ELV - Humana: Mr. Market Got This One Right

2023-08-03 08:55:11 ET

Summary

- Humana's shares spiked after exceeding analysts' expectations for Q2 revenue and adjusted earnings per share.

- The company's Insurance segment performed particularly well, and this trend looks set to continue.

- While there was a downward revision for guidance for the year, Humana's revenue and profits are performing well year over year and shares are reasonably priced.

One of the things that can be most exciting, but also that can be most frustrating, about the market is how fickle it can be. Legendary investor and investment educator Benjamin Graham, the primary instructor of Warren Buffett, even likened the market to a rather irrational or unstable individual known as Mr. Market. A great example of this instability can be seen by looking at the recent performance achieved by insurance behemoth Humana ( HUM ). Shares of the company spiked on August 2nd, closing up 5.6% after exceeding analysts' estimates regarding both revenue and adjusted earnings per share for the second quarter of the company's 2023 fiscal year. While this outperformance is definitely a reason to celebrate, it also came at the same time as a downward revision for guidance for the year as a whole. Normally, you would expect a downward revision for the year as a whole to more than overshadow the positive results for a single quarter. But as somebody who is mildly bullish on the company, I will take what I can get.

A briefer on Humana

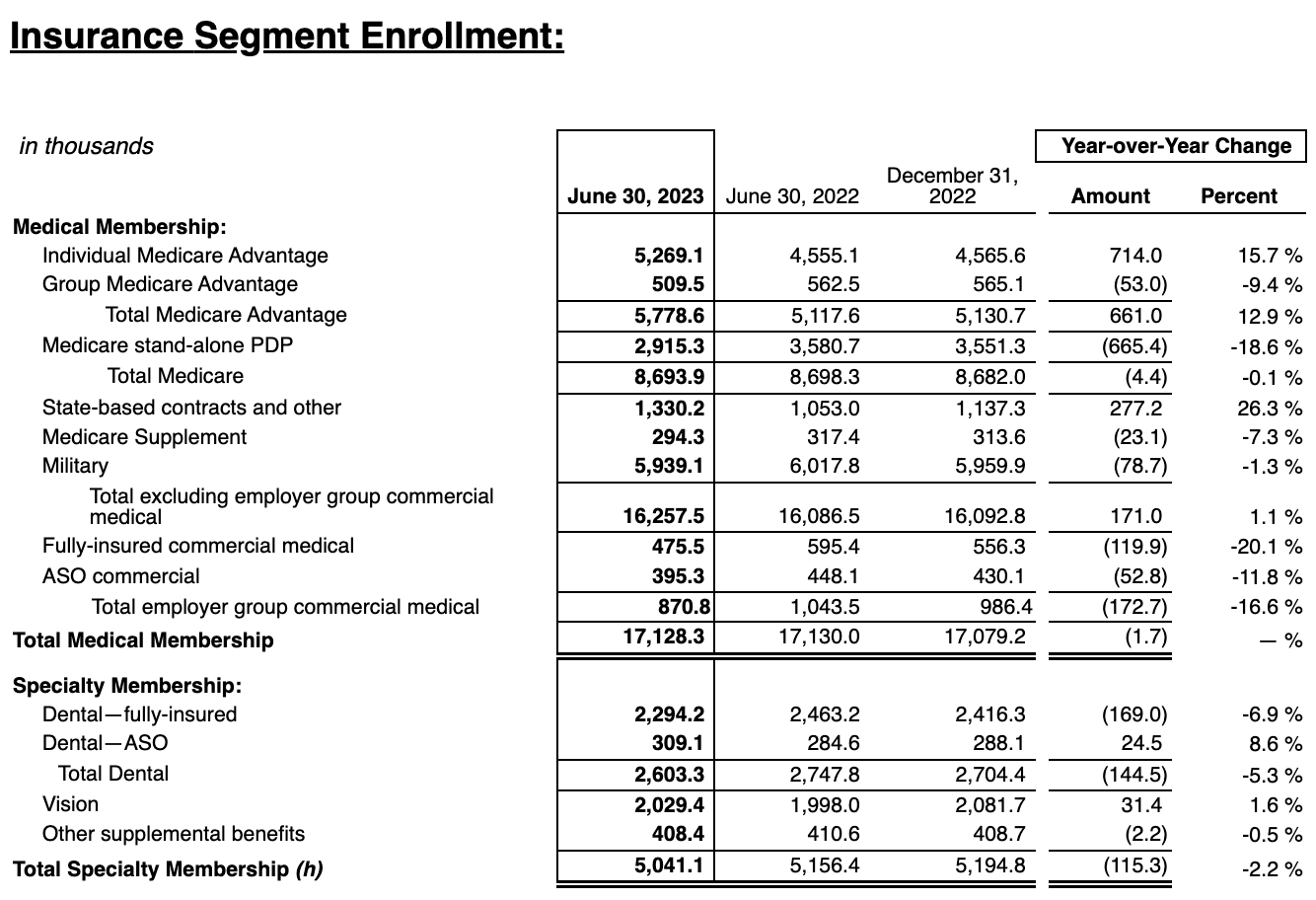

Before we focus on the most recent financial results reported by Humana, we should briefly cover what the company actually does for those who don't know. As I mentioned already, the business focuses on the insurance market. Specifically, its emphasis is on medical insurance, with the company having over 17 million members on its medical benefit plans on top of 5 million members in its specialty products. At its core, the company really focuses on servicing the U.S. government. In fact, during the 2022 fiscal year, 82% of the premiums and services revenue that it collected came from contracts with the federal government. Included in this number was 14% that was attributable to its individual Medicare Advantage contracts in Florida with the Centers for Medicare and Medicaid Services.

Operationally speaking, the company has two different segments. The first of these is the Insurance segment, which includes a wide variety of insurance products such as individual Medicare Advantage offerings, group Medicare Advantage offerings, Medicare Supplement programs, and more. This is the vast majority of what the company does, accounting for 95.8% of the business' overall sales. The other segment is known as CenterWell. And through it, the business offers pharmacy, provider services, and home solutions for its clients. It's also engaged in various strategic partners for activities like developing and operating senior focused primary care centers. It even has a mail order pharmacy business under this umbrella. In all, this unit is responsible for only about 4.2% of the company's revenue.

Diagnosing performance

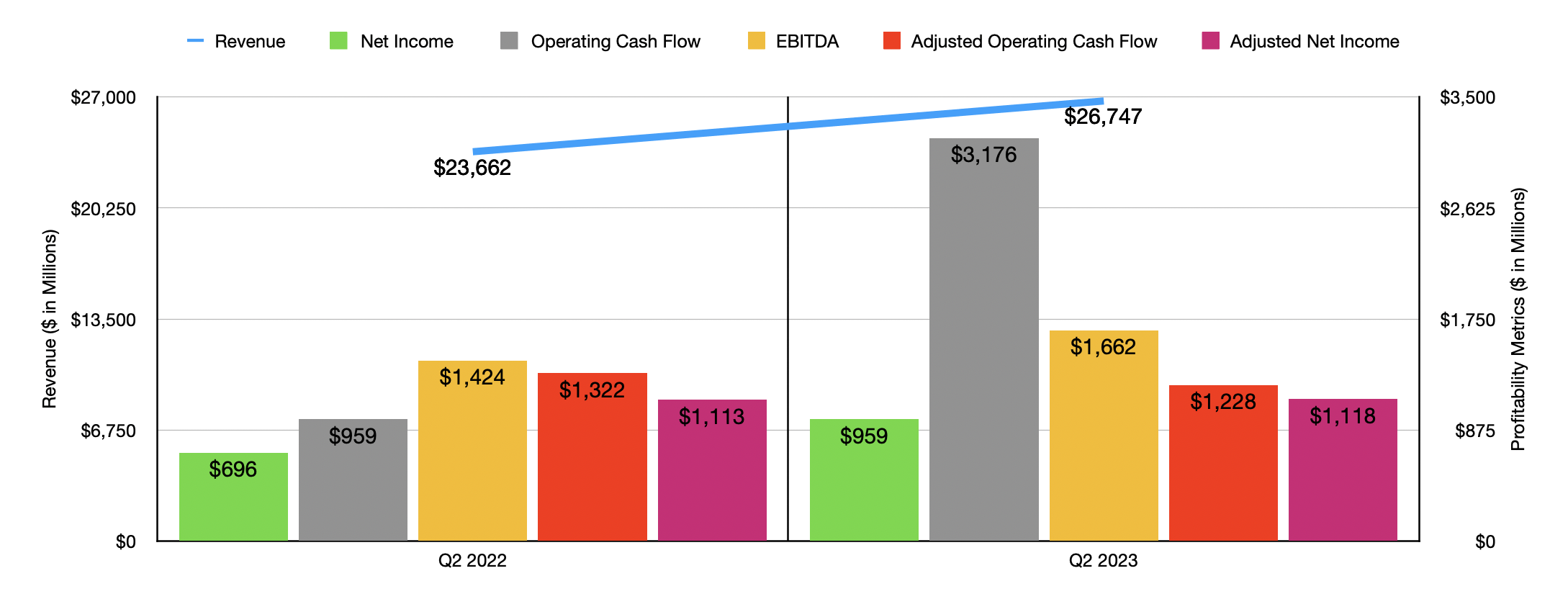

Before the market opened on August 2nd, the management team at Humana announced financial results covering the second quarter of the company's 2023 fiscal year. During that time, revenue came in at $26.75 billion. That represents an impressive 13% increase over the $23.66 billion the company reported one year earlier. In addition, it also exceeded analysts' expectations to the tune of $530.6 million. This sales increase came even as total services revenue dropped from $1.35 billion in the second quarter of 2022 to $978 million at the same time this year. This decline, management said, was largely the result of its sale of the 60% ownership that it owned of Gentiva Hospice that occurred in August of last year.

{kind=link}

Some of the increase in revenue came from investment income, with sales there jumping from $47 million to $274 million thanks to higher interest income on the debt securities that it owns and because of a decline in the value of certain securities that the company experienced last year. The big driver, however, involved growth in premiums. Premium revenue for the company spiked from $22.27 billion to $25.50 billion. This, according to management, can be chalked up to individual Medicare Advantage and state-based contracts membership growth, as well as higher premiums on a per-member basis. Individual Medicare Advantage membership jumped 714,000 from 4.56 million to 5.27 million. The company also saw nice growth of 277,200 under its Medicaid and other category of memberships. Total memberships, however, dipped about 1,700 to roughly 17.13 million under the medical category, while specialty membership numbers declined 115,300 from 5.16 million to 5.04 million.

{kind=link}

On the bottom line, the picture was a bit more complicated. Actual earnings per share of $7.66 exceeded the $5.48 reported one year earlier. However, for as strong as earnings growth was, it still missed analysts' expectations by $1.01 per share. If we adjust for certain things, however, earnings of $8.94 per share exceeded forecasts by $0.11 per share. The earnings per share for the company translated to $959 million for the second quarter this year, while for the same time last year the number was $696 million. The big divide between adjusted earnings and official earnings really involved two key things. The largest was a $0.72 per share hit associated with accruals for litigation costs. The second largest involved $0.44 per share in put/call valuation adjustments involving non consolidating minority interest investments. The important thing to take away from both of these is that they are one-time items that should not impact the company moving forward. And because adjusted earnings don't include any add backs associated with stock-based compensation or anything else like that, the adjusted earnings are probably a more appropriate measure of the company's value than the GAAP earnings are this quarter.

{kind=link}

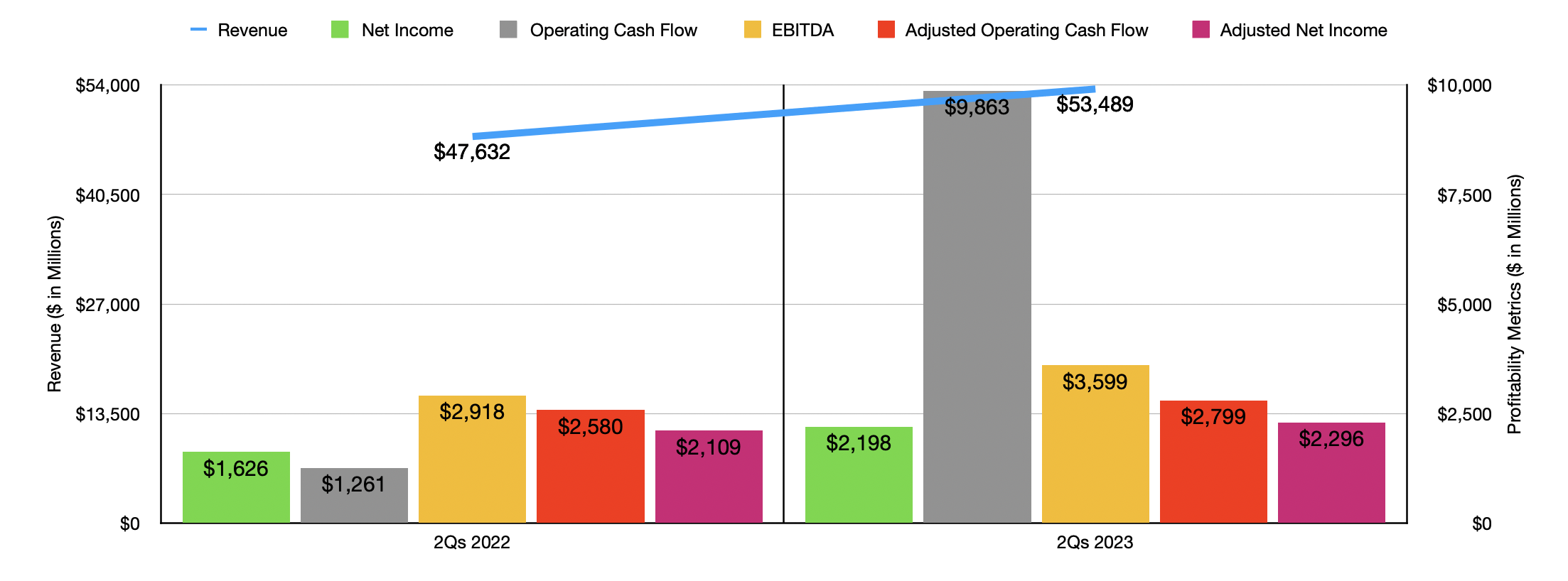

Other profitability metrics for the company were rather mixed. But for the most part, they were positive. Operating cash flow, for instance, shot up from $959 million to $3.18 billion. If we adjust for changes in working capital, however, we would see that the metric fell from $1.32 billion to $1.23 billion. Meanwhile, EBITDA for the company went from $1.42 billion to $1.66 billion. In the chart above, you can also see financial data covering the first half of 2023 compared to the same time of 2022. The overall trend is similar to what we get when looking at the second quarter alone on a year-over-year basis. This is definitely a positive for the company and its shareholders.

{kind=link}

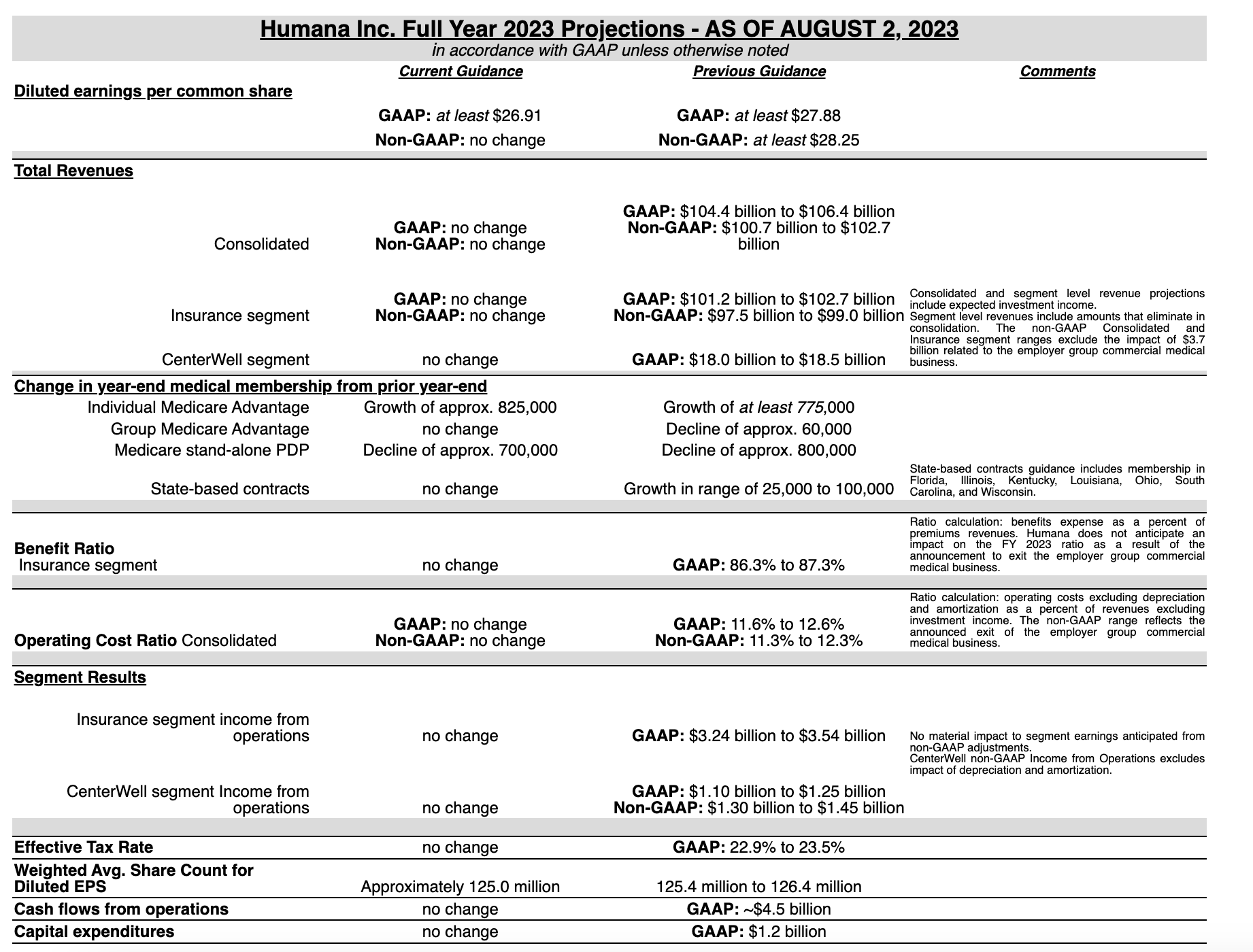

Now, when it comes to the rest of the fiscal year, management has provided a tremendous amount of guidance. Revenue associated with the Insurance segment of the company, for instance, should come in at between $101.2 billion and $102.7 billion, while revenue involving CenterWell should be between $18 billion and $18.5 billion. All combined, this should translate to sales of between $104.4 billion and $106.4 billion. That would represent a sizable increase over the $92.87 billion in sales the company generated in 2022. Even though I mentioned earlier in this article that management revised guidance lower, that was not the case with revenue. Interestingly, keeping guidance unchanged from when the company announced guidance previously in the first quarter is a little surprising since management is now forecasting more attractive results when it comes to the number of medical memberships that it has. Individual Medicare Advantage memberships are now forecasted to grow by 825,000 year over year. That compares to the 775,000 or more that management had forecasted previously. Meanwhile, Medicare stand-alone PDP membership is only expected to fall by 700,000. Prior guidance called for this to drop by 800,000.

Even though revenue figures look unchanged, the same cannot be said of profits. For the year, Humana should generate earnings per share of at least $26.91. This is down from the $27.88 minimum that management forecasted previously. The reason why the market took this news in a positive light is, I believe, because adjusted earnings per share are still forecasted to remain unchanged at $28.25. And as I mentioned previously, much of the change between adjusted earnings and official earnings involved one-time items. Management estimated that operating cash flow should be around $4.5 billion for the year, but they did not provide guidance when it came to EBITDA. My own estimate there calls for a reading of about $6.04 billion.

{kind=link}

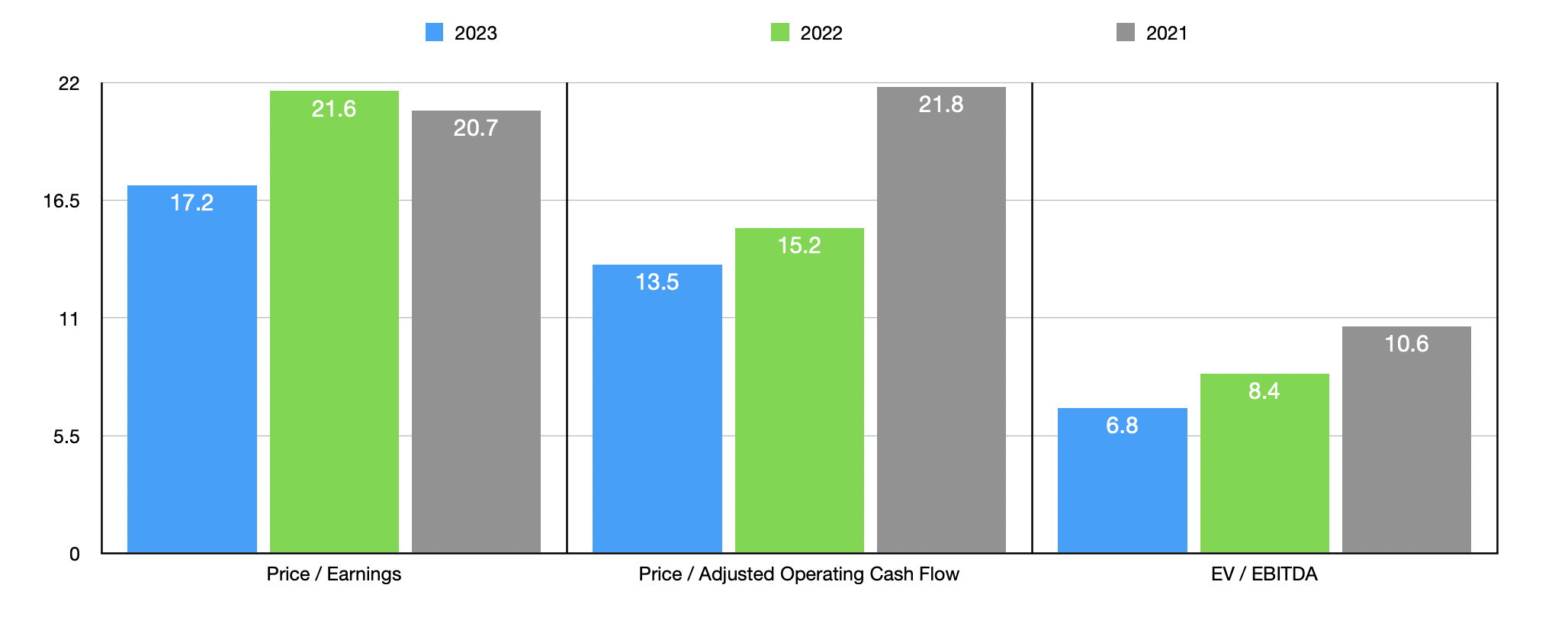

Taking these figures, it becomes easy to value the company. In the chart above, you can see how the stock is priced using estimates for 2023, as well as official numbers for both 2021 and 2022. As you can see, the stock does look cheaper on a forward basis. But for the sake of being conservative, I will instead, in the table below where I compare the enterprise to five similar firms, use the figures derived from 2022 results. In this case, three of the five companies end up cheaper than Humana when it comes to the price to earnings approach. This number increases to four of the companies when we use the price to operating cash flow approach. And when we use the EV to EBITDA approach, it drops to two. Even if we were to use the forward estimates, the company's rank when it comes to the price to operating cash flow multiple would remain unchanged, while the ranking in the EV to EBITDA approach would decline by one and the ranking under the price to earnings approach would drop by two.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Humana |

| 21.6 |

| 15.2 |

| 8.4 |

| Centene ( CNC ) |

| 13.9 |

| 4.4 |

| 5.9 |

| Molina Healthcare ( MOH ) |

| 19.3 |

| 12.3 |

| 7.2 |

| Elevance Health ( ELV ) |

| 17.7 |

| 9.6 |

| N/A |

| Progyny, Inc. ( PGNY ) |

| 95.1 |

| 36.3 |

| 92.1 |

| UnitedHealth Group ( UNH ) |

| 22.6 |

| 11.6 |

| 14.4 |

Takeaway

From what I can tell, Mr. Market got this right, even though the initial news regarding the company may have indicated otherwise. Revenue and profits are performing nicely year over year and shares, while not exactly cheap, do look affordable when you consider the high quality that an operation like this brings to the table. Given these factors, I feel comfortable rating Humana a soft 'buy' at this time.

For further details see:

Humana: Mr. Market Got This One Right