HWM - Howmet: Optimistic Aerospace Market For 2023 Beneficial Guidance And Cheap

2023-04-05 09:44:43 ET

Summary

- Howmet produces innovative lightweight metals engineering products and manufacturing solutions for various markets.

- If management is correct, and the build rate of Boeing 737-MAX and Airbus A350 remains as expected, FCF will likely trend north.

- I assumed that new products and new requirements from clients in the aerospace industry and adequate pricing strategies will likely bring FCF generation.

- Howmet remains a leader in most of its major markets. I believe that the stock price could be much higher than its current level.

Howmet Aerospace Inc. ( HWM ) is a market leader thanks to its innovation, manufacturing excellence, and the expertise accumulated before the separation from Arconic Corporation ( ARNC ) and Alcoa Corporation (AA). Considering the recent guidance and the beneficial information about the aerospace market for 2023, I believe that it is a must-follow stock. Even considering risks from competitors, lack of raw materials, or lack of suppliers, in my view, future FCF would justify a higher price mark.

Howmet Works For Several Industries, And Is Geographically Diversified

Howmet produces innovative lightweight metals engineering products and manufacturing solutions for various markets. Its focus is to offer differentiated solutions such as advanced cooling airfoils, coatings for extreme temperature applications, specially designed fasteners for lightweight composite airframe construction, lightweight aluminum commercial wheels, and other highly engineered products.

Its largest market is aerospace, which accounts for approximately 62% of its revenue, while the commercial transportation market accounts for approximately 23% of its revenue. It also has other industrial markets and reportable segments, such as engine products, fastening systems, engineering structures, and forged wheels. I believe that the number of products sold and the number of markets make the company quite diversified and resistant to periods of crisis.

Besides, Howmet's global presence in 20 countries, including China and Japan, indicates commitment to customer satisfaction, continuous improvement of its operations , and worldwide recognition.

Source: Annual Report

Howmet operates through four globally reportable segments: Engine Products, Fastener Systems, Engineered Structures, and Forged Wheels. Each segment focuses on a specific product line, and is designed to take advantage of the company's unique strengths and capabilities.

Source: Quarterly Presentation

2023 Guidance Includes FCF And EBITDA Growth

In my view, the guidance given for the year 2023 is beneficial, and I want to include it in the article. Revenue should stand at close to $6.1 billion. With an Adjusted EBITDA of $1.37 and EBITDA margin of 22%, the company is also expected to deliver FCF close to $615 million. My numbers are not far from the expectations of management, but I believe that investors may want to have a look at them.

Source: Quarterly Presentation

Among the comments given in the last quarterly report, I would highlight the following text about the beneficial expectations of the airline industry. In my view, if management is correct, and the build rate of Boeing (BA) 737-MAX and Airbus A350 remains as expected, FCF will likely trend north.

Turning to the full year 2023, currently, air travel conditions are very favorable, and airlines are experiencing strong growth, demanding new, more fuel-efficient aircraft. Underpinning full year 2023 guidance are assumed monthly build rates of approximately 30 for the Boeing 737-MAX and 53 to 54 for the Airbus A320 family, and approximately 30 Boeing 787 builds and 65 to 70 Airbus A350 builds for the year. Source: Howmet Aerospace Reports Fourth Quarter and Full Year 2022 Results

Assets

The balance sheet remained approximately close to what the company reported in 2021. Cash in hand, inventories, accounts receivables from customers, and total assets increased in 2022, implying that the business model is in a period of expansion. With that, goodwill declined a bit, and the total amount of property and equipment decreased too, which does not seem worrying in my view.

As of December 31, 2022, the company reported cash and cash equivalents of $791 million, receivables from customers worth $506 million, inventories close to $1.609 billion, and prepaid expenses and other current assets close to $206 million. Besides, total current assets stand at $3.143 billion, significantly larger than the total amount of current liabilities.

Properties, plants, and equipment stands at close to $2.332 million with goodwill of $4.013 billion and total assets of $10.255 billion. Finally, the asset/liability ratio stands at close to 2x, so I believe that the balance sheet stands in a good position.

Source: Annual Report

Liabilities: Investors Should Carefully Study The Total Amount Of Debt

Management reported accounts payable close to $962 million, accrued compensation and retirement costs close to $195 million, taxes, including income taxes of $48 million, and accrued interest payable of $75 million. Besides, total current liabilities stand at close to $1.482 billion.

The long-term debt, less amount due within one year stood at $4.162 billion with accrued pension benefits of $633 million, accrued other postretirement benefits of $109 million, and total liabilities worth $6.654 billion.

Source: Annual Report

The company did work on the total financial leverage as it stands at its minimum level in the last seven years. However, the total amount of debt is not small. I would expect some skepticism from a few investors.

Source: Ycharts

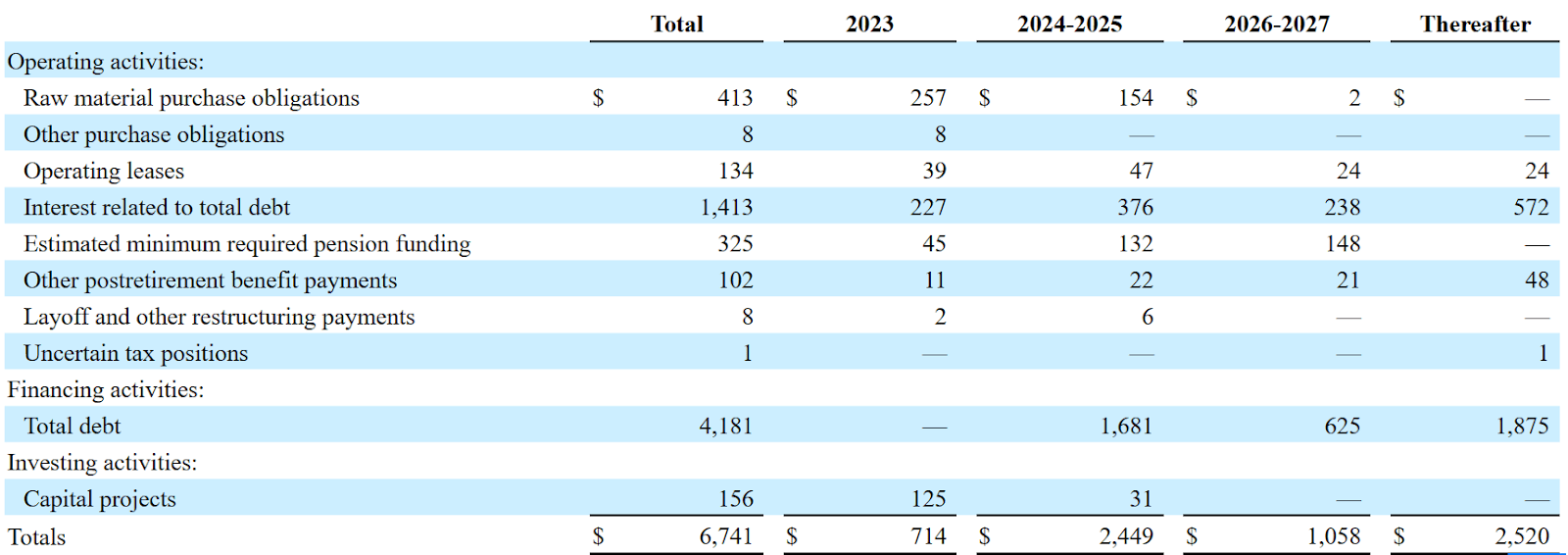

The list of contractual obligations includes payments in 2024-2025, 2026-2027, and thereafter. I believe that future cash flow from operations will likely be close enough to pay some payments. However, the company will likely need to negotiate with debt investors, or ask for more financing in my view.

{kind=link}

Assumptions In My DCF Model

I believe that the amount invested in research and development will likely bring further innovation and manufacturing excellence. The company invests in research and development to create cutting-edge products and advanced technologies. In addition, it is committed to continuous improvement and production efficiency to reduce costs and improve profitability. In my opinion, new products and further efficiency will likely bring FCF growth.

Besides, some of the teams that were working for Alcoa and Arconic are now working for Howmet. Hence, I believe that the know-how accumulated will likely help the company perform like it did before the separation.

Modernization of the commercial and defense platforms is driven by an array of challenging performance requirements. In line with these words, Howmet will likely aim to help its customers achieve greater fuel economies, reduced emissions, and passenger comfort. As a result, I believe that the company may successfully design pricing strategies, which may also enhance EBITDA margins and profitability. Additionally, I expect that Howmet may be able to increase its prices so that inflation may not be a problem.

In 2022, Sales increased 14% over 2021 primarily as a result of higher sales in the commercial aerospace market, an increase in material cost pass through of $225, and favorable product pricing of $67. Price increases are in excess of material and inflationary cost pass through to our customers. Source: Annual Report

Under my base case scenario, I assumed that Howmet will continue to reduce its debt obligations. In 2022, the company acquired a significant number of its own notes, and I expect the same to happen in 2023. Considering the current credit market, I think that further debt reductions will likely push the stock price quite a bit. Most analysts appear to be using a cost of capital close to 9.7%. If the WACC is reduced, future FCF generation would be worth much more, and the fair value of the company will likely increase.

Total debt of $4,162, a decrease of $70 from 2021, reflecting repurchases of $69 of the 5.125% Notes due October 2024. Source: Annual Report

Finally, I am quite optimistic about the stock repurchase program run by Howmet. I assumed that further repurchases of shares will likely bring demand for the stock. As a result, the cost of equity may decrease, which may multiply the fair value of the stock.

As of February 1, 2023, total share repurchase authorization available was approximately $947 million. Source: Howmet Aerospace Reports Fourth Quarter and Full Year 2022 Results

DCF Model

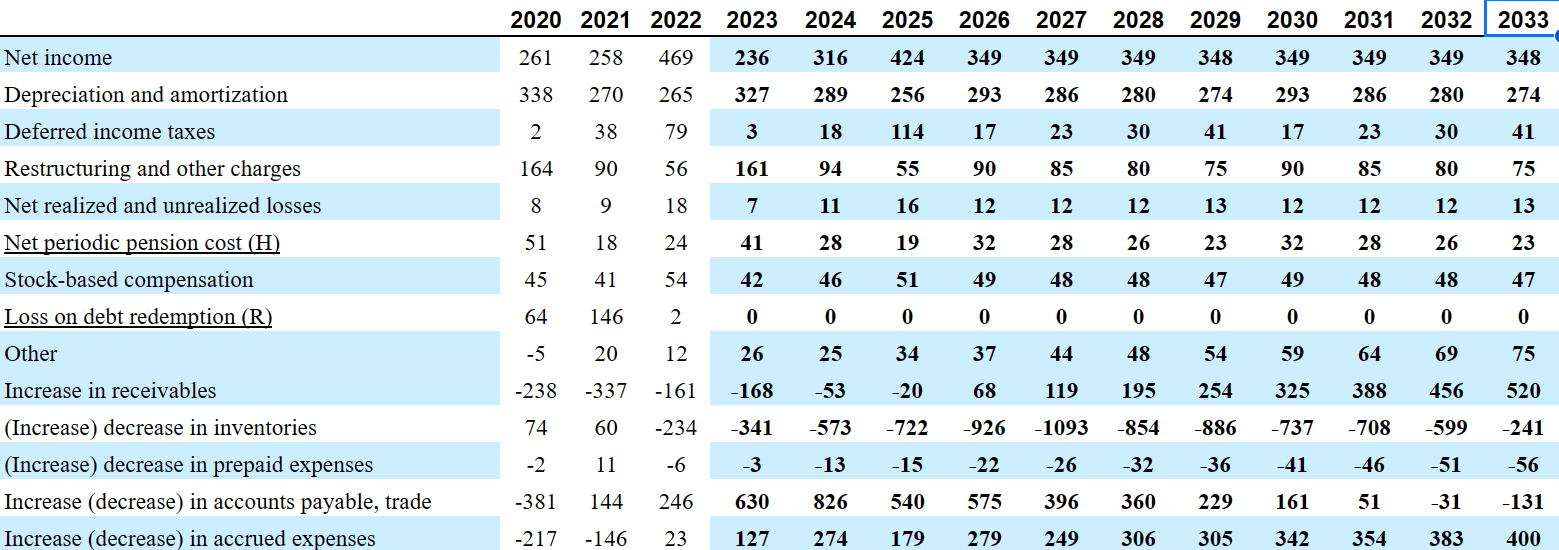

My forecasts include stable net income, CFO growth, and FCF driven by some decline in capital expenditures. I included somewhat stable restructuring charges, increases in accounts receivables, and some decreases in accounts payable. I believe that my numbers are not far from the figures reported in 2020, 2021, and 2022.

The numbers in my DCF model include 2033 net income of $348 million, depreciation and amortization of $273 million, deferred income taxes close to $40 million, restructuring and other charges of $75 million, and 2033 stock-based compensation of $47 million.

I also included 2033 increase in receivables close to $520 million, decrease in inventories of -$241 million, decrease in prepaid expenses of -$57 million, and increase in accounts payable of close to -$132 million.

Besides, I assumed an increase in accrued expenses of close to $400 million, increase in taxes, including income taxes of -$274 million, and pension contributions of close to $1032 million. Finally, I believe that cash provided from operations of $1759 million and capex close to -$78 million would make the free cash flow close to $1.682 billion.

{kind=link}

{kind=link}

With a WACC of 9.7% and an EV/FCF multiple of 29x, the enterprise value would be close to $23.386 billion. If we add cash and cash equivalents of $791 million, long-term debt of $4.162 billion, and accrued pension benefits worth -$633 million, the equity valuation would stand at $19.382 billion, and the fair price would be $47 per share.

{kind=link}

If the company successfully reduces its debt, or the stock repurchase program successfully lowers the cost of equity, we may see a WACC of close to 7%. Only by changing the WACC, I obtained a valuation of $63 per share.

{kind=link}

Among Competitors, Howmet Continues To Be A Leader, But There Are Some Risks

The company is subject to intense competition, however Howmet appears to be a leader in most of its major markets thanks to its advanced technology, manufacturing processes, and experience. Major competitors include companies such as VSMPO, Allegheny Technologies, Lisi Aerospace (LSIIF), and Aubert & Duval among others. In line with my previous words, I believe that readers may want to have a look at the following:

Despite intense competition, Howmet continues as a market leader in most of its principal markets. We believe that factors such as Howmet’s technological expertise, state-of-the-art capabilities, capacity, quality, engaged employees and long-standing customer relationships enable the Company to maintain its competitive position. Source: Annual Report

In the forged wheel division, the company competes with aluminum and steel wheel suppliers, and has seen increased competition from aluminum wheel suppliers from China, Taiwan, India, and South Korea. In addition, many of Howmet's customers have the ability to produce investment castings for their own use, adding further competition to the market.

Howmet faces various risks to its business, including the reliance on cyclical markets influenced by global economic conditions, which could adversely affect its business if there are interruptions to manufacturing operations. Additionally, reliance on a limited number of suppliers for essential materials, services and supply chain disruptions could have a significant adverse effect on the company’s business. In particular, a crisis in the aerospace industry will likely affect the revenue growth of Howmet, may push FCF down, and lead to stock price declines. The war in Ukraine and the implications in the energy markets may also have a dangerous impact on the price of raw materials. Besides, sanctions by certain governments, changes in regulations, import and export limits, and other market forces could deteriorate the margins of Howmet. The company was very clear about these risks in the last annual report.

The costs of certain raw materials (including, but not limited to, nickel, titanium, aluminum, cobalt, and rhenium) necessary for the manufacture of Howmet’s products and other manufacturing and operating costs are influenced by market forces and governmental constraints, including inflation, supply and demand, and shortages, and could be further influenced by export limits, sanctions, new or increased import duties, and countervailing or anti-dumping duties. Source: Annual Report

Finally, I believe that further increases in the interest rates or radical changes in the credit market may not help Howmet. If the company fails to finance its operations at competitive prices, in my view, net income growth will likely remain negative, and the stock price could fall.

Conclusion

Innovation and manufacturing excellence are key values ??for Howmet, which usually invests in research and development to create new products and advanced technologies. I assumed that new products and new requirements from clients in the aerospace industry and adequate pricing strategies will likely bring FCF generation. I am also quite optimistic about new changes in the balance sheet, debt reduction, and stock repurchase agreements, which may lower the cost of capital, and push the fair price up. Despite facing various risks to its business, including intense competition, Howmet remains a leader in most of its major markets. I believe that the stock price could be much higher than its current level.

For further details see:

Howmet: Optimistic Aerospace Market For 2023, Beneficial Guidance, And Cheap