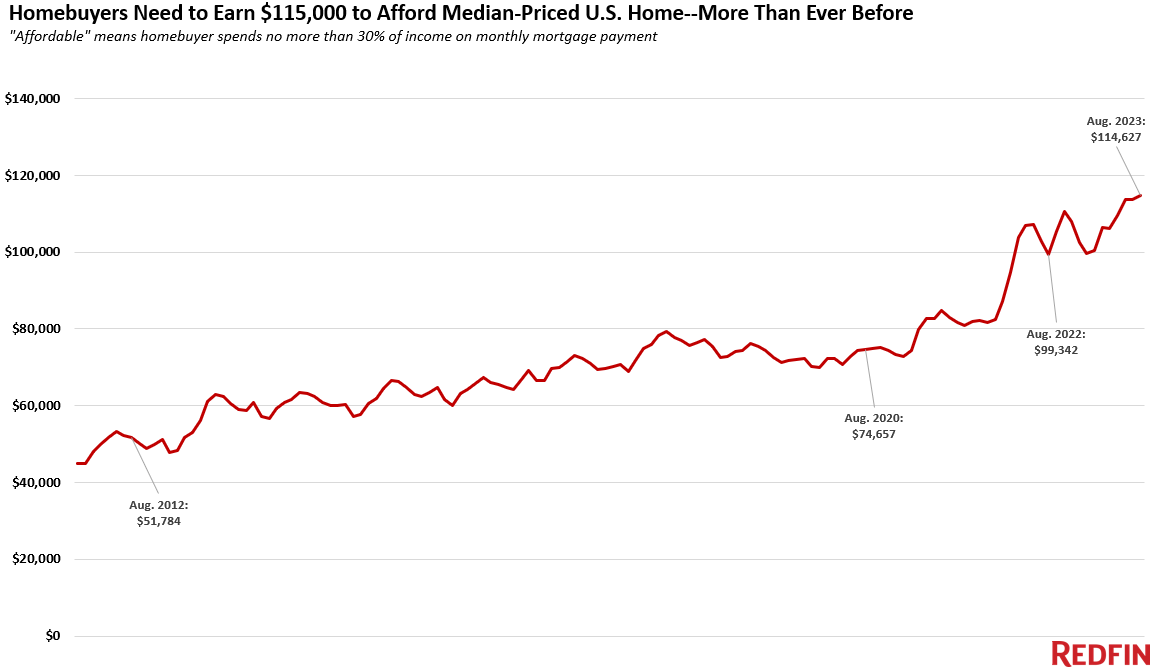

{kind=link}

As of August 2023, the income required to buy the median-priced home without spending more than 30% of one's total income on the monthly mortgage reached nearly $115,000. Surely it has gone higher since then, as home prices have held steady while mortgage rates have soared up to almost 8%.

Demand for mortgages is at its lowest level since 1995.

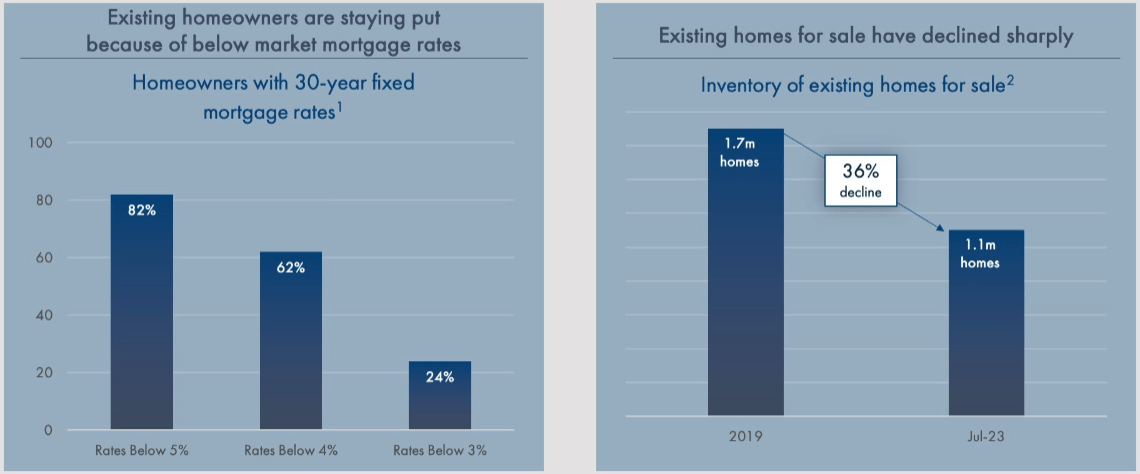

Meanwhile, homeowners with mortgages in place are not eager to sell their house and buy a new one elsewhere, because the vast majority of them have locked in a 30-year mortgage rate well below the current level.

{kind=link}

Hence we find that home sales volume has dropped to its lowest level since the Great Financial Crisis.

Normally, when home sales volume plummets, home prices fall as well, because it is caused by plummeting demand from buyers. But in this case, both buyer demand and seller supply have dried up in unison, keeping home prices stable if not slightly rising.

What would break this impasse? In my estimation, it would require lower mortgage rates, which would in turn probably require the Fed to reverse course on its higher-for-longer warpath.

Buy When Others Are Despondently (Or Short-Sightedly) Selling

To my mind, the above line of reasoning leads me to believe that the current high interest rates are a gift to dividend investors.

It has given investors the opportunity to buy high-quality dividend growth stocks at lower prices and therefore higher dividend yields. In my opinion, a great many investors who are not buying dividend stocks right now, favoring bonds or cash instead, will regret it in a year or two.

My personal investment strategy, which I would commend to almost anyone, has four simple steps:

- Buy high-quality companies

- that pay a growing dividend

- at a discount to fair value (and thus an attractive dividend yield )

- and wait patiently as they compound over time .

Where should one look for the best deals and greatest discounts today?

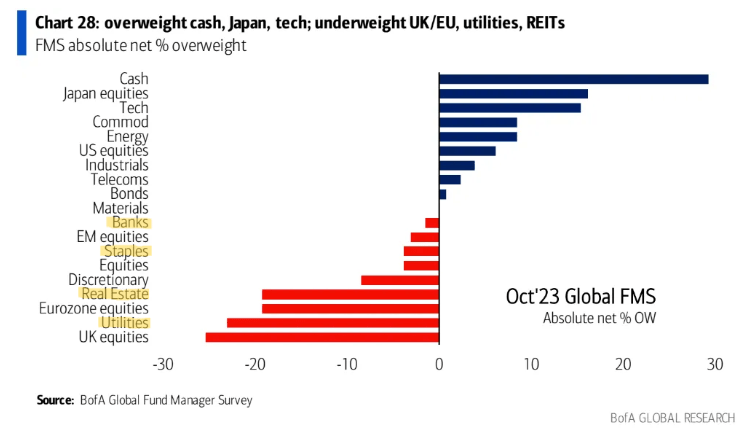

I'd suggest running toward the direction that most investors are running from . According to the Bank of America Global Fund Manager Survey for October 2023, professional investors are underweight four sectors in which dividend stocks tend to be found.

{kind=link}

Banks, staples, real estate, and utilities are underweight in fund managers' portfolios, and I imagine they have become underweight in many individual investors' portfolios as well.

One of my favorite dividend-growing bank stocks right now is Cullen/Frost Bankers ( CFR ), the largest Texas-focused regional bank with a strong and growing market position in most of the Lone Star State's largest cities. The bank has a 29-year dividend growth streak and now offers a nearly 4.3% dividend yield, compared to its 5-year average of 2.9%.

You can read more in my recent pitch for CFR here .

One of my favorite consumer staples stocks to buy right now is PepsiCo ( PEP ), which owns top-performing brands in the snacks and beverages spaces. I sold my PEP position a few years ago and regretted it almost immediately. The Ozempic-driven selloff has given me a chance to buy back in. PEP's 50-year dividend growth streak isn't going to end anytime soon, and its dividend yield of 3.2% is above its 5-year average yield of 2.8%.

I gave a little more of my thoughts on PEP in this article .

Among my favorite real estate stocks right now (it's so hard to choose!) is Mid-America Apartment Communities ( MAA ), the largest owner/developer of apartments in the Sunbelt. The market seems concerned over temporary supply headwinds, but I explained why these headwinds will be milder than assumed in this recent article .

MAA's 12-year dividend growth streak looks likely to continue unabated, while the current dividend yield of 4.3% is well above the 5-year average of 3.2%.

As for utilities, it is again hard to choose just one, but my all-around favorite is probably American Electric Power ( AEP ), an operator of electric utilities in the Midwest and South. AEP has significant transmission and distribution assets across the country as well as ample opportunities to grow its rate base by expanding and upgrading these lines, exemplified recently by the Department of Energy's $27 million grant award to AEP.

AEP's 13-year dividend growth streak appears unthreatened by rising interest rates, and its 4.5% dividend yield is far higher than its 5-year average of 3.4%.

You can read my full pitch for AEP here .

For further details see:

High Interest Rates Are A Gift To Dividend Investors