HWM - Howmet Aerospace: Commercial Aerospace Leading To Consistent Growth

Summary

- Revenue, EBITDA and earnings per share were all up for the fifth consecutive quarter.

- Commercial aerospace will be the key driver over the next two to three years.

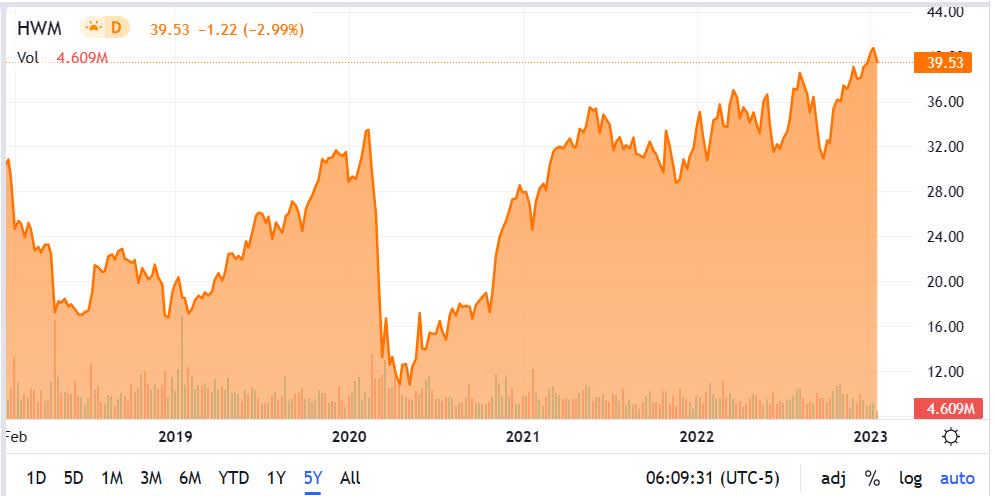

- Since dropping to approximately $10 per share in May 2020 from the impact of the pandemic, the share price of HWM has rebounded nicely, and should continue to grow through.

Howmet Aerospace Inc. ( HWM ) has been recovering nicely ever since it hit a low of approximately $10.00 per share on May 11, 2022, as a result of its share price getting hammered from the pandemic.

Since that time, it is up about 4x as I write, trading at just under $40.00 per share after hitting a 52-week high of $41.02 on January 9, 2023.

{kind=link}

The company has been growing revenue and earnings on a consistent basis recently, as the overall commercial aerospace market continues to recover, led by the North American and European markets.

That has resulted in commercial aerospace being the key catalyst driving the performance of the company, which at this time accounts for just under half of company revenue, and if it recovers to levels near pre-pandemic levels, could once again reach 60 percent of total revenues.

In this article we'll look at some of its recent numbers, the strength and significance of commercial aerospace, and what the next three years look like for HWM.

Some of the numbers

Revenue in the third quarter of 2022 was $1.43 billion, compared to revenue of $1.28 billion in the third quarter of 2021. Revenue in the first nine months of 2022 was $4.15 billion, compared to revenue of $3.7 billion in the first nine months of 2021.

The company guided for fourth quarter revenue to be in a range of $1.45 billion to $1.5 billion.

Adjusted EBITDA in the reporting period was $323 million, up 11 percent from the third quarter of 2021. The improvement in adjusted EBITDA was attributed to an increase in volume in its commercial aerospace segment.

Adjusted EBITDA margin was 22.5 percent, down 30 basis points year-over-year.

Net income in the third quarter of 2022 was $80 million, or $0.19 per diluted share, compared to net income of $26 million, or $0.06 per diluted share in the third quarter of 2021. Net income in the first nine months of 2022 was $356 million, or $0.84 per diluted share, compared to net income of $179 million, or $0.41 per diluted share in the first nine months of 2021.

The company guided for fourth quarter EPS to be in a range of $0.37 per share to $0.39 per share.

For the fifth quarter in a row, revenue, EBITDA and earnings per share were up.

Free cash flow in the reporting period was $23.00 million.

Cash and cash equivalents at the end of the third quarter of 2022 was $453 million, compared to cash and cash equivalents of $720 million at the end of calendar 2021. Not including debt due within one year, at the end of the third quarter of 2022 the company held long-term debt of $4.17 billion, compared to long-term debt of $4.23 billion at the end of calendar 2021.

Performance by segment

Engine Products

Revenue in its Engine Products segment was $683 in the third quarter of 2022, up 14 percent year-over-year. The improvement was the result of its commercial aerospace and oil and gas markets growing, and a boost in material cost pass through.

Adjusted EBITDA in Engine Products was $186 million, up 23 percent from the third quarter of 2021. The improvement was attributed to gains in productivity and an increase in commercial aerospace and oil and gas volumes.

Adjusted EBITDA margin came in at 27.2 percent, up approximately 200 basis points from the same reporting period of 2021.

Fastening Systems

Revenue in its Fastening Systems in the third quarter of 2022 was $291 million, up 15 percent year-over-year. The improvement was attributed to its commercial aerospace market growing by 24 percent and an increase in material cost pass through.

Adjusted EBITDA in Fastening Systems was $64 million, an increase of 8 percent year-over-year. An improvement in volume in the narrow body commercial aerospace market was the positive catalyst there.

Adjusted EBITDA margin was 22.0 percent, down approximately 120 basis points from the third quarter of 2021.

Forged Wheels

Revenue in the Forged Wheels segment was $266 million, up 15 percent from the third quarter of 2021. An increase in volume of 2 percent and an increase in material cost pass through were the main drivers in the reporting period.

Adjusted EBITDA in the third quarter of 2022 was $64 million, down 11 percent from the third quarter of 2021. Most of that was from unfavorable FX.

Adjusted EBITDA margin in the segment was 24.1 percent, down by approximately 710 basis points from the third quarter of 2021. The drop in adjusted EBITDA margin was from FX, elevated energy costs in Europe and an increase in cost of aluminum materials.

Engineered Structures

Revenue in its Engineered Structures was $193 million, down 3 percent year-over-year, primarily from a drop in Boeing 787 production and a weaker defense aerospace market.

Adjusted EBITDA in the segment was $28 million, up 8 percent from the same reporting period of 2021. A boost in volume in the narrow body commercial aerospace market was the reason given for growth in adjusted EBITDA.

Adjusted EBITDA margin was 14.5 percent, up approximately 140 basis points from the third quarter of 2021.

Commercial aerospace market

The overall commercial aerospace market continues to recover well, led by the North American and European markets, with airline schedules and load factors increasing.

With the rebound in airline profits, it has resulted in new aircraft orders, specifically narrow-body aircraft, which have contributed significantly to the performance of HWM in recent quarters.

While the rebound in international travel has been modest in comparison to Europe and North America, there have been signs of strength in those markets, which has resulted in an incremental increase in production associated with those markets, especially in regard to Airbus A350 and the Boeing 787.

These trends point to a positive outlook for increasing aircraft build volume over the next two to three years. One headwind to watch closely is in relationship to supply constraints that have resulted in scarcity of some parts. Until there is more clarity concerning the supply chain, it won't be known whether Airbus (EADSF) will be able to reach its build levels of 55 per month for its A320, or Boeing (BA) will be able to reach build levels of 31 per month for its 737 MAX.

Commercial aerospace is going to be the key driver of performance over the next three years for HWM, with the defense aerospace market expected to return to growth sometime in mid-2023.

Growth in commercial aerospace is projected to increase revenue by approximately 20 percent in 2023, and continue to grow at above normal rates through 2025 before slowing down to an historical 4 percent growth rate.

Commercial aerospace has increased for six straight quarters, and based upon management commentary, should continue that performance over the next two to three years. That's significant because it now accounts for 47 percent of total revenue for HWM, although it remains below the pre-COVID level of 60 percent of total revenue. As its growth trajectory continues up over the next several years, it will probably come close to those levels again. If it's able to do so while growing its other segments, it'll be 60 percent of a bigger pie, which would be a strong catalyst for the stock.

Conclusion

Based upon current visibility, the next two to three years look very solid for HWM, and unless there are some unforeseen issues in the supply chain, it should enjoy consistent growth going forward.

The growth will be led by commercial aerospace, which should start to recapture a higher percentage of total revenue in the quarters and years ahead, which as mentioned above, if other segments help grow the overall revenue pie, will represent a solid growth catalyst in the future.

This is going to take time to unfold, and there is always the unknown concerning the level of response from consumers and businesses toward a weakening global economy. With the ongoing rebound in commercial aerospace in particular, the company will have to increase its inventory levels in order to meet growing demand. That could put some temporary pressure on margins and earnings, but should be offset some by scale. That should improve once initial spend provides the needed inventory. HWM has momentum on its side in the early 2023, and with commercial aerospace expected to grow at above-market levels for the next several years, it should provide some solid returns for shareholders, although its elevated share price at this time does concern me in regard to an entry point.

The company has been trading choppy over the last couple of years, and I think it'll continue to do so. After its recent big run up from about $30.50 to $41.02, I think it's due for a breather, and when it corrects again, it would be the time to take a serious look at taking a position in the stock for those that want exposure to the aerospace sector.

For further details see:

Howmet Aerospace: Commercial Aerospace Leading To Consistent Growth