SBNY - How Low Can Signature Bank Go? We Think $70/Share

2023-03-09 19:29:09 ET

Summary

- Signature Bank is a full-service commercial bank that was established in 2001 in New York City.

- SBNY has increased its depositor base in the past years by catering to the players in the crypto market.

- Signature Bank does not lend in the crypto space, nor does it have loans that are backed by crypto assets.

- As SBNY shrinks its non-interest bearing deposits in the crypto space, its profitability will take a large hit.

- We feel the bank will revert to an EPS profile more closely resembling what it was posting pre-COVID (i.e. the crypto boom).

Thesis

We recently wrote an article regarding Signature Bank's (SBNY) preferred shares here , where we argued rates were the main risk factor driving their performance. The story is quite different when we consider the common equity. With Silvergate Capital ( SI ) winding down operations, the hunt is on for the next shoe to drop in the crypto banking space. Signature Bank is down over -5% as we speak, and is now down almost -30% in the past month as the price is trying to bounce off its historic resistance/support level of $100/share.

The main driver for the current move is the contagion aspect, and unclarity with respect to SBNY's involvement in the crypto space. Let us have a look at what SBNY actually does in crypto and where things are headed for the bank. SBNY has itself started to proactively address market concerns around its involvement in crypto:

NEW YORK--(BUSINESS WIRE)-- Signature Bank (Nasdaq: SBNY), a New York-based, full-service commercial bank, addressed an article today that appeared in the Monday, January 23, 2023 edition of the Wall Street Journal titled “U.S. Home-Loan Banks Help Crypto Lenders Stem Outflows.” The article includes inaccurate statements that the Bank would like to clarify.

The headline falsely refers to Signature Bank as a “crypto lender.” Signature Bank does not lend in the crypto space, nor does it have loans that are backed by crypto assets. Additionally, the Bank does not invest, does not hold, and does not custody crypto assets. Signature Bank’s relationships with clients in the crypto space are limited to U.S. dollar-denominated deposits only.

The article also incorrectly states that Signature Bank is “rushing to stem a flood of customer withdrawals.” In the fourth quarter of 2022, the Bank announced a plan to purposely decrease deposits in the digital asset banking space by reducing the size of relationships; thus, these deposits are declining as the Bank is intentionally managing them to a lower level.

Let us be clear - the main risk factors for crypto related businesses has been around trading / holding crypto and ancillary services such as lending, custody and leverage offered. These are all market risks, and talk about the propensity of an entity to incur loses when engaging in such activities. SBNY does none of that as per the above.

Non-Interest Bearing Deposits Matter when Fed Funds are over 4%

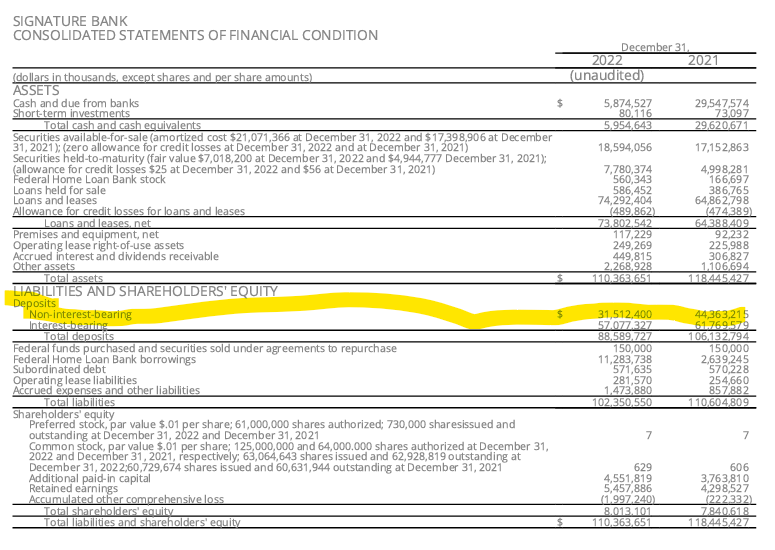

What does SNBY do? They hold crypto related dollars and clear transactions in the space. What does that do for them? Well, it gives them a massive amount of deposits for which they pay very little:

{kind=link}

2022 Balance Sheet (Bank Presentation)

We can see how non-interest bearing deposits reached a peak in 2021 during the crypto frenzy, and have now moved lower to "only" $31 billion. This number is going to move even lower, with the bank targeting a lower figure. We assume many of the players in the crypto space were more interested regarding having an operationally viable platform rather than being paid Fed Funds on their deposits. When Fed Funds were at 0.1% it did not matter much, now at 4.5% it is a different ball-game all-together.

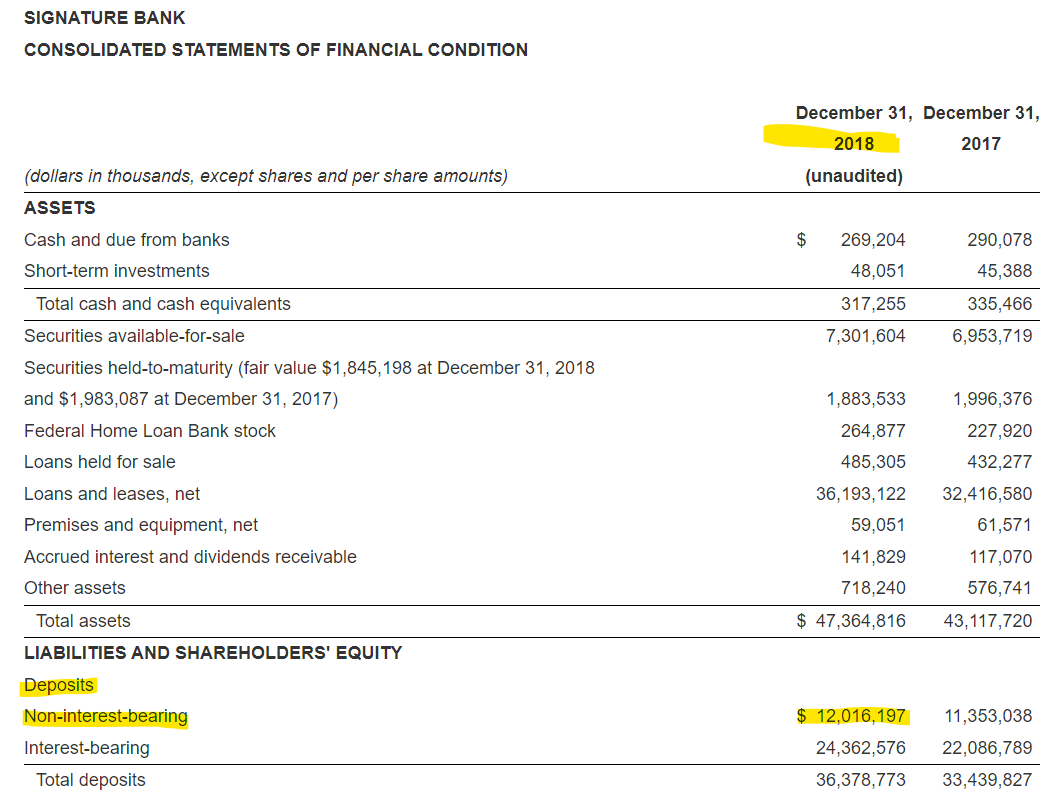

Let us compare this 2022 Q4 snapshot with a similar one from the 2018 Q4 that the bank put out:

{kind=link}

2018 Balance Sheet (Bank Financials)

Quite a different figure in 2018. Basically that balance sheet line item quadrupled from 2018 to 2021, and is now coming back down. A bank's traditional 'money maker' is the net interest income figure, or simply put the difference between what it makes on its loans or investments versus what it pays to its depositors on their funds. SBNY's profitability has been strongly correlated to this line item. As this figure moves down, SBNY's EPS are going to come down and negatively affect its share price.

What is the new target price?

We do not see any losses for SBNY related to crypto assets market risk. However, as the bank shrinks its depositor base in the space, its net interest margins will suffer. A high figure for non-interest bearing deposits simply means a free money machine. Just multiply $31 billion by 4.5% to understand what levels of free cash SBNY is clipping right now.

As its non-interest bearing depositor base shrinks, the bank will have lower earnings per share. We feel the past is a good guidepost for this bank, with pre-crypto boom EPS levels providing a good starting point:

Historic EPS (Seeking Alpha)

We can see how the bank's EPS exploded after 2020. Pre-COVID, we were looking at $10/share in EPS. We feel we are headed back that way. Utilizing the current P/E ratio of 7x for the bank, gives us a share price of around $70, or around -30% downside from here.

Risk Factors

We believe there are exogenous risk factors for SBNY stock related to legal risk of dealing with the crypto space. Just like Tom Brady got sued for his endorsement for FTX (FTT-USD), SBNY is currently being sued for something similar. Expect this to persist. Every time there are large losses investors tend to just sue everybody to see if anything sticks. We are not lawyers but these things usually take time and have a high burden of proof. We are doubtful that SBNY as an entity was fully aware of what was going on with FTX, but the courts will settle that. A large negative settlement here (from the FTX lawsuits or others) can put further pressure on the share price. It is very hard to quantify legal risk here though, and if it was quantifiable from an accounting standpoint the bank would be forced to take a loss provision on it.

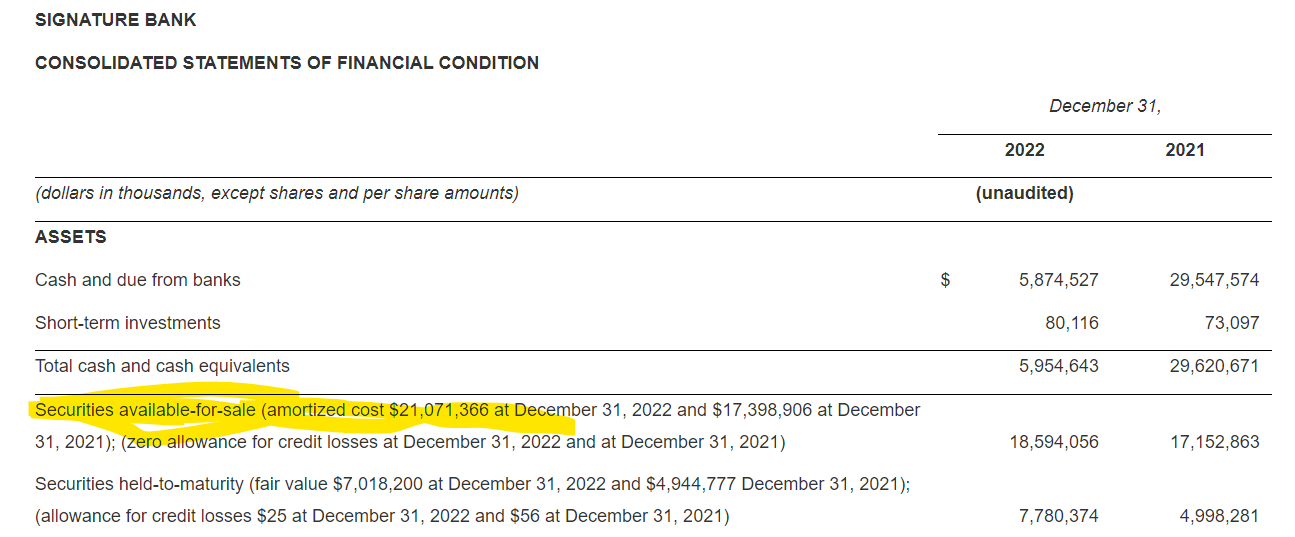

Available for Sale Securities

The concern right now with many regional banks is around their available for sale portfolios and the extent of 'hidden' mark to market losses:

Available-for-sale (AFS) is an accounting term used to describe and classify financial assets. It is a debt or equity security not classified as a held-for-trading or held-to-maturity security—the two other kinds of financial assets

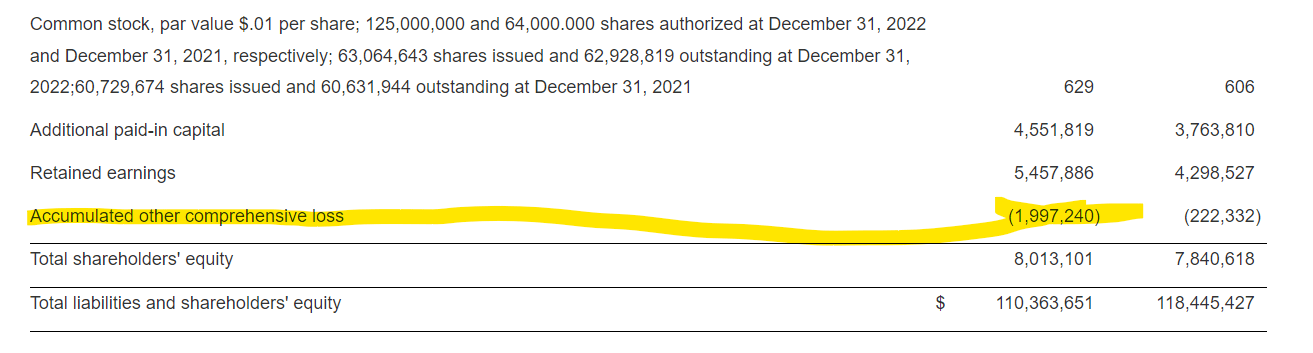

A mark to market asset is priced daily and goes through the profit and loss. Held to maturity refers to bonds a bank will hold until they mature, hence an accrual profit and loss method. In between one finds AFS, where the losses do not hit earnings, but a line item called OCI (other comprehensive loss). SBNY has about $21 billion in AFS securities:

{kind=link}

And the unrealized losses that have been put through OCI are around $1.9 billion:

{kind=link}

These are not large figures when compared to what Silicon Valley Bank (SIVB) posted today. In essence a bank only realizes the OCI if they really mis-manage their asset/liability profile. We think SBNY has a moderate OCI issue in respect to AFS securities, one that can be managed properly. We assign a low probability to SBNY taking hits on actual AFS sales.

Conclusion

SBNY is a commercial bank which aimed to grow by addressing banking needs in the crypto space in the past few years. Signature Bank does not lend in the crypto space, nor does it have loans that are backed by crypto assets. Its market risks around the crypto space are limited, with only its depositor base stemming from this niche being impacted. We can see how SBNY virtually quadrupled its non-interest bearing deposit base from 2018 to 2021 as the crypto mania took hold. The bank still has $31 billion in non-interest deposits, which at 4.5% Fed Funds rates represent a fairly profitable way of making money. This figure is going to continue to shrink, which will affect profitability. The bank also runs the risk of exogenous one-time lawsuit fees payable if its involvement in the crypto space was not at arm's length with respect to its counterparts' practices. We feel SBNY will revert to its pre-crypto boom EPS profile, which was around $10/share. Utilizing the current P/E ratio for the bank gives us a floor price of around $70/share.

For further details see:

How Low Can Signature Bank Go? We Think $70/Share