XLU - Hormel Feeds The Bears Some More

2023-08-31 12:29:56 ET

Summary

- Hormel Foods Corporation is in year three of its journey to normalized valuations from bubble peak.

- HRL's Q3-2023 results showed a drop in volumes and net sales, leading to a lowered fiscal 2023 outlook for adjusted EPS.

- Analysts remain far removed from the reality of HRL's struggles, and the stock's valuation continues to be problematic.

Navigating the markets is often an exercise in patience. Good things take time and waiting for valuation to catch up to where it needs to be, tends to take more time than most things. Today, we go over a bubble in the consumer staples sector that is in year three of its journey to normalized valuations. We will go over the most recent results and look at factors that continue to delay the trough.

Hormel Foods Corporation

Hormel Foods Corporation ( HRL ) is a consumer staples giant with about 20,000 employees in the US and around the world. The company has won many accolades, including being one of the best places to work.

Q3-2023 Presentation

Its brands like SPAM, Skippy, and Planters hold key dominant positions in their respective markets.

Our journey on this one began about two and a half years ago. Back then, despite our admiration for the company, we were able to only muster the lowest rating of "Strong Sell". This thesis stood on three legs. Those were extremely poor valuations, limited growth in earnings from margin compression, and a slower dividend growth from slow sales growth. If you needed a quarterly earnings report to put all three in front of investors, we just got one.

Q3-2023

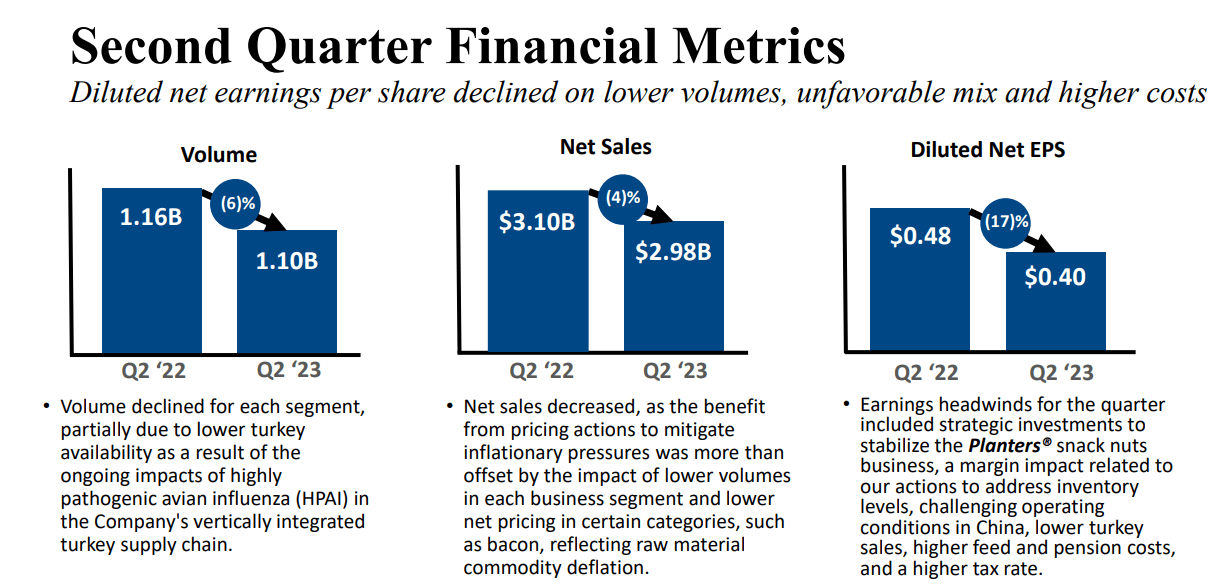

HRL's fiscal year-end is in October, and the results released were for Q3-2023. The last couple of quarters prior to this showed how HRL was struggling with maintaining volumes while hiking prices rapidly. Last quarter (Q2-2023) showed a 6% drop in volumes, a 4% drop in net sales, and a 17% drop in diluted EPS.

{kind=link}

This quarter, HRL finally fixed one out of the three as turkey demand came back in vogue to push volumes up 2%. While we saw broad-based pricing increases in most consumer staples stocks that we follow, HRL was a rare stand-out that managed lower net sales despite volume increases.

{kind=link}

Diluted earnings per share collapsed by 25% but were mainly driven by an adverse arbitration ruling. Excluding that, earnings were flat year over year.

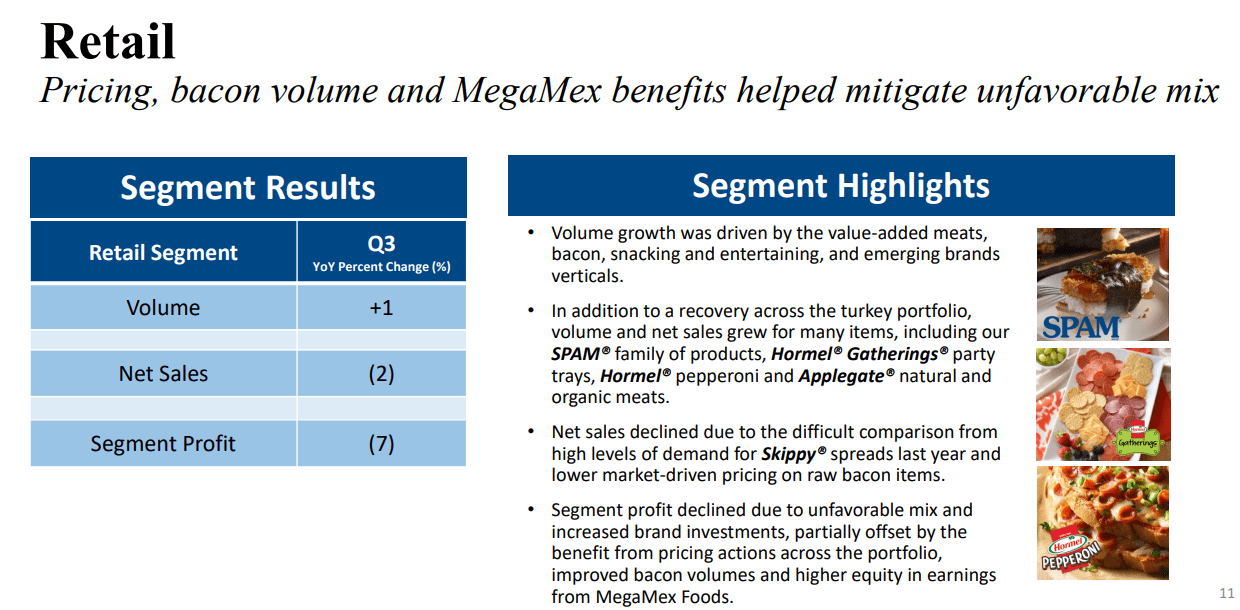

On the segment level, retail was modestly lower, with profits down 7%.

{kind=link}

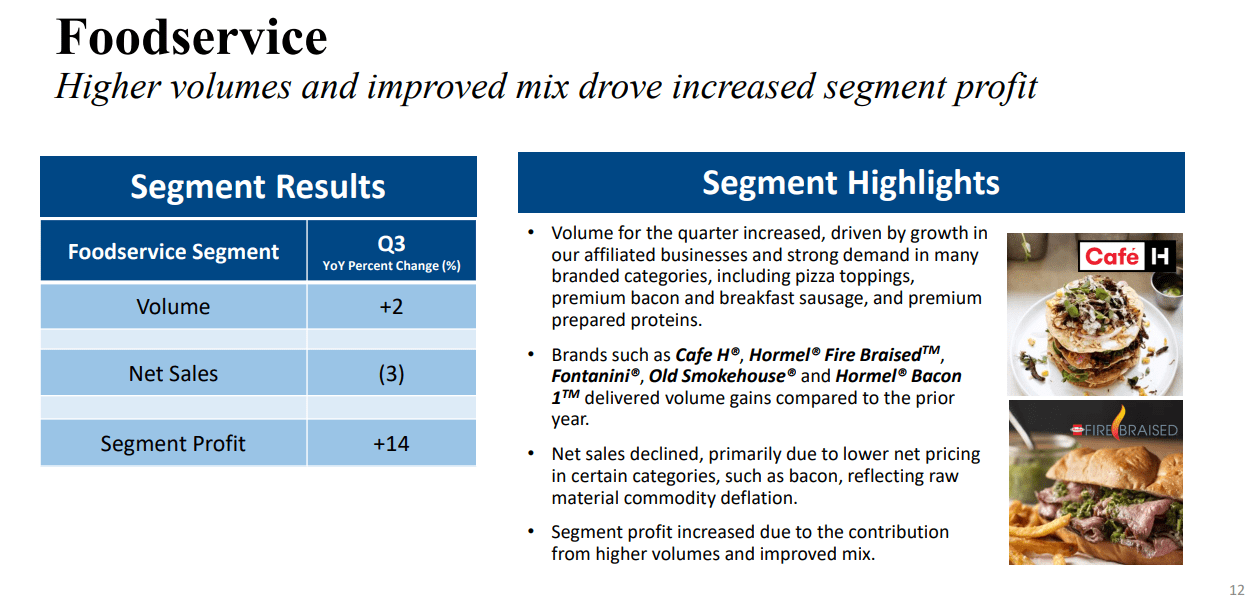

Foodservice was a bright spot with segment profit up double digits.

{kind=link}

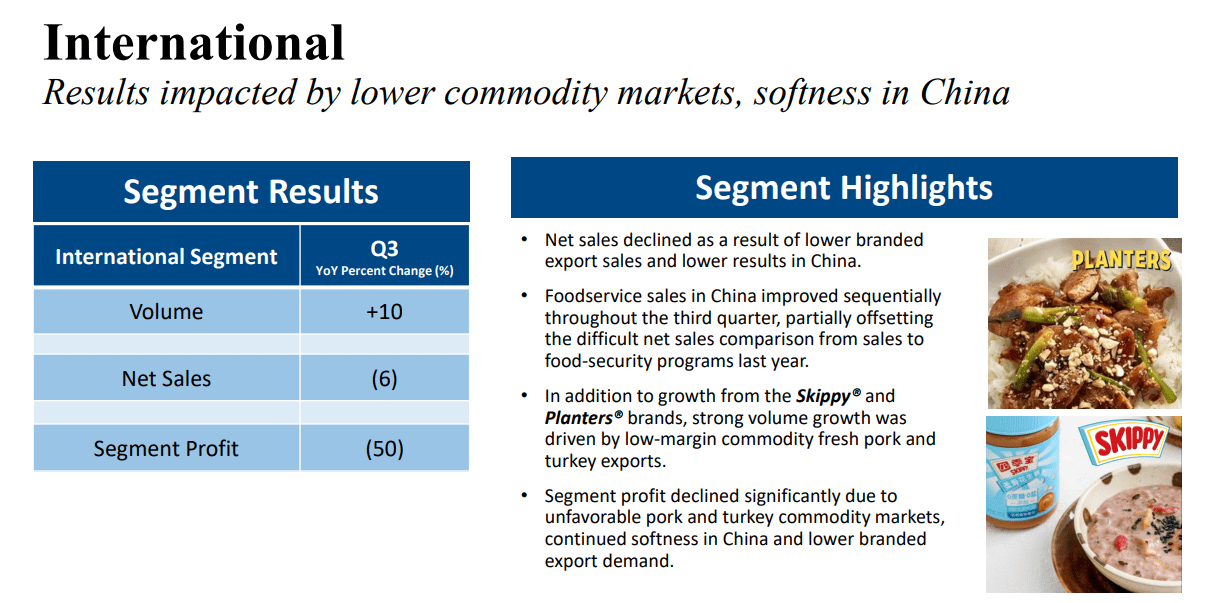

International was a catastrophe, with segment profits down by 50%.

{kind=link}

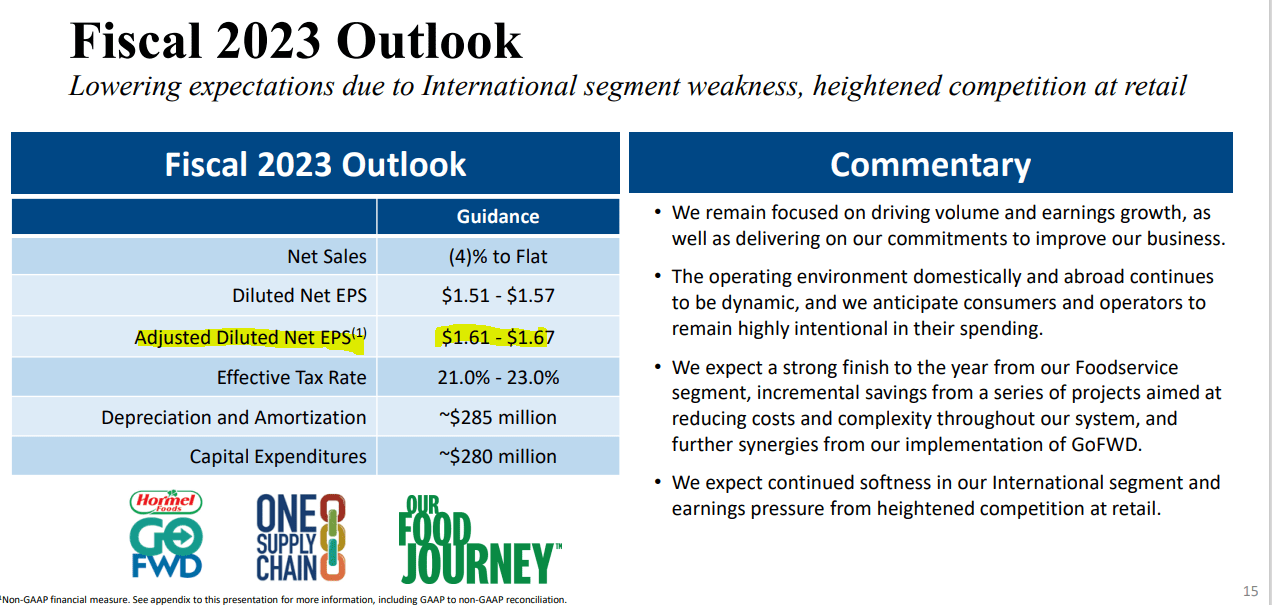

The end result of this weak quarter was that the fiscal 2023 outlook for adjusted EPS was lowered to $1.64 (midpoint) from $1.76 (midpoint) at the end of the last quarter.

{kind=link}

But there is more to this story. While the miss in this quarter at the non-GAAP level (excluding the unfavorable arbitration verdict) was just $0.01 per share, the estimates for the year were driven lower by $0.12. Even worse for the bulls, you just have one quarter left in the fiscal year. So the current estimates for $0.52 for Q4-2023 are off by at least $0.11 per share.

{kind=link}

Analysts again remain far removed from the reality of the situation that HRL is really struggling. This is despite some solid downward revisions over the last six months.

{kind=link}

Our Outlook

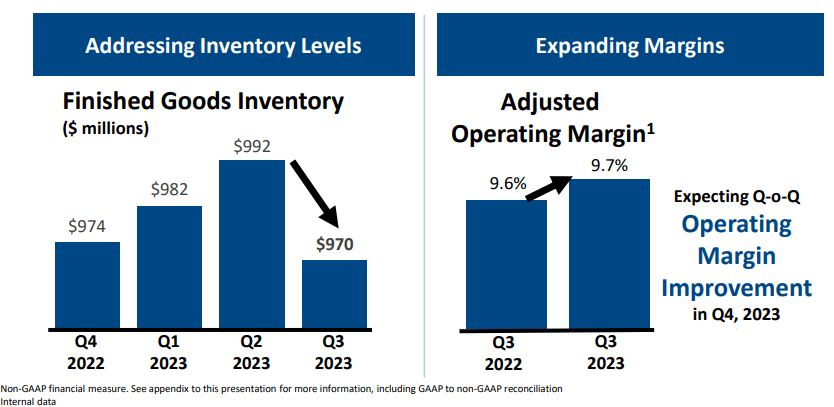

HRL is likely to benefit a bit from peak inflationary pressures being in the rearview mirror. The company noted the improved inventory levels and adjusted operating margins, and those are key for pricing.

{kind=link}

At the same time, the numbers for the next quarter are truly shocking. Analysts downgrades will come in fast and furious and the stock should see negative news flow accelerate. We might see a brief respite if the broader market rolls over as both the consumer staples sector ( XLP ) and the Utilities Select Sector SPDR Fund ETF ( XLU ) are quite oversold on a relative basis.

Verdict

HRL has struggled with volume growth and the only increase in recent times has come from the Planters acquisition. Margins continue to be under pressure, and the adjusted $1.64 will take it back to 2016 levels.

That is all happening, even after the "game-changing" Planters acquisition. Since our first bearish call (See, A Mini SPAM Bubble ), HRL is down 18%.

Seeking Alpha

While it has lagged the broader market by a huge margin, for us the more relevant number is the performance vs XLP. There too HRL's ultra-rich and underserved valuation has acted as a lead anchor.

While we wish we had good news for the bulls, the valuation still looks extremely problematic. The stock is still trading at mid-20s P/E ratio, and the upper end of what we would pay for this business with a risk-free rate of 5% is 16X.

16X is hardly outlandish here as one can get quality consumer staples exposure for far less. Conagra Brands, Inc. ( CAG ), Campbell Soup Co. ( CPB ), and The Kraft Heinz Co. ( KHC ) all trade for far less than HRL today and are even lower than the 16X target multiple we have assigned.

Seeking Alpha's composite valuation indicator, which takes into account multiple metrics, reaches the same conclusion about HRL's valuation with a "D+" rating.

{kind=link}

Our favorite metric price to sales still shows a lot of work needs to be done.

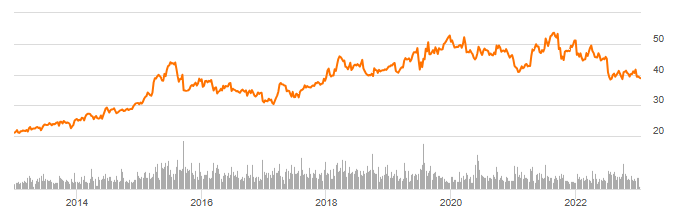

Technically, HRL is also now below key support at $40.00 and the next major level is at $30.00 where the stock bottomed in 2017 and formed a base in 2015.

{kind=link}

While the rapid dividend growth of the 2010-2020 era is the key reason investors fell into the expensive trap in 2021, even that story will come to an end. The payout ratio is climbing rapidly, and room for those 6% annual increases is now decreasing.

We continue to look for more valuation compression and would look to revise our outlook (and our sell rating) at a sub-16X P/E ratio.

For further details see:

Hormel Feeds The Bears Some More