HURC - Hurco: Strong Enough To Endure Current And Potential Headwinds

2023-07-26 22:51:54 ET

Summary

- The share price is trading 56% below all-time highs due to declining revenues and margin contraction.

- Orders have increased slightly during the past quarter, suggesting some demand stabilization.

- Margins have recently declined due to weaker volumes and inflationary pressures, and cash from operations is not enough to cover capital expenditures and dividend payments.

- The company has a debt-free balance sheet with $52 million in cash and equivalents and $176 million in inventories, which means it's prepared to withstand current and potential headwinds for a long time.

- This represents a good opportunity to start averaging down as the company operates in a highly cyclical industry.

Investment thesis

Investors remain cautious regarding Hurco Companies ( HURC ) as the share price currently trades 56% below all-time highs. Revenues have declined for the last three quarters as it has a very high cyclical component and, in addition, inflationary pressures and lower volumes are causing a further contraction in margins, which could end up being reflected in the balance sheet if the situation keeps worsening in the short and medium term.

Despite this, the balance sheet is very robust as the company is debt-free and holds $52.16 million in cash and equivalents and $175.83 million in inventories, so the company, which has been in business for 55 years, is well prepared to overcome significant headwinds for a long time. Furthermore, current headwinds are, in my opinion, likely of a temporary nature as they are directly linked to the current macroeconomic landscape. Still, it is the cyclical component of its operations that makes Hurco Companies a particularly risky investment, so investors interested in obtaining capital gains once the current prospects improve should, in my opinion, buy shares periodically if the price keeps declining (that is, averaging down) in order to get lower average purchase prices as the share price could continue declining given the current complex macroeconomic context.

A brief overview of the company

Hurco Companies is a global manufacturer of computerized machine tools, including vertical machining centers (mills) and turning centers (lathes), for metal cutting companies. The company also provides machine tool components and automation integration equipment and solutions. It was founded in 1968 and its market cap currently stands at $147 million, which means it's a micro-cap company.

Hurco Companies (2022 Annual Report)

{kind=link}

The company pays growing dividends to investors and has recently started performing share buybacks as the cash payout ratio is relatively low. But in my opinion, Hurco is not a good candidate for a buy-and-hold strategy, but rather a company that should be bought during hard times in order to be sold when its prospects improve. In this regard, the company operates in a highly cyclical industry, and if one looks at the historical price of its shares, one will realize how the company's highly cyclical component is reflected in the ups and downs over the years.

Currently, shares are trading at $22.39, which represents a 55.66% decline from recent highs of $50.50 on May 30, 2018, as revenue has shown negative year-over-year growth rates for three consecutive quarters while inflationary pressures and lower volumes are causing significant margin contraction at a time marked by growing fears of a potential recession as a consequence of recent interest rate hikes. In addition, the highly cyclical nature of the company suggests that an economic downturn would have a particularly significant impact on Hurco's operations, so investors remain on the sidelines as the short and medium term is full of uncertainties.

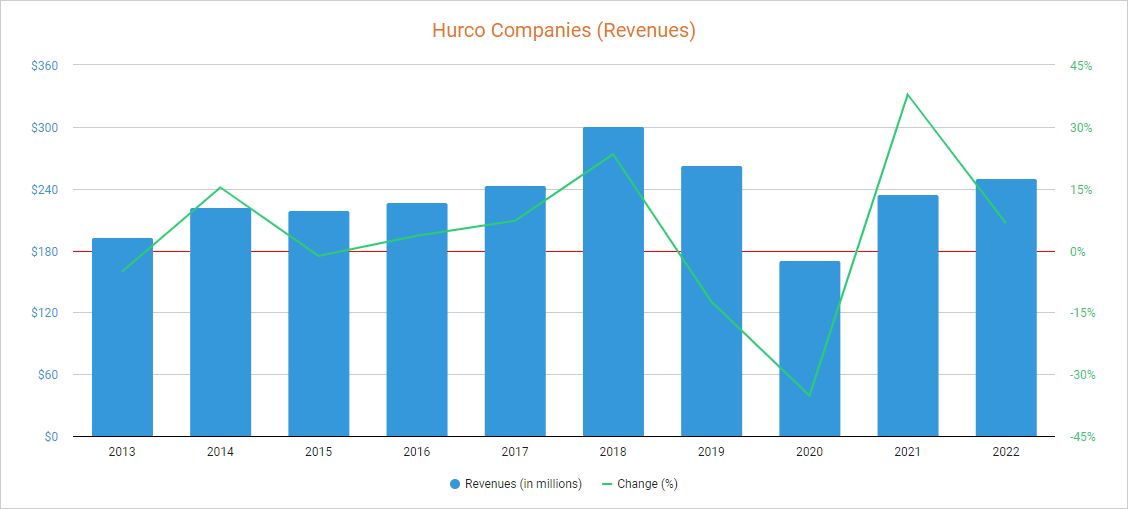

Revenues are showing signs of fatigue, but orders are starting to increase

The company's operations have been suffering in recent years as revenues declined by 12.40% during fiscal 2019. The coronavirus pandemic crisis caused another negative impact as revenues declined by a further 35.22% during fiscal 2020, but they partially recovered in subsequent years as they increased by 37.84% in fiscal 2021 and by a further 6.64% in fiscal 2022. Using fiscal 2022 as a reference, 50% of revenues are generated through operations in Europe, whereas 38% take place in the Americas, and 12% in Asia Pacific.

Hurco Companies revenues (Seeking Alpha)

{kind=link}

But despite recent revenue growth, the company reported an 8.00% decline year over year during the fourth quarter of fiscal 2022, an 18.25% decline (also year over year) during the first quarter of fiscal 2023, and a 14.34% decline during the second quarter. Nevertheless, orders increased by 2% year over year during the second quarter of fiscal 2023 (and 13% sequentially), which means demand is showing signs of stabilization. Still, investors remain pessimistic as margins remain depressed and the current macroeconomic context is very complex as recent interest rate hikes could cause an economic contraction and lower orders in the medium term.

The recent partial recovery in revenues (regarding fiscal 2021 and 2022) coupled with a steady share price decline has caused a sharp drop in the P/S ratio to 0.643, which means the company currently generates annual revenues of $1.56 for each dollar held in shares by investors.

This ratio is 30.41% lower than the average of the past 10 years and represents a 54.30% decline from decade-highs of 1.407 reached in 2021. This decline shows growing pessimism among investors as they are placing significantly less value on the company's sales not only due to weak demand and an uncertain macroeconomic landscape but also as a consequence of a weaker capacity of converting said sales into actual cash as profit margins are suffering a significant contraction.

Inflationary pressures and lower volumes are negatively impacting profit margins

Overall, the company has historically achieved relatively stable gross profit margins of over 25% and EBITDA margins of over 10%, but the coronavirus pandemic crisis and global restrictions derived from it caused a significant decline that pushed the EBITDA margin to negative territory. After a significant recovery in 2021, inflationary pressures and weak volumes are now causing further margin declines as the trailing twelve months' gross profit margin currently stands at 24.94% and the EBITDA margin at 4.61%.

The second quarter of fiscal 2023 was especially weak as the company reported a gross profit margin of 23.83%, and the EBITDA margin suffered even more as it stood at 3.29%, which explains current pessimism among investors. In this sense, the current macroeconomic landscape represents a swampy territory for the company's operations, whose cyclical component is very high. That is why it is expected that the company will have to make use of the resources available on the balance sheet (cash and inventories) to navigate current and potential headwinds. But luckily, the balance sheet is very robust and should allow Hurco to ride those headwinds for a very long time.

The balance sheet is very robust

Hurco enjoys a debt-free balance sheet, which significantly reduces the risk of a negative cycle leading to long-term viability issues. In addition, the company enjoys a very high cash pile as cash and equivalents currently stands at $52 million. Furthermore, the low demand of the last few quarters has caused a significant increase in inventories to stratospheric levels at $176 million, which is higher than the company's market cap itself as the company could have serious trouble emptying those inventories as demand remains weak.

In this sense, the company's balance sheet is very robust and should allow it to navigate inflationary pressures, weaker demand, and even a potential recession for quite a long time as it has no interest expenses to meet at the end of each period. Furthermore, dividends paid and capital expenditures represent a very low percentage of that cash (and of historical cash from operations), so cash and equivalents should decline relatively slowly as the company keeps enduring current (and potential) headwinds.

The dividend appears relatively safe, but I don't recommend investing with a dividend growth perspective

The company has been paying growing dividends since 2013, which means dividend payments are relatively recent. The latest dividend raise was announced in March 2023 when the management decided to increase it by 6.67% to $0.16 per share and quarter.

Using the current share price of $22.39 as a reference, the dividend yield currently stands at 2.86%, which is relatively generous considering that the company has historically allocated a very small portion of cash from operations to cover it. In the following table, I have calculated the sustainability of the dividend in the long term by calculating which percentage of cash from operations has been used to cover dividend payments.

| Fiscal year |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| $16.3 |

| $28.8 |

| -$6.7 |

| $30.4 |

| $21.0 |

| -$6.4 |

| $10.9 |

| $32.2 |

| -$4.0 |

| Dividends paid (in millions) |

| $1.7 |

| $2.0 |

| $2.3 |

| $2.6 |

| $2.9 |

| $3.2 |

| $3.4 |

| $3.7 |

| $3.9 |

| Cash payout ratio |

| 10.43% |

| 6.94% |

| - |

| 8.55% |

| 13.81% |

| - |

| 31.19% |

| 11.49% |

| - |

As one can see in the table above, annual dividends paid of $4 million represent a relatively small portion of the company's cash from operations (in normal years), which makes the dividend quite sustainable in the long run. Cash from operations was negative at -$4.0 million in fiscal 2022, but inventories increased by $8 million and accounts payable declined by $8.2 million while accounts receivable declined by just $3.5 million. As for the past quarter, cash from operations was $1.0 million, inventories increased by $7.2 million, and accounts receivable increased by $0.1 million, but accounts payable also increased significantly by $7.2 million, which means the company is starting to make use of cash and equivalents to offset current margin contraction as it not only has to cover dividend payments of around $4 million per year but also annual capital expenditures of around $2.5 million.

In this regard, cash and equivalents of $52 million is enough to cover these two expenses for a long time (and keep raising inventories if the management fails to empty them), but still, investors should not forget that the company's high cyclical component could eventually force it to cut (or cancel) the dividend during any economic downturn. For this reason, I do not consider Hurco to be a good candidate for dividend growth investors, but rather as a cyclical company with high price volatility. In this sense, dividends and share buybacks should help to obtain a higher total return once the share price reflects more optimism, although the management could decide to cancel them if cash and equivalents continue to decline for much longer.

Share buybacks at the right time

In March 2020, the company announced a share repurchase program of up to $7 million, and an identical program was also announced in March 2021. During the past 5 years, the total number of shares outstanding declined by 3.79%, which means each share now represents a bigger slice of the company.

Although this is a very modest reduction, I believe that high cash and equivalents on the balance sheet and increasingly lower share prices could put pressure on the management to continue performing share buybacks in the short and medium term, which should help stabilize the share price in the medium and long term and increase the total shareholder returns once current pessimism eases.

Risks worth mentioning

In my opinion, Hurco Companies is a company with a high-risk profile, despite its healthy balance sheet and relatively low cash payout ratio, due to the highly cyclical nature of the industry in which it operates. For this reason, I would like to highlight the risks that I consider to be the most significant in the short and medium term.

- A potential recession as a consequence of recent interest rate hikes could have a material impact on the company's operations, which would lead to a weakening balance sheet due to lower cash from operations and, as a consequence, a further decline in the share price.

- If demand remains depressed, profit margins could remain at low levels as a consequence of lower volumes (and thus higher unabsorbed labor), which would keep cash from operations low.

- The company could have serious difficulties emptying its inventories as demand remains weak despite a recent increase in orders. In this sense, it seems that the only way to empty inventories profitably is by reducing the company's production capacity.

- As the current macroeconomic landscape is negative for the company's operations, the management could decide to cut (or even cancel) the dividend if current and potential headwinds remain for too long.

- Although the current share price represents a good opportunity to buy back the company's shares at low prices compared to recent years, a further contraction in profit margins could make this practice risky as cash and equivalents are at risk of drying up if headwinds last for too long.

Conclusion

Despite the fact that orders have increased in the last quarter, revenues have been declining for three consecutive quarters, and considering the impact that lower demand is currently having on profit margins, investors prefer to remain cautious as the share price has declined by 53% from all-time highs.

Cash and equivalents of $52.16 million and inventories of $175.83 million should allow the company to operate with depressed margins for a long time, so the company should be prepared to withstand current headwinds and even a potential recession for a long time, especially considering that there are no interest expenses thanks to a debt-free balance sheet. Still, cash from operations is very weak as a consequence of said margin contraction, so the company is making use of cash and equivalents to cover dividends and capital expenditures. Also, it does not seem that emptying inventories will actually be possible until demand picks up again as the company would have to drastically cut production capacity to achieve this. Nevertheless, the fact that the company enjoys a robust balance sheet gives it the opportunity to continue making share buybacks at lower share prices in order to keep reducing the total number of outstanding shares, which should help achieve some stabilization of the share price in the long run. But despite this, I recommend investing with caution by using a dollar-cost average strategy as the current macroeconomic landscape is very volatile and the company's cyclical nature is very high.

Considering the current 30.41% decline in the P/S ratio from the average of 0.924 of the past decade, I consider that expecting a 40% appreciation from current share price levels is quite realistic, so I think the company should have no serious problems reaching a share price of over $31 in the medium to the long term. Meanwhile, share buybacks should help in eventually reaching that price level and dividends should increase shareholders' total return once it's achieved.

In my opinion, the weight of the risks and the rewards are currently similar on the scale, but the fact that the company is well prepared to face short and medium-term adversities mean that those investors who average down cautiously and wait patiently will see their patience rewarded once the macroeconomic landscape offers more optimism to investors as current headwinds are directly linked to it.

For further details see:

Hurco: Strong Enough To Endure Current And Potential Headwinds