REIT - Holiday Hangover

2024-01-07 09:00:00 ET

Summary

- U.S. equity markets stumbled on the first week of the new year as investors parsed employment data that gave conflicting signals on the state of the U.S. economy.

- Employment data showed a continued cooling in wage pressures, but the steady pace of hiring raised questions over the likely magnitude and timing of Fed interest rate cuts.

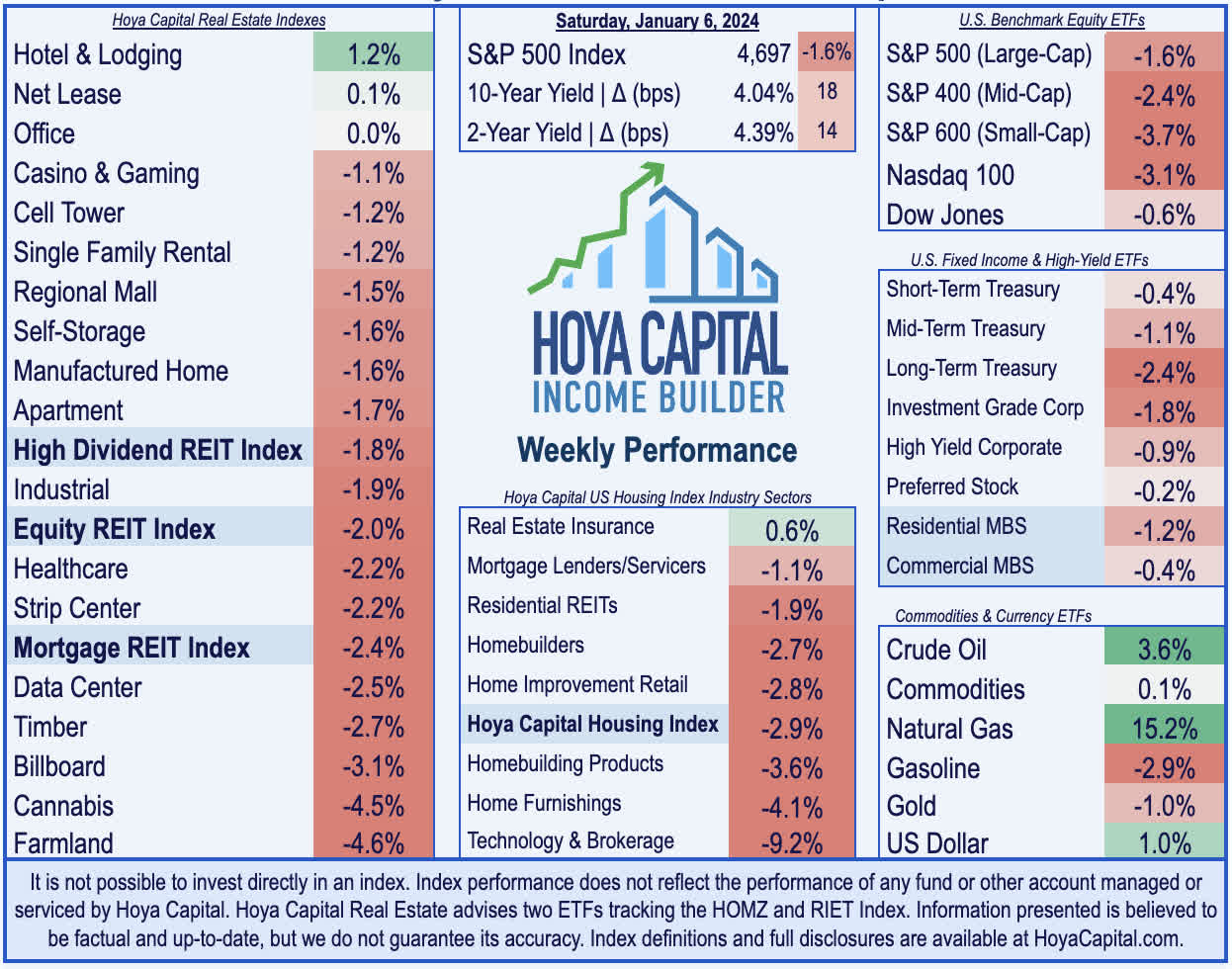

- Snapping its nine-week winning streak and retreating from the cusp of record-highs, the S&P 500 slipped 1.6% on the week. Mid-Caps and Small-Caps were under sharper pressure.

- Real estate equities also lagged this week as a generally solid slate of business updates and M&A news were offset by pressure from the rebound in benchmark interest rates. The Equity REIT Index slipped 2.0% this week.

- Office REITs continued their recent rebound after Hudson Pacific announced the successful sale of a LA office building. Troubles continued for hospital REIT Medical Properties Trust, which announced further problems with its largest tenant, Steward Healthcare.

Real Estate Weekly Outlook

U.S. equity markets stumbled on the first week of the new year as investors parsed employment data that gave conflicting signals on the state of the U.S. economy, raising questions over the likely magnitude and timing of Fed interest rate cuts. While the critical slate of data showed a continued cooling in wage pressures and a steady pace of hiring, it fell short of delivering the decisive evidence that the U.S. economy is trending towards a "soft landing."

{kind=link}

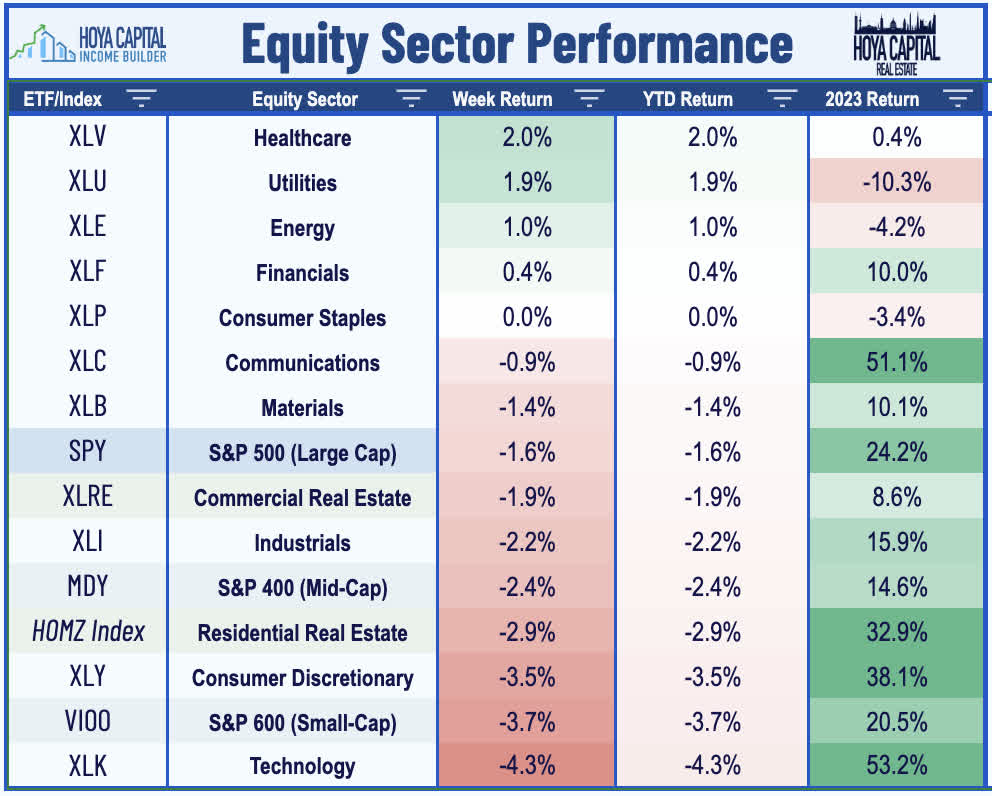

Snapping its nine-week winning streak and retreating from the cusp of record highs, the S&P 500 slipped 1.6% on the week - its first down week since October. The Mid-Cap 400 and Small-Cap 600 - which led the furious rally in the final two months of 2023 - were under sharper pressure this week with declines of 2.4% and 3.7%, respectively. The tech-heavy Nasdaq 100 was also under pressure this week, posting declines of over 3% following its surge of over 50% in 2023. Real estate equities also lagged this week as a generally solid slate of business updates and M&A news were offset by pressure from the rebound in benchmark interest rates. The Equity REIT Index slipped 2.0% this week, with 15-of-18 property sectors in negative territory, while the Mortgage REIT Index declined 2.4%. Homebuilders posted declines of nearly 3% as mortgage rates edged higher for the first time in nine weeks.

{kind=link}

The scorching bond market rally also paused this week as traders reigned in their bets on the timing and magnitude of central bank interest rate cuts as employment data showed a less-than-definitive cooling of labor market conditions. The 10-Year Treasury Yield jumped 18 basis points to 4.04% (up from its lows last week of 3.79%), while the policy-sensitive 2-Year Treasury Yield rose 14 basis points to 4.39% (up from lows of 4.24%). Swaps markets are now pricing in a 66% probability that the Federal Reserve will cut interest rates for the first time this cycle during its March meeting, down from the nearly 90% odds at the peak last week. Looking longer term, swaps markets still see a median year-end Federal Funds rate of 4.09% - up from the lows last week of around 3.85%. Traders also eyed commodities, which have caught a bid over the past two weeks following a slide throughout the fourth quarter. WTI Crude Oil - the key "swing" inflation input - rebounded by nearly 4% this week, while Natural Gas surged 15% on expectations of colder weather patterns. Six of the eleven GICS equity sectors were lower this week, with Technology ( XLK ) stocks lagging on the downside.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

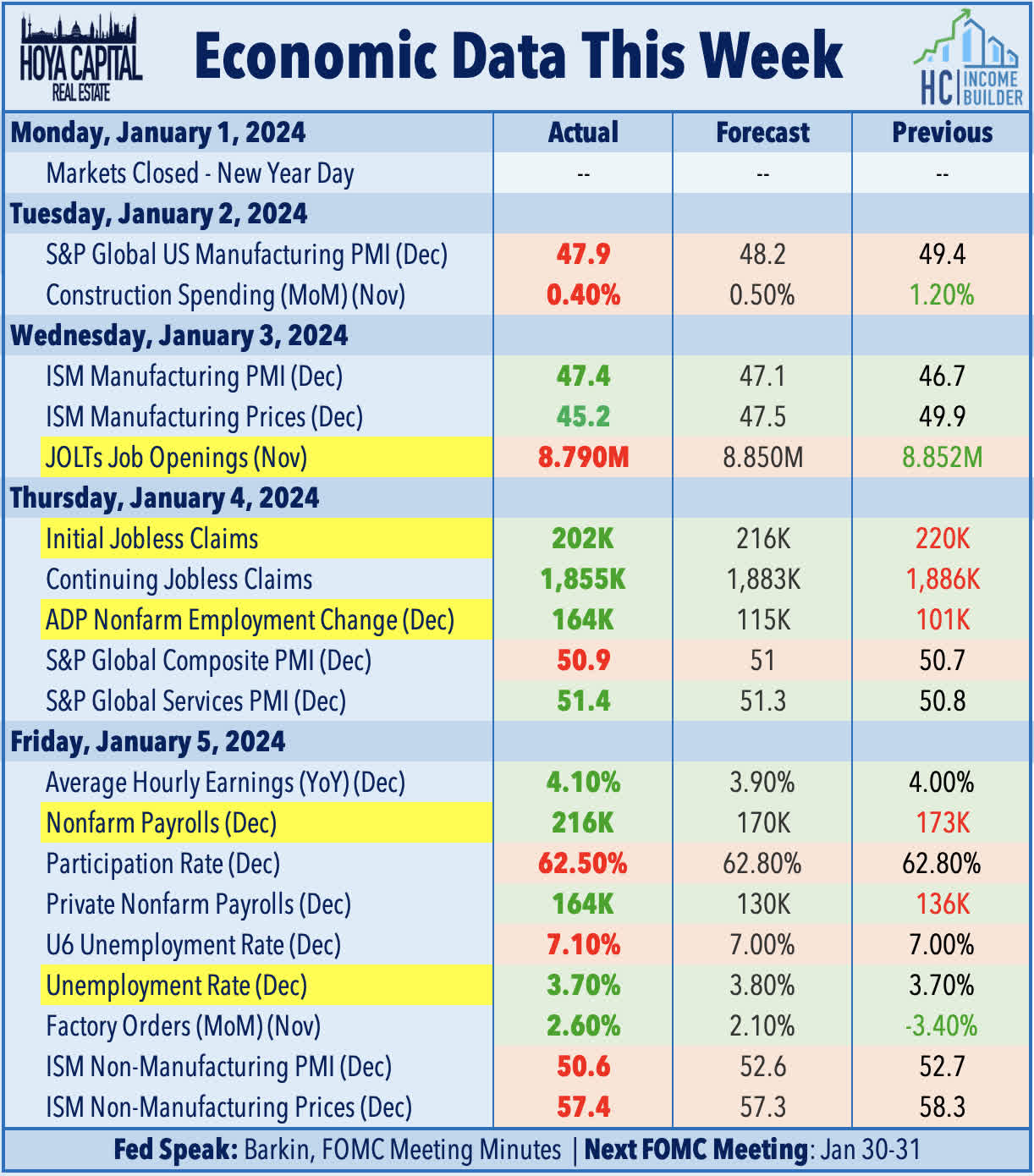

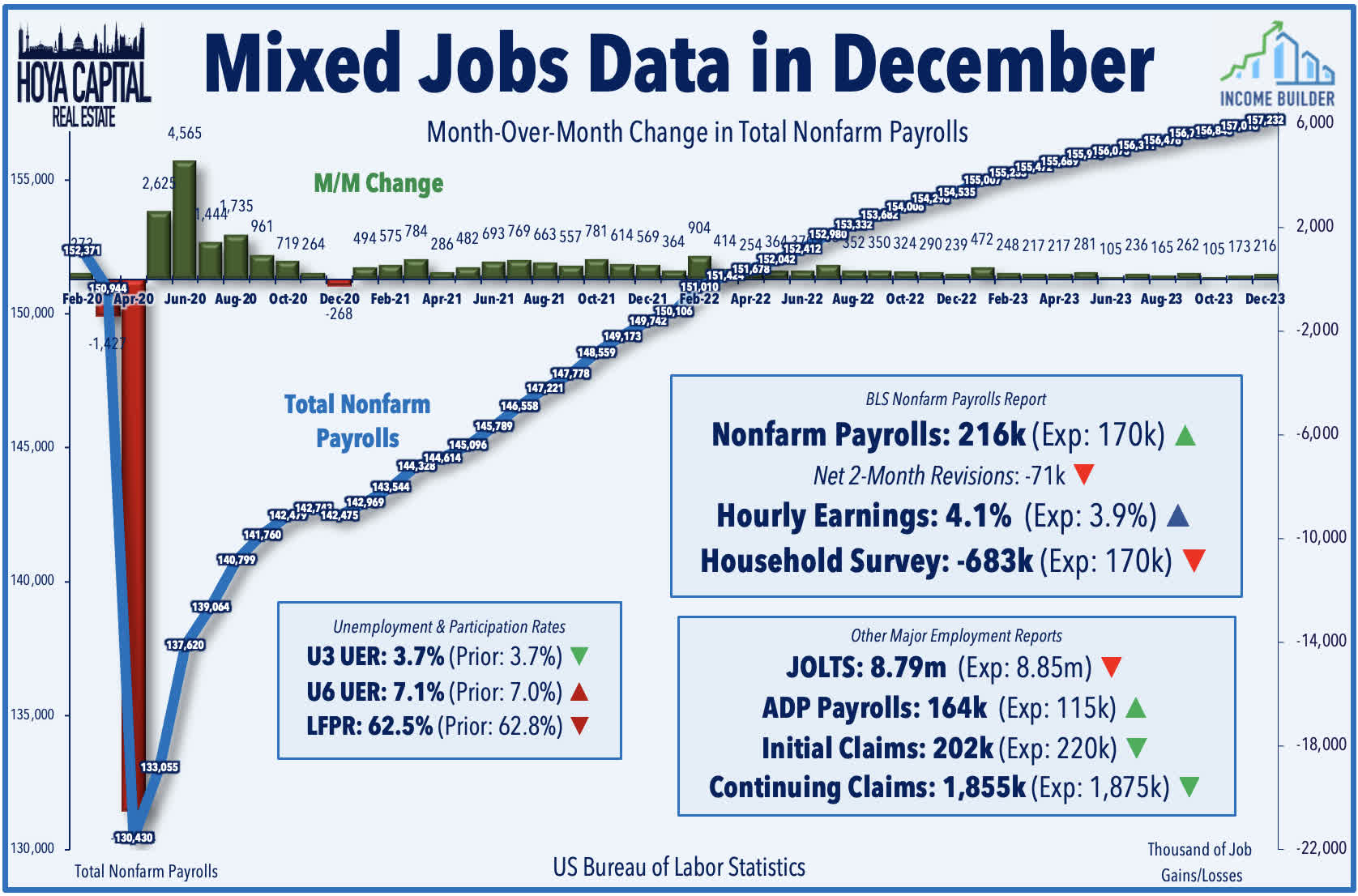

This week's critical BLS nonfarm payrolls report showed that the U.S. economy added 216k jobs in December - above consensus estimates of 170k - while average hourly earnings unexpectedly accelerated to 4.1%. The report wasn't as strong as it appeared on the surface, however, as net revisions subtracted 71k from the prior two months - the eleventh downward revision in the past twelve reports - while trends seen in the Household Survey - which is used to calculate the unemployment rate and participation rate - were significantly softer than the Establishment Survey, which drives the job growth metrics. The Household Survey - which admittedly has been quite noisy and has given several "false alarms" since mid-2022- showed a nearly 700k decline in the employment level, which was the weakest month since April 2020. The U6 "underemployment" rate rose to 7.1% (up from 7.0%), while the labor force participation rate declined to 62.5% (down from 62.8%).

{kind=link}

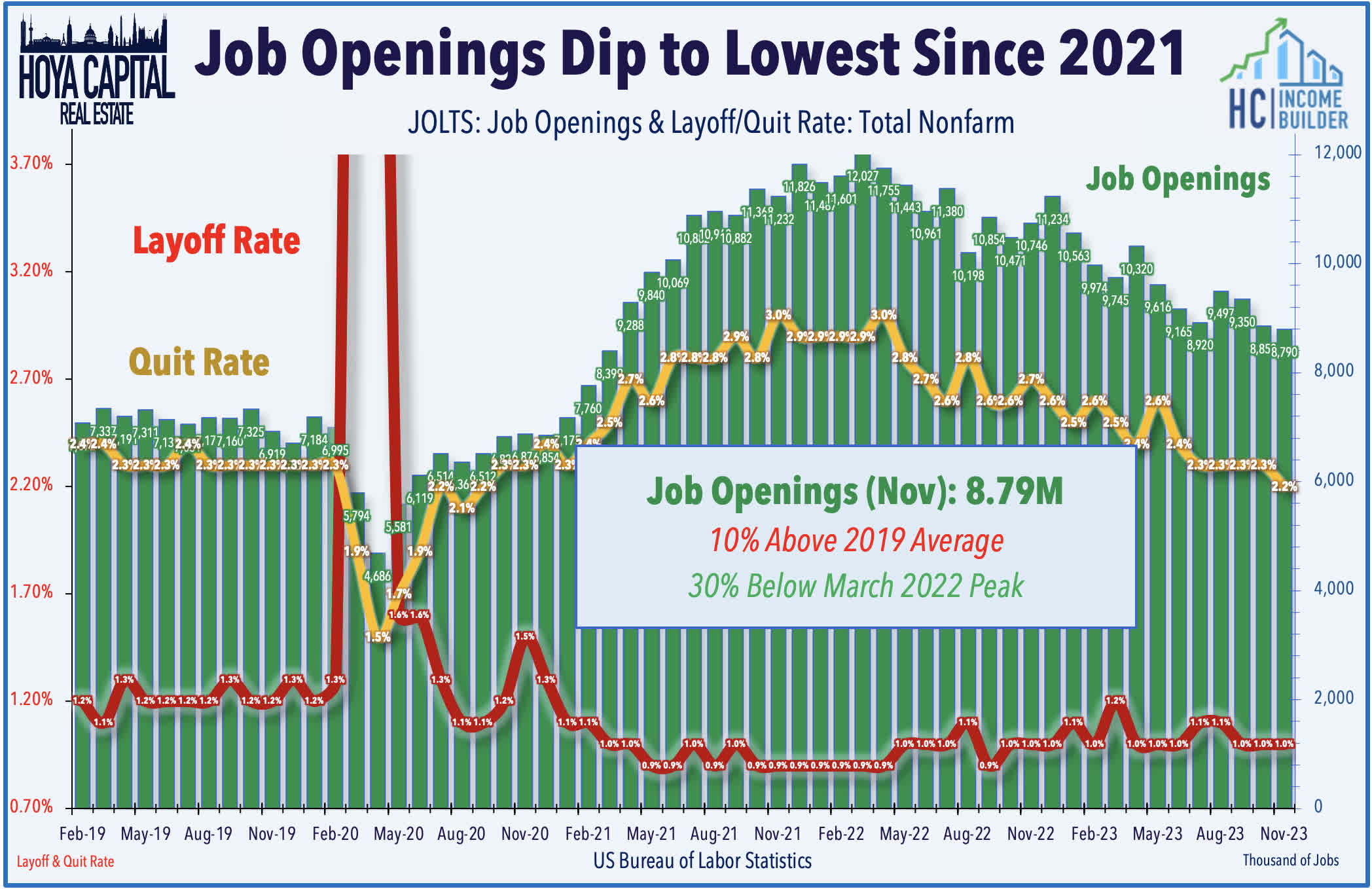

Consistent with the pattern seen in the prior month, the relatively solid BLS report followed a softer data slate earlier in the week. The Labor Department's Job Openings and Labor Turnover Survey ("JOLTS") showed that job openings in November dipped to the lowest level since March 2021, with the number of openings falling to 8.79 million - down roughly 30% from the peak of the labor market shortages seen in early 2022. The figure was well below consensus estimates, but the prior month was revised higher. The ratio of vacancies for every unemployed worker fell to 1.3, returning much closer to the pre-pandemic high of 1.2. The report showed that while we haven't yet seen a major uptick in corporate layoffs, employees are far more hesitant to voluntarily quit their jobs than seen earlier in the pandemic. The "quit rate" - which jumped during the pandemic as workers bargained for higher pay and better opportunities - has now fully returned to pre-pandemic levels. ADP reported that private payrolls grew by 164k in December - above consensus estimates of around 115k - but despite the uptick in hiring, wage growth remained on a downward trajectory, with ADP reporting that its measure of annual pay posted its smallest annual gain since September 2021 at 5.4%.

{kind=link}

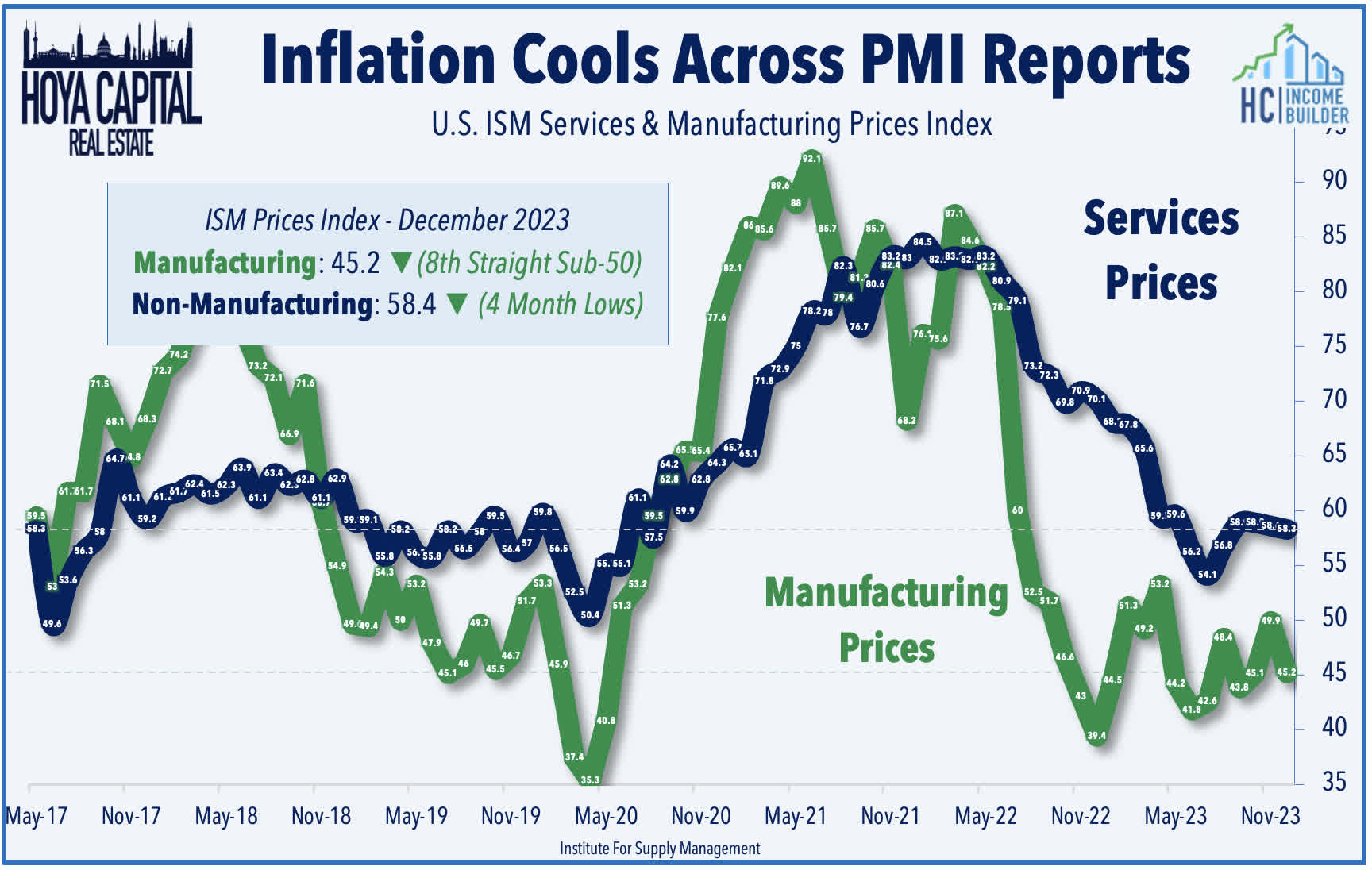

The latest PMI data released by S&P Global and ISM this week also pointed to a further cooling of pandemic-era inflation pressures. ISM reported that its Manufacturing PMI remained in contraction territory for a 14th straight month in December - extending the longest stretch of shrinking activity since 2000-2001 - but edged up slightly from the prior month to 47.4, helped by a pickup in production. More importantly to the macroeconomic story, the ISM Price Index dipped to 45.2 in December - down 4.7 percentage points from November - driven by a dip in raw materials prices. The index has been in contraction (or “decreasing”) territory since May. “Panelists’ comments indicate that buyers and suppliers continue to negotiate price levels for 2024, with commodity markets remaining highly volatile. ISM notes that recent decreases in energy prices have been partially offset by increases in metals prices. Of note, 86% percent of panelists’ reported ‘same’ or ‘lower’ prices in December.

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

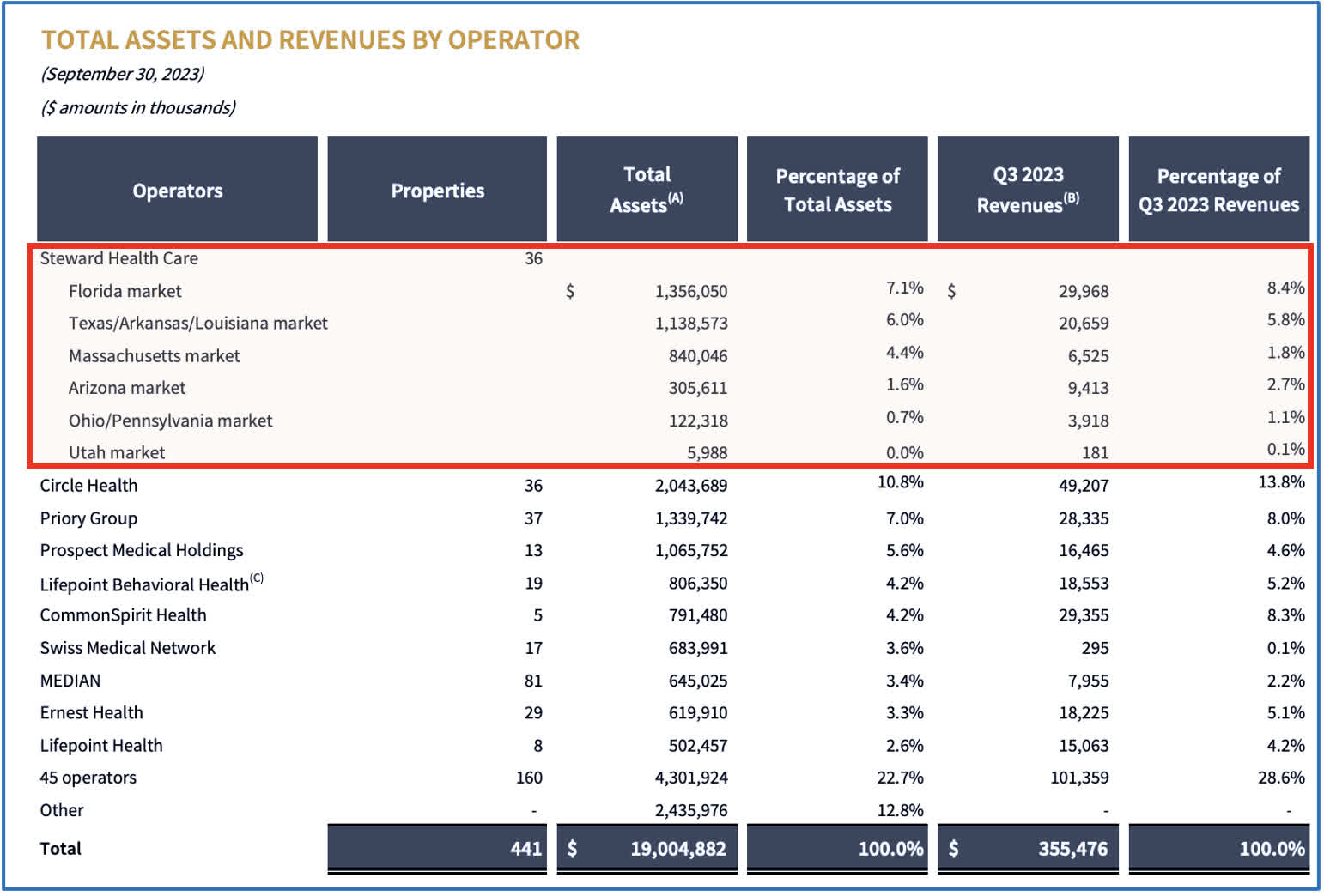

Healthcare : Not out of the woods yet. Embattled hospital owner Medical Properties Trust ( MPW ) plunged more than 25% this week - dipping to its lowest levels since 2009 - after it announced deepening financial distress with its largest tenant, Steward Healthcare. Sparked by missed rent payments for its September and October rent, MPW noted that it has engaged legal advisors and intents to "accelerate its efforts to recover uncollected rents and outstanding loan obligations" from Steward with plans to "significantly reduce its exposure" to the troubled hospital operator. Steward - which represents 23% of MPW's annual rent - has leaned on MPW for financial support in recent years and struggled to stay current on rent amid a challenging post-pandemic operating environment across the "public pay" healthcare space. MPW notes that Steward owes $50M in unpaid rent (exclusive of $50M previously deferred). Despite being burned in the recent past, MPW continues to "work closely with Steward and its own advisors" on a plan to keep Steward afloat, an unusual allegiance between the two entities that has been a central critique from short-sellers. MPW extended another $60M to Steward through a bridge loan and agreed to defer $55M in rent until June 30. MPW plans to effectively write off Steward's portfolio in its Q4 earnings results with a $225M write-off, not including further asset impairment. Having already slashed its dividend in half this past June, MPW noted that its AFFO payout ratio would still be in the "high 70%" range if all Steward-related contributions were removed based on its current $0.15/quarter dividend payout (12.0% dividend yield).

{kind=link}

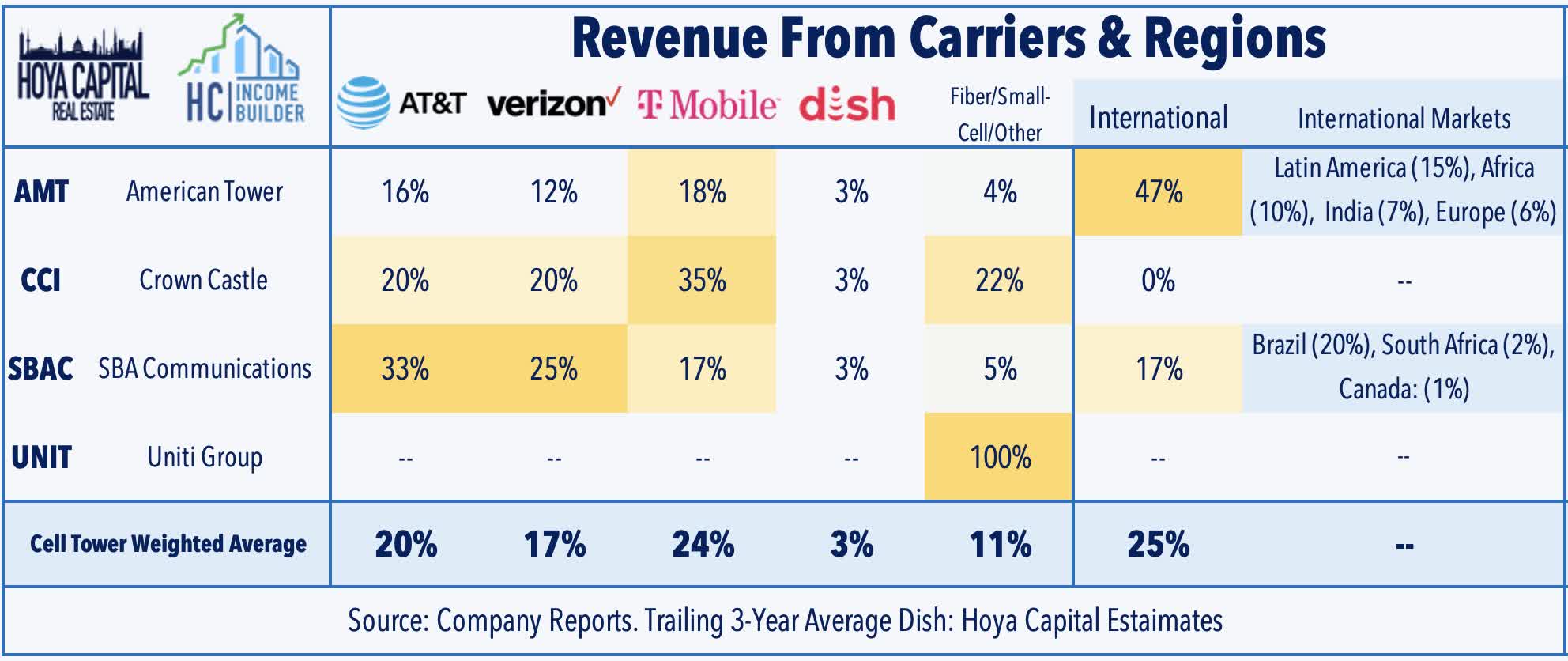

Cell Tower : American Tower ( AMT ) - the largest cell tower REIT - finished flat this week after it announced a $2.5B deal to sell its India operations to an affiliate of Brookfield Asset Management ( BAM ), which completes AMT's exit from the Indian market - a region that has been a source of turbulence for the firm in recent years. AMT initially entered India in 2007 - its first market investment outside of the Americas - and expanded its portfolio to over 75,000 cell sites through acquisitions and site development. India became AMT's largest international market at roughly a third of its total cell site and 10% of annual revenues, yet contributed just 4% of gross margin and has been a negative FFO contribution for much of the past half-decade. Not unlike the trends seen domestically, a wave of carrier consolidations in India over the past decade from a handful of smaller players into two dominant carriers has been a nagging operational headache for AMT in recent years, leading to double-digit churn rates in the region and prompting a series of write-offs and lease renegotiations. AMT has been in talks to sell parts or all of its India operations for several years, conceding in a recent earnings call that its high expectations "didn’t materialize," citing rapid carrier consolidation and competition in site development from state-run entities.

{kind=link}

A win-win for AMT and BAM - and perhaps a bit of vindication for Crown Castle ( CCI ) given its domestic focus and tack towards density (small-cells) over mass coverage - the $2.0B valuation on ATC India is at the upper end of the $1.5-2.0B range discussed over the past year. Brookfield - which already owns 135k cell sites in India - will expand its market share in the region to around 50%. AMT, meanwhile, will use the proceeds to pay down debt when the deal closes in the second-half of 2024. A perennial outperformer within the REIT sector for much of the prior decade, Cell Tower REITs were among the weakest-performing sectors in 2023 - lagging the broader REIT sector by around ten percentage points amid headwinds from a slowdown in network investment by domestic carriers and by their relatively high variable rate debt exposure. Notably, AMT has outperformed its domestic-focused peer Crown Castle on a 3-, 5-, and 10-year basis by 4-6 percentage points annually, in part due to the success of its international operations apart from India. Following the India exit, AMT's international exposure will be 40% of revenues, with Brazil, Mexico, Nigeria, Germany, and Spain as its top international markets.

{kind=link}

The emergence of satellite cell service also may change the economics of these emerging markets. On that note, SpaceX announced this week it successfully launched its first batch of Starlink satellites that have the added capability to connect directly to unmodified 4G LTE smartphones - an advancement beyond the emergency-use-only satellite technology that is currently available in mobile devices. Through a partnership with T-Mobile ( TMUS ), SpaceX plans to enable texting from space this year, with voice and data connectivity coming in 2025. SpaceX CEO Elon Musk noted that the satellites “will allow for mobile phone connectivity anywhere on Earth,” but conceded that they are not "meaningfully competitive" with existing ground-based networks for mobile devices given the high power consumption and direct line-of-sight signal required of satellite-based communications. Satellite internet has been around for decades through providers including EchoStar's ( SATS ) HughesNet and Viasat ( VSAT ) that use geostationary satellites that are roughly 20k miles from Earth, but new Low Earth Orbit ("LEO") systems can provide broadband-like speeds through "constellations" of satellites that are several hundred miles above Earth. Starlink - which has already deployed roughly 3,000 LEO satellites and recently surpassed 2M subscribers - is one of a handful of companies working on LEO broadband and related technologies.

{kind=link}

Office : Having already seen its share price double over the past two months amid a broader rebound across the office REIT sector sparked by easing interest rate headwinds, West Coast-focused office REIT Hudson Pacific ( HPP ) rallied another 4% this week after it announced alongside mall REIT Macerich ( MAC ) that it sold One Westside and Westside Two in Los Angeles to the University of California for $700 million. HPP held a 75% interest in the joint venture, while Macerich held the other 25% interest in the property, which UCLA will convert into a research facility. HPP noted that it will use the proceeds to repay debt - pushing out its nearest maturity to the end of 2025 and lowering its Debt to EV to 35% from 39%. Google had signed a 14-year lease in 2022 with plans to redevelop the property, a lease that UCLA will presumably assume. Elsewhere, Armada Hoffler ( AHH ) traded flat after it announced a new office tenant at Town Center of Virginia Beach - KPMG LLP, reaching 98% leased office space. While still below pre-pandemic levels, office leasing activity nationally has picked up a bit over the past several quarters after bottoming in early 2023, particularly in faster-growing Sunbelt markets. Sunbelt markets reported leasing activity that was within 10% of pre-pandemic levels in Q3, while Coastal leasing volume was 25% underwater.

{kind=link}

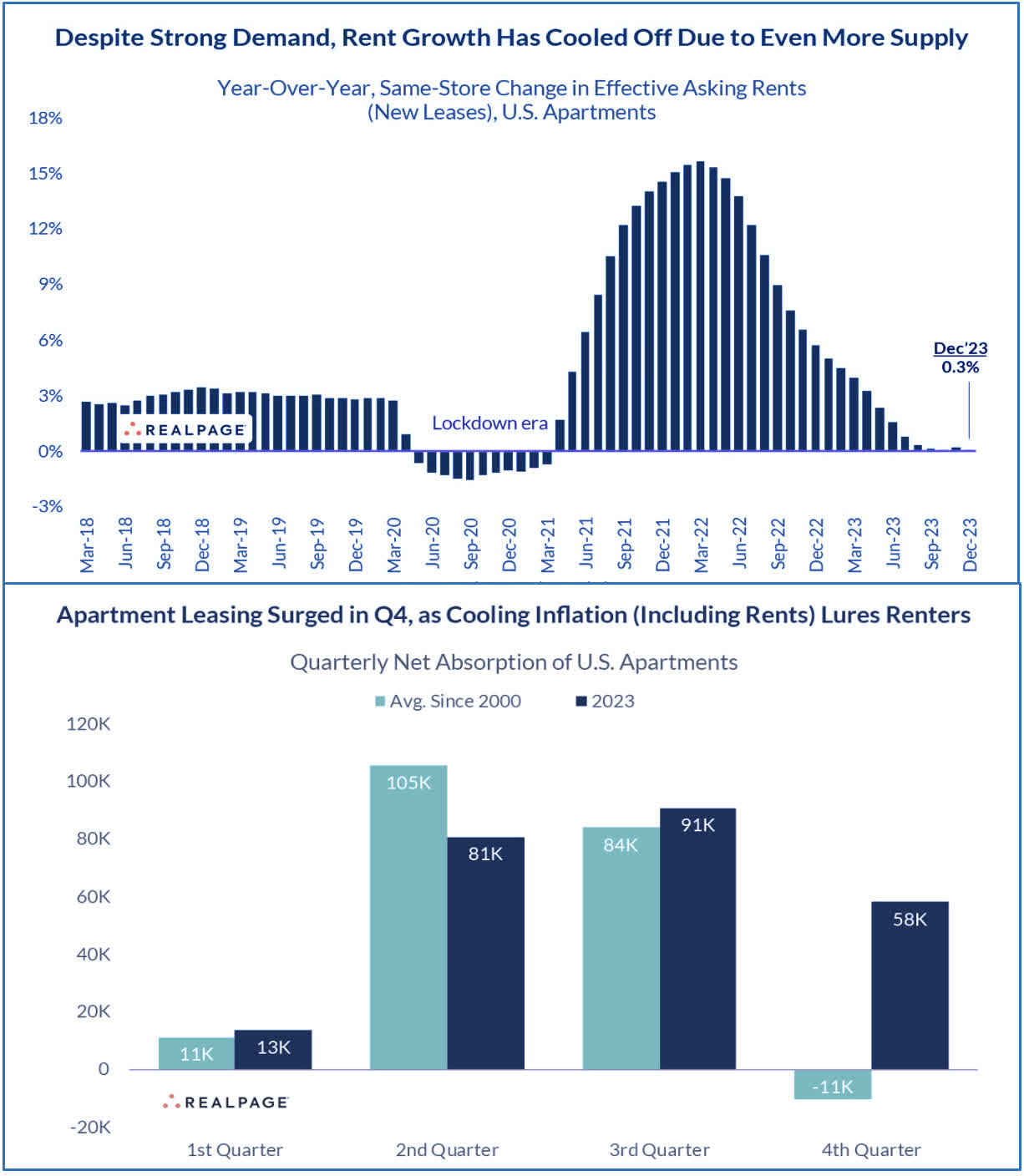

Apartment : Sticking with the M&A theme and deleveraging theme, sunbelt-focused multifamily REIT Independence Realty ( IRT ) announced the sale of four "non-core" properties as part of a portfolio optimization and debt reduction strategy that it initiated last October, raising gross proceeds of $200.7 million, which was used to repay debt. IRT also noted that five of the six additional properties identified in its optimization strategy are currently under contract and expected to close this quarter. IRT expects to generate $525M from these sales, which will enable the firm to lower its Debt-to-EBITDA multiple to a "mid-5x" range by year-end 2024." Relevant to the inflation theme, RealPage published its monthly rent report this week, which noted that apartment completions jumped to 36 year-highs in 2023, but surprisingly strong demand - especially in the fourth quarter - helped to partially offset the supply headwinds. Nearly 440k apartment units were completed in 2023 - the highest in nearly four decades - with a similar quantity expected in 2024 before "plunging" into 2025 due to high financing costs and softer fundamentals. RealPage noted that apartment demand was surprisingly strong in the fourth quarter, however, with net absorption of 58.2k units - the third-strongest 4th quarter in 25 years - bringing the full-year total to 234k units, which was similar to pre-COVID norms. Supply still outpaced demand for the year, resulting in an uptick in occupancy to 94.1% (still within the typical pre-COVID range of 93-95%), and a slowdown in rent growth to just 0.3% for full-year 2023, which was the second-weakest year since 2009.

{kind=link}

Importantly, RP data shows that rent growth is no longer decelerating, however, holding in the 0-1% year-over-year range since July following a swift deceleration from double-digit peaks in 2022. RealPage forecasts 2024 to bring "another year of more supply than demand – adding another challenge for apartment investors also confronting higher expenses and elevated debt costs," but sees a rebound in fundamentals by early 2025 and into 2026, given the recent slowdown in new multifamily starts. At the regional level, elevated supply has generally followed regions with the strongest demand, with the Sunbelt and Mountain West adding the most new supply in 2023: 62% of completions, but also 70% of demand. The Northeast and Midwest regions have seen more balanced conditions, combining for roughly 20% of new supply and 20% of new demand. The West Coast has been the notable weak spot, however, accounting for 10% of new supply but just 4% of net demand. Markets seeing the strongest demand included Dallas, Houston, Phoenix, Austin, and DC. Of note, 10 of the 12 highest-demand markets were in the Sunbelt and Mountain West regions, while just one West Coast market – Seattle – ranked among the top 35.

{kind=link}

Industrial : A handful of industrial REITs provided business updates this week. Small-cap Plymouth ( PLYM ) provided preliminary fourth-quarter metrics, which showed a modest deceleration in rent growth and leasing activity from the prior quarter, consistent with the broader moderation in industrial fundamentals in recent quarters. PLYM noted progress in filling its relatively large book of expiring leases for 2024 - which total roughly 20% of its portfolio - a potential risk factor that explains its discounted valuations. PLYM trades with a forward Price-to-FFO multiple of 12x, a sizable discount from the industrial REIT sector average of around 23x. PLYM signed an additional 700k in leases in Q4 for commencement in 2024, raising the total to 2.9M SF, representing 41.4% of its total 2024 expirations. Elsewhere in the industrial space, Rexford ( REXR ) announced that it completed $1.5B in activity in 2023 - all in Southern California - including two recent purchases: a $57.0M property in Anaheim at a 6.7% unlevered stabilized cash yield and a $12.5M property near Los Angeles at a 6.4% unlevered stabilized. Terreno ( TRNO ) reported that it sold an industrial property in Compton, CA for $15.9M, which it had purchased in 2017 for $9.4M, generating an IRR of 13.0%. Americold ( COLD ) announced a series of leadership changes, including the "mutually agreed" termination of its CFO Marc Smernoff, effective next week, who will be replaced by Jay Wells - currently the CFO at Primo Water. COLD also realigned several roles to "reflect its continued international expansion," naming CCO Rob Chambers as its Head of Americas and COO as its Head of International.

{kind=link}

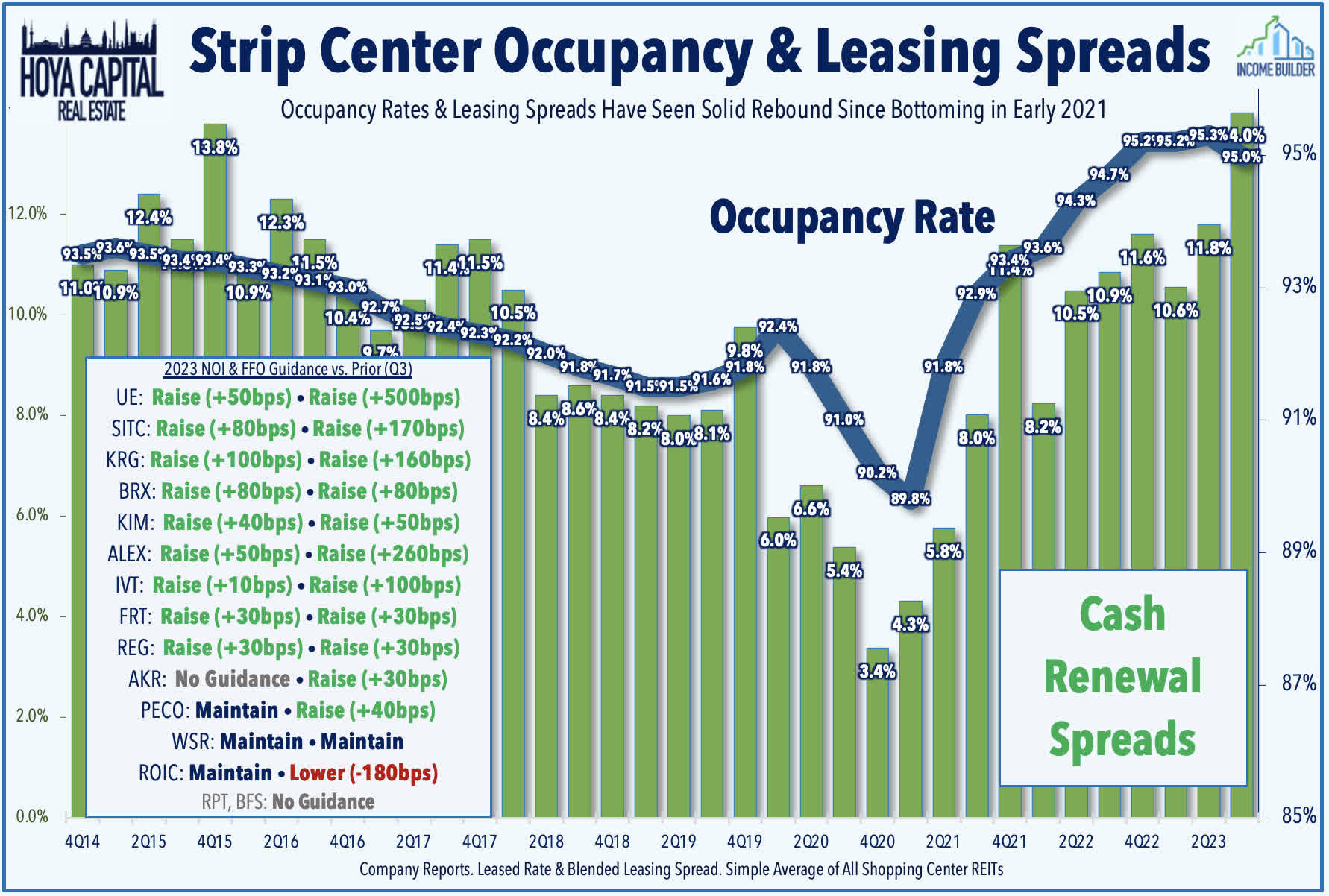

Strip Center : While industrial fundamentals have cooled in recent quarters, retail fundamentals have remained as strong as they've been in at least a decade. Strip center REIT Urban Edge ( UE ) - which owns 76 strip centers, primarily in the Northeast - was little-changed after providing preliminary fourth-quarter metrics showing that it achieved record leasing activity and accelerating rent growth. UE noted that it signed 234k SF in new leases in Q4 - including the backfill of a former Bed Bath location - which lifted its same-property occupancy rate to 96%, which is the highest since 2018. UE generated same-space rent growth on these new leases of 38%, underscoring the continued demand - and lack of supply for well-located "big box" space. UE highlighted the firm's "transformational" year in 2023, and announced that it completed the sale of Freeport Commons and a self-storage facility in New Jersey in separate deals for a combined $101M in proceeds, representing a blended 5.8% cap rate on forward NOI. CTO Realty ( CTO ) reported similar strong trends, noting that it signed nearly 100k square feet in leases in Q4, which generated comparable rent per square foot growth of 17.9%. For the full-year, CTO signed 497k SF of leases, which generated rent growth of 7.5%.

{kind=link}

Elsewhere in the strip center space, Kimco Realty ( KIM ) - the largest strip-center REIT - closed this week on its previously announced acquisition of small-cap strip center REIT RPT Realty. The acquisition of RPT - which had a market capitalization of roughly $1B - adds 56 open-air shopping centers (43 of which are wholly owned) comprising 13.3 million square feet, to Kimco’s existing portfolio of 527 properties. Kimco expects to see earnings accretion stemming from initial cost savings synergies of approximately $34 million, of which approximately 85% is expected to be realized in 2024. RPT common shareholders received 0.6049 newly issued shares of Kimco common stock, while owners RPT's 7.25% Series D preferred stock (RPT.PD) received a share of newly issued Kimco 7.25% Class N Preferred Stock. The deal was one of a dozen REIT-to-REIT consolidations seen across the broader industry in 2023 - a trend that we expect to continue in early 2024 as larger REITs with the balance sheet "firepower" advantage of the continued discounted valuations of public REITs relative to the slow-to-adjust private markets.

{kind=link}

Net Lease : We also heard business updates from a pair of net lease REITs, both of which we featured in our new Hoya Hotseat interview series launched last month. Agree Realty ( ADC ) reported that its acquisition activity totaled $1.34B in 2023 - an impressive haul - but down from its record of $1.71B in 2022. Its 2023 acquisitions were completed at a weighted average capitalization rate of 6.9% and had a weighted average remaining lease term of 11.3 years. ADC noted that cap rates trended higher through the year, averaging 7.2% in Q4, which was 80 basis points higher than the fourth quarter of 2022. Three-fourths of ADC's acquisitions have investment-grade retail tenants - consistent with its IG-focused strategy - while 9% were ground leased assets - a growing segment within ADC's business - raising its total ground lease portfolio to 12% of rents. Alpine Income ( PINE ) was among the better-performers this week after it announced its 2023 investment activity, noting that it purchased 14 net lease properties for $82.9M, representing a weighted average going-in cash cap rate of 7.4%. PINE sold 24 net lease properties for $108.3M at a weighted average exit cap rate of 6.3%.

{kind=link}

Mortgage REIT Week In Review

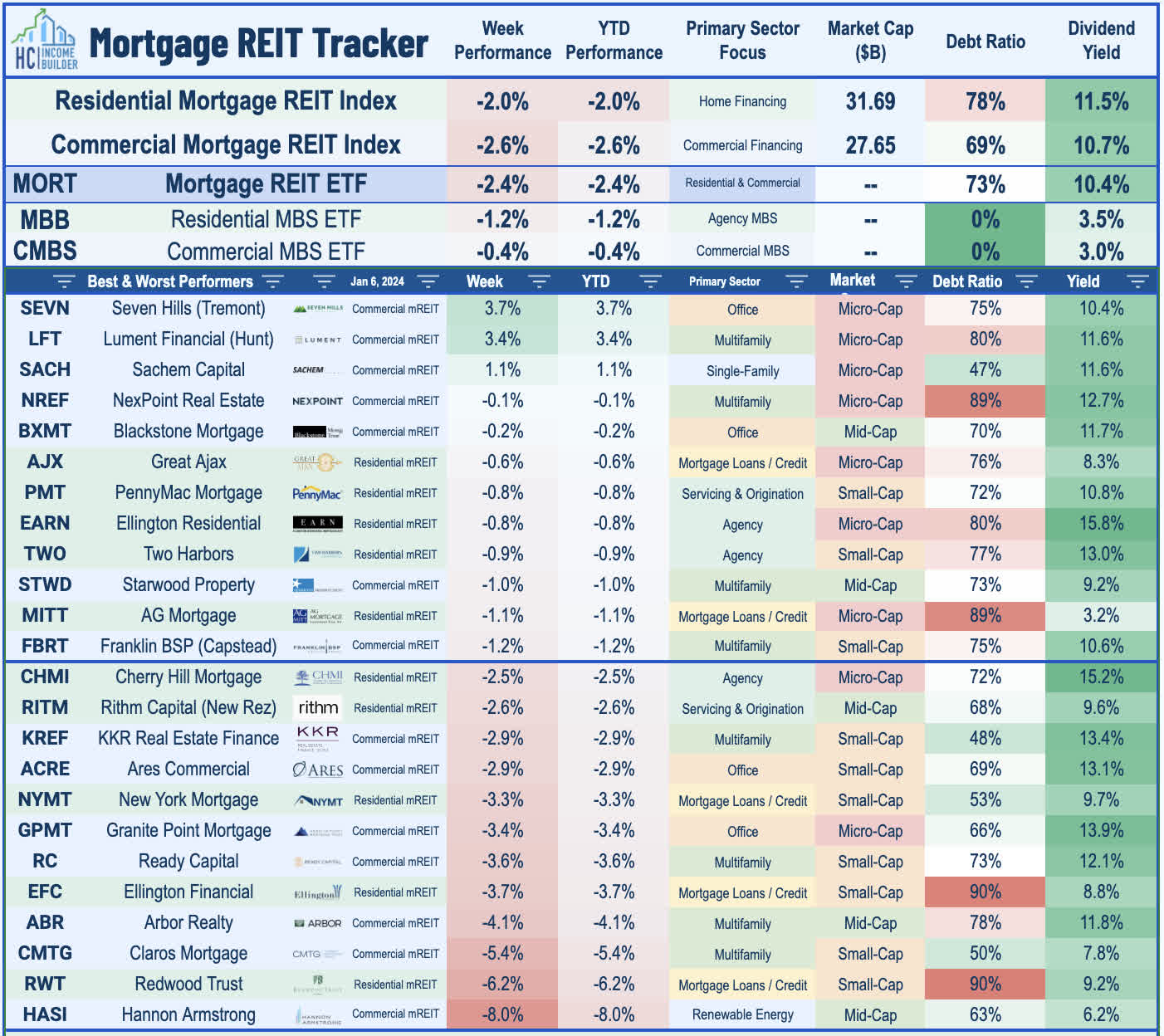

Mortgage REITs were under pressure for a second-straight week following a dramatic 30% surge in the final nine weeks of 2023. The iShares Mortgage REIT ETF ( REM ) slipped 2.4% this week after posting total returns of roughly 15% in 2023. On an otherwise quiet week of newsflow, ARMOUR Residential ( ARR ) traded lower by 2% this week after it lowered its monthly dividend to $0.24/share (14.9% dividend yield) - consistent with the guidance provided last month - which was a 40% reduction from its prior dividend of $0.40/share. Despite the wave of 14 dividend reductions across the mREIT space in 2023, the average mortgage REIT continues to pay a dividend yield of over 10%. As discussed in our Weekly Outlook , mortgage REITs are likely to report their best quarter for underlying Book Values since the start of the pandemic. The iShares Residential MBS ETF ( MBB ) - which tracks the un-levered performance of RMBS - posted total returns of 7.3% in Q4 - one of its strongest quarters on record. The iShares Commercial MBS ETF ( CMBS ) - which tracks the un-levered performance of RMBS - posted gains of 5.0% in Q4, also one of its strongest quarterly gains on record.

{kind=link}

2023 Performance Recap

Looking back on 2023, the Equity REIT Index finished with total returns of 11.8%, while the Mortgage REIT Index posted total returns of 14.9%. At the bottom in late October, both indexes were lower by over 10% on a year-to-date basis and trading at their lowest-level since the depths of the pandemic in May 2020. This compares with the 26.2% gain on the S&P 500 , the 16.1% gain for the S&P Mid-Cap 400 , and the 16.2% gain for the S&P Small-Cap 600 . Within the REIT sector, 15 of 18 property sectors finished the year in positive territory, led by Data Center, Regional Malls, and Hotel REITs, while Cell Tower, Net Lease and Farmland REITs lagged on the downside. The 10-Year Treasury Yield ended the year lower by 1 basis point - up from its 2023 intra-day lows of 3.26% in April, but down sharply from peaks above 5.0% in mid-October. Following the worst year for bonds in decades, the Bloomberg US Bond Index posted total returns of 5.5%. WTI Crude Oil prices declined by 5% in 2023, while Natural Gas prices dipped 64%.

{kind=link}

Economic Calendar In The Week Ahead

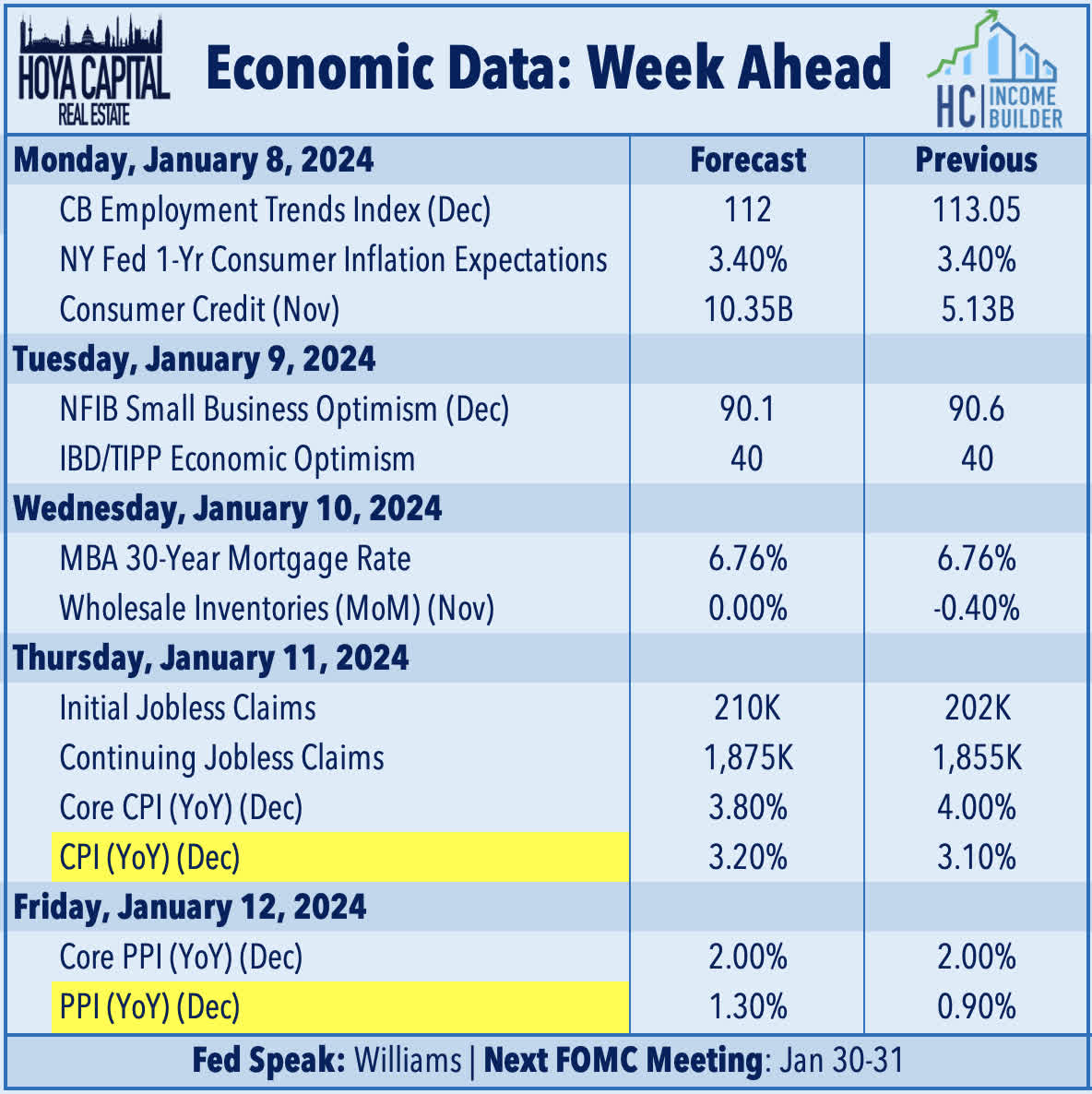

A critical slate of inflation data highlights the economic calendar in the week ahead. The main event comes on Thursday with the Consumer Price Index for December, which investors and the Fed are hoping will show a continued cooling of inflationary pressures. The Core CPI is expected to moderate to a 3.8% year-over-year rate - down from 4.0% last month - as some of the effects from the heavily weighted shelter component finally begin to moderate. Headline CPI is expected to tick slightly higher to 3.2% from 3.1% in the prior month after two very "cool" months, which would keep the Q4 rate at 2.8%. Gasoline prices - which drove a reacceleration in inflation from June through September - were lower by an average of 6% during December compared with the prior month, and are currently more than 35% below the recent September peak. On Friday, we'll see the Producer Price Index, which has recently shown an even more significant cooling of price pressures. The Core PPI is expected to remain at 2.0% in December, while Headline PPI is expected to show a 1.3% inflation rate - remaining below the Fed's 2% policy objective. Earlier in the week, we'll see inflation survey data from the NY Fed, and we'll be watching weekly Jobless Claims data on Thursday as well.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Holiday Hangover