WBA - Hims & Hers: Niche Telehealth Player With Huge Potential

2023-08-15 15:30:00 ET

Summary

- Hims & Hers Health, Inc. posted strong quarterly results, beating Q2 expectations and raising its full-year revenue guidance.

- The company has tremendous potential to revolutionize the healthcare industry with its value proposition and disruptive approach.

- Hims & Hers has a strong and loyal customer base, high gross margins, and a subscription-based revenue stream, making it a promising long-term investment.

- Hims & Hers Health operates in a niche and has a significant moat, hard to overtake by newcomers. As such, we believe the stock is a strong buy.

Introduction

Hims & Hers Health, Inc. ( HIMS ) is a healthcare company that offers a convenient and discreet way for people to address personal medical concerns like hair loss and erectile dysfunction. They connect individuals with healthcare professionals online, providing tailored solutions and treatments.

Their approach aims to remove the discomfort of traditional doctor visits and offer a more accessible and private healthcare experience. HIMS focuses on subscription-based services, aiming to modernize and simplify healthcare access.

Hims & Hers posted another excellent quarterly result for Q2 , in which it beat on the top and bottom lines. In addition, HIMS raised its full-year revenue guidance to $830M-$850M, up from $810M-$830M. Revenues came in at $207.9M, an 83% year-over-year increase.

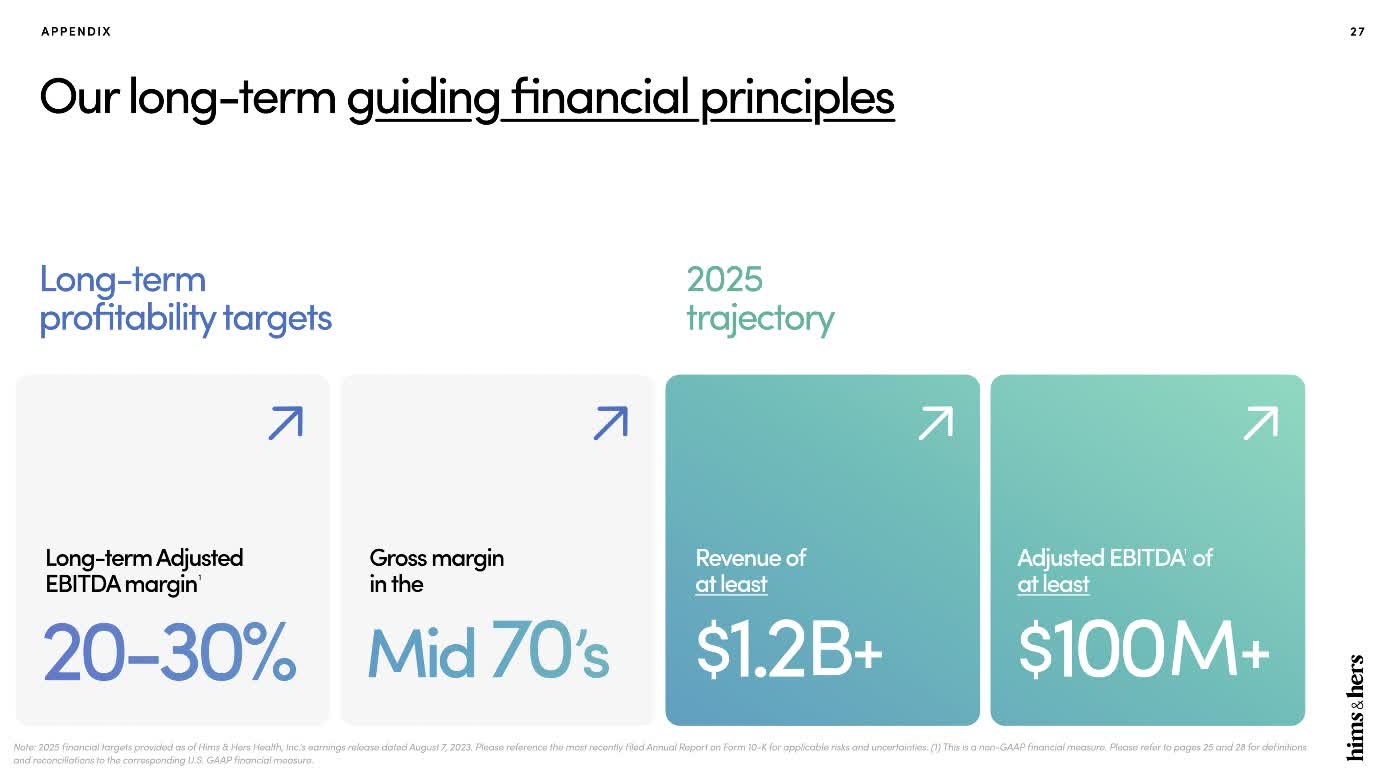

HIMS has a history of guiding quite conservatively and exceeding expectations time and time again, and we expect them to continue this execution in the future. In the chart below, you can see the long-term profitability goals, which HIMS is on track to achieving easily, even in these rough macroeconomic circumstances.

{kind=link}

In this article, we will take a look at HIMS’ potential and why we believe it could become a 10-bagger in the upcoming decade. In addition, we will discuss the risks associated with HIMS, the high short interest, and a competitor analysis.

Tremendous Potential Provides Multi-Bagger Potential

HIMS presents a refreshingly straightforward value proposition that’s poised to revolutionize the way we approach sensitive medical issues. We believe there is a huge market for this within the $4T US healthcare sector, and HIMS is one of the few companies that offers a solution. We believe HIMS is one of the companies that is able to disrupt this “old” model of the healthcare system.

In addition to that, HIMS has shown to be very capable of executing and growing its subscriber base. Furthermore, if HIMS were to cut their marketing expenses right now, this company would already be profitable!

Imagine this: no more awkward trips to the pharmacy or uncomfortable face-to-face conversations with doctors. This is where HIMS comes in. HIMS has the mission to discreetly tackle those often hushed-about health concerns like erectile dysfunction ((ED)) and hair loss.

How does HIMS solve this problem? Hims & Hers offers a virtual rendezvous with a healthcare professional, a true confidant in the digital realm. Picture a seamless journey where you're effortlessly connected with an expert who understands your unique needs, all from the comfort of your own space.

Furthermore, if it's deemed suitable, your personalized medical solution discreetly arrives at your doorstep, ushering in a new era of healthcare convenience.

HIMS isn't just shaking up the status quo; it's doing so with a savvy business model that boasts both elegance and expansiveness. The allure of this enterprise hinges on its potential for rapid growth, fortified by an enticing margin profile.

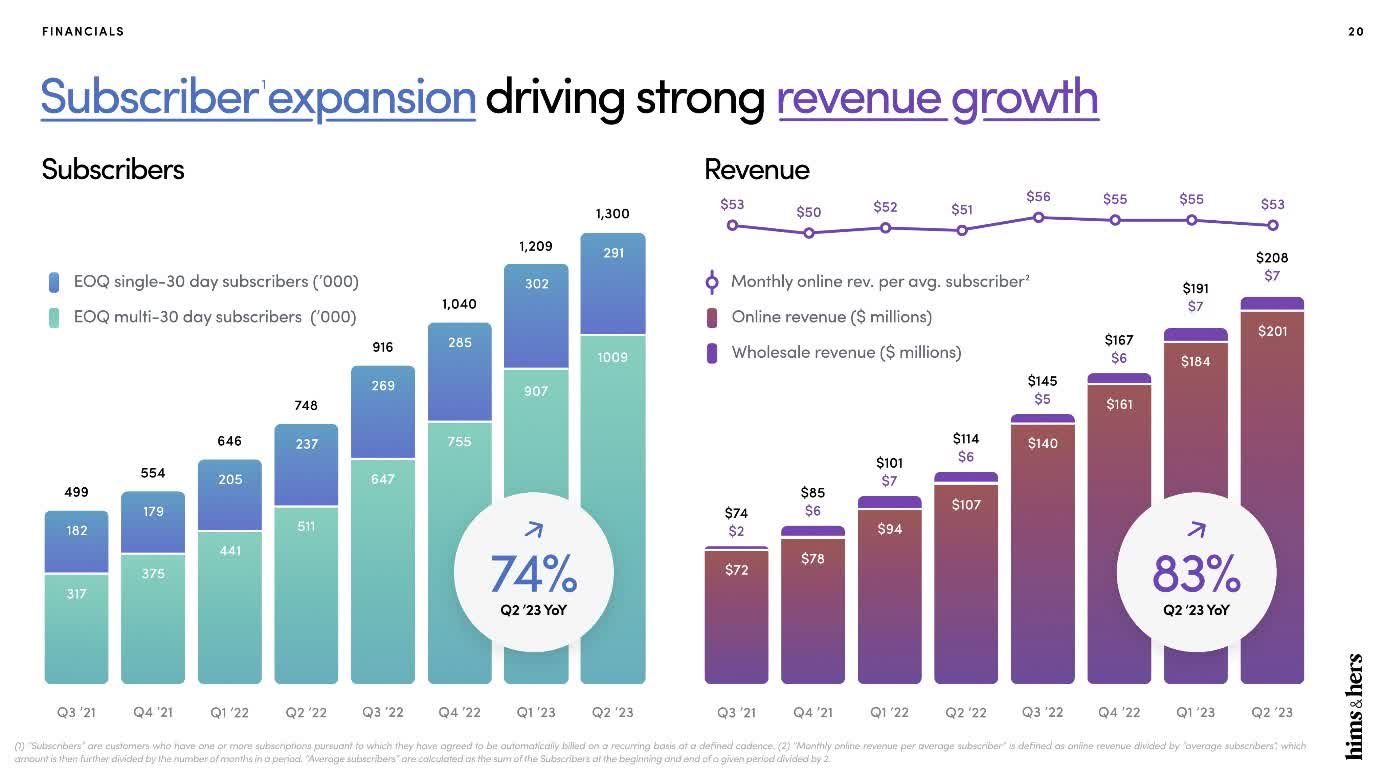

And here's where it gets even more intriguing – the engine that fuels this innovation is a robust subscription model, a drumbeat of recurring revenue that resonates with both the company and its clientele. In the chart below, you can see the excellent subscriber and revenue growth the company has achieved over the last 2.5 years.

{kind=link}

Steering through multiple quarters with an unwavering growth trajectory, HIMS is swiftly carving its niche in the healthcare landscape. It's not merely about addressing health issues; it's about transforming the entire experience, making it smoother, more accessible, and decidedly less awkward. The journey ahead for Hims & Hers is as exciting as it is promising – a trajectory fueled by ingenuity, a touch of rebellion as it fights against the big healthcare companies, and the unwavering pursuit of modernizing healthcare.

In addition, the high percentage of recurring revenue and high gross margins are something worth noticing as well.

If you want to learn more about the potential of the Healthcare Technology sector and why it is poised to grow significantly in the next decade, I highly recommend you to check out my article on the potential of this sector as a whole.

Earnings Review and Expanding Their TAM

As mentioned earlier, HIMS guides quite conservatively and beats these expectations. This time was no difference, another triple beat, with earnings improving further to breakeven.

Online revenues grew by +87% YoY, while wholesale revenues were down -9%. The number of subscribers increased by +74% to 1.3 mln. The number of orders increased by +52% YoY, while the average order value ("AOV") was up +22%.

Furthermore, the company is embarking on exciting new initiatives to drive long-term growth. HIMS is diligently channeling resources into advancing its AI technology to enhance tailored healthcare based on real-time health data and to be able to better serve individual healthcare needs. CEO Dudum has offered an insightful glimpse into their direction, with more to be unveiled next quarter:

“…through tracking systems on the individual, or Apple watches, et cetera, you'll be able to more sophisticatedly treat these patients on the go and leveraging truly best-in-class clinical guidelines at the platform level, and then offer a really data-oriented and ML capabilities to better prescribe and diagnose and treat these individuals.

So I think that's where we're running towards. We mentioned we filed a number of provisional trademarks around the name MEDMATCH and are going to be sharing a lot of that AI technology in the next quarter. But a big part of this is the ability to predict the diagnosis and the appropriate treatment to help providers make more informed and clinically appropriate decisions.”

In addition, another big announcement was made. HIMS will enter the weight loss market next quarter, with personalized treatments to find the underlying causes of being overweight for an individual. I believe this will expand their total addressable market, or TAM, significantly, and this puts them one step closer to their goal of becoming a full-service healthcare provider.

Beyond robust revenue expansion, HIMS is well on its way to profitability as well. Notably, EBITDA margins climbed from 3% to 5%, while Net Income margins currently stand at -3%. As such, I believe GAAP profitability seems well within reach, potentially materializing by early 2024.

Although HIMS is currently decreasing its prices, I believe this is due to the fact that they want to rapidly expand and penetrate the mass market, while delivering customers with the optimal value proposition. Notably, profit margins further improve due to management’s excellent execution.

Spruce Point Capital, Amazon, And Other Risks

Whenever you are writing an investment thesis, it is interesting to look at the risks of the business and to consider other opinions. The most dangerous thing in investing is becoming biased, and that’s exactly why I’ll be discussing some of the risks for HIMS in this post and I’ll give you my opinion regarding them.

The company isn’t profitable: Yes, despite the explosive revenue and gross profit growth, HIMS barely has a positive cash flow. If we take out the stock-based compensation, the cash flow is still negative over a trailing twelve-month period. This is a valid point that the bears and Spruce Point Capital (a firm focused on short-selling) are making.

However, HIMS is still focusing on growth and they are executing fabulously. We believe this is the right focus, HIMS has very high gross margins, combined with its relatively low need for advertising due to its strong brand name it already has within the industry. In addition, HIMS is a non-capital intensive business. As such, I believe Hims & HERS will become a cash machine once the business reaches scale.

This might take some more time as the management sees amazing growth opportunities in the upcoming years to re-invest potential profits. Nonetheless, the company could already be profitable now if it would cut its advertising spending significantly, but, that wouldn’t be beneficial for its growth.

Competitive Industry: Yes, HIMS operates in the healthcare industry, which is a competitive and heavily regulated industry by nature.

Nonetheless, HIMS has been able to grow at a stellar pace, this does indicate that HIMS has a strong brand and that people are returning customers. HIMS clearly has an edge and does something differently compared to their so-called competitors.

“Amazon ( AMZN ) is eating into their core business”: This is a claim that I’ve seen multiple times in the last few weeks. Whenever you see someone mentioning this, you can confidently say that they don’t understand HIMS’ business model.

Amazon Care is a healthcare platform that connects healthcare providers with customers. Just this one sentence is enough to know that they don’t directly compete with HIMS. The only argument that can be made is that Amazon does give HIMS’s competitors a platform to sell their products. But, that’s as far as the competition with Amazon goes. AMZN doesn’t sell nor produce anything, while Hims & Hers does.

Due to HIMS' strong brand and superior execution, HIMS is able to retain their customers with HIMS growing its customer base at a steady pace in addition to gathering data, which will help them cross-sell even more as they grow over time.

In addition, HIMS is able to grow significantly due to the TAM of the market. As such, this isn't a winner-takes-all market. HIMS is gaining an advantage and seems to be able to capture a nice amount of the market before big players decide to jump in.

For example, according to allied market research, the global ED market is expected to reach $5.1B by 2032 and is currently valued at $2.6B as of 2022. In addition, future market insights expects the TAM of hair loss treatment to reach $22.5B by 2032 and the market is currently valued at $8.4B as of 2022.

In addition, HIMS has a low amount of churn and an average monthly revenue per subscriber of $53. With 85% long-term retention and strong key components to drive future growth.

Hims & Hers Earnings Presentation

{kind=link}

Furthermore, HIMS maintains a payback period across their portfolio of less than 1 year and the company expects organic growth to be the primary growth driver in the future. Furthermore, the company has multiple partnerships and affiliations, such as the American college of Cardiology.

Hims & Hers earnings Presentation

{kind=link}

Something that has to be addressed is that the CAC grew to $497. Yes, this is a lot, but due to HIMS's focus on growth and the amazing customer retention rate, I believe this can be justified for a growth company. Management attributed this increase from $425 to $497 to "an increase in investment in display, search, and linear and streaming television marketing, as they continue to identify opportunities to drive new customer growth," according to their latest 10-Q report.

This isn't an issue for potential profitability in the future. The company could easily decide to cut marketing expenses once they reach the desired scale.

“HIMS uses Celebrity-Endorsed Marketing”: Yes, you are reading that right. This is one of the main points the short-selling hedge fund Spruce Point Capital is making.

If you like it or not, this is the new evolution in marketing, brands use influencer and celebrity marketing to market their products as it has been shown that this is one of the most effective ways to target a younger customer base like Millennials and Gen Z, which are obviously the target group of HIMS. Big clothing brands like Nike ( NKE ) and adidas (ADDYY) use celebrities and influencers all the time. In addition, Mr. Beast’s Feastables and Logan Paul and KSI’s PRIME are both brands that have exploded and they are solely focused on the brand of one or two people.

Influencer marketing is radically changing the advertising market and for HIMS this has been an excellent way to grow their loyal customer base. In my opinion, this “Celebrity-Endorsed Marketing” isn’t actually a point for the bear thesis, but for the bull thesis as it shows that HIMS knows their target group and more importantly, how to attract these new customers.

Spruce Point Capital tries to fuel the narrative that this isn’t a good marketing strategy, by showing companies that didn’t succeed, but they fail to acknowledge that this doesn’t have to do anything with the influencer/ celebrity marketing, but more due to the fact that they had weak-business models, with a lot of debt, with low amounts of growth and made significant losses each year.

In addition, these businesses are in a whole different industry, such as Oatly ( OTLY ), which has a gross margin of 14%.

“Downside to $5.20-$6.50”: This is a small cap high growth company. Yes, of course, the stock can go down to $5.20-$6.50 in the short-term. The stock price of a high growth company is volatile. I’m giving this company a strong-buy rating and I can even see it drop as low as $3-$4 in the short to mid-term, that’s how these companies move sometimes. With the current macro headwinds and the possibility of a recession it is fairly clear that there is some downside risk to the thesis.

As such, I think this downside target is quite weak for a short report. There are many better opportunities if you want to capitalize by writing a short-report on companies that aren’t necessarily fraudulent. For example, companies like Carvana ( CVNA ) or Upstart ( UPST ) are even more volatile and provide better short opportunities right now.

While there are lots more points to cover from this short report, I think we covered the main points and I think it is pretty clear that some of these are obvious risks to investing in high-growth companies. Nevertheless, if you want to read the report yourself, you can find it here.

Valuation

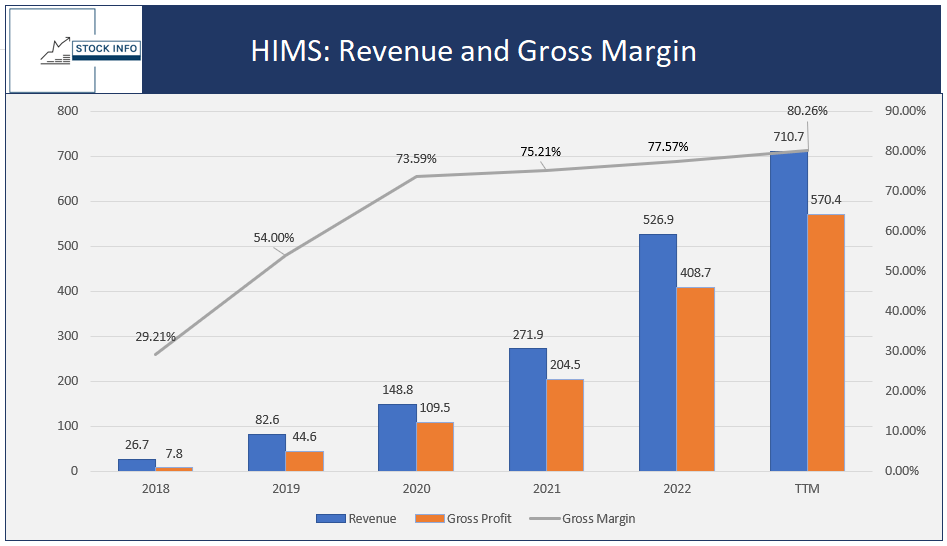

Now let’s move on to the valuation, which is quite attractive at this moment in time. As can be seen in the chart below, HIMS has a solid track record of growing its revenue and cash flow. In addition, the company was able to improve its gross margin over the years, with a current gross margin of over 80% indicating that the business has strong pricing power.

{kind=link}

Furthermore, Hims & Hers boasts a 5Y revenue CAGR of 53.79%, numbers that are unheard of. You really don’t see these types of numbers often, especially in addition to such high gross margins. Furthermore, HIMS is currently very close to break-even cash flow wise as we mentioned earlier in the article. As such, I would like to reinstate that this company could become a cash-flowing machine in the future.

In addition, the company has a close to 40% 5Y operating income CAGR. When we take a look at the price-to-sales ratio ((PS)) of HIMS, the company is currently trading at close to its cheapest price ever. The stock is now trading at the same level as in October-November of last year, when the stock was trading at $4 per share. Furthermore, it is as cheap as in May of 2022, when the stock reached a low of $2.72 per share.

Ycharts

I personally started buying some HIMS from February 2022 till early June of 2022. I bought some additional shares last October and I did sell some in March and April of this year. I traded HIMS often in periods prior to that, but now as I’ve been following the company for a long time I believe the company is a great hold for the long-term if you buy it at the right price. I sincerely believe, and I wouldn’t be surprised if this becomes a 10 to 100 bagger in the future.

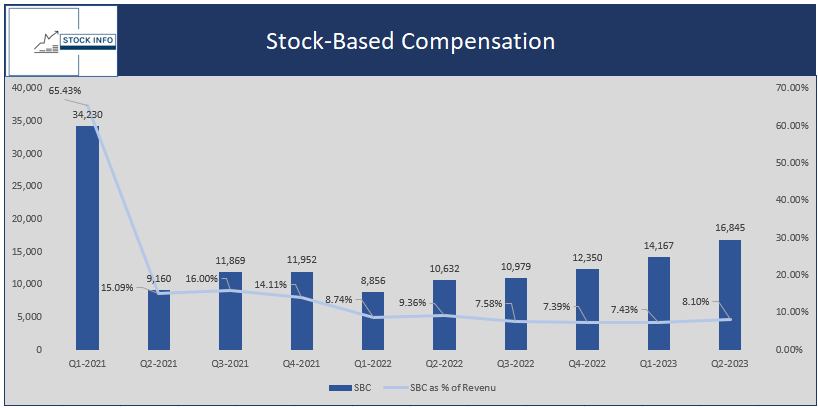

Furthermore, HIMS has been on a steady trajectory of lowering its stock-based compensation as a % of revenue, as can be seen in the chart below.

{kind=link}

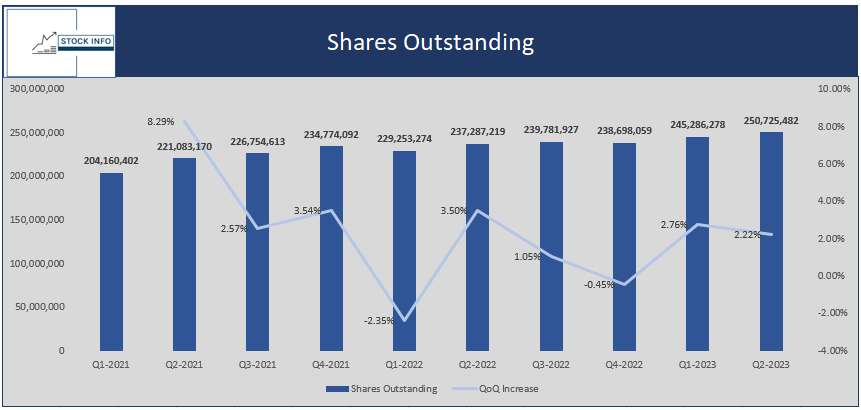

In addition, we can see that the dilution of HIMS is still pretty heavy with around 2% per quarter. Nonetheless, this is an overall decline and we expect this to improve in the future, if HIMS continues executing.

In addition, it is important to point out that the dilution from Q4 2021 to Q4 2022 was only 1.67%. 2% QoQ dilution is definitely not the standard for HIMS. Furthermore, the recent uptick in dilution can be attributed to the newly created RSUs for further expanding the management team and growing the board.

To conclude, I expect the rate of dilution to ease off a bit sooner rather than later.

{kind=link}

Thanks to @Agrippa_Inv for providing me with a spreadsheet to quickly analyze the data.

Something I would like to add to the valuation as well is that HIMS definitely has a moat, which some people doubt it has. I believe Hims & Hers is more than just a telehealth platform, HIMS is a pioneer in the industry and they set the tone and the standard.

HIMS uses telehealth as a gateway to a wide range of health products, such as baldness treatments and treatments for ED, as indicated earlier. HIMS can be seen like some digital pharmacy as well, not only offering patients treatments, but also the product itself directly, which is a huge edge over competitors.

Companies like Teladoc ( TDOC ) are also focused on telehealth, but aren’t close to the practicality and brand loyalty HIMS has. HIMS has the better products and the better execution as of now. In addition, HIMS has a wide arrange of data from its 1.3M subscribers. They are able to cross-sell this to help people further with all their health needs. Keep in mind, HIMS isn’t only for a hair-solution or an ED pill.

Nonetheless, as indicated earlier, I believe the real edge of HIMS lies in their strong customer base and brand value. Their user base and the capability to introduce and cross-sell other products are something new in the industry and I believe it is very hard for newcomers to replicate or catch-up to HIMS in the next few years.

Technical Analysis

Yes, I know what you might be thinking, "I don't care about TA, because I plan on holding this stock for years." That's definitely a valid point and for the long-term holders fundamentals are more important. Nonetheless, everyone can benefit from some quick technical analysis.

TA gives you the possibility to identify key levels, which can help you with deciding when to add some more shares or when you want to sell some shares. This is especially important for volatile stocks like HIMS, a little bit of knowledge about TA can help you significantly with making decisions regarding the right entry points.

In addition, technical analysis can also be very helpful for the option strategy, which helps generate extra income. TA can be a very useful tool to help you decide when you might want to sell some puts or calls.

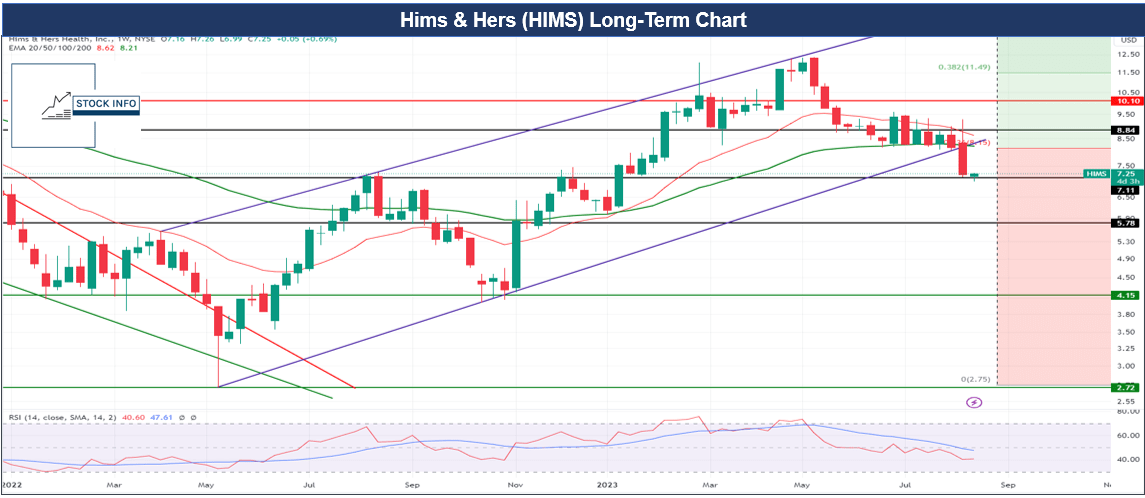

Let's take a quick look at the chart. As you can see, HIMS recently broke out of the purple channel. Unfortunately, it was to the downside. This upward-trending channel was intact since the all-time low back in May of 2022.

Fortunately, it seems like the $7 provides some support right now. It is important for the stock to stay above this level as the first decent support if the $7 level would break is around $5.80.

{kind=link}

Conclusion

In a remarkable quarter that once again beat expectations, Hims & Hers exceeded both top and bottom-line estimates. The growth trajectory is undeniable, with a robust 83% YoY increase in revenues, and the company has raised its revenue guidance for the full year, signaling their confidence in the road ahead.

HIMS' knack for overachievement is a testament to their strategic execution. The path to profitability is clearly illuminated, with impressive strides already made in EBITDA margins, and a forecasted GAAP profitability expected to dawn in early 2024.

The potential for exponential returns is clear as HIMS reinvents the healthcare and more specifically the telehealth landscape. Their disruptive approach to addressing sensitive health concerns discreetly, through virtual interactions and personalized solutions ensures they are poised to grow in the upcoming years and further disrupt the traditional healthcare model.

The seamless integration of AI technology into their platform further underscores their commitment to improving healthcare, and their commitment to helping their subscribers as efficiently as possible. I believe the recent advancements in AI could further improve HIMS’ growth story with new techniques to further revolutionize the future of healthcare.

HIMS' business model can be described as unique and as a leader in its industry. The strong customer-focused business model, accentuated by strong growth potential and great financial metrics, such as its 80% gross margin. The subscription-based revenue stream, underpinned by a loyal customer base, propels the company forward and gives it the possibility to do so for many years to come.

Spruce Pont Capital’s short thesis isn’t as strong as some people would believe at first glance. In this article, I addressed some of the main risk risks, according to Spruce Point Capital. Nonetheless, HIMS has shown exceptional resilience and differentiation. In addition, the company's influencer-driven marketing strategy unveils a modern approach that resonates with the millennial and Gen Z demographic, which is their target group, bolstering brand loyalty.

As Hims & Hers navigates a dynamic industry landscape, which is known for its rapid evolution, HIMS’ continuous strong execution, with a strong Founder/CEO like Andrew Dudum in a leading role inspires confidence. The expansion into weight loss treatments extends their reach, while the commitment to modernize healthcare acts as a driving force. HIMS is more than a telehealth platform – it's a pioneer, setting the industry standard, backed by a growing arsenal of data and the remarkable power of brand loyalty.

The journey ahead is nothing short of exciting. A company poised to further innovate and revolutionize the industry, with a pioneering spirit.

Hims & Hers excellent execution and continuous outperformance, while seemingly effortlessly reaching their milestones shows that HIMS has a bright future ahead of itself. As such, we believe HIMS is an excellent investment opportunity for people with a long-term mindset. I believe HIMS has the potential to generate 10X+ returns in the next decade for investors.

As such, I rate this high-growth pioneer of telehealth with a strong buy rating, where each stock price below $6 could be seen as a tremendous opportunity to further expand your position.

Nevertheless, this is a hyper-growth company and thus very volatile. It is crucial to keep an eye on the numbers as these are crucial to the investment thesis.

For further details see:

Hims & Hers: Niche Telehealth Player With Huge Potential