HOOK - Hookipa Pharma: A Speculative Biotech Worthy Of A Spot On My Watch List

2023-04-18 17:23:51 ET

Summary

- Hookipa Pharma’s platform has two technologies that are based on arenaviruses that stimulate the immune system to be used to combat infectious diseases or cancer.

- The replication defective modified arenavirus termed VaxWave, is designed to safely express antigens that excite the immune system for infectious diseases. Gilead has partnered for HIV and HBV programs.

- Hookipa's TheraT tech employs attenuated-viral vectors to stimulate the immune system to fight cancer. The company is working with Merck and Roche in separate programs.

- HOOK’s market cap is around $40M and is trading at discount for its partnership revenue and price-to-book. In addition, the ticker currently has a negative enterprise value.

- Any positive update could force the market to value the ticker in line with its peers. I believe HOOK is worthy of a spot on my speculative watch list.

The COVID-19 pandemic generated an immense amount of interest and investments in biotech tickers as the world became reliant on their cutting-edge technology to make it through. Eventually, the momentum subsided and most of the small-cap biotechs have been chopping around since the beginning of 2022. Hookipa Pharma ( HOOK ) has been under this sustained selling pressure over the past year and has crushed the ticker's valuation down to a ~$39M market cap with a negative enterprise value. Hookipa's arenavirus vaccine technologies, VaxWave and TheraT, have the prospects to be operative against infectious diseases and cancer. I am looking to put HOOK on my Compounding Healthcare "Bio Boom" speculative watch list for a potential investment in the coming weeks.

I intend to provide a background on Hookipa and its current valuation. In addition, I discuss why HOOK would be a solid "Bio Boom" candidate. Then, I will highlight some key downside risks that investors need to consider when managing their position. Finally, I reveal my strategy for initiating a position in HOOK and possibly finding a spot in my speculative portfolio.

Background On Hookipa

Hookipa Pharma is a clinical-stage biopharma dedicated to creating immunotherapies utilizing their arenavirus platform, which are intended to facilitate targeted T cells, thus, improving the body's ability to combat or inhibit serious disease. Their goal is to trigger strong and long-lasting antigen-specific CD8+ T cell reactions and pathogen-neutralizing antibodies. Hookipa's pipeline comprises immunotherapies that are targeting HPV 16-positive cancers, prostate cancers, and other unrevealed oncology programs. Hookipa is collaborating with Roche ( RHHBY ) on an immuno-therapy for KRAS-mutated cancers. In addition, Hookipa is working with Gilead ( GILD ) to develop functional cures for HBV and HIV.

Platform Technology

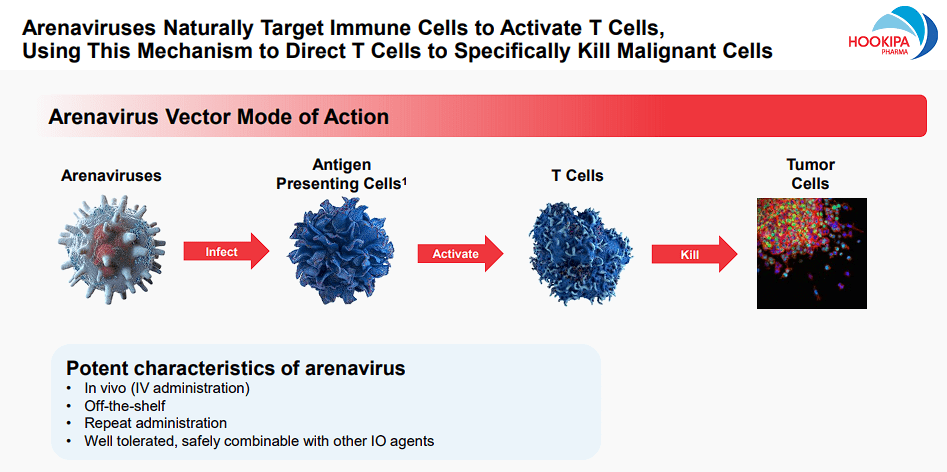

The company technology is designed to elicit a bespoke immune response by CD8+ T cells to then be used to target and treat disease. Hookipa has an interesting delivery platform that utilizes engineered arenaviruses that trigger a robust CD8+ T cell response that activates dendritic cells. In addition, arenaviruses have the advantage of allowing for repeat administration and do not require to be adjuvanted. Thus far, arenaviruses have been well-tolerated in both preclinical studies and clinical trials.

Hookipa is attempting to be the forerunner in arenavirus therapeutics with a platform that has two technologies: replicating and non-replicating. The company's replicating technology, also known as TheraT, is intended to generate a robust CD8+ T cell response that the company is employing for oncology indications. The company's non-replicating technology, also known as VaxWav, is supposed to conjure a powerful immune response to be used as prophylactic against infectious diseases thanks to its ability to produce improved immunological memory and fortification against re-challenge.

Pipeline Programs

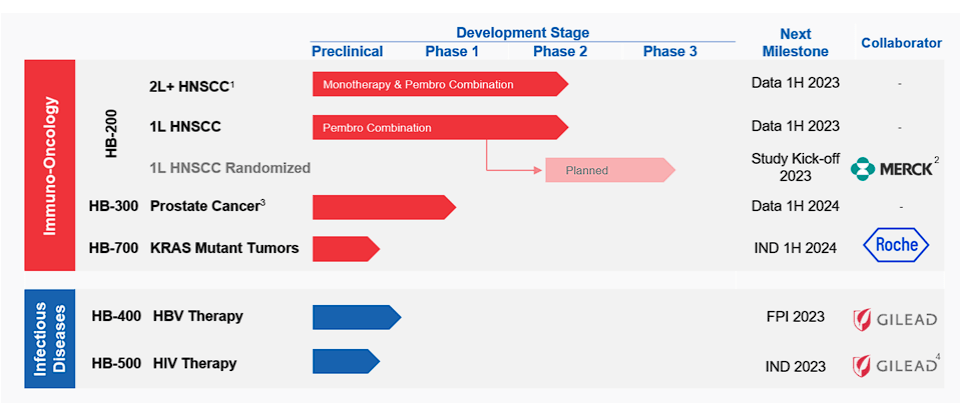

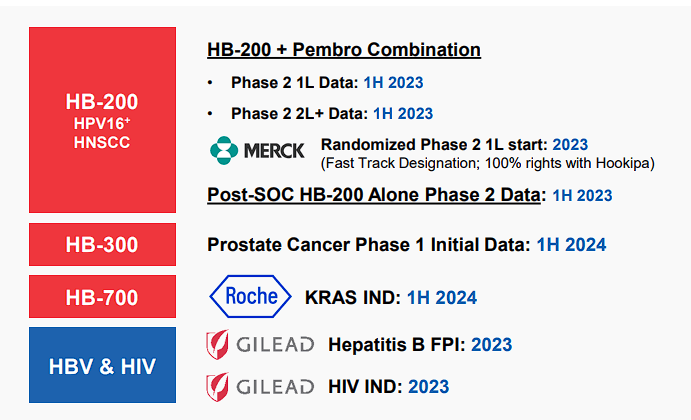

Hookipa's pipeline is divided into immuno-oncology programs and infectious disease programs. The company's immuno-oncology programs are from their TheraT technology, which consists of attenuated-arenavirus, which vigorously excites T cells to abolish cancer cells. The current TheraT oncology programs include therapy for HPV16+ head and neck cancer, prostate cancer, and KRAS mutant cancers. The company's lead candidate, HB-200, has advanced to Phase II in combination with Merck's ( MRK ) Keytruda (pembrolizumab) for head and neck cancers. The company expects data from their Phase II study in Q2 of this year.

Hookipa's Arenavirus MOA For Oncology (Hookipa Pharma)

{kind=link}

Hookipa is also taking aim at prostate cancer with HB-300, which is now open for enrollment. The company expects to report data in the first half of 2024.

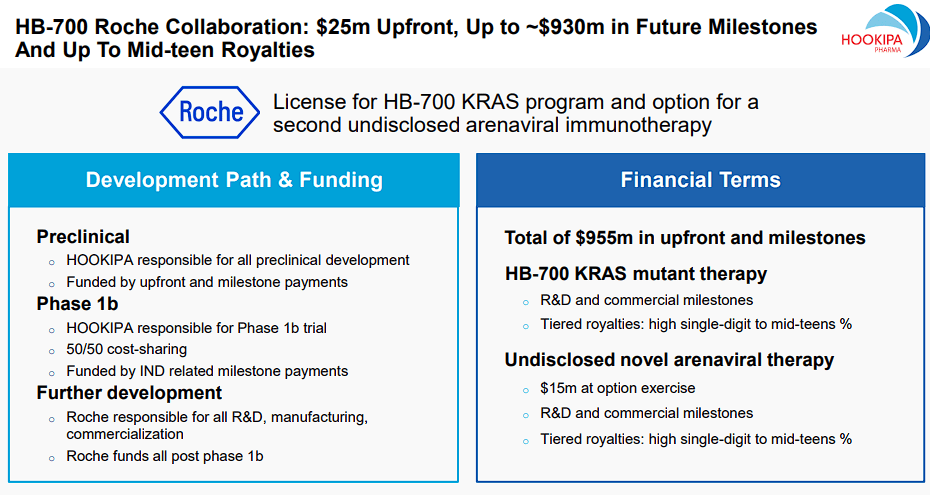

Their HB-700 program triggered a milestone payment from Roche and is moving closer to a planned IND submission in Q4 of this year. The Roche partnership could deliver a total of $995M in upfront and milestone payments, as well as high single-digit to mid-teen royalties.

Hookipa Pharma and Roche Partnership (Hookipa Pharma) Hookipa Pharma Pipeline (Hookipa Pharma)

{kind=link}

{kind=link}

The company's infectious disease programs are powered by their VaxWave technology.

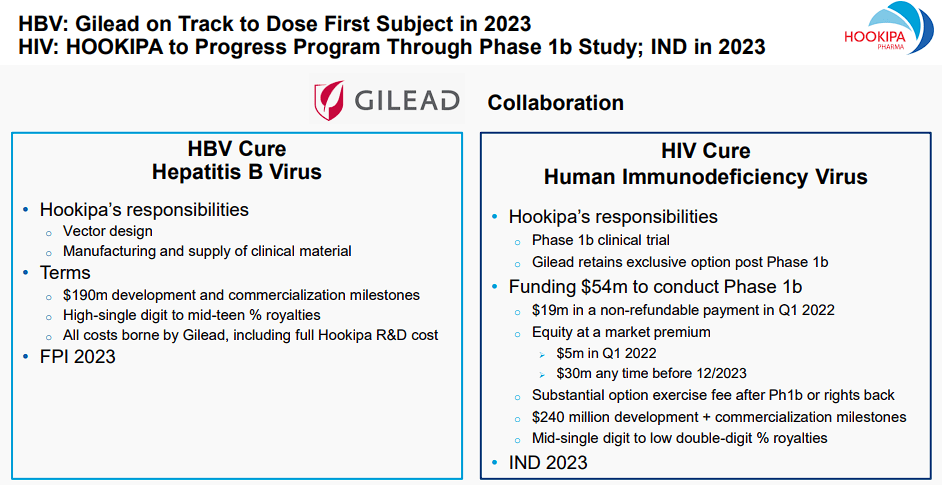

Their HB-400 program is a collaboration with Gilead for a curative regimen for HBV. At this point, Gilead is responsible for the remaining development and commercialization activities. Hookipa is eligible for $190M in milestones as well as high single-digit to mid-teens royalties.

Hookipa Pharma and Gilead Partnership (Hookipa Pharma)

{kind=link}

HB-500 is the company's potential functional curative regimen for HIV which is another collaboration with Gilead. At this point, Hookipa is responsible for progressing the HIV program through Phase Ib clinical trial. The company expects to submit an IND at some point this year. The Gilead partnership can deliver $54M in funding for Phase Ib, and up to $240M in milestones, as well as mid-single-digit to mid-teen royalties.

Financials

Hookipa does generate partnership revenue and pulled in $7.8M in Q4 of 2022 and $14.2M for the full-year 2022. The company reported a net loss of $12.3M in Q4 and $64.9M for the full year. In terms of cash, Hookipa finished 2022 with $113.4M in cash and added an additional $15M in cash from collaboration milestones in Q1 of this year.

Potential "Bio Boom" Candidate

The Bio Boom Portfolio is filled with healthcare tickers that are speculative, yet, they offer significant upside thanks to a potent upcoming catalyst, projected revenue growth, or a potential turnaround. Normally, these are small to mid-cap companies with volatile tickers that will provide consistent trading opportunities to help generate substantial profit while amassing a "house money" position. These tickers will be traded as long as they are in play or the company graduates to the Bioreactor Portfolio.

For HOOK, I am looking at the valuation, financials, growth potential, and chart technical analysis. At the moment, HOOK has ~$39M market cap and negative enterprise value.

HOOK Capital Structure (Seeking Alpha)

In addition, HOOK is trading at a significant discount when you consider its ~3x price-to-sales and 0.39x price-to-book.

HOOK Valuation Grades (Seeking Alpha)

{kind=link}

These grades should only improve as the company continues to move their pipeline forward and collect additional milestone payments from their partners.

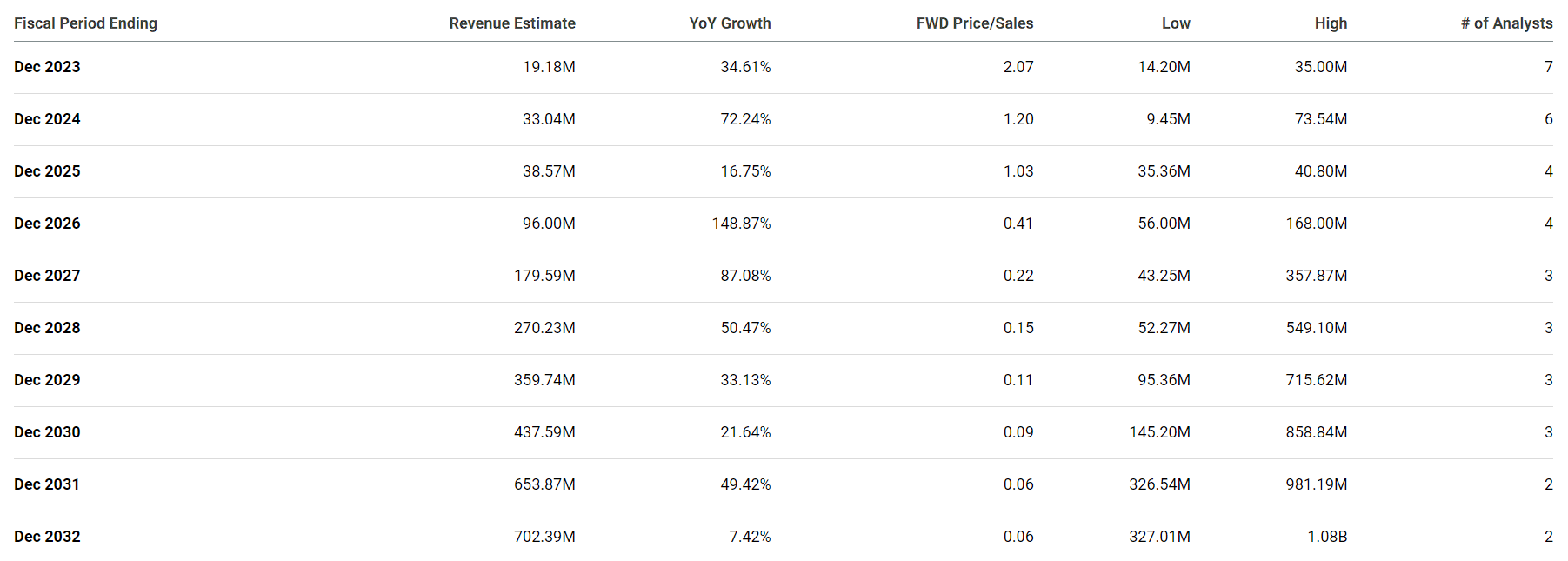

HOOK Analyst Revenue Estimates (Seeking Alpha)

{kind=link}

Looking at the figure above, we can see that Street expects HOOK to report solid double-digit and triple-digit growth for the remainder of the decade.

What is more, Hookipa is considered one of the pioneers in arenavirus technology, which could allow them to carve out and demand a significant portion of their target markets.

For HIV, there are roughly 56K new HIV infections in the US and an estimated 1.5M around the globe each year. Current antiviral therapies are capable of curing HIV, plus, they have significant side effects, and are expensive for a lifetime of viral suppression. For HBV, it is estimated that 1.4M people in the United States and 240M around the world are infected with the hepatitis B virus. Chronic hepatitis B infection may cause liver failure or even cancer. Current Hepatitis B vaccines are only prophylactic; there is no current therapy that can cure the disease after one has been infected. So, there is clearly a market for both HB-400 and HB-500 at this point in time, so Hookipa and Gilead could be the only players in these markets. Obviously, the immuno-oncology programs all have substantial upsides and could lead to additional programs in other oncology indications.

Overall, Hookipa's growth potential is significant considering they could have the only potential cures for HIV and HBV infections. In addition, their oncology efforts could reveal a new method of treating cancer and preventing its reoccurrence.

HOOK's opportunity is the upcoming catalysts and their ability provides a proof-of-concept across the company's pipeline.

Hookipa's Upcoming Catalysts (Hookipa Pharma)

{kind=link}

First, we should see data from the Phase II HB-200 in HPV16+ head and neck cancers this quarter. In addition, we should see initial data for HB-300 in prostate cancer in the first half of 2024. Furthermore, HB-500 should have an IND submission this year. Plus, the company is also moving forward with HB-700 in KRAS-mutated cancers and plans to submit an IND in 2024. The point is, these catalysts should give us an idea that the company has a viable pipeline program that should deliver some value in the coming years. So, we should have some trading opportunities over the next year or two. I believe the company only has to hit on one of these programs to justify a much higher valuation.

How Big of an Opportunity?

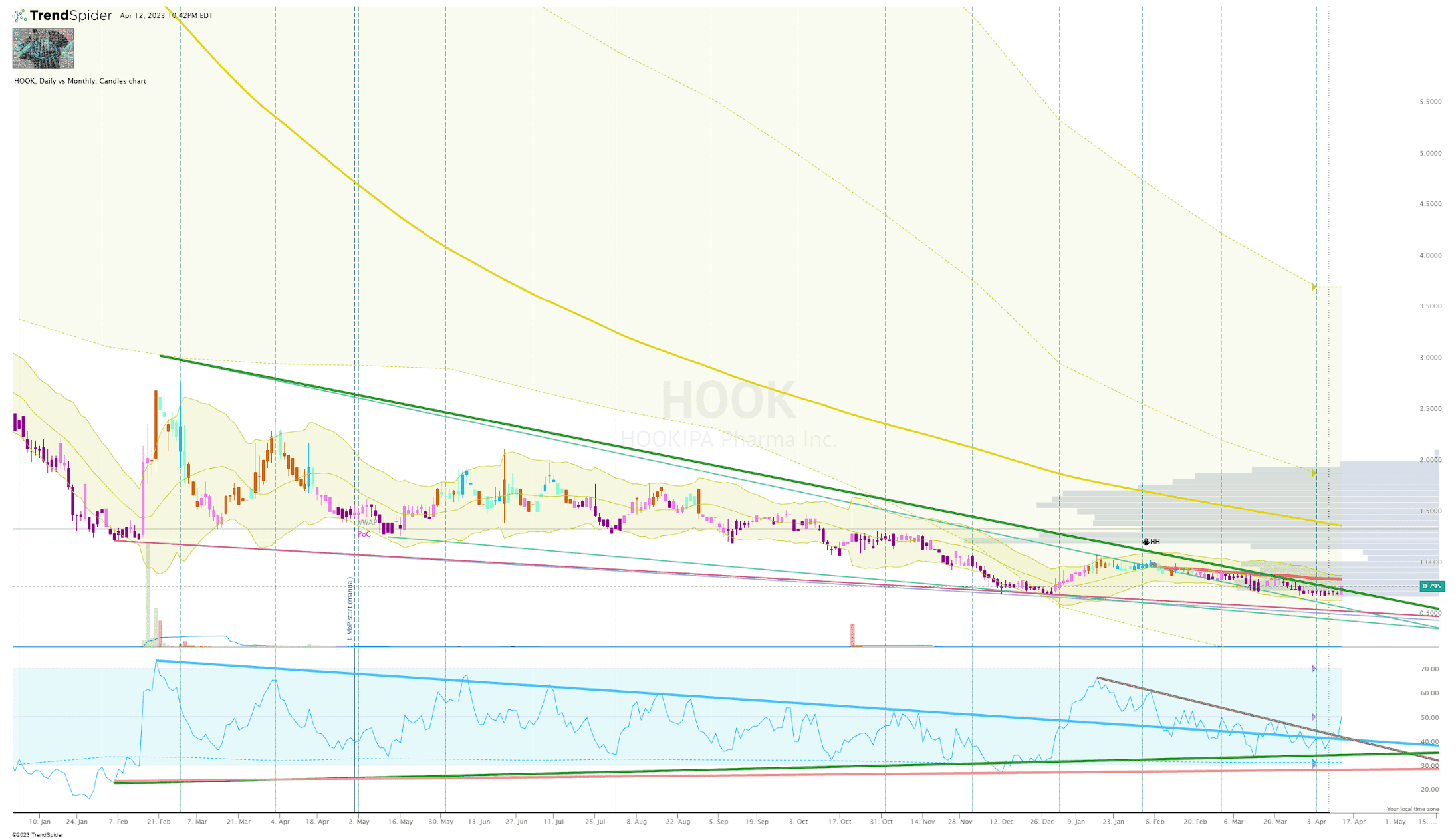

Looking at the daily chart, we can see the share price has been decimated over the past couple of years, so any hint that the company's pipeline contains a winner, we should see a solid mean reversal move that will be supported by a negative enterprise value.

HOOK Daily Chart (Trendspider)

{kind=link}

HOOK Daily Chart Enhanced View ( Trendspider )

Keep in mind, HOOK's market cap is around $40M, so any positive update from one of these programs should probably bring the valuation in line with its cash position, or at least get to a neutral enterprise value. Considering the ticker's enterprise value is around -$60M, we could see the share price more than double following a positive update from one of their pipeline programs. Remember, Gilead could owe roughly $240M in payments plus royalties, and Roche has nearly $1B in payments plus royalties. So, as long as those programs are active, HOOK should remain in play with explosive upside potential. This makes HOOK a great Bio Boom candidate.

Downside Risks

Hookipa was developing a VaxWave candidate, HB-101, for the prevention of human cytomegalovirus "HCMV" infection, which is a type of herpes virus that frequently impacts transplant patient recovery due to an infected transplant organ. This is challenging because the virus invades the patient's immune system that is already intentionally suppressed for transplant and is often unable to fight off the virus. Hookipa administered HB-101 in advance of the transplant to bolster immunity in uninfected patients.

HB-101 produced a robust immune response in the phase I trial and was well tolerated in 36 patients receiving a transplant. In addition, other trial results show HB-101 neutralized HCMV in excess of 12 months, which suggests HB-101 could have developed into a prophylactic for the broad population.

Hookipa's final phase II data revealed that administering two doses of HB-101 did not show superiority at reducing viral infection over placebo in kidney transplant patients. As a result, the company appears to be stepping away from the program, and will most likely not find a partner to explore further development. It should be noted that the failure to achieve the desired marks was not entirely on HB-101, but that the company noticed that "small numbers and lower-than-expected incidence of CMV disease limit conclusion regarding efficacy". So, it is possible that COVID-19 impacted the study and subjects dealt HB-101 a bad hand that did not allow it to show if there was any possibility to continue with a two-dose development. However, the company did see a pathway for a three-dose schedule however, the fact that two doses of HB-101 had no impact on the incidence of CMV infection, syndrome, or disease, or the use of antivirals definitely hurt the program's outlook. Therefore, there is some doubt that Hookipa's infectious disease candidates will be effective enough to make it through the FDA and find their way onto the market.

In addition to the regulatory risks, HOOK is also dealing with the ticker trading below the $1.00 per share threshold to maintain NASDAQ compliance. As a result, Hookipa will have to find a way to get HOOK back above $1.00 per share for at least 10 consecutive trading days, or they will ultimately get delisted from NASDAQ. Typically, a company will perform a reverse split, which reduces the number of shares, thus, raising the price-per-shares well above the $1.00 threshold. Or, a company can rely on catalysts to drive the share price above $1.00 per share and hope it holds above that mark for 10 consecutive trading days. Last but not least, the company can simply wait for the sector to catch a bid and the ticker gets bid up along with their peers. For Hookipa, I believe that all three of these scenarios are possible. However, the threat of a potential reverse split or delisting often weighs on the share price until the issue has been addressed.

Considering these risks, I have provided HOOK with a conviction level of 1 out of 5.

Preliminary Plan

In spite of the company's current value and potential upside, the share price has deteriorated by more than 60% over the past twelve months. This divergence between intrinsic value and market valuation presents an opportunity to get involved in a speculative ticker that is technically oversold and fundamentally undervalued. I suspect the market will continue to focus on the ticker's downside risks, however, upcoming catalysts could force the market to recognize the ticker's prospects and price it appropriately. As a result, I am going to keep a close eye on HOOK and look for a technical entry point. Once I have established a position, I will wait for a data readout to assess the company's prospects and will eventually formulate Buy Targets and Sell Targets for HOOK in order to find a spot in the Bio Boom Portfolio and start my compounding process.

For further details see:

Hookipa Pharma: A Speculative Biotech Worthy Of A Spot On My Watch List