TOL - Hovnanian Enterprises: An Upgrade Is Warranted As Q4 Earnings Near

2023-11-29 15:36:17 ET

Summary

- Hovnanian Enterprises is expected to announce financial results for Q4 of its 2023 fiscal year, showing signs of recovery.

- Revenue and profits have declined recently, but new orders and cancellation rates have improved.

- The company is refinancing debt to push out maturities and reduce interest expense and shares look to be trading on the cheap.

Before the market opens on December 5, the management team at Hovnanian Enterprises, Inc. ( HOV ) is expected to announce financial results covering the final quarter of the company's 2023 fiscal year. For those who don't know, Hovnanian Enterprises focuses on the production and sale of single-family detached homes, attached townhomes, condominiums, and other similar residential developments. From a revenue and profit perspective, the company has experienced a rather difficult year. But recently, there have been signs that a recovery for the business is well underway.

Earlier this year, I found myself taking a rather bearish stance on the homebuilding market. Higher interest rates and inflationary pressures, combined with the concern of a rough landing for the economy, led me to believe that we would see a downturn that would last at least a year for the space. But by the middle of the year, new orders started coming in strong. Unfortunately, this strength occurred shortly after I rated the company a 'hold' back in March. In the article in which I rated the company that, I recognized how cheap shares were, and I stated that I believed the company did have nice potential. But because of the large amount of debt on its books and my outlook for the space, a more neutral stance was the best that I could take at the time. Since then, the recovery has sent the stock up 30.8% at a time when the S&P 500 has increased only 12.5%. Of course, the picture can change at a moment's notice. That is why investors would be wise to see what additional data comes out when management reports financial results next week. If the data continues to look positive, shares could warrant even further upside. But any real pullback in the recovery could necessitate additional caution.

A look at the good and the bad

{kind=link}

To understand just how bad things have been for Hovnanian Enterprises, we should look at the most recent financial data provided by management. This data involves the third quarter of the company's 2023 fiscal year. During that quarter, revenue for the company came in at $650 million. That represents a decline of 15.3% compared to the $767.6 million the company reported one year earlier. This drop in revenue was really driven by one factor. And that was a drop in the number of homes delivered from 1,412 to 1,198. This was somewhat offset by an increase in the average price per home delivered from $521,710 to $526,186.

{kind=link}

On the bottom line, the picture also showed signs of deteriorating. Net income actually fell from $79.9 million to $53.1 million. At a time when significant weakness developed in the space, it should be no surprise that the company would have to cut down on its margins in order to attract customers. So I am not surprised by this fall in profits. All other profitability metrics worsened as well, with the exception of one. That would be operating cash flow. It shot up from $33.6 million to $225.6 million. But if we adjust for changes in working capital, we would get a decrease from $77.3 million to $48.8 million. Over the same window of time, EBITDA for the company plunged from $146.7 million to $108.9 million. For context, I also showed in the chart below, the financial data for the first nine months of this year relative to the same time last year. As you can see, revenue, profits, and cash flows remain depressed, indicating that the most recent quarter was not a blip on the radar.

{kind=link}

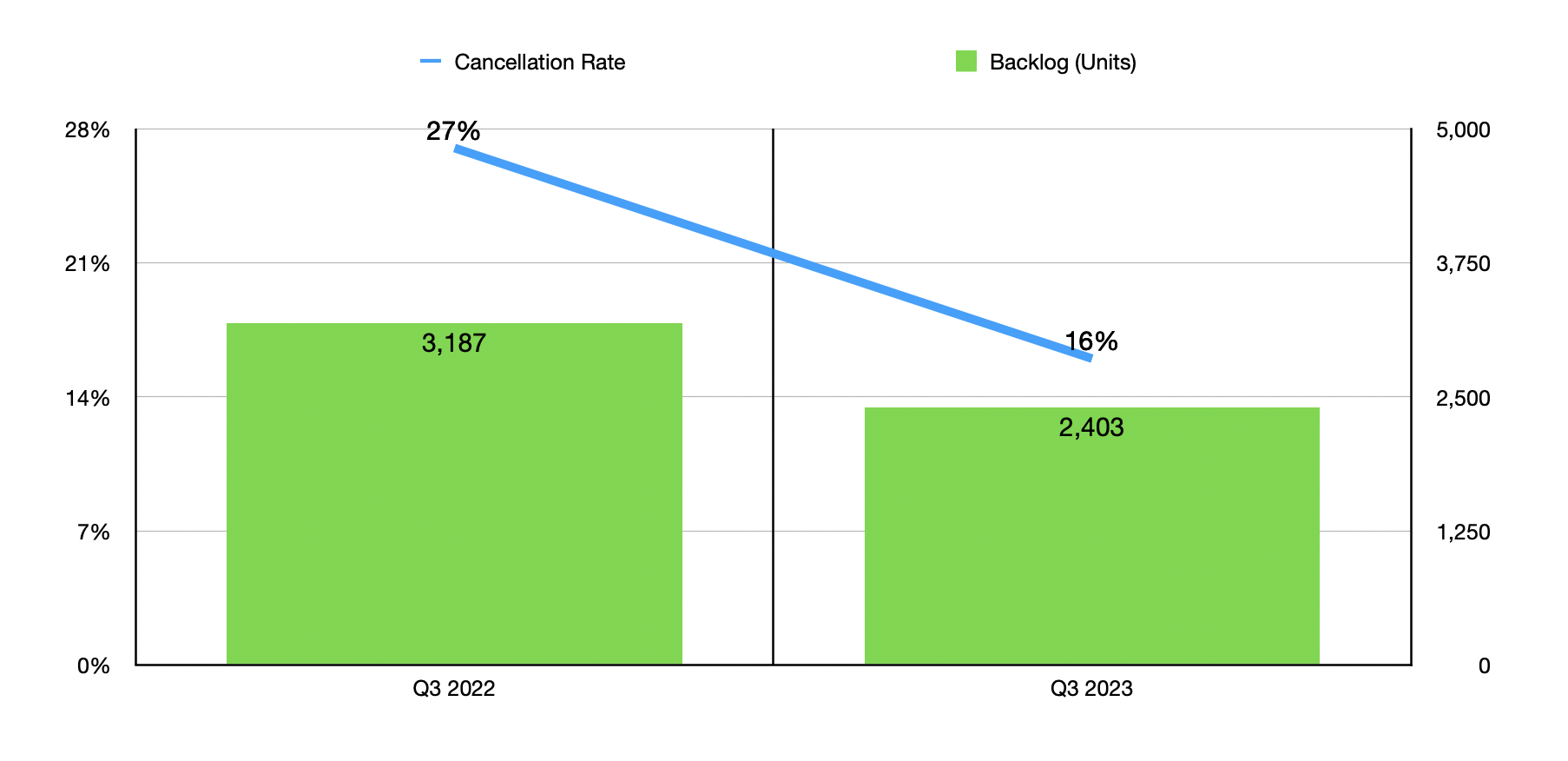

There were some other worrying signs for the company as well. As an example, the backlog for the business ended during the third quarter at 2,403 units. That's down from the 3,817 units reported at the same time last year. The backlog can be a good indicator of what future revenue and profits will be since it is a good barometer of demand for the company's offerings. But the great thing for shareholders is that this is the only leading indicator reported by the company that looked negative. There were others that came in that showed improvements on a year-over-year basis. As an example, the cancellation rate in the most recent quarter was 16%. While higher than I would like to see, it does mark a stark improvement over the 27% cancellation rate reported one year earlier.

{kind=link}

{kind=link}

Even more important were the net new contracts that the company locked in. During the most recent quarter, Hovnanian Enterprises reported new contracts for 1,444 homes. That's almost double the 799 reported for the same time one year earlier. But there is a slight negative to this. And that is that management only achieved this improvement by lowering prices. The average home price of a new contract in the first quarter of last year was $585,656. That number has now been reduced to $515,701.

{kind=link}

It would be wise, of course, for investors to pay attention to what data comes out when management announces financial results next week. There aren't any formal estimates that analysts have provided. However, management did forecast revenue for the year in its entirety of between $2.6 billion and $2.7 billion. At the midpoint, that would imply sales of between $731 million and $831 million. That would be down from the $886.8 million reported one year earlier. A drop in price for deliveries from the $541,971 reported last year and a drop in the total number of deliveries from the 1,599 units reported then, could be the main drivers behind such a fall. In the table above, you can see other financial data for the final quarter of 2022 for context.

{kind=link}

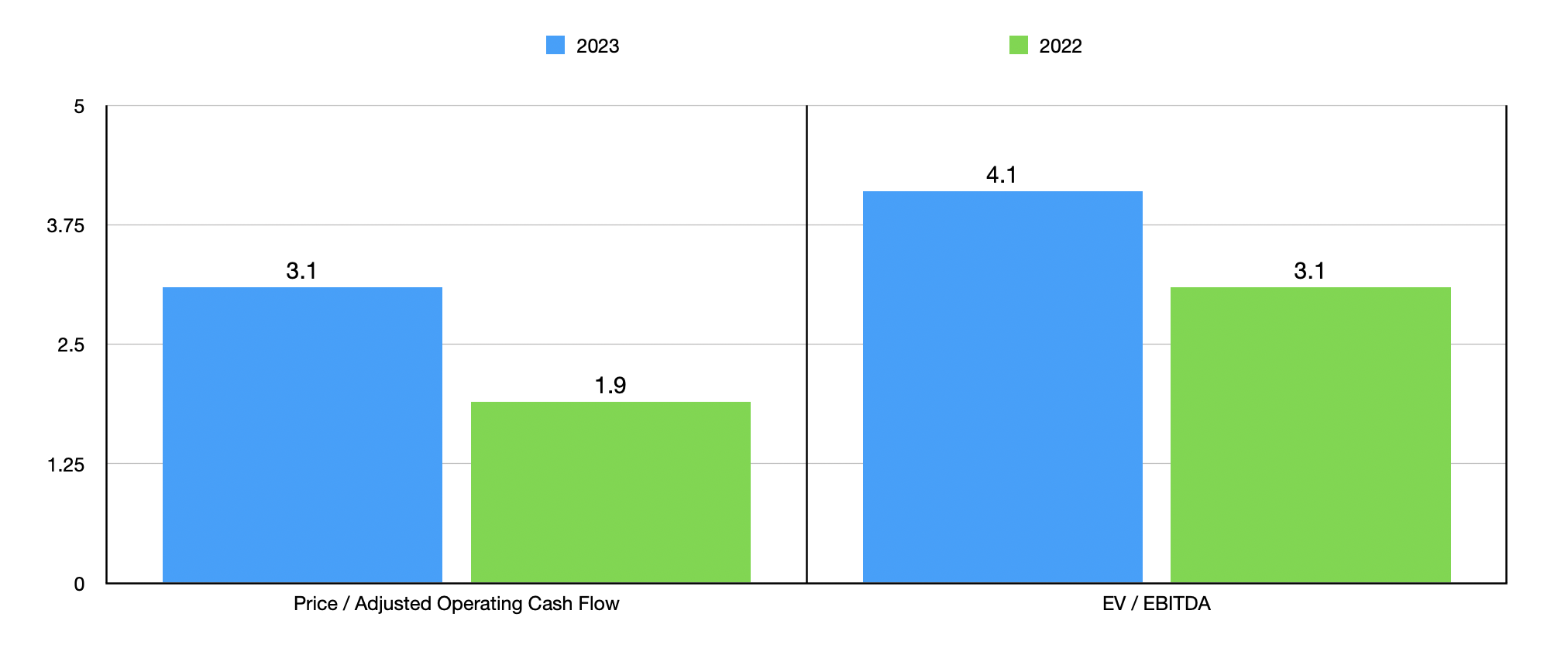

On the bottom line, for the year in its entirety, management has been forecasting EBITDA of between $350 million and $370 million. If this comes to fruition, it would imply an adjusted operating cash flow of around $198 million for the year. Using this data, I was unable to value the company as shown in the chart above. I also valued it using data from 2022. In the table below, I compared the firm to five similar enterprises. And under either scenario, it ended up being the cheapest of the group.

| Company |

| Price / Operating Cash Flow |

| EV/ EBITDA |

| Hovnanian Enterprises, Inc. |

| 3.1 |

| 4.1 |

| Beazer Homes USA, Inc. ( BZH ) |

| 4.5 |

| 7.6 |

| Legacy Housing Corporation ( LEGH ) |

| 44.3 |

| 6.8 |

| Landsea Homes Corporation ( LSEA ) |

| 4.0 |

| 13.9 |

| M/I Homes, Inc. ( MHO ) |

| 4.2 |

| 4.8 |

| Toll Brothers, Inc. ( TOL ) |

| 5.0 |

| 5.2 |

Outside the change in financial condition that management has reported, there's also the fact that, on September 25, the company announced that they were essentially refinancing some of their debt. The end goal here is to push out over $600 million worth of debt that is to come due between 2025 and 2026 to between 2028 and 2029. Although interest rates are higher now, the increase in interest expense should only amount to roughly $1.3 million per annum. That is a small price to pay for a longer-term debt maturities.

Takeaway

Based on the data provided, Hovnanian Enterprises seems to be doing fine. The most recent financial data is discouraging. But when you dig deeper and look at the leading indicators, the firm is in the early stages of what looks to be a robust recovery. It would be a good idea for investors to continue to pay attention to the key metrics on this front. So long as we continue to see improvements in orders, I would make the case that the stock looks cheap enough to warrant an upgrade from the 'hold' I had it rated previously to a 'buy' today.

For further details see:

Hovnanian Enterprises: An Upgrade Is Warranted As Q4 Earnings Near