ACTV - How Rates Stand After The Fed Pause

2023-06-20 12:00:00 ET

Summary

- Skyrocketing inflation led to aggressive interest rate hikes by the Fed.

- These are nearing their end, with the Fed keeping rates steady at its last meeting.

- A look as to where interest rates stand follows.

Author's note: This article was released to CEF/ETF Income Laboratory members on June 16th.

With the Fed's recent decision to keep rates on hold, thought to write a quick article on where interest rates stand. Four facts stand out.

Nominal interest rates remain elevated, which means higher yields for most bonds and bond funds, and the potential for moderate capital gains, contingent on inflation and rates normalizing.

Real interest are slightly below their historical averages, but rapidly increasing. Bonds should see strong returns if inflation continues to normalize, weak otherwise.

Spreads between long-term bonds and short-term bonds are significantly below average, so short-term bonds look particularly compelling right now.

Spreads between investment grade and non-investment grade bonds are a bit narrower than average, as economic conditions and investor sentiment are both broadly bullish.

In my opinion, as interest rates are elevated and inflation rapidly normalizing, bonds are strong investment opportunities right now. Focusing on high-yield corporate bonds, due to their strong yields, seems best. Safer assets, including T-bills, have very respectable yields too, for those investors wishing to minimize risk.

Nominal Rates Remain Elevated

Nominal rates remain elevated across the board. Federal Funds Rate are at 5.00% - 5.25%, benchmark 10Y treasury rates at 3.8%, and high-yield corporate bonds at 8.0%. All three are at their highest levels in over a decade, as is the case for most relevant interest rates. A quick table on some of these.

Seeking Alpha and Bankrate - Chart by author

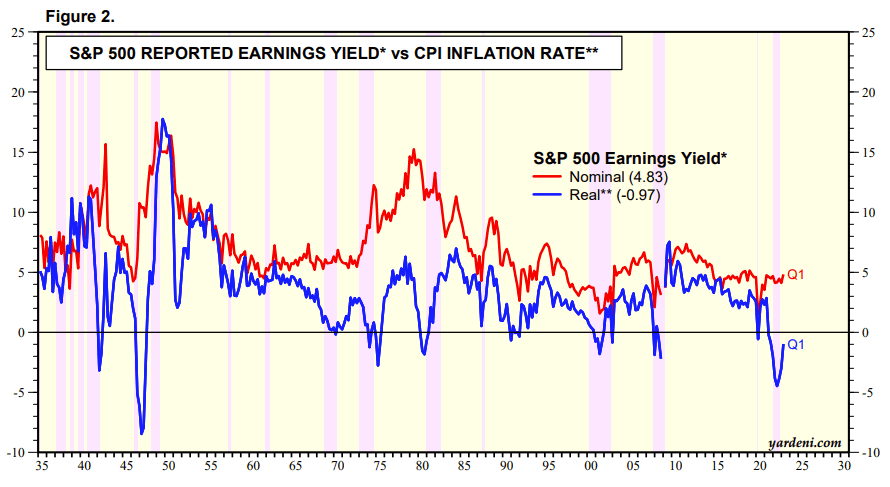

As rates increase, so does the attractiveness of bonds and other fixed-income securities, especially in comparison to equities. As an example, the S&P 500 earnings yield is currently a bit lower than the yield on BBB-rated corporate bonds, even though equities are much riskier, and junior to bonds.

JPMorgan Guide to the Markets

The gap between high-yield corporate bonds and equity earnings yield is even wider, at around 2.5% for BB-rated securities.

Data by YCharts

Higher nominal interest rates means higher income for bond investors, and the potential for some capital gains if interest rates normalize.

Due to the above, investors might consider investing in bonds and other fixed-income securities, especially those wishing to avoid equity volatility and risk. Conservative investors and retirees might prefer to focus on safe T-bills yielding +5.0% over more volatile, lower-yielding equities. More aggressive income investors might prefer to focus on high-yield bonds, as these should be yielding around 8.0%. Lots of choices here, most offering strong, competitive yields.

Looking at ETFs, the FlexShares High Yield Value-Scored Bond Index Fund ETF ( HYGV ) offers a particularly strong 9.9% SEC yield, highest for a bond fund, excluding leveraged funds and the like.

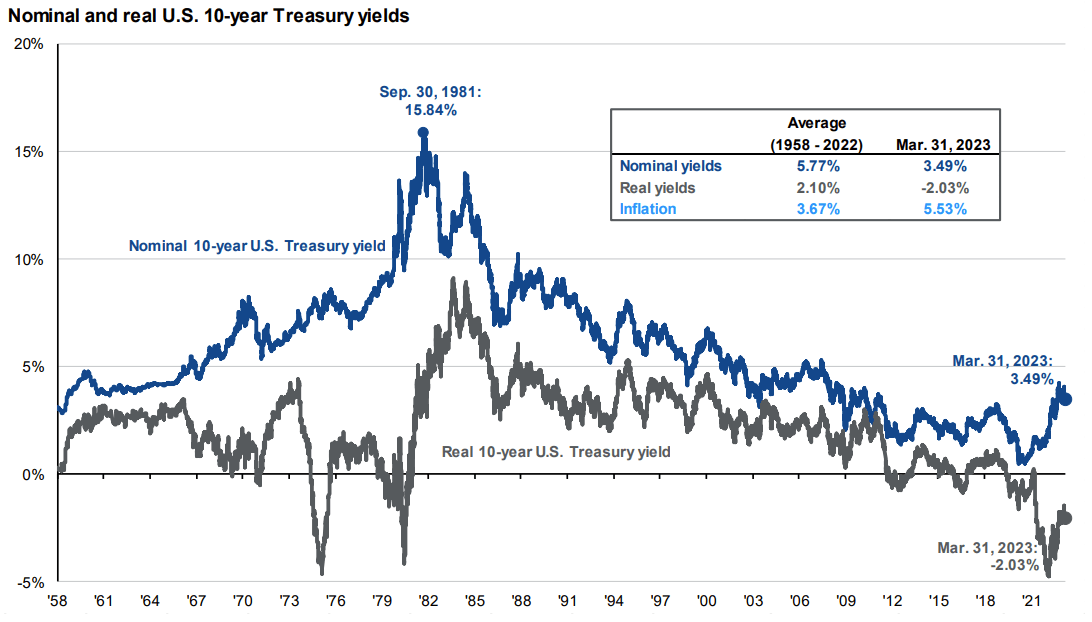

Real Rates Are Low, But Increasing

Real rates, defined as nominal rates minus inflation, are quite low, but rapidly increasing. As per JPMorgan ( JPM ), 10Y real yields stood at -2.0% in 1Q2023, much lower than their historical average, but quite a bit higher than their 2022 lows. By my calculations, 10Y real yields currently stand at -0.2%, in line with their 2010s averages. Inflation continues to decrease on a monthly basis, which could result in 2.0% - 3.0% real yields in the coming months, much higher than their recent historical averages.

{kind=link}

Considering the above, it seems markets are pricing in a moderate decrease in inflation from here on out, but not a return to the Fed's long-term 2.0% target. Meaning, inflation of 2.0% means strong bond real yields, which should lead to strong bond returns. On the other hand, if inflation remains at 4.0%, real yields would be negative and somewhat below-average, so bond returns would almost certainly be quite weak.

In my opinion, inflation is likely to normalize from here on out, as has been the case since late 2022, and as most of the key inflation drives, including supply chain issues and the Ukraine War, prove to be transitory. Due to this, I expect strong bond returns moving forward. Long-term bond funds, including the iShares 20+ Year Treasury Bond ETF ( TLT ) and the iShares 25+ Year Treasury STRIPS Bond ETF ( GOVZ ), would see the highest gains in this scenario. These funds have very high interest rate risk, so I'm not sure that their overall risk-return profile is the best.

As a final point, thought it interesting that the S&P 500 real earnings yield is at its lowest since the 40s . I'm unsure about the implications of this, considering inflation does boost corporate revenue, although I imagine the situation will normalize soon enough.

{kind=link}

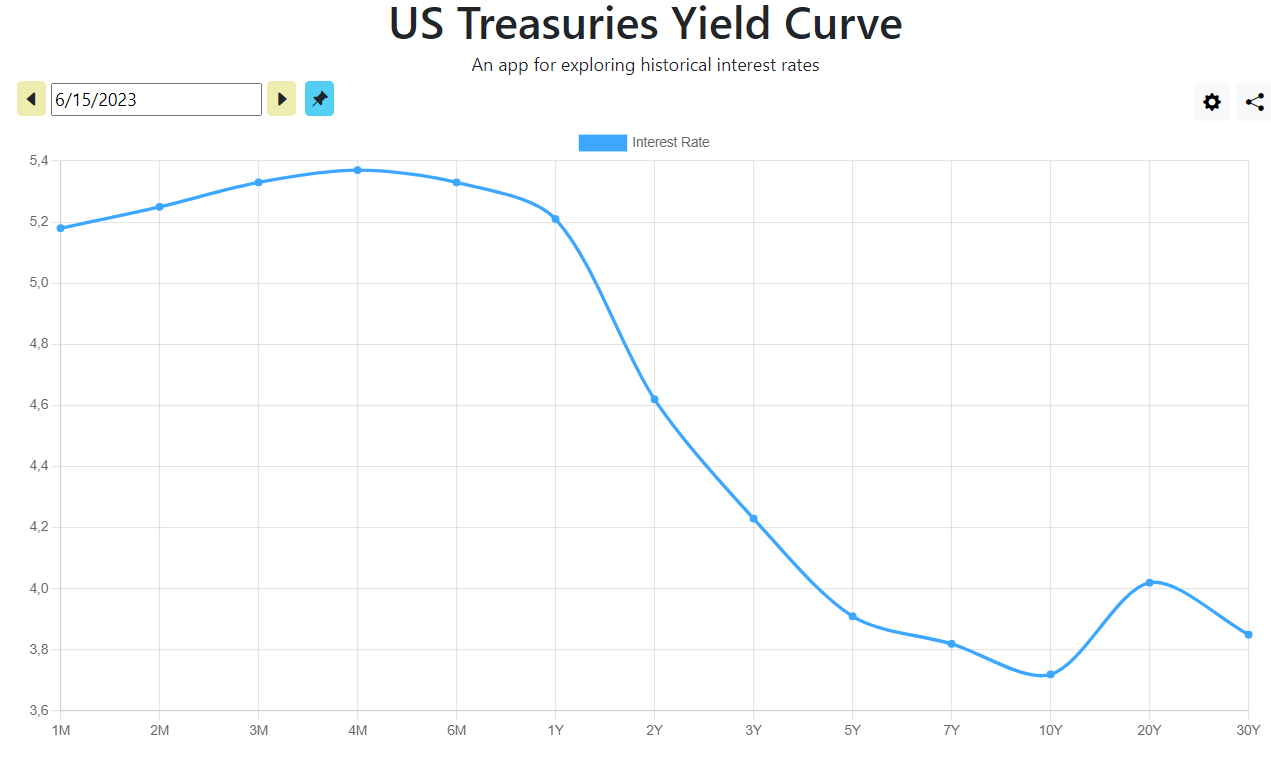

Inverted Yield Curve

In the vast majority of cases, long-term bonds have higher interest rates than comparable short-term bonds, to compensate investors for locking up their cash for longer periods of time, and as compensation for increased interest rate risk.

Right now, the opposite is true, with long-term bonds generally yielding more than comparable short-term securities. As an example, the current treasury yield curve.

{kind=link}

As can be seen above, treasury yields peak around the 4M mark, then steadily decline until the 10Y mark. Right now, the yield curve reflects the market's expectation of future interest rates. The market expects the Fed to hike once or twice in the coming months, as per Fed soft guidance, and for rates to decline afterwards, as inflation continues to ease.

Currently, short-term bonds offer higher yields than long-term bonds, but lower potential capital gains if inflation continues to decline (more than expected).

In my opinion, short-term bonds are the more compelling investment right now, as these offer higher yields and lower overall risk. Long-term bonds do offer greater potential capital gains, contingent on inflation and rates normalizing faster than expected , but this is an uncertain benefit. Focusing on T-bills and receiving a safe, certain +5.0% yield seems better than investing in 10Y treasuries yielding +3.8%, hoping inflation and rates decrease more than expected.

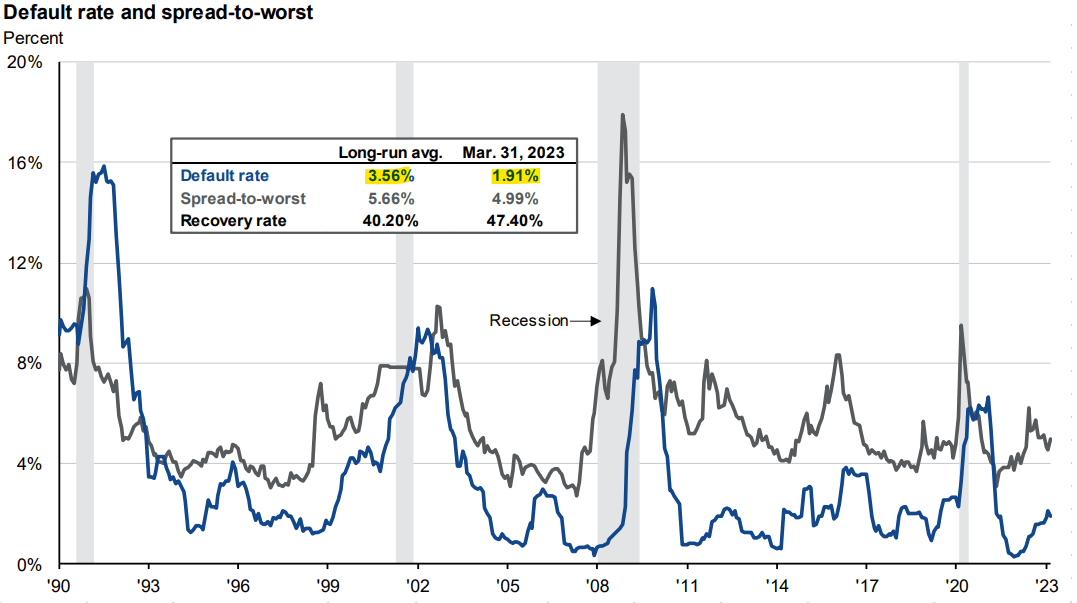

Slightly Narrow Credit Spreads

Non-investment grade bonds effectively always yield more than investment-grade bonds, to compensate investors for their greater level of risk. Spreads do vary. These tend to be wide when the economy is weak and investors are fearful, narrow when the economy is strong and investors are bullish.

Right now, spreads are slightly more narrow than average, due to reasonably strong economic conditions and bullish sentiment. Default rates, of particular importance to bonds, are quite low right now, lower than their historical average. Importantly, a recession or downturn is not priced-in at these spreads, something for more bearish investors to consider.

{kind=link}

In my opinion, high-yield bonds are currently well-priced, and so are perfectly fine investment opportunities. Overall, I would pick high-yield bonds over T-bills and the like, for the yield. Other, more conservative or bearish investors might disagree. Seems obvious and not particularly informative, but spreads are at (roughly) historically average levels, so there is little room for further analysis or a different conclusion.

Conclusion

Right now, nominal interest rates are elevated, real interest rates are a bit low, the yield curve is inverted, and credit spreads are about average. In my opinion, under these conditions, bonds are strong investment opportunities, especially high-yield corporate bonds.

For further details see:

How Rates Stand After The Fed Pause