HWM - Howmet Aerospace: Hard To Invest At 24x P/E

2023-05-10 12:28:41 ET

Summary

- HWM reported impressive 1Q23 results, with revenue growth of 21% to $1.6 billion, surpassing the consensus estimate of $1.48 billion.

- Engine Products and Fastener segments are expected to remain strong, with the Defense end market seeing huge demand for spare parts and the O&G industry holding strong.

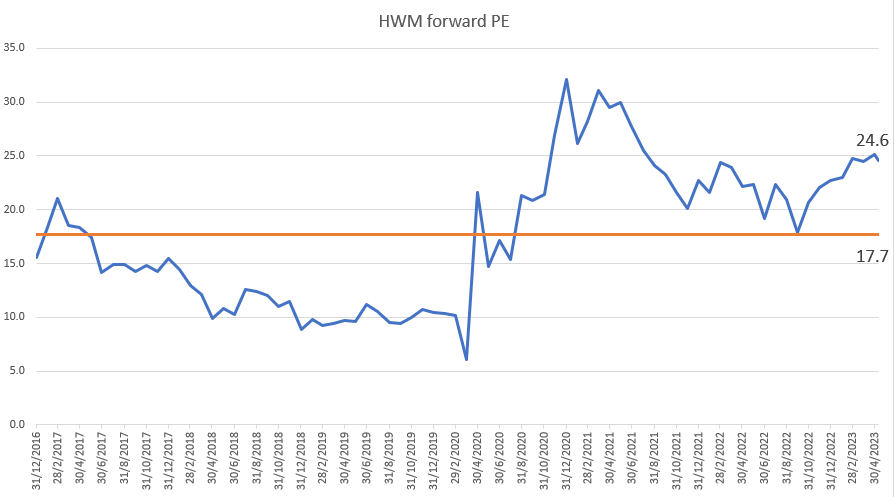

- The current valuation of HWM at 24x forward PE is significantly higher than its historical average of 17.6x. There is a risk of valuation reversion if expectations are not met.

Investment thesis

Howmet Aerospace (HWM) is a renowned manufacturer of a wide range of products and solutions, including investment castings for jet engines and industrial gas turbines, fasteners, forged components for jet engines and wheels, as well as various machined and forged aircraft parts. In the most recent quarter, HWM delivered exceptional 1Q23 results, surpassing consensus expectations in terms of both revenue and earnings. As a result, the company has revised its guidance for FY23, reflecting a positive outlook. The notable growth in revenue, which accelerated to 21% this quarter, and the consistent strength of the EBITDA margin are highly encouraging indicators. I also expect HWM to continue to gain prominence in terms of growth, particularly as industry giants Boeing and Airbus demonstrate a greater readiness to increase their production rates. This favorable development is likely to translate into increased demand for HWM's products, leading to improved top-line performance and enhanced margins and cash flow.

However, it should be noted that the current valuation of HWM stands at 24x forward PE, which is significantly higher than its historical average of 17.6x. I believe this valuation already incorporates all the anticipated earnings growth. Consensus estimates that HWM will achieve EPS of $2.07 in FY24, indicating a remarkable 52% growth. Consequently, there is a heightened risk associated with the company's performance, as any failure to meet these expectations could result in a downward revision of both valuation and estimates, potentially leading to a negative impact on the company's prospects. Considering these factors, I would recommend a hold rating for HWM.

1Q23 results

HWM announced impressive financial results, with a notable revenue growth of 21%, reaching $1.6 billion, beating the consensus estimate of $1.48 billion. The performance across various segments was as follows: Engine products demonstrated a growth of 9%, reaching $795 million; Fastening Systems exhibited a growth of 6%, reaching $312 million; Engineered Structures experienced a growth of 4%, reaching $207 million; and Forged Wheels displayed an impressive growth of 17%, reaching $289 million. Furthermore, the company achieved an overall adjusted EBITDA growth of 20%, amounting to $360 million, outperforming the consensus estimate of $336 million. These results reflect the strong operational performance and effective execution of HWM's business strategies.

Engine products and Fastener

The Engine Products segment saw sales grow 9% sequentially with 40% each from Defense and Industrial and others, with the remaining from Commercial Aeroplane. I believe the Defense end market will continue to remain strong for the foreseeable future, as the F-35 is currently seeing a huge demand for its spare parts (due to lack of supply). There are also nascent and fast growing segments that should extend the growth runway, such as drones and equipment in the space domain. As for Industrial and other sales, I also expect things to continue with the current trend as turbine demand continues to hold strong from the O&G industry, according to management. Lastly, HWM should continue to leverage the need for more spare parts in both narrowbody and widebody. As for Fastener, my expectations is that we should see profitability improve in the Fastener segment, as the decrease in margin this quarter was largely due to increase headcount and a slow widebody ramp. On the former, it is a fixed cost that needs to be recognized before revenue can kick in, while the latter is a matter of timing. To put in other words, cost is pulled forward but revenue has yet to be where it should be.

Margin

As HWM resumed hiring in anticipation of increased demand, overall margins dipped slightly to 22.5%. I think this is just a matter of timing, and it's better for HWM to take a hit to margins now and be prepared to meet the coming demand than to fall behind. However, there is also the possibility of over-hiring, as was the case in 2022 when expected construction volumes failed to materialize. While HWM has no say over the construction pace, I believe this time is different due to the improved likelihood of rate improvements in 2H23 and FY24.

Guidance

For FY23, management now expects a range of $6.2 to $6.325 billion in revenue, $1.4 to $1.435 billion in adj EBITDA, $1.65 to $1.70 in adj EPS, and $600 to $670 million in free cash flow. A key assumption that management made was that build rates will be lower than mentioned by the OEMs, which puts the guidance more towards the conservative end. If higher rates materialize, this could set up a scenario where HWM exceeds expectations and raises guidance for the next few quarters. This would certainly spin a positive earnings momentum and also the stock, possibly defying the high valuation that it is trading at today, for a short period of time.

Valuation

HWM historically trades at around 18x forward PE, and is now trading at almost 25x, a stark premium if we take into account the equity risk premium today. I believe the market has embedded a lot of optimism into the stock given the possible beat and raise scenario and increased visibility into growth. Investing in the stock today faces a huge risk of valuation reversion to mean, which could erase any short-term gains (if multiples reverse in a sharp manner).

{kind=link}

Conclusion

HWM exceeded expectations in 1Q23, reporting revenue growth of 21% to $1.6 billion, beating the consensus estimate of $1.48 billion. While HWM shows promising growth potential given the increased visibility into growth and OEM statements on build rates, I think the current valuation of 24x forward PE has already baked in this growth potential. As such, missing expectations could lead to downward revisions in valuation and estimates. Considering these factors, I would rather wait for valuation to come down and provide a better entry point.

For further details see:

Howmet Aerospace: Hard To Invest At 24x P/E